Konica Minolta, Inc.: $333.4M Operating Profit Reversal Near Tokyo Headquarters as SaaS Pipeline Masks 3.6% Hardware Contraction

Date : 2026-06-15

Reading : 263

HDIN Executive Takeaways

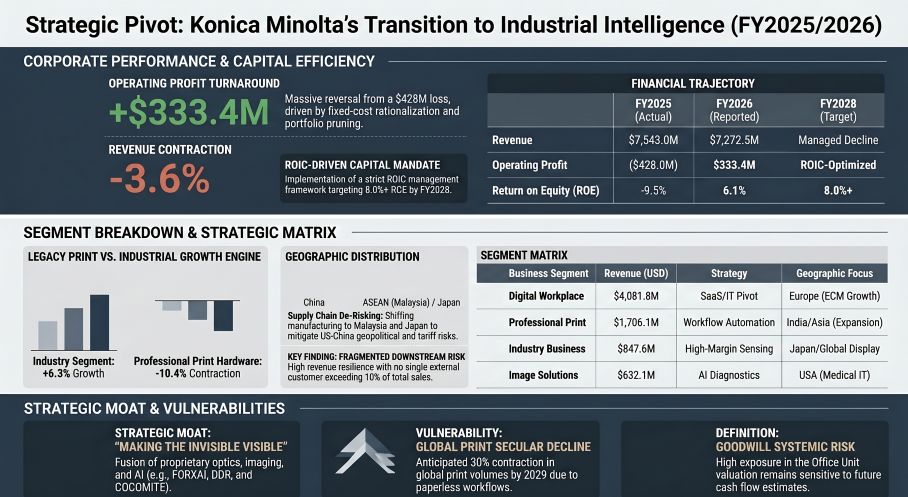

* Operating profit rebounded to $333.4 million (+4.58% margin), masking a 3.6% top-line contraction ($7,272.5 million) driven by a projected 30% secular decline in global electrophotographic print volumes by 2029.

* A $61.5 million facility in Melaka, Malaysia anchors an ASEAN supply chain decentralization, mitigating a $70.9 million gross US tariff hit, while memory chip stockpiling inflated inventory by 1.4% to $1,407.2 million.

* Structural deleveraging and a 6.1% ROE exceed FY2025 mandates, yet an $82.22 million net deferred tax asset and $540.91 million in un-impaired Office Unit goodwill expose the balance sheet to acute macroeconomic friction.

Figure Konica Minolta's Transition to Industrial intelligence (FY2025/2026)

Segmental Realities and Capital Allocation

Segmental Realities and Capital Allocation

Management executed a strict cost-reduction pivot under the “Turn Around 2025” strategy, shifting from a $428.0 million (JPY 64.0 billion) operating loss to a $333.4 million (JPY 49.8 billion) operating profit. This turnaround established a lower breakeven point by expanding gross margins by 150 basis points and contracting SG&A expenses by 60 basis points. The balance sheet reflects this stabilization: Return on Equity (ROE) achieved 6.1% (surpassing the 5.0% target and reversing a -9.5% deficit), while the equity ratio strengthened by 5.4 percentage points to 43.4%.

Konica Minolta, Inc. [TOKYO: 4902] generated $576.9 million (JPY 86.3 billion) in Operating Cash Flow, recovering from $341.6 million, backed by a $290.2 million pre-tax profit and $392.3 million in depreciation add-backs. Capital expenditures totaled $408.5 million, heavily weighted by the strategic repurchase of real estate trust beneficiary rights for the Tokyo Hino site. Free Cash Flow reached $349.0 million. The company converted all statutory financials at an FY2025 average rate of 1 USD = 149.5686 JPY.

Total consolidated revenue contracted by 3.6% year-over-year to $7,272.5 million (JPY 1,087.7 billion). Segmented operational dynamics are heavily polarized between hardware contraction and software expansion:

* Digital Workplace (56.1% of Revenue): Revenue contracted 1.0% to $4,081.8 million, while Operating Profit expanded 165.2% to $247.8 million. Growth relies on DW-DX unit software monetization via the “COCOMITE” manual creation platform and “tomoLinks” AI educational SaaS.

* Professional Print (23.5% of Revenue): Revenue dropped 10.4% to $1,706.1 million. Operating Profit recovered to $62.5 million from an $88.2 million loss. Commercial print operations emphasize the B2-size AccurioJet 30000, AccurioLabel series, and workflow automation via AccurioPro Flux and Dashboard software. The segment recorded a $41.73 million (JPY 6.24 billion) impairment and a $24.02 million (JPY 3.59 billion) provision to exit 26 entities under Marketing Services EMEA.

* Industry Business (11.6% of Revenue): Revenue expanded 6.3% to $847.6 million ($847.1 million noted in internal breakdowns). Operating Profit reached $148.9 million, reversing an $85.2 million loss. The unit monetizes zero-birefringence optical films (SANUQI, SAZMA) for OLED displays and hyperspectral imaging (Specim RETEX, Specim SX25).

* Image Solutions (8.7% of Revenue): Revenue fell 11.6% to $632.1 million, operating at an $8.9 million loss. Focus centers on Dynamic Digital Radiography (DDR), the SONIMAGE UX1 ultrasound system, and the FORXAI imaging IoT platform. The MOBOTIX AG divestiture incurred a $34.34 million (JPY 5.13 billion) impairment and a $33.42 million (JPY 5.0 billion) provision, ultimately settling with an $11.49 million gain.

Management radically contracted "Business Structural Improvement Expenses" to $7.70 million (JPY 1.15 billion), down from prior-year charges of $144.56 million (JPY 21.62 billion) and $135.06 million (JPY 20.2 billion) for selection and concentration. Consequently, the global workforce contracted by 1,268 full-time equivalents (3.5%) to 34,363 employees. Sector headcount allocations place 27,929 employees in Digital Workplace/Professional Print, 2,878 in Industry, 2,236 in Image Solutions, and 1,320 in Corporate. The Japan parent company retains 3,888 employees with an average annual salary of $56,437 (JPY 8.44 million), up 2.7% year-over-year.

R&D expensing validates an aggressive pivot toward data science and software. Out of a $366.24 million (JPY 54.77 billion) R&D budget, only $6.93 million (JPY 1.03 billion) in self-created intangibles was capitalized. The expensed budget allocated $213.28 million (JPY 31.9 billion) to Digital Workplace/Professional Print, $78.23 million (JPY 11.7 billion) to Industry, $35.44 million (JPY 5.3 billion) to Image Solutions, and $39.45 million (JPY 5.9 billion) to basic research. Future R&D mandates allocate over 20% of the budget to disruptive technologies, including perovskite solar cell barrier films co-developed with EneCoat Technologies.

Manufacturing Footprint and Geopolitical Supply Chains

Global sales values illustrate a stark regional divergence, heavily influenced by tariff friction and a strategic pivot away from Mainland China. Geopolitical volatility forced inventory levels up 1.4% to $1,407.2 million as the company stockpiled volatile memory chips and absorbed lead-time elongations from Red Sea conflicts, Suez Canal detours via the Cape of Good Hope, and the "2024 Problem" in Japanese trucking.

Table Geographic Revenue Distribution

Table Production Value by Segment

To counter supply chain chokepoints, Konica Minolta is re-shoring and decentralizing manufacturing. The ASEAN hub is anchored by the $61.5 million Konica Minolta Business Technologies (Malaysia) Sdn. Bhd. facility in Melaka. Chinese production remains divided between Dongguan (MFPs) and Dalian (lenses). Domestic Japanese production focuses on high-value IP: Kofu, Yamanashi manufactures toner; Toyokawa, Aichi handles mechatronics; and Sayama, Saitama engineers medical equipment.

Currency and trade policies enforce direct margin pressures. US tariffs inflated procurement costs by $70.9 million (JPY 10.6 billion), which mitigation efforts reduced to a net $35.4 million (JPY 5.3 billion) drag on operating profit. Foreign exchange sensitivities indicate a 1 JPY depreciation against the EUR increases operating profit by $3.34 million (JPY 500 million), and against the CNY by $6.69 million (JPY 1 billion). Conversely, a 1 JPY depreciation against the USD erodes operating profit by $0.67 million (JPY 100 million).

HDIN Institutional Verdict

Konica Minolta's strategic architecture relies entirely on the premise modeled by IDC: a 30% contraction in global electrophotographic print volumes by 2029, with monochrome falling to 68.9% and color to 83.3% of 2024 levels. While management has structurally de-risked the balance sheet of legacy M&A premiums—recording a mere $6.6 million impairment this cycle compared to a prior-year $341.7 million wipeout involving Radiant Vision Systems and MGI Digital Technology—critical vulnerabilities persist.

Total Goodwill and Intangibles stand at $1,222.01 million (JPY 182.77 billion). This comprises $897.31 million (JPY 134.20 billion) in Goodwill, $226.40 million (JPY 33.86 billion) in Software, $13.84 million (JPY 2.07 billion) in Technology IP, $10.52 million (JPY 1.57 billion) in Customer Relationships, and $73.93 million (JPY 11.05 billion) in Other Intangibles. The Audit Committee, chaired by Soichiro Sakuma alongside Independent Chair Takuko Sawada, flagged a highly subjective $540.91 million (JPY 80,903 million) goodwill concentration in the Office Unit. Tested against a $940.56 million (JPY 140,679 million) non-financial asset base using an 11.1% discount rate and 0.0% terminal growth rate, this represents the single largest equity shock risk if AI-agent workflows accelerate the paperless transition faster than anticipated.

Simultaneously, the parent entity recognized an $82.22 million (JPY 12,298 million) net Deferred Tax Asset, balanced against $332.33 million (JPY 49,707 million) in gross deductions and a $229.39 million (JPY 34,309 million) valuation allowance. The recoverability of this DTA is entirely dependent on sustained domestic profitability.

Debt restructuring demonstrates a defensive lock-in of capital. Total interest-bearing debt dropped $91 million to $2,203.9 million, with short-term borrowings aggressively paid down from $650.5 million to $458.3 million, funded by the issuance of $523.5 million (JPY 78.3 billion) in bonds. Off-balance sheet exposures remain contained: external third-party guarantees total $1.72 million (JPY 258 million), while a $52.91 million (JPY 7,914 million) guarantee covers US subsidiary lease obligations, alongside the elimination of a prior $6.88 million (JPY 1,029 million) Chinese medical subsidiary guarantee. A $1.09 billion (JPY 164,238 million) intercompany loan facility centralizes group liquidity, with $503.71 million (JPY 75,839 million) drawn and $591.02 million (JPY 88,398 million) unexecuted. Routine liabilities reflect $11.95 million (JPY 1,787 million) in warranty provisions, $1.97 million (JPY 294 million) in settlement income (down from $11.01 million), and Asset Retirement Obligations falling from $44.80 million (JPY 6,700 million) to $13.10 million (JPY 1,959 million) following $33.39 million (JPY 4,994 million) in site restoration utilization.

To force accountability, the Compensation Committee, chaired by Yoshihiko Kawamura, alongside Nomination Chair Masumi Minegishi, removed ESG metrics from CEO Toshimitsu Taiko's compensation. Executive pay shifted to a 40% Fixed / 30% Cash / 30% Stock model. The equity portion is strictly bifurcated: 40% linked to relative TSR and 60% tethered to the 8.0% Corporate Plan 2026-2028 ROE target. Despite decoupling ESG from compensation, the Board reported aggressive diversity and inclusion metrics: global female management reached 19.8% (12.2% parent), aiming for 26% globally and 18% domestically by 2030, drastically outperforming the 4-9% Japanese industry average. The parent company gender pay gap sits at 79.5% (total) and 79.0% (regular employees), while male childcare leave acquisition achieved 86.2%. Enterprise engagement scores ticked up to 7.1 from 6.8, supported by an internally tracked succession pool of 150 global talents. The mandate is clear: Konica Minolta will rely on advanced internal software networks (e.g., WIPO GREEN IP deployment, IQ-520/601 automation) to offset structural hardware decay and defend capital efficiency.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating profit rebounded to $333.4 million (+4.58% margin), masking a 3.6% top-line contraction ($7,272.5 million) driven by a projected 30% secular decline in global electrophotographic print volumes by 2029.

* A $61.5 million facility in Melaka, Malaysia anchors an ASEAN supply chain decentralization, mitigating a $70.9 million gross US tariff hit, while memory chip stockpiling inflated inventory by 1.4% to $1,407.2 million.

* Structural deleveraging and a 6.1% ROE exceed FY2025 mandates, yet an $82.22 million net deferred tax asset and $540.91 million in un-impaired Office Unit goodwill expose the balance sheet to acute macroeconomic friction.

Figure Konica Minolta's Transition to Industrial intelligence (FY2025/2026)

Segmental Realities and Capital AllocationManagement executed a strict cost-reduction pivot under the “Turn Around 2025” strategy, shifting from a $428.0 million (JPY 64.0 billion) operating loss to a $333.4 million (JPY 49.8 billion) operating profit. This turnaround established a lower breakeven point by expanding gross margins by 150 basis points and contracting SG&A expenses by 60 basis points. The balance sheet reflects this stabilization: Return on Equity (ROE) achieved 6.1% (surpassing the 5.0% target and reversing a -9.5% deficit), while the equity ratio strengthened by 5.4 percentage points to 43.4%.

Konica Minolta, Inc. [TOKYO: 4902] generated $576.9 million (JPY 86.3 billion) in Operating Cash Flow, recovering from $341.6 million, backed by a $290.2 million pre-tax profit and $392.3 million in depreciation add-backs. Capital expenditures totaled $408.5 million, heavily weighted by the strategic repurchase of real estate trust beneficiary rights for the Tokyo Hino site. Free Cash Flow reached $349.0 million. The company converted all statutory financials at an FY2025 average rate of 1 USD = 149.5686 JPY.

Total consolidated revenue contracted by 3.6% year-over-year to $7,272.5 million (JPY 1,087.7 billion). Segmented operational dynamics are heavily polarized between hardware contraction and software expansion:

* Digital Workplace (56.1% of Revenue): Revenue contracted 1.0% to $4,081.8 million, while Operating Profit expanded 165.2% to $247.8 million. Growth relies on DW-DX unit software monetization via the “COCOMITE” manual creation platform and “tomoLinks” AI educational SaaS.

* Professional Print (23.5% of Revenue): Revenue dropped 10.4% to $1,706.1 million. Operating Profit recovered to $62.5 million from an $88.2 million loss. Commercial print operations emphasize the B2-size AccurioJet 30000, AccurioLabel series, and workflow automation via AccurioPro Flux and Dashboard software. The segment recorded a $41.73 million (JPY 6.24 billion) impairment and a $24.02 million (JPY 3.59 billion) provision to exit 26 entities under Marketing Services EMEA.

* Industry Business (11.6% of Revenue): Revenue expanded 6.3% to $847.6 million ($847.1 million noted in internal breakdowns). Operating Profit reached $148.9 million, reversing an $85.2 million loss. The unit monetizes zero-birefringence optical films (SANUQI, SAZMA) for OLED displays and hyperspectral imaging (Specim RETEX, Specim SX25).

* Image Solutions (8.7% of Revenue): Revenue fell 11.6% to $632.1 million, operating at an $8.9 million loss. Focus centers on Dynamic Digital Radiography (DDR), the SONIMAGE UX1 ultrasound system, and the FORXAI imaging IoT platform. The MOBOTIX AG divestiture incurred a $34.34 million (JPY 5.13 billion) impairment and a $33.42 million (JPY 5.0 billion) provision, ultimately settling with an $11.49 million gain.

Management radically contracted "Business Structural Improvement Expenses" to $7.70 million (JPY 1.15 billion), down from prior-year charges of $144.56 million (JPY 21.62 billion) and $135.06 million (JPY 20.2 billion) for selection and concentration. Consequently, the global workforce contracted by 1,268 full-time equivalents (3.5%) to 34,363 employees. Sector headcount allocations place 27,929 employees in Digital Workplace/Professional Print, 2,878 in Industry, 2,236 in Image Solutions, and 1,320 in Corporate. The Japan parent company retains 3,888 employees with an average annual salary of $56,437 (JPY 8.44 million), up 2.7% year-over-year.

R&D expensing validates an aggressive pivot toward data science and software. Out of a $366.24 million (JPY 54.77 billion) R&D budget, only $6.93 million (JPY 1.03 billion) in self-created intangibles was capitalized. The expensed budget allocated $213.28 million (JPY 31.9 billion) to Digital Workplace/Professional Print, $78.23 million (JPY 11.7 billion) to Industry, $35.44 million (JPY 5.3 billion) to Image Solutions, and $39.45 million (JPY 5.9 billion) to basic research. Future R&D mandates allocate over 20% of the budget to disruptive technologies, including perovskite solar cell barrier films co-developed with EneCoat Technologies.

Manufacturing Footprint and Geopolitical Supply Chains

Global sales values illustrate a stark regional divergence, heavily influenced by tariff friction and a strategic pivot away from Mainland China. Geopolitical volatility forced inventory levels up 1.4% to $1,407.2 million as the company stockpiled volatile memory chips and absorbed lead-time elongations from Red Sea conflicts, Suez Canal detours via the Cape of Good Hope, and the "2024 Problem" in Japanese trucking.

Table Geographic Revenue Distribution

| Geographic Region | Revenue | % of Total | YoY Growth |

|---|---|---|---|

| Europe | $2,338.6M | 32.1% | -1.1% |

| United States | $1,855.1M | 25.5% | -7.1% |

| Japan | $1,164.8M | 16.0% | +0.7% |

| Asia (ex-China/Japan) | $785.4M | 10.8% | N/A |

| Mainland China | $597.7M | 8.2% | -13.3% |

Table Production Value by Segment

| Segment | Production Value | YoY Growth |

|---|---|---|

| Digital Workplace & Professional Print | $2,290.6M | -5.9% |

| Industry | $787.9M | +4.9% |

| Image Solutions | $126.1M | -31.5% |

To counter supply chain chokepoints, Konica Minolta is re-shoring and decentralizing manufacturing. The ASEAN hub is anchored by the $61.5 million Konica Minolta Business Technologies (Malaysia) Sdn. Bhd. facility in Melaka. Chinese production remains divided between Dongguan (MFPs) and Dalian (lenses). Domestic Japanese production focuses on high-value IP: Kofu, Yamanashi manufactures toner; Toyokawa, Aichi handles mechatronics; and Sayama, Saitama engineers medical equipment.

Currency and trade policies enforce direct margin pressures. US tariffs inflated procurement costs by $70.9 million (JPY 10.6 billion), which mitigation efforts reduced to a net $35.4 million (JPY 5.3 billion) drag on operating profit. Foreign exchange sensitivities indicate a 1 JPY depreciation against the EUR increases operating profit by $3.34 million (JPY 500 million), and against the CNY by $6.69 million (JPY 1 billion). Conversely, a 1 JPY depreciation against the USD erodes operating profit by $0.67 million (JPY 100 million).

HDIN Institutional Verdict

Konica Minolta's strategic architecture relies entirely on the premise modeled by IDC: a 30% contraction in global electrophotographic print volumes by 2029, with monochrome falling to 68.9% and color to 83.3% of 2024 levels. While management has structurally de-risked the balance sheet of legacy M&A premiums—recording a mere $6.6 million impairment this cycle compared to a prior-year $341.7 million wipeout involving Radiant Vision Systems and MGI Digital Technology—critical vulnerabilities persist.

Total Goodwill and Intangibles stand at $1,222.01 million (JPY 182.77 billion). This comprises $897.31 million (JPY 134.20 billion) in Goodwill, $226.40 million (JPY 33.86 billion) in Software, $13.84 million (JPY 2.07 billion) in Technology IP, $10.52 million (JPY 1.57 billion) in Customer Relationships, and $73.93 million (JPY 11.05 billion) in Other Intangibles. The Audit Committee, chaired by Soichiro Sakuma alongside Independent Chair Takuko Sawada, flagged a highly subjective $540.91 million (JPY 80,903 million) goodwill concentration in the Office Unit. Tested against a $940.56 million (JPY 140,679 million) non-financial asset base using an 11.1% discount rate and 0.0% terminal growth rate, this represents the single largest equity shock risk if AI-agent workflows accelerate the paperless transition faster than anticipated.

Simultaneously, the parent entity recognized an $82.22 million (JPY 12,298 million) net Deferred Tax Asset, balanced against $332.33 million (JPY 49,707 million) in gross deductions and a $229.39 million (JPY 34,309 million) valuation allowance. The recoverability of this DTA is entirely dependent on sustained domestic profitability.

Debt restructuring demonstrates a defensive lock-in of capital. Total interest-bearing debt dropped $91 million to $2,203.9 million, with short-term borrowings aggressively paid down from $650.5 million to $458.3 million, funded by the issuance of $523.5 million (JPY 78.3 billion) in bonds. Off-balance sheet exposures remain contained: external third-party guarantees total $1.72 million (JPY 258 million), while a $52.91 million (JPY 7,914 million) guarantee covers US subsidiary lease obligations, alongside the elimination of a prior $6.88 million (JPY 1,029 million) Chinese medical subsidiary guarantee. A $1.09 billion (JPY 164,238 million) intercompany loan facility centralizes group liquidity, with $503.71 million (JPY 75,839 million) drawn and $591.02 million (JPY 88,398 million) unexecuted. Routine liabilities reflect $11.95 million (JPY 1,787 million) in warranty provisions, $1.97 million (JPY 294 million) in settlement income (down from $11.01 million), and Asset Retirement Obligations falling from $44.80 million (JPY 6,700 million) to $13.10 million (JPY 1,959 million) following $33.39 million (JPY 4,994 million) in site restoration utilization.

To force accountability, the Compensation Committee, chaired by Yoshihiko Kawamura, alongside Nomination Chair Masumi Minegishi, removed ESG metrics from CEO Toshimitsu Taiko's compensation. Executive pay shifted to a 40% Fixed / 30% Cash / 30% Stock model. The equity portion is strictly bifurcated: 40% linked to relative TSR and 60% tethered to the 8.0% Corporate Plan 2026-2028 ROE target. Despite decoupling ESG from compensation, the Board reported aggressive diversity and inclusion metrics: global female management reached 19.8% (12.2% parent), aiming for 26% globally and 18% domestically by 2030, drastically outperforming the 4-9% Japanese industry average. The parent company gender pay gap sits at 79.5% (total) and 79.0% (regular employees), while male childcare leave acquisition achieved 86.2%. Enterprise engagement scores ticked up to 7.1 from 6.8, supported by an internally tracked succession pool of 150 global talents. The mandate is clear: Konica Minolta will rely on advanced internal software networks (e.g., WIPO GREEN IP deployment, IQ-520/601 automation) to offset structural hardware decay and defend capital efficiency.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."