Duality Biotherapeutics: Exercising DB-1311 US Co-Commercialization Option Near New Jersey R&D Hub as $194.15M BioNTech Revenue Signals Profitable Transition to Vicarious Execution

Date : 2026-06-16

Reading : 145

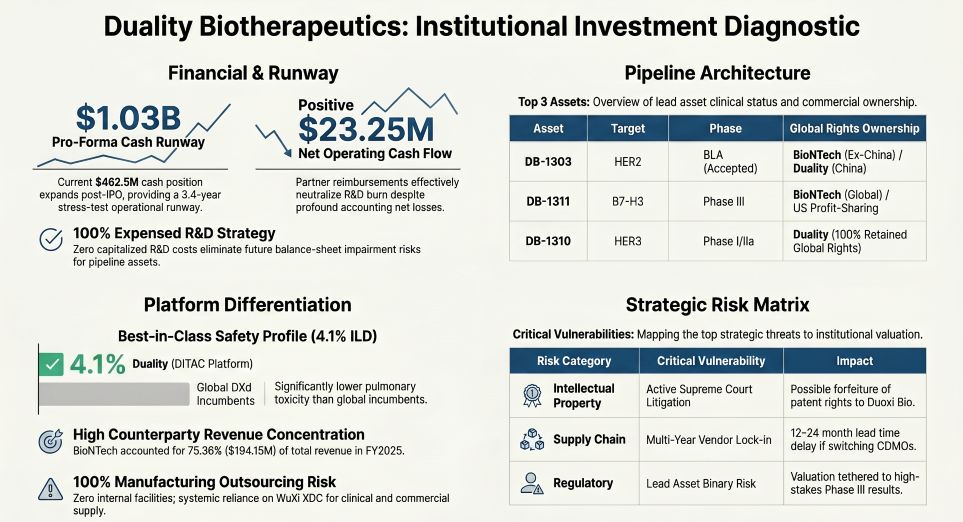

Duality Biotherapeutics [HKEX: Pending, STAR: Pending] operates a hyper-asset-light Antibody-Drug Conjugate (ADC) engine, converting a -$362.53M accounting net loss into a $23.25M positive operating cash flow for FY2025 through its global out-licensing architecture. While a $462.54M liquidity pool and $570.43M in planned IPO proceeds provide ~3.4 years of pro-forma capital runway, extreme vendor consolidation poses acute geopolitical risks. With 100% outsourced manufacturing reliant on Tier-1 CDMOs, shifting cross-border trade controls and biosecure legislation directly threaten the firm's >$6.00B global transaction pipeline.

Figure Duality Biotherapeutics: Institutional Investment Diagnostic

FY2025 Financial Realities: Deconstructing Duality Biotherapeutics’ Segmental Margins & Capital Architecture

FY2025 Financial Realities: Deconstructing Duality Biotherapeutics’ Segmental Margins & Capital Architecture

A. Liquidity, P&L Adjustments, & Burn Rate Dynamics

The company’s reported net losses escalated from -$46.36M (CNY 333.19M) in 2023, to -$139.16M (CNY 1,000.23M) in 2024, reaching -$362.53M (CNY 2,605.70M) in 2025, culminating in a cumulative unrecovered deficit of $659.05M (CNY 4.73B). However, fundamental cash-flow dynamics demonstrate pure operational solvency.

* Non-Cash Artifacts: The 2025 net loss includes a -$306.89M (CNY 2.21B) fair value change loss from convertible preferred shares (100% converted to ordinary shares upon HKEX IPO) and $21.71M (CNY 156.04M) in share-based compensation (SBC). Historical SBC totaled $26.49M (CNY 190.41M) in 2024 and $3.33M (CNY 23.95M) in 2023. Management has authorized 22,287,582 options (2020 plan) and 3,210,854 shares (2025 plan).

* Cash Flow: Net operating cash flow remained positive at $23.25M in 2025, $36.15M in 2024, and $110.18M in 2023. Gross operating cash outflow for 2025 stood at $303.82M.

* Pro-Forma Runway: Current cash equivalents of $462.54M yield a 1.5-year stress-test runway. Factoring in $570.43M from the STAR Market IPO (issuing 15,779,190 new A-shares, up to 15% dilution), the $1.03B liquidity pool extends the runway to ~3.4 years.

* Debt & Liabilities: Short-term borrowings equal $19.63M (CNY 141.06M) via Industrial and Commercial Bank of China (ICBC) and Bank of China (BOC), supplemented by a $13.91M (CNY 100M) China Merchants Bank credit line. Current lease liabilities are $0.67M (CNY 4.81M); non-current lease liabilities sit at $0.54M (CNY 3.91M).

B. Asset Quality & Conservative R&D Expenditures

Duality deploys an immediate-expensing R&D methodology (0% capitalized costs), insulating the balance sheet from clinical impairment risks. Total assets are $543.51M, of which current assets represent 98.50%. Pure cash represents 86.40% of current assets. Fixed assets total $1.94M; intangible assets equal $0.52M.

* Total R&D spend: $73.43M (2023), $105.77M (2024), and $115.45M (2025).

* 2025 Phase-Specific Allocation: DB-1303 ($25.88M), DB-1310 ($16.90M), DB-2304 ($11.36M), DB-1419 ($8.32M), DB-1311 ($5.39M), DB-1418 ($4.85M), and DB-1305 ($1.33M).

* Clinical Unit Economics: Total technical R&D service expenses reached $65.80M (CNY 472.97M) in 2023, $84.07M (CNY 604.25M) in 2024, and $90.03M (CNY 647.05M) in 2025, totaling $239.90M. Distributed across >3,500 enrolled patients (50% overseas), the blended clinical execution cost is ~$68,542 per patient.

C. Revenue Structural Shift & Margin Compression

Total revenue scaled from $248.56M in 2023 to $270.09M in 2024, stabilizing at $257.63M in 2025.

* Income Quality: Upfront technology licensing fees dropped from 79.71% ($198.14M) in 2023 to 24.50% ($63.12M) in 2025. Conversely, recurring R&D service revenue surged to 75.36% ($194.15M) in 2025.

* Counterparty Reliance: BioNTech SE drove 98.86% ($245.72M) of FY2023 revenue and 75.36% ($194.15M) in FY2025. Avenzo Therapeutics accounted for 23.28% ($59.98M), and Adcendo ApS generated 1.36% ($3.50M) in 2025. BeiGene represented 17.08% of 2024 revenue.

* COGS Matrix: FY2025 COGS hit $178.37M. Technical Service Expenses (CDMO/CRO) dominated at $157.91M (88.53%), Employee Compensation reached $12.44M (6.97%), and SBC represented $4.15M (2.33%). Gross margins contracted by 4,490 bps, falling from 75.67% in 2023 to 30.77% in 2025 as the firm absorbed capital-intensive Phase III trial executions.

D. Fiscal Dependency & Tax Engineering

Direct government subsidies provide negligible net loss mitigation (0.9% in 2023, 0.7% in 2024, 0.3% in 2025), totaling $0.44M (CNY 3.15M), $0.99M (CNY 7.12M), and $1.11M (CNY 7.99M) respectively. Specific grants include Suzhou Unicorn Enterprise ($0.83M/CNY 6.00M), Jinji Lake Talent ($0.16M/CNY 1.16M), and Shanghai Special Fund ($0.26M/CNY 1.90M).

* Tax Inflows: 2025 VAT refunds of $23.06M (CNY 165.73M) and overseas withholding tax refunds of $13.53M (CNY 97.22M) generated $37.70M in non-dilutive liquidity (mitigating 10.4% of the net loss).

* Tax Optimization & Friction: Suzhou Ying'en utilizes a 15% High and New Technology Enterprise (HNTE) CIT rate. It exempts the first $0.70M (CNY 5.00M) of technology transfer income. However, German 15.825% withholding taxes (versus the 10% treaty cap) locked up $16.06M (CNY 115.40M) in 2024 and $3.54M (CNY 25.45M) in 2025 as non-current assets. The Cayman and Hong Kong offshore entities carry severe "Deemed Resident Enterprise" 25% CIT risk under Circular 82.

Logistics and Logistics Hubs: Evaluating the Transnational Manufacturing & R&D Footprint

A. Global Operational Architecture

The company executes 10 Global Multi-Center Clinical Trials (MRCTs) across ~20 countries utilizing a 100% outsourced model. Its internal footprint focuses strictly on R&D command centers:

1. Shanghai (Mainland China): Global HQ and the Lingang biological discovery facility.

2. Suzhou (Mainland China): ADC conjugation process development hub.

3. Beijing (Mainland China): Clinical registration affairs.

4. New Jersey (USA): R&D and translational medicine center.

5. California (USA): Global clinical trial execution hub.

B. Vendor Consolidation & Upstream Supply Friction

The Top 5 R&D vendors monopolize procurement, absorbing $83.59M/CNY 600.81M (66.89%) in 2023, $168.12M/CNY 1,208.34M (70.47%) in 2024, and $168.63M/CNY 1,212.05M (67.65%) in 2025.

* CDMO Dependency: Manufacturing involves a strict 6-step cycle (Thawing/Reduction, Conjugation, Purification, Formulation, Lyophilization, Labeling). WuXi Biologics Inc. / WuXi XDC handled 27.83% ($66.40M) of procurement in 2024 and 17.77% ($44.31M) in 2025. Zhenge Biotech controlled 10.51% ($25.08M) in 2024, while Haoyuan Chemexpress captured 8.34% ($10.42M) in 2023. Western production relies heavily on Catalent Pharma Solutions LLC (USA) and Catalent Germany Schorndorf GmbH.

* CDMO Switching Costs: Duality holds binding contracts with WuXi XDC for the WBP2378 ADC project (active through September 2027) and WBP3804 ADC project (June 2028 / September 2027), imposing an estimated 12-to-24-month CMC bridging lead-time delay if vendor replacement is required.

* CRO Execution: Global clinical logistics are routed through Tigermed ($61.71M / 24.75% in 2025), IQVIA ($28.79M / 11.55%), and Parexel ($19.58M / 7.86%).

Strategic Execution & Portfolio Assets: Quantifying the >$6.00 Billion ADC Pipeline

A. Foundational Therapeutics & Clinical Economics

Duality’s DITAC, DIMAC, DUPAC, and DIBAC platforms (utilizing P1003 and P1021 exatecan topoisomerase I inhibitors) actively bypass the resistance profiles of Daiichi Sankyo’s DXd technology.

1. DB-1303 (HER2): NMPA BLA accepted. Targets full-spectrum expression (IHC 1+/2+/3+). FDA BLA submission scheduled for 2026 (BTD and FTD granted). Competes with Daiichi’s DS-8201 (Enhertu), RemeGen’s RC48, and Kelun-Biotech's A166. BioNTech holds global rights (ex-China/HK/Macao), while 3SBio (Sansom) executes domestic commercialization. Drug-to-Antibody Ratio (DAR) is 8. Uses Trastuzumab amino acid sequence.

2. DB-1311 (B7-H3): Phase III for mCRPC (readout 2028-2029) competing with Daiichi’s DS-7300. Holds ODD for ESCC/SCLC. Delivered an 11.3-month median PFS and 22.5-month mOS. Exhibited pristine safety with 1 Grade 2 ILD case among 110 patients at the 6mg/kg dose. DAR 6. In May 2026, Duality officially exercised its option to share US development costs and commercial profits with BioNTech. Relies on WuXi Biologics B7-H3 mAb license.

3. DB-1310 (HER3): Phase I/IIa. DAR 8. Targets novel epitope on Domain I. Generated an unconfirmed ORR of 43.5% and 18.89-month mOS in 3rd-line EGFR-mutant NSCLC. ILD rate of 4.1% in 246 patients. 100% retained global rights. Competes with Baili-Tianheng's BL-B01D1. Relies on Sinotau/Beijing Xiantong HER3 mAb license.

4. DB-1305 (TROP2): Phase I/IIa (TTM 3.5-5 years). FTD for Platinum-Resistant Ovarian Cancer. Generated 83.3% ORR when combined with Pumitamig. Competes with Kelun-Biotech's SKB264. BioNTech holds rights. DAR 4.

5. Expanded Pipeline: DB-1418 (EGFRxHER3, licensed to Avenzo ex-China/HK/Macao/Taiwan), DB-1419 (B7-H3xPD-L1, licensed from Darts Bio), DB-2304 (BDCA2 for SLE/CLE), DB-1312 (B7-H4, licensed from Nona Biosciences, 100% to BeiGene), DB-1324 (CDH17, GSK exclusive option ex-China), DB-1317 (ADAM9). Pre-clinical: DB-1329 (CDCP1), DB-1326 (TA-MUC1). Adcendo holds global DITAC options, Duality retains China/HK/Macao/Taiwan options.

B. IP Litigation & Corporate Governance Mechanics

* Duoxi Bio Patent Litigation: Duality faces IP volatility against domestic competitor Duoxi Bio regarding three patent applications. The Shanghai Intellectual Property Court dismissed all of Duoxi Bio's claims in December 2025. Two rulings are legally effective; one is currently appealed to the Supreme People's Court. The firm reports 0 pending employment arbitrations.

* Cap Table: Duality lacks a controlling shareholder. Lilly Asia Ventures (LAV USD) holds 13.03%, Chairman/CEO Dr. John Zhu (Zhu Zhongyuan) holds 7.31% via DualityBio Ltd., Shanghai Yingjia holds 7.14%, and King Star (Lin Xianghong) holds 5.89%. Strategic investors include WX Venture and AstraZeneca-CICC. Leadership includes CSO Dr. QIU Yang (former Daiichi Sankyo), CMO Dr. MU Hua, and SAB members Dr. Antoine Yver and Dr. Pasi A. Jänne.

C. Addressable Market (TAM/SAM) Projections

1. HER2 Segment: Global TAM projected from $6.70B (2024) to $43.50B (2035) at an 18.5% CAGR. The HER2-low SAM expands from 926.4K incident cases in 2024 to 1.20M in 2035 (China: 144.8K to 175.4K).

2. TROP2 Segment: Global TAM expanding from $1.50B (2024) to $42.50B (2035) at a 35.4% CAGR. TNBC SAM scales from 299.6K to 389.3K.

3. HER3/NSCLC Segment: Total NSCLC incidence grows from 2.21M (2024) to 2.92M (2035), with China accounting for 973.2K to 1.32M cases. The EGFR-mutant SAM expands from 615.1K to 821.6K.

4. B7-H3 Segment: Projected from $100M (2026) to $14.20B (2035) at a 59.7% CAGR. The mCRPC SAM grows from 468.2K to 733.0K.

HDIN Institutional Perspective

Duality Biotherapeutics' hyper-asset-light model is a mathematically exact mechanism for offloading capital risk, effectively insulating the balance sheet from a $303.82M gross operational burn. However, the exact variables generating this insulation—the 100% outsourced manufacturing network and the 75.36% revenue reliance on BioNTech—form the firm's central vulnerability. The exercising of the DB-1311 US profit-share option in May 2026 marks a required strategic evolution into co-commercialization. Yet, with 67.65% of all R&D procurement centralized in just 5 vendors, and the core WuXi XDC production pipeline increasingly exposed to shifting US biosecurity legislation, Duality is fundamentally trading clinical capital risk for systemic sovereign and supply chain risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Duality Biotherapeutics: Institutional Investment Diagnostic

FY2025 Financial Realities: Deconstructing Duality Biotherapeutics’ Segmental Margins & Capital ArchitectureA. Liquidity, P&L Adjustments, & Burn Rate Dynamics

The company’s reported net losses escalated from -$46.36M (CNY 333.19M) in 2023, to -$139.16M (CNY 1,000.23M) in 2024, reaching -$362.53M (CNY 2,605.70M) in 2025, culminating in a cumulative unrecovered deficit of $659.05M (CNY 4.73B). However, fundamental cash-flow dynamics demonstrate pure operational solvency.

* Non-Cash Artifacts: The 2025 net loss includes a -$306.89M (CNY 2.21B) fair value change loss from convertible preferred shares (100% converted to ordinary shares upon HKEX IPO) and $21.71M (CNY 156.04M) in share-based compensation (SBC). Historical SBC totaled $26.49M (CNY 190.41M) in 2024 and $3.33M (CNY 23.95M) in 2023. Management has authorized 22,287,582 options (2020 plan) and 3,210,854 shares (2025 plan).

* Cash Flow: Net operating cash flow remained positive at $23.25M in 2025, $36.15M in 2024, and $110.18M in 2023. Gross operating cash outflow for 2025 stood at $303.82M.

* Pro-Forma Runway: Current cash equivalents of $462.54M yield a 1.5-year stress-test runway. Factoring in $570.43M from the STAR Market IPO (issuing 15,779,190 new A-shares, up to 15% dilution), the $1.03B liquidity pool extends the runway to ~3.4 years.

* Debt & Liabilities: Short-term borrowings equal $19.63M (CNY 141.06M) via Industrial and Commercial Bank of China (ICBC) and Bank of China (BOC), supplemented by a $13.91M (CNY 100M) China Merchants Bank credit line. Current lease liabilities are $0.67M (CNY 4.81M); non-current lease liabilities sit at $0.54M (CNY 3.91M).

B. Asset Quality & Conservative R&D Expenditures

Duality deploys an immediate-expensing R&D methodology (0% capitalized costs), insulating the balance sheet from clinical impairment risks. Total assets are $543.51M, of which current assets represent 98.50%. Pure cash represents 86.40% of current assets. Fixed assets total $1.94M; intangible assets equal $0.52M.

* Total R&D spend: $73.43M (2023), $105.77M (2024), and $115.45M (2025).

* 2025 Phase-Specific Allocation: DB-1303 ($25.88M), DB-1310 ($16.90M), DB-2304 ($11.36M), DB-1419 ($8.32M), DB-1311 ($5.39M), DB-1418 ($4.85M), and DB-1305 ($1.33M).

* Clinical Unit Economics: Total technical R&D service expenses reached $65.80M (CNY 472.97M) in 2023, $84.07M (CNY 604.25M) in 2024, and $90.03M (CNY 647.05M) in 2025, totaling $239.90M. Distributed across >3,500 enrolled patients (50% overseas), the blended clinical execution cost is ~$68,542 per patient.

C. Revenue Structural Shift & Margin Compression

Total revenue scaled from $248.56M in 2023 to $270.09M in 2024, stabilizing at $257.63M in 2025.

* Income Quality: Upfront technology licensing fees dropped from 79.71% ($198.14M) in 2023 to 24.50% ($63.12M) in 2025. Conversely, recurring R&D service revenue surged to 75.36% ($194.15M) in 2025.

* Counterparty Reliance: BioNTech SE drove 98.86% ($245.72M) of FY2023 revenue and 75.36% ($194.15M) in FY2025. Avenzo Therapeutics accounted for 23.28% ($59.98M), and Adcendo ApS generated 1.36% ($3.50M) in 2025. BeiGene represented 17.08% of 2024 revenue.

* COGS Matrix: FY2025 COGS hit $178.37M. Technical Service Expenses (CDMO/CRO) dominated at $157.91M (88.53%), Employee Compensation reached $12.44M (6.97%), and SBC represented $4.15M (2.33%). Gross margins contracted by 4,490 bps, falling from 75.67% in 2023 to 30.77% in 2025 as the firm absorbed capital-intensive Phase III trial executions.

D. Fiscal Dependency & Tax Engineering

Direct government subsidies provide negligible net loss mitigation (0.9% in 2023, 0.7% in 2024, 0.3% in 2025), totaling $0.44M (CNY 3.15M), $0.99M (CNY 7.12M), and $1.11M (CNY 7.99M) respectively. Specific grants include Suzhou Unicorn Enterprise ($0.83M/CNY 6.00M), Jinji Lake Talent ($0.16M/CNY 1.16M), and Shanghai Special Fund ($0.26M/CNY 1.90M).

* Tax Inflows: 2025 VAT refunds of $23.06M (CNY 165.73M) and overseas withholding tax refunds of $13.53M (CNY 97.22M) generated $37.70M in non-dilutive liquidity (mitigating 10.4% of the net loss).

* Tax Optimization & Friction: Suzhou Ying'en utilizes a 15% High and New Technology Enterprise (HNTE) CIT rate. It exempts the first $0.70M (CNY 5.00M) of technology transfer income. However, German 15.825% withholding taxes (versus the 10% treaty cap) locked up $16.06M (CNY 115.40M) in 2024 and $3.54M (CNY 25.45M) in 2025 as non-current assets. The Cayman and Hong Kong offshore entities carry severe "Deemed Resident Enterprise" 25% CIT risk under Circular 82.

Logistics and Logistics Hubs: Evaluating the Transnational Manufacturing & R&D Footprint

A. Global Operational Architecture

The company executes 10 Global Multi-Center Clinical Trials (MRCTs) across ~20 countries utilizing a 100% outsourced model. Its internal footprint focuses strictly on R&D command centers:

1. Shanghai (Mainland China): Global HQ and the Lingang biological discovery facility.

2. Suzhou (Mainland China): ADC conjugation process development hub.

3. Beijing (Mainland China): Clinical registration affairs.

4. New Jersey (USA): R&D and translational medicine center.

5. California (USA): Global clinical trial execution hub.

B. Vendor Consolidation & Upstream Supply Friction

The Top 5 R&D vendors monopolize procurement, absorbing $83.59M/CNY 600.81M (66.89%) in 2023, $168.12M/CNY 1,208.34M (70.47%) in 2024, and $168.63M/CNY 1,212.05M (67.65%) in 2025.

* CDMO Dependency: Manufacturing involves a strict 6-step cycle (Thawing/Reduction, Conjugation, Purification, Formulation, Lyophilization, Labeling). WuXi Biologics Inc. / WuXi XDC handled 27.83% ($66.40M) of procurement in 2024 and 17.77% ($44.31M) in 2025. Zhenge Biotech controlled 10.51% ($25.08M) in 2024, while Haoyuan Chemexpress captured 8.34% ($10.42M) in 2023. Western production relies heavily on Catalent Pharma Solutions LLC (USA) and Catalent Germany Schorndorf GmbH.

* CDMO Switching Costs: Duality holds binding contracts with WuXi XDC for the WBP2378 ADC project (active through September 2027) and WBP3804 ADC project (June 2028 / September 2027), imposing an estimated 12-to-24-month CMC bridging lead-time delay if vendor replacement is required.

* CRO Execution: Global clinical logistics are routed through Tigermed ($61.71M / 24.75% in 2025), IQVIA ($28.79M / 11.55%), and Parexel ($19.58M / 7.86%).

Strategic Execution & Portfolio Assets: Quantifying the >$6.00 Billion ADC Pipeline

A. Foundational Therapeutics & Clinical Economics

Duality’s DITAC, DIMAC, DUPAC, and DIBAC platforms (utilizing P1003 and P1021 exatecan topoisomerase I inhibitors) actively bypass the resistance profiles of Daiichi Sankyo’s DXd technology.

1. DB-1303 (HER2): NMPA BLA accepted. Targets full-spectrum expression (IHC 1+/2+/3+). FDA BLA submission scheduled for 2026 (BTD and FTD granted). Competes with Daiichi’s DS-8201 (Enhertu), RemeGen’s RC48, and Kelun-Biotech's A166. BioNTech holds global rights (ex-China/HK/Macao), while 3SBio (Sansom) executes domestic commercialization. Drug-to-Antibody Ratio (DAR) is 8. Uses Trastuzumab amino acid sequence.

2. DB-1311 (B7-H3): Phase III for mCRPC (readout 2028-2029) competing with Daiichi’s DS-7300. Holds ODD for ESCC/SCLC. Delivered an 11.3-month median PFS and 22.5-month mOS. Exhibited pristine safety with 1 Grade 2 ILD case among 110 patients at the 6mg/kg dose. DAR 6. In May 2026, Duality officially exercised its option to share US development costs and commercial profits with BioNTech. Relies on WuXi Biologics B7-H3 mAb license.

3. DB-1310 (HER3): Phase I/IIa. DAR 8. Targets novel epitope on Domain I. Generated an unconfirmed ORR of 43.5% and 18.89-month mOS in 3rd-line EGFR-mutant NSCLC. ILD rate of 4.1% in 246 patients. 100% retained global rights. Competes with Baili-Tianheng's BL-B01D1. Relies on Sinotau/Beijing Xiantong HER3 mAb license.

4. DB-1305 (TROP2): Phase I/IIa (TTM 3.5-5 years). FTD for Platinum-Resistant Ovarian Cancer. Generated 83.3% ORR when combined with Pumitamig. Competes with Kelun-Biotech's SKB264. BioNTech holds rights. DAR 4.

5. Expanded Pipeline: DB-1418 (EGFRxHER3, licensed to Avenzo ex-China/HK/Macao/Taiwan), DB-1419 (B7-H3xPD-L1, licensed from Darts Bio), DB-2304 (BDCA2 for SLE/CLE), DB-1312 (B7-H4, licensed from Nona Biosciences, 100% to BeiGene), DB-1324 (CDH17, GSK exclusive option ex-China), DB-1317 (ADAM9). Pre-clinical: DB-1329 (CDCP1), DB-1326 (TA-MUC1). Adcendo holds global DITAC options, Duality retains China/HK/Macao/Taiwan options.

B. IP Litigation & Corporate Governance Mechanics

* Duoxi Bio Patent Litigation: Duality faces IP volatility against domestic competitor Duoxi Bio regarding three patent applications. The Shanghai Intellectual Property Court dismissed all of Duoxi Bio's claims in December 2025. Two rulings are legally effective; one is currently appealed to the Supreme People's Court. The firm reports 0 pending employment arbitrations.

* Cap Table: Duality lacks a controlling shareholder. Lilly Asia Ventures (LAV USD) holds 13.03%, Chairman/CEO Dr. John Zhu (Zhu Zhongyuan) holds 7.31% via DualityBio Ltd., Shanghai Yingjia holds 7.14%, and King Star (Lin Xianghong) holds 5.89%. Strategic investors include WX Venture and AstraZeneca-CICC. Leadership includes CSO Dr. QIU Yang (former Daiichi Sankyo), CMO Dr. MU Hua, and SAB members Dr. Antoine Yver and Dr. Pasi A. Jänne.

C. Addressable Market (TAM/SAM) Projections

1. HER2 Segment: Global TAM projected from $6.70B (2024) to $43.50B (2035) at an 18.5% CAGR. The HER2-low SAM expands from 926.4K incident cases in 2024 to 1.20M in 2035 (China: 144.8K to 175.4K).

2. TROP2 Segment: Global TAM expanding from $1.50B (2024) to $42.50B (2035) at a 35.4% CAGR. TNBC SAM scales from 299.6K to 389.3K.

3. HER3/NSCLC Segment: Total NSCLC incidence grows from 2.21M (2024) to 2.92M (2035), with China accounting for 973.2K to 1.32M cases. The EGFR-mutant SAM expands from 615.1K to 821.6K.

4. B7-H3 Segment: Projected from $100M (2026) to $14.20B (2035) at a 59.7% CAGR. The mCRPC SAM grows from 468.2K to 733.0K.

HDIN Institutional Perspective

Duality Biotherapeutics' hyper-asset-light model is a mathematically exact mechanism for offloading capital risk, effectively insulating the balance sheet from a $303.82M gross operational burn. However, the exact variables generating this insulation—the 100% outsourced manufacturing network and the 75.36% revenue reliance on BioNTech—form the firm's central vulnerability. The exercising of the DB-1311 US profit-share option in May 2026 marks a required strategic evolution into co-commercialization. Yet, with 67.65% of all R&D procurement centralized in just 5 vendors, and the core WuXi XDC production pipeline increasingly exposed to shifting US biosecurity legislation, Duality is fundamentally trading clinical capital risk for systemic sovereign and supply chain risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."