Aisan Industry: CapEx Reallocation Near India and Kentucky as Working Capital Stretch Signals FCF Friction

Date : 2026-06-13

Reading : 69

Aisan Industry’s FY2026 filings reveal a calculated managed-decline strategy, aggressively extracting cash from legacy Internal Combustion Engine (ICE) assets to fund zero-emission mobility. While the $50.1 million acquisition of Trice Corporation secures critical motor component IP, institutional LPs must weigh this against a deteriorating Free Cash Flow profile (-$29.2 million) and elongated cash conversion cycles. The company is actively migrating ICE capacity to the Aisan Industry India and Kentucky facilities, masking the acute margin friction caused by domestic wage inflation severely outpacing revenue-per-employee growth.

Figure Aisan industry Vision 2030: Navigating the Electrification Pivot

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

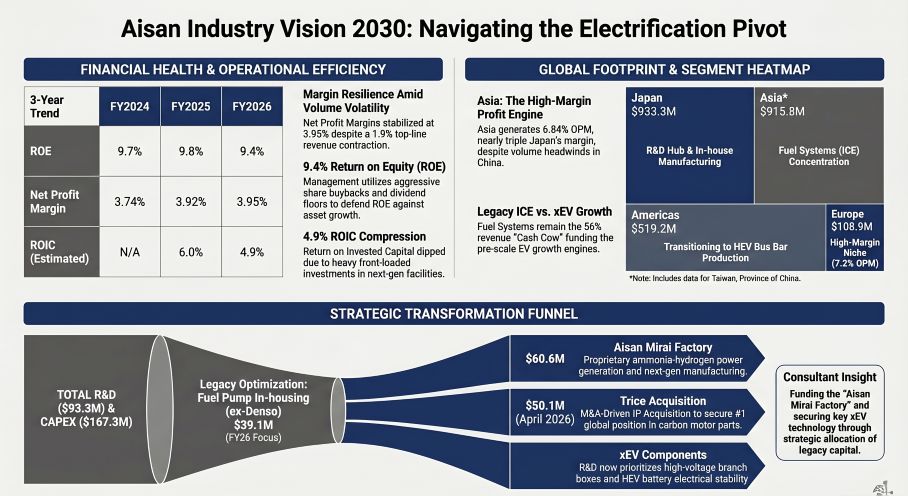

A Forensic Analysis of TYO: 7283 reveals a resilient operating margin defense mechanism, despite top-line contraction and working capital deterioration. Operating leverage is currently sustained by the in-housing of legacy Denso fuel pump module lines, which structurally lowered breakeven points across domestic segments.

* Top-Line & ROIC Compression: FY2026 consolidated revenue contracted 1.9% to $2,211.9 million, heavily dragged by a 5.8% drop in the Asia segment ($915.8 million) due to NYSE: TM (Toyota) and other Japanese OEMs losing market share in China. Estimated ROIC compressed from 6.0% to 4.9%, driven by an expanded asset base and a higher effective tax rate (34.5%).

* Working Capital & FCF Conversion: Free Cash Flow plunged to -$29.2 million, driven by sustained capital expenditures and a severely stretched Cash Conversion Cycle (CCC), which elongated by 12.1 days to 55.4 days.

* Unit Economics & Labor Friction: The company implemented an aggressive 7.5% year-over-year increase in average salaries ($51,120), significantly outpacing the 2.27% growth in labor productivity (revenue-per-employee: $337,446). This presents immediate margin friction on fixed costs.

* Contingent Liabilities & Pensions: Aisan carries a massive $46.65 million product warranty provision (reduced from $98.02 million in FY2025). Conversely, its defined-benefit pension acts as a hidden asset, operating in a net overfunded position of $56.19 million.

* Capital Allocation: Shareholder return mechanisms remain aggressive. The company executed a $62.9 million share buyback (5.5 million shares) and distributed $29.6 million in dividends ($0.53/share), enforcing a strict 35% payout ratio baseline.

Supply Chain Audit & Geo-Economic Moat

Aisan’s physical footprint dictates a highly bifurcated strategy: maximizing localized ICE profitability in emerging markets while centralizing high-risk zero-emission R&D in Japan.

* Asset Stranding & Geographic Realignment: The delayed 2035 European ICE ban temporarily benefits Aisan's product mix, but physical asset risk is actively materializing. In FY2026, the company recognized a $12.07 million impairment loss on machinery and buildings at its Mexico facility due to deteriorating regional ICE demand.

* Concentrated CapEx in Legacy Hardware: Despite targeting a 60% reduction in Scope 1 and 2 emissions by 2030, forward-looking CapEx commitments strictly prioritize fuel pump module capacity. Key April 2026 to March 2027 deployments include expansions at the Aisan Industry India plant ($12.1 million), the Hyundam Industrial facility in South Korea ($7.1 million), and the Aisan Industry Kentucky plant ($5.6 million).

* Next-Gen Hubs & M&A: Domestic CapEx is overwhelmingly funneled into the new Aisan Mirai Factory ($60.6 million) for ammonia-hydrogen power generation validation, alongside the upcoming IMI Factory expansion ($14.1 million, concluding January 2027). The $50.1 million acquisition of Trice Corporation (April 2026) internalizes critical carbon motor brush supply chains.

* Extreme Customer Concentration: The firm’s operational cadence is entirely tethered to NYSE: TM (48.9% of external sales, $1,082.1 million) and KRX: 005380 (Hyundai, 10.4%). Furthermore, Aisan models a $140.4 million potential exposure to transitional climate risks, including the introduction of global carbon taxes and CBAM equivalents.

HDIN Institutional Perspective

Management champions its "VISION2030" pivot toward electrified architectures, but the physical capital allocation tells a differentiated story. Aisan's immediate cash engine remains fundamentally wired to legacy ICE fuel systems across transition markets. While the in-housing of Denso’s fuel pump lines secures near-term margin defense, the heavy deployment of CapEx into India and Kentucky presents a severe mid-term asset stranding risk. Furthermore, while the company maintains a robust TCFD reporting framework, the glaring omission of conflict mineral audits and raw material traceability for its new high-voltage battery connection components exposes a latent ESG vulnerability that the Street is currently underpricing.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Aisan industry Vision 2030: Navigating the Electrification Pivot

Forensic Financials & Segmental InventoryA Forensic Analysis of TYO: 7283 reveals a resilient operating margin defense mechanism, despite top-line contraction and working capital deterioration. Operating leverage is currently sustained by the in-housing of legacy Denso fuel pump module lines, which structurally lowered breakeven points across domestic segments.

* Top-Line & ROIC Compression: FY2026 consolidated revenue contracted 1.9% to $2,211.9 million, heavily dragged by a 5.8% drop in the Asia segment ($915.8 million) due to NYSE: TM (Toyota) and other Japanese OEMs losing market share in China. Estimated ROIC compressed from 6.0% to 4.9%, driven by an expanded asset base and a higher effective tax rate (34.5%).

* Working Capital & FCF Conversion: Free Cash Flow plunged to -$29.2 million, driven by sustained capital expenditures and a severely stretched Cash Conversion Cycle (CCC), which elongated by 12.1 days to 55.4 days.

* Unit Economics & Labor Friction: The company implemented an aggressive 7.5% year-over-year increase in average salaries ($51,120), significantly outpacing the 2.27% growth in labor productivity (revenue-per-employee: $337,446). This presents immediate margin friction on fixed costs.

* Contingent Liabilities & Pensions: Aisan carries a massive $46.65 million product warranty provision (reduced from $98.02 million in FY2025). Conversely, its defined-benefit pension acts as a hidden asset, operating in a net overfunded position of $56.19 million.

* Capital Allocation: Shareholder return mechanisms remain aggressive. The company executed a $62.9 million share buyback (5.5 million shares) and distributed $29.6 million in dividends ($0.53/share), enforcing a strict 35% payout ratio baseline.

Supply Chain Audit & Geo-Economic Moat

Aisan’s physical footprint dictates a highly bifurcated strategy: maximizing localized ICE profitability in emerging markets while centralizing high-risk zero-emission R&D in Japan.

* Asset Stranding & Geographic Realignment: The delayed 2035 European ICE ban temporarily benefits Aisan's product mix, but physical asset risk is actively materializing. In FY2026, the company recognized a $12.07 million impairment loss on machinery and buildings at its Mexico facility due to deteriorating regional ICE demand.

* Concentrated CapEx in Legacy Hardware: Despite targeting a 60% reduction in Scope 1 and 2 emissions by 2030, forward-looking CapEx commitments strictly prioritize fuel pump module capacity. Key April 2026 to March 2027 deployments include expansions at the Aisan Industry India plant ($12.1 million), the Hyundam Industrial facility in South Korea ($7.1 million), and the Aisan Industry Kentucky plant ($5.6 million).

* Next-Gen Hubs & M&A: Domestic CapEx is overwhelmingly funneled into the new Aisan Mirai Factory ($60.6 million) for ammonia-hydrogen power generation validation, alongside the upcoming IMI Factory expansion ($14.1 million, concluding January 2027). The $50.1 million acquisition of Trice Corporation (April 2026) internalizes critical carbon motor brush supply chains.

* Extreme Customer Concentration: The firm’s operational cadence is entirely tethered to NYSE: TM (48.9% of external sales, $1,082.1 million) and KRX: 005380 (Hyundai, 10.4%). Furthermore, Aisan models a $140.4 million potential exposure to transitional climate risks, including the introduction of global carbon taxes and CBAM equivalents.

HDIN Institutional Perspective

Management champions its "VISION2030" pivot toward electrified architectures, but the physical capital allocation tells a differentiated story. Aisan's immediate cash engine remains fundamentally wired to legacy ICE fuel systems across transition markets. While the in-housing of Denso’s fuel pump lines secures near-term margin defense, the heavy deployment of CapEx into India and Kentucky presents a severe mid-term asset stranding risk. Furthermore, while the company maintains a robust TCFD reporting framework, the glaring omission of conflict mineral audits and raw material traceability for its new high-voltage battery connection components exposes a latent ESG vulnerability that the Street is currently underpricing.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."