bioAffinity Technologies, Inc.: $3.4 Million Dilutive Equity Issuance Near San Antonio Processing Laboratory as 36% Consolidated Revenue Contraction Signals Escalating Operational Insolvency

Date : 2026-06-15

Reading : 117

bioAffinity Technologies, Inc. [NASDAQ: BIAF] confronts a critical liquidity crisis, reporting $3.1 million in cash with a runway exhausted by June 2026. Despite a 114% year-over-year expansion in Q1 2026 CyPath® Lung revenue ($361,000), total consolidated top-line contracted 36% to $1.4 million. The firm’s absolute dependency on its single San Antonio CLIA-certified laboratory exposes LPs to single-node logistical risk. Imminent equity dilution to fund $3.4 million in net proceeds threatens to trigger Internal Revenue Code Section 382 ownership thresholds, permanently impairing the utility of the company’s $72.2 million accumulated deficit tax shield.

Figure bioAffinity Technologies: S-1 Corporate Blueprint

1. Q1 2026 Financial Realities: Deconstructing bioAffinity Technologies, Inc.’s Segmental Margins and Structural Overhang

1. Q1 2026 Financial Realities: Deconstructing bioAffinity Technologies, Inc.’s Segmental Margins and Structural Overhang

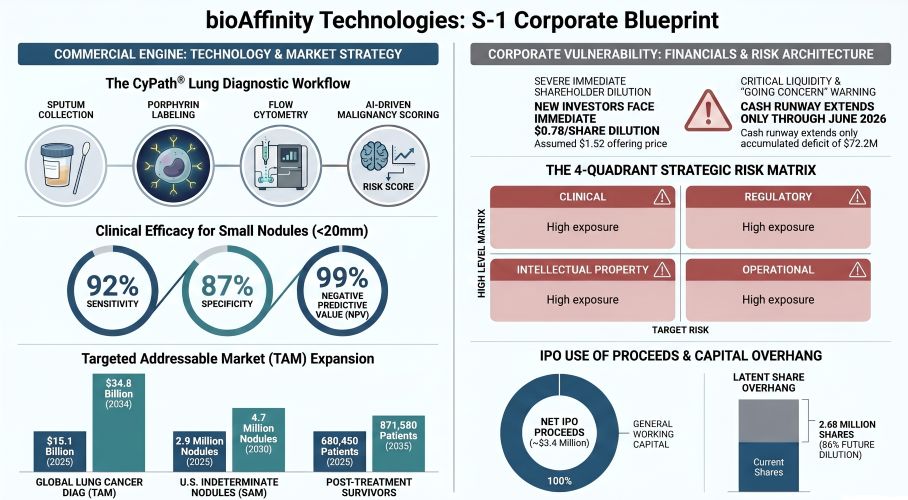

The company's financial architecture exhibits a severe structural deficit characterized by top-line volatility and an immediate reliance on highly dilutive derivative financing. WithumSmith+Brown, PC issued an explicit "going concern" qualification for the fiscal year ended December 31, 2025.

1.1 Top-Line Revenue and Cash Flow Segmentation

Revenue generation transitioned from zero pre-2022 to an absolute reliance on the September 2023 acquisition of Precision Pathology Laboratory Services (PPLS) from Village Oaks Pathology Services, P.A. and Dr. Roby P. Joyce.

* FY 2022 Revenue: $0

* FY 2023 Revenue: $2.5 million (post-September acquisition)

* FY 2024 Revenue: $9.4 million

* FY 2025 Revenue: $6.2 million

* Q1 2025 Revenue: $1.9 million consolidated (CyPath® Lung contributed $169,000)

* Q1 2026 Revenue: $1.4 million consolidated (36% YoY decline; CyPath® Lung contributed $361,000, representing a 114% YoY increase).

* Balance Sheet: $3.1 million cash on hand (March 31, 2026); $72.2 million accumulated deficit.

1.2 Offering Mechanics and Immediate Equity Dilution

The company’s June 2026 offering is structurally dilutive, generating an estimated $3.4 million in net proceeds strictly for general working capital, bypassing ring-fenced allocations for R&D.

Table: Summary of Public Offering Terms, Net Tangible Book Value Adjustment, and Shareholder Dilution Effects

1.3 Derivative Overhang and Latent Capital Restructuring

The capitalization table contains 2,687,028 potential new derivative shares, establishing a 36% future inflationary dilution parameter against the post-IPO base. Between April 1, 2026, and June 10, 2026, the company issued 83,331 shares via Series B conversion and 161,055 shares to consultants and employees.

Table: Overview of Outstanding Convertible Securities, Warrants, Options, and Equity Incentive Plan Reserves

2. B2B Logistical Architecture and Point-of-Failure Diagnostics: Auditing the San Antonio Production Moat

2.1 Infrastructure and Single-Node Dependency

bioAffinity Technologies operates a monolithic processing infrastructure restricted to a single CAP-accredited, CLIA-certified geographic node.

* Headquarters & Commercial Laboratory: 3300 Nacogdoches Road, Suite 216, San Antonio, Texas. All CyPath® Lung assays and anatomical pathology revenues originate entirely from this PPLS facility.

* Legacy R&D Hub: Historically leased at The University of Texas at San Antonio (UTSA). UTSA issued a non-renewal eviction notice in January 2026, forcing a capital-intensive relocation to privately owned space.

* Commercial Office Liability: Assumed office lease maintained with 343 West Sunset, LLC.

2.2 Supply Chain Architecture and Third-Party Risk

The firm's commercial fulfillment relies on highly fragmented B2B partnerships lacking long-term reagent purchase agreements.

* Physical Collection (Tier-1 Supplier): The test exclusively utilizes the Acapella™ Choice Blue positive expiratory pressure device, an FDA 510(k)-cleared Class I medical device manufactured by ICU Medical.

* Logistics Hub: Overnight biological transport is contracted entirely to Cardinal Health.

* Capital Market Restraints: WallachBeth Capital LLC secured an aggressive 3-month Right of First Refusal (ROFR) on future debt/equity and a 12-month Tail provision ensuring full cash/warrant compensation for introduced investors.

3. Addressable Market Economics and Intellectual Property: Quantifying the CyPath® Lung Diagnostic Arbitrage

3.1 Standard of Care Disruption vs. Competitive Friction

CyPath® Lung targets patients with indeterminate pulmonary nodules (IPNs) ranging from 6mm to 30mm. Standard Low-Dose Computed Tomography (LDCT) operates at 94% sensitivity but 73% specificity, yielding a Positive Predictive Value (PPV) below 4%. Invasive procedures (bronchoscopy, fine/core needle biopsies) carry systemic infection and hemorrhage risks.

* Unit Economics: CyPath® Lung eliminates unnecessary biopsies, saving an average of $2,773 per Medicare patient and $6,460 per privately insured patient. The test monetizes via a specific Medicare Proprietary Laboratory Analysis (PLA) code: 0406U (effective January 1, 2024).

* Competitor Metrics: LungLife AI’s LungLB (77% sensitivity, 72% specificity); Biodesix’s Nodify XL2 (44% specificity) and Nodify CDT; Veracyte’s Percepta Nasal Swab (50% indeterminate result rate).

3.2 TAM and Pipeline Expansion Variables

* Lung Cancer TAM: Expanding from $15.1 billion (2023) to $34.8 billion (2034) at a 7.9% CAGR. Screening compliance is forecast to increase from 18.1% in 2023 to 50% by 2030.

* IPN SAM: 2.9 million IPNs (2025) expanding 62% to 4.7 million (2030), carrying a market value exceeding $4.7 billion.

* Survivor Surveillance Segment: Cohort expanding 28% from 680,450 (2025) to 871,580 (2035), generating an $870 million opportunity.

* Asthma/COPD Pipeline: A $5.6 billion (2023) to $8.2 billion (2029) SAM, targeting 23 million U.S. patients, 27 million EU patients, and 45.7 million Chinese patients.

3.3 Clinical Trial Phasing and Efficacy Verification

The core diagnostic mechanism utilizes meso-tetra (4-carboxyphenyl) porphyrin (TCPP) evaluated via flow cytometry. An AI algorithm generates a numeric probability score between 0.1 and 1.0 within 20 minutes of data acquisition. The science originated at Los Alamos National Laboratory and St. Mary’s Hospital utilizing sputum from 12 uranium miners.

* Retrospective Milestones: A 2015 *Journal of Thoracic Oncology* study confirmed 81% accuracy, 77.9% sensitivity, and 65.7% specificity via manual microscopy. A January 2023 *Respiratory Research* 150-patient study (28 cancer, 122 cancer-free) confirmed an overall 82% sensitivity, 88% specificity, and a 0.89 Area Under the Curve (AUC).

* Optimal Nodule Detection (<20mm): Within a 132-patient sub-cohort (13 cancer, 119 cancer-free), CyPath® Lung delivered 92% sensitivity, 87% specificity, 88% accuracy, a 0.94 AUC, and a 99% Negative Predictive Value (NPV), correctly identifying 80% (8 out of 10) of Stage I tumors. A specific April 2026 case study successfully confirmed an "Unlikely Malignancy" result, deferring a biopsy.

* Longitudinal Trial (NCT07168993): Commenced March 2026, targeting 2,063 high-risk patients across 17 centers, including Brooke Army Medical Center (BAMC), Walter Reed Medical Center, South Texas Audie L. Murphy Memorial Veterans Medical Center, and supported by the John P. Murtha Cancer Center Research Program. Over 600 Phase 1 pilot tests were delivered in Texas in 2024. Phase 2 spans 2026 geographic expansion (Mid-Atlantic, South Atlantic, Southeast, Northeast, Midwest, West, and federal markets).

3.4 IP Moat and OncoSelect® Therapeutics

The patent estate includes 19 issued patents (3 U.S., 16 international across Australia, Canada, China, France, Germany, Hong Kong, Italy, Japan, Mexico, Spain, Sweden, UK), plus 21 diagnostic and 8 therapeutic pending applications (including a U.S. application for proprietary compensation beads).

* Diagnostic Expirations: 2030 (1 U.S., 9 non-U.S.); 2039 (3 non-U.S.); 2042 (1 non-U.S.).

* Therapeutic Expirations: 2037 (1 U.S., 2 non-U.S.); 2039 (1 non-U.S.); 2042 (1 U.S.).

* Therapeutic Efficacy: OncoSelect® utilizes siRNA to achieve a 90% mRNA knockdown of CD320 and LRP2 receptors, yielding up to an 80% cancer cell kill rate in vitro.

4. Corporate Governance, Regulatory Bottlenecks, and Off-Balance Sheet Liabilities

4.1 Human Capital and Entrenchment Matrix

The executive board is structured to maximize insider control. President/CEO/Founder Maria Zannes works alongside COO Xavier Reveles (25 years experience, CG(ASCP)cm certified), CMO Gordon Downie (30+ years experience, 30+ peer-reviewed publications), CSO William Bauta, and VP of Sales Dallas Coleman (15 years experience). The Board includes Executive Chairman Steven Girgenti, CFO J. Michael Edwards, John Oppenheimer, Peter S. Knight, Roberto Rios, and Jamie Platt. The Scientific Advisory Board includes Dr. David Ost and Dr. Daniel Sterman.

Compensation involves $18,750 per quarter in restricted stock for directors. Related-party transactions include Timothy Zannes (employed since February 1, 2015), Michael Dougherty, and Dr. Roby Joyce (who received 18,832 shares via the Joyce Living Trust).

4.2 Regulatory Arbitrage and Compliance Risk

bioAffinity markets CyPath® Lung strictly as a Laboratory Developed Test (LDT), successfully avoiding FDA Premarket Approval. While a March 2025 federal court ruling vacated the FDA's attempt to regulate LDTs, any reclassification of its AI algorithm as Software as a Medical Device (SaMD) would immediately halt operations. International Phase 3 expansion is structurally bottlenecked by the EU In Vitro Diagnostic Device Regulation (IVDR) requiring Notified Body review (delaying launches by 6 to 12 months) and strict General Data Protection Regulation (GDPR) frameworks, where violations trigger penalties up to $22.61 million (€20 million) or 4% of global revenues.

5. HDIN Institutional Perspective: The "Going Concern" Paradox

bioAffinity Technologies operates in a state of terminal friction: its underlying diagnostic science (99% NPV for nodules under 20mm) displays objective clinical superiority to legacy LDCT imaging, yet its financial architecture is optimized for structural value destruction. Management’s aggressive reliance on dilutive pre-funded warrants ($0.007 exercise price) to cover a basic $3.4 million working capital injection mathematically confirms that internal laboratory operations (PPLS) cannot internally fund the massive 2,063-patient NCT07168993 clinical trial. Furthermore, by initiating continuous equity issuances, management will likely trigger the IRS Section 382 ownership change threshold, effectively evaporating the primary upside for potential acquiring entities: the $72.2 million NOL tax shield. For LPs, the asset is trapped; the technology requires a Tier-1 pharmaceutical buyout, but the corporate entrenchment (20,000,000 blank check preferred shares) acts as an absolute deterrent to hostile acquisition.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.

Figure bioAffinity Technologies: S-1 Corporate Blueprint

1. Q1 2026 Financial Realities: Deconstructing bioAffinity Technologies, Inc.’s Segmental Margins and Structural OverhangThe company's financial architecture exhibits a severe structural deficit characterized by top-line volatility and an immediate reliance on highly dilutive derivative financing. WithumSmith+Brown, PC issued an explicit "going concern" qualification for the fiscal year ended December 31, 2025.

1.1 Top-Line Revenue and Cash Flow Segmentation

Revenue generation transitioned from zero pre-2022 to an absolute reliance on the September 2023 acquisition of Precision Pathology Laboratory Services (PPLS) from Village Oaks Pathology Services, P.A. and Dr. Roby P. Joyce.

* FY 2022 Revenue: $0

* FY 2023 Revenue: $2.5 million (post-September acquisition)

* FY 2024 Revenue: $9.4 million

* FY 2025 Revenue: $6.2 million

* Q1 2025 Revenue: $1.9 million consolidated (CyPath® Lung contributed $169,000)

* Q1 2026 Revenue: $1.4 million consolidated (36% YoY decline; CyPath® Lung contributed $361,000, representing a 114% YoY increase).

* Balance Sheet: $3.1 million cash on hand (March 31, 2026); $72.2 million accumulated deficit.

1.2 Offering Mechanics and Immediate Equity Dilution

The company’s June 2026 offering is structurally dilutive, generating an estimated $3.4 million in net proceeds strictly for general working capital, bypassing ring-fenced allocations for R&D.

Table: Summary of Public Offering Terms, Net Tangible Book Value Adjustment, and Shareholder Dilution Effects

| Offering Metric | Hard Data Point |

|---|---|

| Total Shares / Pre-Funded Warrants Offered | 2,631,579 units (Pre-funded warrants exercisable at $0.007 per share) |

| Assumed Public Offering Price | $1.52 per share |

| Placement Agent & Offering Fees | 7.5% of gross proceeds payable to WallachBeth Capital LLC, plus approximately $280,000 in offering-related expenses |

| Historical NTBV (March 31, 2026) | $1.6 million, equivalent to $0.35 per share based on 4,498,675 shares outstanding |

| Pro Forma NTBV Before Current Offering | $2.1 million, equivalent to $0.43 per share based on 4,743,061 shares outstanding after prior May 2026 issuances |

| Pro Forma As-Adjusted NTBV After Offering | $5.4 million, equivalent to $0.74 per share based on 7,374,640 shares outstanding following the offering |

| Immediate Dilution to New Investors | $0.78 per share |

| Increase in NTBV for Existing Shareholders | $0.31 per share |

1.3 Derivative Overhang and Latent Capital Restructuring

The capitalization table contains 2,687,028 potential new derivative shares, establishing a 36% future inflationary dilution parameter against the post-IPO base. Between April 1, 2026, and June 10, 2026, the company issued 83,331 shares via Series B conversion and 161,055 shares to consultants and employees.

Table: Overview of Outstanding Convertible Securities, Warrants, Options, and Equity Incentive Plan Reserves

| Derivative Instrument | Outstanding Volume | Conversion / Exercise Price |

|---|---|---|

| Blank Check Preferred Stock | 20,000,000 shares authorized | N/A |

| Series B Convertible Preferred Stock | 450 shares outstanding (reduced from 990 shares issued in August 2025 for gross proceeds of $990,000) | Convertible into 150,000 common shares at a conversion price of $3.00 per share |

| Outstanding Warrants | 1,713,894 shares issuable upon exercise | Weighted Average Exercise Price (WAEP): $22.38 per share |

| Outstanding Stock Options | 385,849 shares issuable upon exercise | Weighted Average Exercise Price (WAEP): $6.52 per share |

| 2024 Equity Incentive Plan Reserve | 437,285 shares reserved for future equity awards | N/A |

2. B2B Logistical Architecture and Point-of-Failure Diagnostics: Auditing the San Antonio Production Moat

2.1 Infrastructure and Single-Node Dependency

bioAffinity Technologies operates a monolithic processing infrastructure restricted to a single CAP-accredited, CLIA-certified geographic node.

* Headquarters & Commercial Laboratory: 3300 Nacogdoches Road, Suite 216, San Antonio, Texas. All CyPath® Lung assays and anatomical pathology revenues originate entirely from this PPLS facility.

* Legacy R&D Hub: Historically leased at The University of Texas at San Antonio (UTSA). UTSA issued a non-renewal eviction notice in January 2026, forcing a capital-intensive relocation to privately owned space.

* Commercial Office Liability: Assumed office lease maintained with 343 West Sunset, LLC.

2.2 Supply Chain Architecture and Third-Party Risk

The firm's commercial fulfillment relies on highly fragmented B2B partnerships lacking long-term reagent purchase agreements.

* Physical Collection (Tier-1 Supplier): The test exclusively utilizes the Acapella™ Choice Blue positive expiratory pressure device, an FDA 510(k)-cleared Class I medical device manufactured by ICU Medical.

* Logistics Hub: Overnight biological transport is contracted entirely to Cardinal Health.

* Capital Market Restraints: WallachBeth Capital LLC secured an aggressive 3-month Right of First Refusal (ROFR) on future debt/equity and a 12-month Tail provision ensuring full cash/warrant compensation for introduced investors.

3. Addressable Market Economics and Intellectual Property: Quantifying the CyPath® Lung Diagnostic Arbitrage

3.1 Standard of Care Disruption vs. Competitive Friction

CyPath® Lung targets patients with indeterminate pulmonary nodules (IPNs) ranging from 6mm to 30mm. Standard Low-Dose Computed Tomography (LDCT) operates at 94% sensitivity but 73% specificity, yielding a Positive Predictive Value (PPV) below 4%. Invasive procedures (bronchoscopy, fine/core needle biopsies) carry systemic infection and hemorrhage risks.

* Unit Economics: CyPath® Lung eliminates unnecessary biopsies, saving an average of $2,773 per Medicare patient and $6,460 per privately insured patient. The test monetizes via a specific Medicare Proprietary Laboratory Analysis (PLA) code: 0406U (effective January 1, 2024).

* Competitor Metrics: LungLife AI’s LungLB (77% sensitivity, 72% specificity); Biodesix’s Nodify XL2 (44% specificity) and Nodify CDT; Veracyte’s Percepta Nasal Swab (50% indeterminate result rate).

3.2 TAM and Pipeline Expansion Variables

* Lung Cancer TAM: Expanding from $15.1 billion (2023) to $34.8 billion (2034) at a 7.9% CAGR. Screening compliance is forecast to increase from 18.1% in 2023 to 50% by 2030.

* IPN SAM: 2.9 million IPNs (2025) expanding 62% to 4.7 million (2030), carrying a market value exceeding $4.7 billion.

* Survivor Surveillance Segment: Cohort expanding 28% from 680,450 (2025) to 871,580 (2035), generating an $870 million opportunity.

* Asthma/COPD Pipeline: A $5.6 billion (2023) to $8.2 billion (2029) SAM, targeting 23 million U.S. patients, 27 million EU patients, and 45.7 million Chinese patients.

3.3 Clinical Trial Phasing and Efficacy Verification

The core diagnostic mechanism utilizes meso-tetra (4-carboxyphenyl) porphyrin (TCPP) evaluated via flow cytometry. An AI algorithm generates a numeric probability score between 0.1 and 1.0 within 20 minutes of data acquisition. The science originated at Los Alamos National Laboratory and St. Mary’s Hospital utilizing sputum from 12 uranium miners.

* Retrospective Milestones: A 2015 *Journal of Thoracic Oncology* study confirmed 81% accuracy, 77.9% sensitivity, and 65.7% specificity via manual microscopy. A January 2023 *Respiratory Research* 150-patient study (28 cancer, 122 cancer-free) confirmed an overall 82% sensitivity, 88% specificity, and a 0.89 Area Under the Curve (AUC).

* Optimal Nodule Detection (<20mm): Within a 132-patient sub-cohort (13 cancer, 119 cancer-free), CyPath® Lung delivered 92% sensitivity, 87% specificity, 88% accuracy, a 0.94 AUC, and a 99% Negative Predictive Value (NPV), correctly identifying 80% (8 out of 10) of Stage I tumors. A specific April 2026 case study successfully confirmed an "Unlikely Malignancy" result, deferring a biopsy.

* Longitudinal Trial (NCT07168993): Commenced March 2026, targeting 2,063 high-risk patients across 17 centers, including Brooke Army Medical Center (BAMC), Walter Reed Medical Center, South Texas Audie L. Murphy Memorial Veterans Medical Center, and supported by the John P. Murtha Cancer Center Research Program. Over 600 Phase 1 pilot tests were delivered in Texas in 2024. Phase 2 spans 2026 geographic expansion (Mid-Atlantic, South Atlantic, Southeast, Northeast, Midwest, West, and federal markets).

3.4 IP Moat and OncoSelect® Therapeutics

The patent estate includes 19 issued patents (3 U.S., 16 international across Australia, Canada, China, France, Germany, Hong Kong, Italy, Japan, Mexico, Spain, Sweden, UK), plus 21 diagnostic and 8 therapeutic pending applications (including a U.S. application for proprietary compensation beads).

* Diagnostic Expirations: 2030 (1 U.S., 9 non-U.S.); 2039 (3 non-U.S.); 2042 (1 non-U.S.).

* Therapeutic Expirations: 2037 (1 U.S., 2 non-U.S.); 2039 (1 non-U.S.); 2042 (1 U.S.).

* Therapeutic Efficacy: OncoSelect® utilizes siRNA to achieve a 90% mRNA knockdown of CD320 and LRP2 receptors, yielding up to an 80% cancer cell kill rate in vitro.

4. Corporate Governance, Regulatory Bottlenecks, and Off-Balance Sheet Liabilities

4.1 Human Capital and Entrenchment Matrix

The executive board is structured to maximize insider control. President/CEO/Founder Maria Zannes works alongside COO Xavier Reveles (25 years experience, CG(ASCP)cm certified), CMO Gordon Downie (30+ years experience, 30+ peer-reviewed publications), CSO William Bauta, and VP of Sales Dallas Coleman (15 years experience). The Board includes Executive Chairman Steven Girgenti, CFO J. Michael Edwards, John Oppenheimer, Peter S. Knight, Roberto Rios, and Jamie Platt. The Scientific Advisory Board includes Dr. David Ost and Dr. Daniel Sterman.

Compensation involves $18,750 per quarter in restricted stock for directors. Related-party transactions include Timothy Zannes (employed since February 1, 2015), Michael Dougherty, and Dr. Roby Joyce (who received 18,832 shares via the Joyce Living Trust).

4.2 Regulatory Arbitrage and Compliance Risk

bioAffinity markets CyPath® Lung strictly as a Laboratory Developed Test (LDT), successfully avoiding FDA Premarket Approval. While a March 2025 federal court ruling vacated the FDA's attempt to regulate LDTs, any reclassification of its AI algorithm as Software as a Medical Device (SaMD) would immediately halt operations. International Phase 3 expansion is structurally bottlenecked by the EU In Vitro Diagnostic Device Regulation (IVDR) requiring Notified Body review (delaying launches by 6 to 12 months) and strict General Data Protection Regulation (GDPR) frameworks, where violations trigger penalties up to $22.61 million (€20 million) or 4% of global revenues.

5. HDIN Institutional Perspective: The "Going Concern" Paradox

bioAffinity Technologies operates in a state of terminal friction: its underlying diagnostic science (99% NPV for nodules under 20mm) displays objective clinical superiority to legacy LDCT imaging, yet its financial architecture is optimized for structural value destruction. Management’s aggressive reliance on dilutive pre-funded warrants ($0.007 exercise price) to cover a basic $3.4 million working capital injection mathematically confirms that internal laboratory operations (PPLS) cannot internally fund the massive 2,063-patient NCT07168993 clinical trial. Furthermore, by initiating continuous equity issuances, management will likely trigger the IRS Section 382 ownership change threshold, effectively evaporating the primary upside for potential acquiring entities: the $72.2 million NOL tax shield. For LPs, the asset is trapped; the technology requires a Tier-1 pharmaceutical buyout, but the corporate entrenchment (20,000,000 blank check preferred shares) acts as an absolute deterrent to hostile acquisition.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.