ChatPlus: Up-Market AI Pivot Across Japan as Upsell Metrics Signal 36.1% Operating Margins

Date : 2026-06-13

Reading : 84

ChatPlus must look beyond its 36.3% top-line growth to understand its core structural catalyst: Japan’s impending "2025 Cliff" and chronic demographic labor shortages. By aggressively cannibalizing lower-tier legacy accounts to force enterprise migrations toward its premium generative AI product, the company is extracting exceptional price-mix variance. However, while 105.9% operating cash flow growth signals pristine capital efficiency, a hyper-lean 22-person organization heavily dependent on external U.S. application programming interfaces (APIs) exposes an underlying vulnerability to foreign exchange volatility.

Figure ChatPlus Strategic Assessment: Scaling High-Value Enterprise Al

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

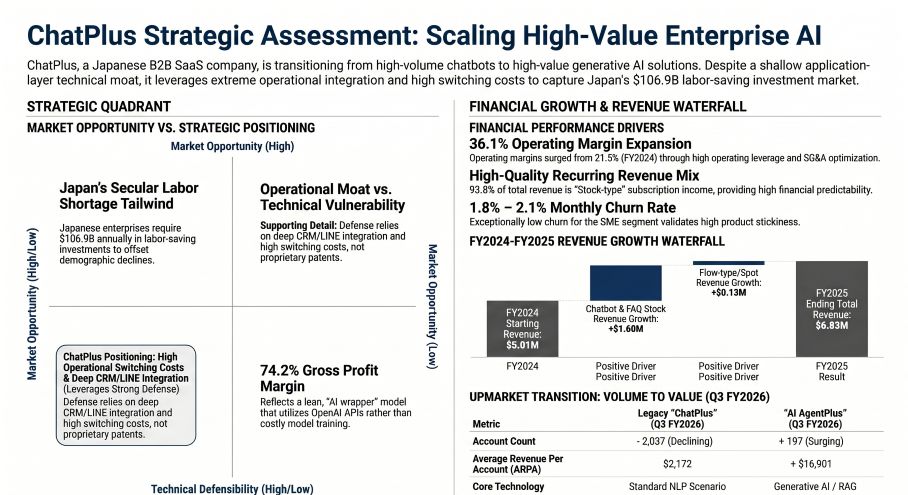

ChatPlus operates a highly concentrated, single-segment B2B SaaS model. A Forensic Analysis of the transition from FY2024 to FY2025 reveals deliberate strategic attrition at the volume level, engineered to drive immense pricing leverage and Annual Recurring Revenue (ARR) expansion.

* Top-Line & Quality of Revenue: Total FY2025 revenue reached $6.83 million (JPY 1,021 million), a 36.3% YoY increase. The revenue mix is exceptionally high-quality, with 93.8% generated from "Stock-type" recurring subscriptions. Total ARR closed FY2025 at $7.20 million.

* Unit Economics & ARPA Expansion: The company is intentionally shedding its legacy $13.24/month basic accounts. Basic "ChatPlus" accounts declined from 2,199 to 2,037, while high-tier "AI AgentPlus" accounts surged from 44 to 197 (Q1 FY24 to Q3 FY26). Consequently, blended Average Revenue Per Account (ARPA) expanded by 85% to $3,556, with the AI tier commanding an ARPA of $16,901. Monthly churn remains fixed at an elite 1.8% to 2.1%.

* Operating Leverage Profile: Structural unit economics align favorably with top-quartile enterprise SaaS. Cost of Sales growth (75.5%) was easily absorbed, yielding a Gross Profit Margin of 74.2%. Operating Profit surged 128.8% to $2.47 million, delivering a 36.1% Operating Margin.

* Cash Conversion & Internal Capital Allocation: Operating Cash Flow (OCF) grew 105.9% to $2.74 million. This liquidity is driven by a highly favorable negative working capital cycle: 39.1% of SaaS contracts are billed annually in advance, inflating contract liabilities (unearned revenue) by $344,700 and effectively allowing customers to fund operations pre-service delivery.

Cloud Supply Chain & Geo-Economic Moats

While ChatPlus acts as an enterprise software provider, a physical supply chain audit reveals absolute reliance on U.S.-based cloud and algorithmic infrastructure to serve its domestically concentrated client base (Japan accounts for >90% of revenue).

* Vendor Concentration Risk: The platform's physical hosting is exclusively anchored in NASDAQ: AMZN (Amazon Web Services) data centers, while its core "AI AgentPlus" engine operates strictly via OpenAI’s GPT-4o APIs.

* The Foreign Exchange (FX) Squeeze: This supply chain creates an asymmetrical macroeconomic vulnerability. Revenue is earned in Japanese Yen (JPY), but tier-1 infrastructure costs are paid in U.S. Dollars (USD). Sustained JPY depreciation acts as a direct headwind to Gross Margins.

* Enterprise Security Compliance Moat: To defend against public AI data leakage concerns, ChatPlus secured a "Zero Data Retention Amendment" directly with OpenAI. This contract structurally prohibits OpenAI from utilizing ChatPlus’s enterprise client data to train external Large Language Models (LLMs), granting the company a vital regulatory compliance moat required for Japanese municipal and government procurement.

HDIN Institutional Perspective

Challenge to the Narrative: While the prospectus positions ChatPlus as a cutting-edge AI innovator paving a path toward a "fully automated society," an audit of internal capital allocation definitively challenges this "deep tech" classification. In FY2025, total expensed R&D was a mere $41,499—representing an anemic 0.6% of total revenue.

ChatPlus is fundamentally an "Application Layer" AI wrapper, not a foundational model architect. Its proprietary anti-hallucination technology relies on basic Retrieval-Augmented Generation (RAG) rather than highly defensible algorithmic intellectual property (Patent book value sits at a negligible $1,136). The Street should not price ChatPlus as a deep-tech AI firm.

The True Value Driver: Instead, the company must be valued as an elite, high-touch sales and Customer Success organization. Its actual moat is operational entrenchment. By integrating directly into legacy CRMs and platforms like LINE/WhatsApp, ChatPlus engineers exceptionally high switching costs. However, institutional investors modeling FY2026 free cash flow per share must aggressively discount for the 14.0% equity dilution overhang stemming from unexercised stock options—a costly mechanism utilized to attract talent to an otherwise hyper-lean 22-person corporate structure.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure ChatPlus Strategic Assessment: Scaling High-Value Enterprise Al

Forensic Financials & Segmental InventoryChatPlus operates a highly concentrated, single-segment B2B SaaS model. A Forensic Analysis of the transition from FY2024 to FY2025 reveals deliberate strategic attrition at the volume level, engineered to drive immense pricing leverage and Annual Recurring Revenue (ARR) expansion.

* Top-Line & Quality of Revenue: Total FY2025 revenue reached $6.83 million (JPY 1,021 million), a 36.3% YoY increase. The revenue mix is exceptionally high-quality, with 93.8% generated from "Stock-type" recurring subscriptions. Total ARR closed FY2025 at $7.20 million.

* Unit Economics & ARPA Expansion: The company is intentionally shedding its legacy $13.24/month basic accounts. Basic "ChatPlus" accounts declined from 2,199 to 2,037, while high-tier "AI AgentPlus" accounts surged from 44 to 197 (Q1 FY24 to Q3 FY26). Consequently, blended Average Revenue Per Account (ARPA) expanded by 85% to $3,556, with the AI tier commanding an ARPA of $16,901. Monthly churn remains fixed at an elite 1.8% to 2.1%.

* Operating Leverage Profile: Structural unit economics align favorably with top-quartile enterprise SaaS. Cost of Sales growth (75.5%) was easily absorbed, yielding a Gross Profit Margin of 74.2%. Operating Profit surged 128.8% to $2.47 million, delivering a 36.1% Operating Margin.

* Cash Conversion & Internal Capital Allocation: Operating Cash Flow (OCF) grew 105.9% to $2.74 million. This liquidity is driven by a highly favorable negative working capital cycle: 39.1% of SaaS contracts are billed annually in advance, inflating contract liabilities (unearned revenue) by $344,700 and effectively allowing customers to fund operations pre-service delivery.

Cloud Supply Chain & Geo-Economic Moats

While ChatPlus acts as an enterprise software provider, a physical supply chain audit reveals absolute reliance on U.S.-based cloud and algorithmic infrastructure to serve its domestically concentrated client base (Japan accounts for >90% of revenue).

* Vendor Concentration Risk: The platform's physical hosting is exclusively anchored in NASDAQ: AMZN (Amazon Web Services) data centers, while its core "AI AgentPlus" engine operates strictly via OpenAI’s GPT-4o APIs.

* The Foreign Exchange (FX) Squeeze: This supply chain creates an asymmetrical macroeconomic vulnerability. Revenue is earned in Japanese Yen (JPY), but tier-1 infrastructure costs are paid in U.S. Dollars (USD). Sustained JPY depreciation acts as a direct headwind to Gross Margins.

* Enterprise Security Compliance Moat: To defend against public AI data leakage concerns, ChatPlus secured a "Zero Data Retention Amendment" directly with OpenAI. This contract structurally prohibits OpenAI from utilizing ChatPlus’s enterprise client data to train external Large Language Models (LLMs), granting the company a vital regulatory compliance moat required for Japanese municipal and government procurement.

HDIN Institutional Perspective

Challenge to the Narrative: While the prospectus positions ChatPlus as a cutting-edge AI innovator paving a path toward a "fully automated society," an audit of internal capital allocation definitively challenges this "deep tech" classification. In FY2025, total expensed R&D was a mere $41,499—representing an anemic 0.6% of total revenue.

ChatPlus is fundamentally an "Application Layer" AI wrapper, not a foundational model architect. Its proprietary anti-hallucination technology relies on basic Retrieval-Augmented Generation (RAG) rather than highly defensible algorithmic intellectual property (Patent book value sits at a negligible $1,136). The Street should not price ChatPlus as a deep-tech AI firm.

The True Value Driver: Instead, the company must be valued as an elite, high-touch sales and Customer Success organization. Its actual moat is operational entrenchment. By integrating directly into legacy CRMs and platforms like LINE/WhatsApp, ChatPlus engineers exceptionally high switching costs. However, institutional investors modeling FY2026 free cash flow per share must aggressively discount for the 14.0% equity dilution overhang stemming from unexercised stock options—a costly mechanism utilized to attract talent to an otherwise hyper-lean 22-person corporate structure.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."