Ajinomoto: FY2026 Divestiture of Althea and $2,005.8M M&A Pivot Signal Structural Transition Toward 19.0% EBITDA Target

Date : 2026-06-15

Reading : 387

HDIN Executive Takeaways

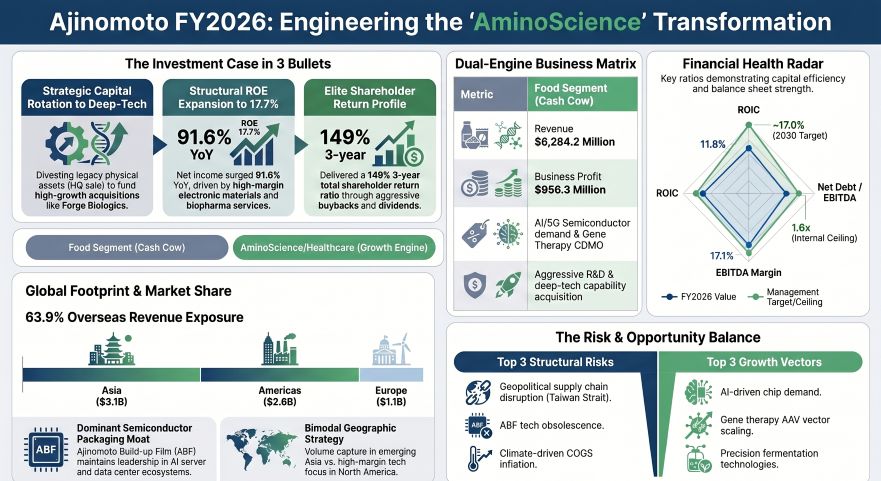

* Consolidated sales reached $10,588.6 million (+3.5% YoY), with core Business Profit expanding 13.7% YoY to $1,211.2 million, propelled directly by a 45.1% YoY profit expansion within the Healthcare & Electronic Materials segment.

* Management earmarked $5,014.4 million (750.0 billion JPY) for 2023–2030 CapEx alongside a dedicated $2,005.8 million (300.0 billion JPY) M&A budget, offsetting capital dilution through the $27.0 million divestiture of Ajinomoto Althea, Inc. and a $301.5 million (45.1 billion JPY) corporate headquarters sale.

* A 1.5°C climate transition exposes the firm to $421.2 million (63.0 billion JPY) in annual carbon tax liabilities by 2050, accelerating a shift to AI-driven precision fermentation to decouple cost of goods sold from the 12 agricultural commodities dictating 70% of current global procurement.

Figure Ajinomoto FY2026: Engineering the 'AminoScience' Transformation

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Ajinomoto Co., Inc. [TYO: 2802] operates a dual-engine architecture, utilizing a mature Fast-Moving Consumer Goods (FMCG) cash base to fund capital-intensive Biotechnology and Fine Chemicals (B&FC) expansion. FY2026 organic growth registered at 3.7%, trailing management's >5.0% baseline target for the FY2022–2025 period. The corporate objective is to recalibrate the B&FC to Food profit ratio from 1:2 (FY2021) to 1:1 by FY2030. FY2027 guidance targets $11,519.8 million (1,723.0 billion JPY) in revenue and $1,317.1 million (197.0 billion JPY) in core Business Profit.

Table Segment-Level Financial Performance, Asset Growth, and Capital Allocation Overview

*Note: All financial metrics converted at 1 USD = 149.5686 JPY.*

Infrastructure Layout and Regional Moats

Total FY2026 R&D expenditure stood at $214.67 million (32,108 million JPY), with $69.41 million (32.3%) reserved for centralized corporate frontier research. The company commands an intellectual property portfolio of 4,280 global patents, monetizing proprietary AminoScience platforms including Deliciousness Design Technology, AJI-EMap, AJIPHASE, CORYNEX, and AJICAP.

Overseas revenue constitutes 63.9% of the consolidated top line, distributed across key hubs:

* Japan ($3,822.3M): Production at Kawasaki, Tokai, Kyushu, Ajinomoto Fine-Techno (ABF), and Ajinomoto Frozen Foods. The domestic market relies on SKU rationalization and premiumization to defend margins against demographic contraction.

* Asia ($3,106.3M): High-volume hubs situated in Thailand (Ajinomoto Betagro Frozen Foods), Indonesia, Vietnam, the Philippines, and Malaysia. Strategic B2B ingredients and B2C flavor localization drive regional volume. Additional global nodes operate in Brazil, Peru, and Nigeria.

* Americas ($2,556.7M): Footprint spans Ajinomoto Foods North America (AFNA) and the acquired Forge Biologics facility (gene therapy CDMO).

* Europe ($1,102.5M): Anchored by Ajinomoto OmniChem (Belgium) for CDMO services and Ajinomoto Frozen Foods France, extending Asian frozen food distribution into mainstream retail.

Ecosystem control is enforced via strategic equity tie-ups, including a 33.33% stake in Promasidor Holdings, cross-shareholdings in Seven & i Holdings ($42.5 million / 6,363 million JPY), Aeon, Itochu Shokuhin, and Kato Sangyo, and an equity-method joint venture in EA Pharma Co., Ltd. Pipeline velocity is augmented via corporate venture capital hubs in Boston and Silicon Valley, backed by localized R&D tie-ups with Astellas Pharma, Enhanced Medical Nutrition, v2food, Kai Technology, OKAN, and Japan's NEDO (focusing on AI precision fermentation). Consumer testing operates via entities like Atlr.72 in Singapore.

Financial Forensics and Off-Balance Sheet Variables

Ajinomoto Co., Inc. dictates a strict 7.0% WACC threshold. In FY2026, the firm delivered a 11.8% ROIC, establishing a +4.8% economic spread. Total assets scale to $12,117.2 million against $5,644.7 million in total equity, yielding a 42.5% equity ratio. Interest-bearing debt sits at $2,817.1 million, suppressing the Net Debt/EBITDA multiple to 1.6x (below the 2.0x policy ceiling).

Bottom-line net income surged 91.6% YoY to $900.4 million, fortified by a $271.7 million (40.6 billion JPY) pre-tax gain from the corporate headquarters sale. The company recorded $1,600.3 million in Operating Cash Flow and $594.5 million in depreciation and amortization. Investing Cash Flow measured -$563.1 million, generating over $1.03 billion in Free Cash Flow. Financing outflows totaled -$1,508.4 million, optimizing year-end cash equivalents at $713.3 million. Capital distributions included $289.0 million in dividends (targeting 50 JPY/share for FY2027) and $869.2 million in share repurchases, generating a 3-year TSR of 149%. Reported FY2026 total CapEx stood at $690.1 million, despite stated operational allocations reaching $869.2 million (130.0 billion JPY).

Impairment Architecture and Contingencies:

Total consolidated goodwill is $829.39 million (124,051 million JPY). The $281.44 million (42,095 million JPY) Gene Therapy CDMO goodwill operates with a margin-of-error headroom of $123.28 million (18,439 million JPY); an upward revision of 1.4% to its 18.7% pre-tax discount rate triggers structural impairment. The AFNA goodwill of $235.08 million (35,161 million JPY) maintains $296.90 million (44,407 million JPY) in headroom, triggering impairment at a 3.1% discount rate hike. Prior year (FY2025) impairments included $199.51 million (29,840 million JPY) tied to the Althea divestiture, of which $139.82 million (20,913 million JPY) was goodwill.

FY2026 balance sheet friction includes:

* Fixed asset write-downs: $56.50 million (8,450 million JPY), spanning machinery ($30.97M / 4,632M JPY) and buildings ($17.30M / 2,588M JPY).

* Loss on fixed asset disposal: $34.21 million (5,117 million JPY).

* Asset Retirement Obligations (ARO): Escalated from $8.41 million (1,258 million JPY) to $24.31 million (3,636 million JPY).

* Environmental Provisions: $8.03 million (1,201 million JPY).

* Litigation Provision: Contracted to $11.01 million (1,647 million JPY) from $13.44 million (2,010 million JPY). Off-balance-sheet guarantees tally $78.27 million (11,707 million JPY).

* Taxation: $2,852.98 million (426,716 million JPY) in unrecognized deferred tax liabilities (DTL) tied to overseas temporary differences. Exposure to the 15% Global Minimum Tax (IIR/QDMTT) remains immaterial.

Pension Obligation Spread:

The domestic defined benefit plan functions as a massive structural shield, carrying a present value obligation of $1,109.27 million (165,912 million JPY) against a $1,805.86 million (270,100 million JPY) fair value of assets, suppressed by a $511.46 million (76,499 million JPY) accounting asset ceiling. Overseas plans represent a net liability of $176.69 million (26,428 million JPY) based on $267.76 million (40,049 million JPY) in obligations and $100.87 million (15,087 million JPY) in assets. A -0.1% discount rate adjustment (from 3.3% domestic / 4.9% overseas) inflates domestic obligations by $13.26 million (1,983 million JPY) and overseas obligations by $3.11 million (465 million JPY).

Supply Chain ESG and Operational Governance

Ajinomoto Co., Inc. identifies 12 High Impact Commodities (HIC) controlling 70% of baseline procurement: sugarcane, cassava, corn, raw milk, soybeans, rapeseed, rice, beef, coffee, palm oil, copper, and crude oil. Under a 4°C warming scenario, extreme weather events dictating agricultural yield erosion project a negative financial impact of $60.2 million (9.0 billion JPY) annually by 2050, alongside a $26.7 million (4.0 billion JPY) penalty from fossil fuel inflation.

In a heavily regulated 1.5°C scenario, systemic carbon taxation presents an annual liability of $180.5 million (27.0 billion JPY) by 2030, escalating to $421.2 million (63.0 billion JPY) by 2050. Management is responding via $86.9 million in renewable CapEx, supply chain cycle counting integration, and SBTi-certified mandates:

* Scope 1 & 2 emissions reduction of 50.4%, Scope 3 reduction of 30%, and FLAG Scope 3 reduction of 36.4% by 2030 (2018 baseline). Target 90% aggregate cut by 2050.

* Zero deforestation by December 31, 2025. 100% sustainable sourcing for critical raw materials by 2030.

* 15% reduction in total water usage by FY2040. Zero plastic waste, 99% resource recovery, and a 50% food loss reduction by 2030.

Governance Architecture:

The 10-member Board of Directors features 6 independent external directors (60%) and is chaired by external director Kimie Iwata. Female officer representation stands at 29.0%. Both the Nomination (5 members) and Compensation (4 members) committees are 100% independent. The Audit Committee mixes 4 external and 1 internal director. Corporate Behavior was reorganized into the Group Compliance Committee (GCC), alongside the establishment of a C-level CHRO.

Executive compensation dictates a 25% Base, 25% STI (pegged 33.3% to Revenue, 66.7% to Core Business Profit), and 50% LTI framework. The FY2026–2028 LTI architecture enforces:

* Economic (60%): 12.4% ROIC (30%), Relative TSR vs. TOPIX at 1.0 (30%).

* Social (20%): GHG reduction mandates (10%), extension of healthy life expectancy to 9.8 billion people (10%).

* Intangible (20%): 86% Employee Engagement (10%), 30% Global Female Manager Ratio (5%), 7% Corporate Brand Value CAGR vs. FY2022 (5%).

Internal friction surfaced via a 78% Employee Engagement Score, missing the 80% FY2026 target due to bureaucratic decision-making speed. Management deployed an AI-assisted "Ya-He-Ka" framework to eliminate 600 inefficient processes, subsequently raising the 2030 engagement target to 88%.

HDIN Institutional Verdict

Ajinomoto Co., Inc. is executing a textbook structural rerating. The aggressive $199.51 million FY2025 write-down of Althea followed by its $27.0 million divestiture proves management will cut operational deadweight to defend its 11.8% ROIC. However, the $11,519.8 million FY2027 revenue target faces distinct execution headwinds given FY2026 organic growth stalled at 3.7%, lagging the 5.0% mandate. With the Gene Therapy CDMO goodwill sitting precariously on a $123.28 million margin of error against an 18.7% discount rate, the firm’s march toward a 19.0% EBITDA margin is entirely reliant on the continued hyper-scaling of ABF substrates and pricing elasticity holding firm against $421.2 million in looming 2050 carbon tax liabilities.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Consolidated sales reached $10,588.6 million (+3.5% YoY), with core Business Profit expanding 13.7% YoY to $1,211.2 million, propelled directly by a 45.1% YoY profit expansion within the Healthcare & Electronic Materials segment.

* Management earmarked $5,014.4 million (750.0 billion JPY) for 2023–2030 CapEx alongside a dedicated $2,005.8 million (300.0 billion JPY) M&A budget, offsetting capital dilution through the $27.0 million divestiture of Ajinomoto Althea, Inc. and a $301.5 million (45.1 billion JPY) corporate headquarters sale.

* A 1.5°C climate transition exposes the firm to $421.2 million (63.0 billion JPY) in annual carbon tax liabilities by 2050, accelerating a shift to AI-driven precision fermentation to decouple cost of goods sold from the 12 agricultural commodities dictating 70% of current global procurement.

Figure Ajinomoto FY2026: Engineering the 'AminoScience' Transformation

Segmental Realities and Margin CompressionAjinomoto Co., Inc. [TYO: 2802] operates a dual-engine architecture, utilizing a mature Fast-Moving Consumer Goods (FMCG) cash base to fund capital-intensive Biotechnology and Fine Chemicals (B&FC) expansion. FY2026 organic growth registered at 3.7%, trailing management's >5.0% baseline target for the FY2022–2025 period. The corporate objective is to recalibrate the B&FC to Food profit ratio from 1:2 (FY2021) to 1:1 by FY2030. FY2027 guidance targets $11,519.8 million (1,723.0 billion JPY) in revenue and $1,317.1 million (197.0 billion JPY) in core Business Profit.

Table Segment-Level Financial Performance, Asset Growth, and Capital Allocation Overview

| Segment | Revenue | Profit | Assets (YoY Change) | CapEx | R&D |

|---|---|---|---|---|---|

| Seasonings & Foods | $6,264.2M | $956.3M | $4,848.7M (+$477.4M / 71.4B JPY YoY) | $391.4M (58.5B JPY) | $56.08M (26.1% of total) |

| Frozen Foods | $1,941.0M | $56.5M (-35.0% YoY) | $1,451.4M (+$70.2M / 10.5B JPY YoY) | $71.8M (10.7B JPY) | $13.08M (6.1% of total) |

| Healthcare & Electronic Materials | $2,283.3M | $442.6M (+45.1% YoY) | $3,214.1M (+$188.5M / 28.2B JPY YoY) | $186.1M (27.8B JPY) | $75.50M (35.2% of total) |

| Others | $100.1M | $40.5M | N/A | N/A | $0.59M (0.3% of total) |

Infrastructure Layout and Regional Moats

Total FY2026 R&D expenditure stood at $214.67 million (32,108 million JPY), with $69.41 million (32.3%) reserved for centralized corporate frontier research. The company commands an intellectual property portfolio of 4,280 global patents, monetizing proprietary AminoScience platforms including Deliciousness Design Technology, AJI-EMap, AJIPHASE, CORYNEX, and AJICAP.

Overseas revenue constitutes 63.9% of the consolidated top line, distributed across key hubs:

* Japan ($3,822.3M): Production at Kawasaki, Tokai, Kyushu, Ajinomoto Fine-Techno (ABF), and Ajinomoto Frozen Foods. The domestic market relies on SKU rationalization and premiumization to defend margins against demographic contraction.

* Asia ($3,106.3M): High-volume hubs situated in Thailand (Ajinomoto Betagro Frozen Foods), Indonesia, Vietnam, the Philippines, and Malaysia. Strategic B2B ingredients and B2C flavor localization drive regional volume. Additional global nodes operate in Brazil, Peru, and Nigeria.

* Americas ($2,556.7M): Footprint spans Ajinomoto Foods North America (AFNA) and the acquired Forge Biologics facility (gene therapy CDMO).

* Europe ($1,102.5M): Anchored by Ajinomoto OmniChem (Belgium) for CDMO services and Ajinomoto Frozen Foods France, extending Asian frozen food distribution into mainstream retail.

Ecosystem control is enforced via strategic equity tie-ups, including a 33.33% stake in Promasidor Holdings, cross-shareholdings in Seven & i Holdings ($42.5 million / 6,363 million JPY), Aeon, Itochu Shokuhin, and Kato Sangyo, and an equity-method joint venture in EA Pharma Co., Ltd. Pipeline velocity is augmented via corporate venture capital hubs in Boston and Silicon Valley, backed by localized R&D tie-ups with Astellas Pharma, Enhanced Medical Nutrition, v2food, Kai Technology, OKAN, and Japan's NEDO (focusing on AI precision fermentation). Consumer testing operates via entities like Atlr.72 in Singapore.

Financial Forensics and Off-Balance Sheet Variables

Ajinomoto Co., Inc. dictates a strict 7.0% WACC threshold. In FY2026, the firm delivered a 11.8% ROIC, establishing a +4.8% economic spread. Total assets scale to $12,117.2 million against $5,644.7 million in total equity, yielding a 42.5% equity ratio. Interest-bearing debt sits at $2,817.1 million, suppressing the Net Debt/EBITDA multiple to 1.6x (below the 2.0x policy ceiling).

Bottom-line net income surged 91.6% YoY to $900.4 million, fortified by a $271.7 million (40.6 billion JPY) pre-tax gain from the corporate headquarters sale. The company recorded $1,600.3 million in Operating Cash Flow and $594.5 million in depreciation and amortization. Investing Cash Flow measured -$563.1 million, generating over $1.03 billion in Free Cash Flow. Financing outflows totaled -$1,508.4 million, optimizing year-end cash equivalents at $713.3 million. Capital distributions included $289.0 million in dividends (targeting 50 JPY/share for FY2027) and $869.2 million in share repurchases, generating a 3-year TSR of 149%. Reported FY2026 total CapEx stood at $690.1 million, despite stated operational allocations reaching $869.2 million (130.0 billion JPY).

Impairment Architecture and Contingencies:

Total consolidated goodwill is $829.39 million (124,051 million JPY). The $281.44 million (42,095 million JPY) Gene Therapy CDMO goodwill operates with a margin-of-error headroom of $123.28 million (18,439 million JPY); an upward revision of 1.4% to its 18.7% pre-tax discount rate triggers structural impairment. The AFNA goodwill of $235.08 million (35,161 million JPY) maintains $296.90 million (44,407 million JPY) in headroom, triggering impairment at a 3.1% discount rate hike. Prior year (FY2025) impairments included $199.51 million (29,840 million JPY) tied to the Althea divestiture, of which $139.82 million (20,913 million JPY) was goodwill.

FY2026 balance sheet friction includes:

* Fixed asset write-downs: $56.50 million (8,450 million JPY), spanning machinery ($30.97M / 4,632M JPY) and buildings ($17.30M / 2,588M JPY).

* Loss on fixed asset disposal: $34.21 million (5,117 million JPY).

* Asset Retirement Obligations (ARO): Escalated from $8.41 million (1,258 million JPY) to $24.31 million (3,636 million JPY).

* Environmental Provisions: $8.03 million (1,201 million JPY).

* Litigation Provision: Contracted to $11.01 million (1,647 million JPY) from $13.44 million (2,010 million JPY). Off-balance-sheet guarantees tally $78.27 million (11,707 million JPY).

* Taxation: $2,852.98 million (426,716 million JPY) in unrecognized deferred tax liabilities (DTL) tied to overseas temporary differences. Exposure to the 15% Global Minimum Tax (IIR/QDMTT) remains immaterial.

Pension Obligation Spread:

The domestic defined benefit plan functions as a massive structural shield, carrying a present value obligation of $1,109.27 million (165,912 million JPY) against a $1,805.86 million (270,100 million JPY) fair value of assets, suppressed by a $511.46 million (76,499 million JPY) accounting asset ceiling. Overseas plans represent a net liability of $176.69 million (26,428 million JPY) based on $267.76 million (40,049 million JPY) in obligations and $100.87 million (15,087 million JPY) in assets. A -0.1% discount rate adjustment (from 3.3% domestic / 4.9% overseas) inflates domestic obligations by $13.26 million (1,983 million JPY) and overseas obligations by $3.11 million (465 million JPY).

Supply Chain ESG and Operational Governance

Ajinomoto Co., Inc. identifies 12 High Impact Commodities (HIC) controlling 70% of baseline procurement: sugarcane, cassava, corn, raw milk, soybeans, rapeseed, rice, beef, coffee, palm oil, copper, and crude oil. Under a 4°C warming scenario, extreme weather events dictating agricultural yield erosion project a negative financial impact of $60.2 million (9.0 billion JPY) annually by 2050, alongside a $26.7 million (4.0 billion JPY) penalty from fossil fuel inflation.

In a heavily regulated 1.5°C scenario, systemic carbon taxation presents an annual liability of $180.5 million (27.0 billion JPY) by 2030, escalating to $421.2 million (63.0 billion JPY) by 2050. Management is responding via $86.9 million in renewable CapEx, supply chain cycle counting integration, and SBTi-certified mandates:

* Scope 1 & 2 emissions reduction of 50.4%, Scope 3 reduction of 30%, and FLAG Scope 3 reduction of 36.4% by 2030 (2018 baseline). Target 90% aggregate cut by 2050.

* Zero deforestation by December 31, 2025. 100% sustainable sourcing for critical raw materials by 2030.

* 15% reduction in total water usage by FY2040. Zero plastic waste, 99% resource recovery, and a 50% food loss reduction by 2030.

Governance Architecture:

The 10-member Board of Directors features 6 independent external directors (60%) and is chaired by external director Kimie Iwata. Female officer representation stands at 29.0%. Both the Nomination (5 members) and Compensation (4 members) committees are 100% independent. The Audit Committee mixes 4 external and 1 internal director. Corporate Behavior was reorganized into the Group Compliance Committee (GCC), alongside the establishment of a C-level CHRO.

Executive compensation dictates a 25% Base, 25% STI (pegged 33.3% to Revenue, 66.7% to Core Business Profit), and 50% LTI framework. The FY2026–2028 LTI architecture enforces:

* Economic (60%): 12.4% ROIC (30%), Relative TSR vs. TOPIX at 1.0 (30%).

* Social (20%): GHG reduction mandates (10%), extension of healthy life expectancy to 9.8 billion people (10%).

* Intangible (20%): 86% Employee Engagement (10%), 30% Global Female Manager Ratio (5%), 7% Corporate Brand Value CAGR vs. FY2022 (5%).

Internal friction surfaced via a 78% Employee Engagement Score, missing the 80% FY2026 target due to bureaucratic decision-making speed. Management deployed an AI-assisted "Ya-He-Ka" framework to eliminate 600 inefficient processes, subsequently raising the 2030 engagement target to 88%.

HDIN Institutional Verdict

Ajinomoto Co., Inc. is executing a textbook structural rerating. The aggressive $199.51 million FY2025 write-down of Althea followed by its $27.0 million divestiture proves management will cut operational deadweight to defend its 11.8% ROIC. However, the $11,519.8 million FY2027 revenue target faces distinct execution headwinds given FY2026 organic growth stalled at 3.7%, lagging the 5.0% mandate. With the Gene Therapy CDMO goodwill sitting precariously on a $123.28 million margin of error against an 18.7% discount rate, the firm’s march toward a 19.0% EBITDA margin is entirely reliant on the continued hyper-scaling of ABF substrates and pricing elasticity holding firm against $421.2 million in looming 2050 carbon tax liabilities.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."