Eisai: 2026 Capex Realignment Near Kawashima and European Hubs as $5,518.4 Million Revenue Signals Structural Neurological Pivot

Date : 2026-06-16

Reading : 320

HDIN Executive Takeaways

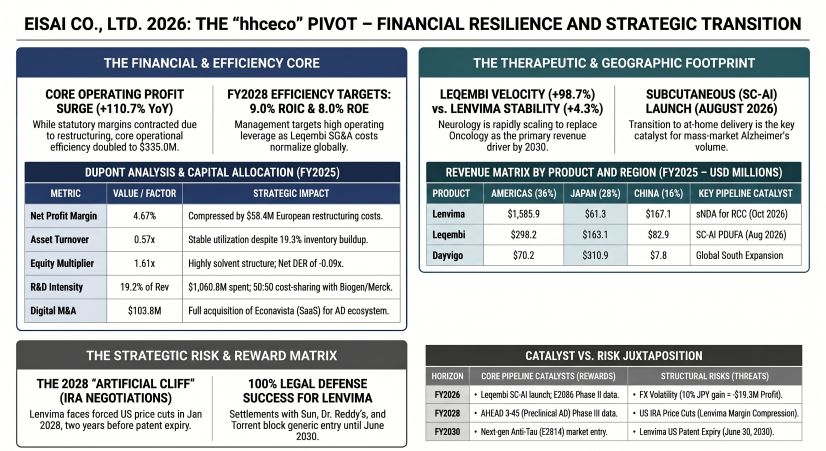

* Eisai Co., Ltd. [TYO: 4523] posted FY2025 revenue of $5,518.4 million (+4.6% YoY) against a 18.8% statutory operating profit contraction to $295.1 million, absorbing $58.4 million in European restructuring and $1,057.7 million in Merck & Co. profit-sharing.

* Wholesaler concentration presents acute risk with McKesson Corporation, Cencora, Inc., and Medipal Holdings driving $1,475.0 million (26.7% of sales), mitigated by decentralized API buffers across Gifu, Jiangsu, and Vizag.

* Despite 110.7% core operating profit expansion, long-term ROE (currently 4.4%) faces strict compression from 2028 US Inflation Reduction Act pricing caps on the $2,289.9 million Lenvima asset.

Figure EISAI 2026: THE hhceco PIVOT - FINANCIAL RESILIENCE AND STRATEGIC TRANSITION

Segmental Realities and Margin Compression

Eisai Co., Ltd. operates an asymmetric revenue matrix dominated by its $5,420.8 million (98.2%) Pharmaceutical Business, leaving Other Business at $97.6 million (1.8%). Top-line expansion is overwhelmingly leveraged to the $2,424.8 million Oncology and $1,742.1 million Neurology portfolios. FY2025 foreign exchange conversions anchor at 1 USD = 149.5686 JPY.

Table 1: Revenue Architecture and Geographic Stratification

Table 2: Operating Leverage, Margin Dynamics, and Cash Conversion

Table 3: Balance Sheet Capitalization and Provisions Risk

Table 4: 2026-2028 Forward Guidance and IP M&A

Infrastructure Layout and Regional Moats

Eisai Co., Ltd. operates a highly decentralized global supply chain, systematically mitigating single-source dependency. Operations in Japan are anchored by the Tsukuba Research Laboratories and Kobe Research Laboratories. Domestic production relies on the Kawashima Industrial Park (Gifu) and the Kashima Plant (Ibaraki), supplemented by a targeted $42.8 million (JPY 6.4 billion) capital expenditure program at the EA Pharma Fukushima Plant extending through March 2029.

In the Americas, genetic-guided dementia and oncology discovery are isolated at the Exton Site (Pennsylvania) and G2D2 (Massachusetts). European operations, localized at the European Knowledge Centre (UK), are currently executing a £50 million capacity expansion through March 2030 to support commercial rollouts, parallel to the acquisition of EMEA rights for taletrectinib. Asian penetration utilizes localized nodes at the Suzhou Plant (Jiangsu) and Liaoning Plant in China, counteracting volume-based procurement pressures. Global South access is routed via PT Eisai Indonesia and the Eisai Knowledge Centre in Vizag, India, which has supplied 2.81 billion DEC tablets across 33 countries to the World Health Organization at a strict zero-price mandate. Total capital expenditure for FY2025 reached $138.5 million (JPY 20.7 billion).

The corporate "hhceco" transition is governed by massive digital asset accumulation. The company capitalized $15.2 million (JPY 2.2 billion) in software during FY2025, bringing the standalone software balance to $95.3 million (JPY 14.3 billion). This infrastructure supports a multi-layered digital platform linking Econavista's Liferhythm Navi, Arteryex Inc.'s Pashatto Karte, Teoria Technologies Inc.'s Teotoru, and the Yin Fa Tong platform in China. Internally, HR analytics are optimized via Kaonavi systems.

Ecological controls display rigid adherence to 2030 targets. Eisai Co., Ltd. achieved a 51.6% reduction in Scope 1 and 2 emissions against a 2019 baseline (targeting 55%), running on 98.7% renewable energy (targeting 100%). In Japan, 100% of the commercial sales fleet utilizes hybrid or electric vehicles. However, Scope 3 Category 1 emissions expanded by 80.9%, exposing supply-chain carbon inelasticity. The company aims for a 7% reduction in water intake and waste generation by 2030 against a 2023 baseline.

Legal moats defending Lenvima until its June 30, 2030, US exclusivity expiration are solidified via settlements with SUN Pharmaceutical Industries Ltd. & Inc. (March 21, 2024), Dr. Reddy’s Laboratories, Ltd. & Inc. (September 22, 2025), and Torrent Pharmaceuticals Ltd. (November 6, 2025). The sole immediate threat is a pending appellate challenge from Shilpa Medicare Limited. Clinical velocities are timed precisely: the Leqembi subcutaneous auto-injector (SC-AI) holds a US FDA PDUFA date of August 24, 2026, with a China BLA priority review accepted in January 2026, and Japan filing completed in November 2025. Oncology replacement Lenvima+Belzutifan holds an October 4, 2026, US PDUFA date (Japan filing March 2026). The neurological pipeline is padded by E2814 (anti-MTBR tau antibody, Fast Track September 2025), E2086 (Selective Orexin 2 Receptor Agonist, Orphan Drug February 2026), and EA8001 (evenamide, Phase III). Additionally, the company previously executed a $650 million unutilized upfront refund from Bristol Myers Squibb to regain complete control of MORAb-202.

HDIN Institutional Verdict

An objective audit of Eisai Co., Ltd. exposes a highly aggressive 50:50 externalization model driving R&D efficiency, partnered with Biogen Inc. and Merck & Co. The company limits systemic exposure by paying Merck $1,057.7 million (JPY 158.2 billion) in profit shares, recorded under SG&A, ensuring high-margin throughput despite limiting standalone upside.

However, macroeconomic friction exposes critical vulnerabilities. Customer concentration is severe, with McKesson Corporation ($575.2 million / 10.42%), Cencora, Inc. ($504.0 million), and Medipal Holdings ($395.8 million) commanding 26.7% of global volume. Foreign exchange sensitivity is acute; a 10% JPY appreciation translates directly to a $4.2 million pre-tax profit contraction against the USD, and $15.1 million against the EUR.

The 11-member Board of Directors maintains a 63.6% independent majority (7 outside directors, 4 internal), chaired by outside director Fumihiko Ike, while CEO Haruo Naito controls execution. Female representation sits at 17.9% (2 members), trailing the 30% internal target. Audit oversight is managed by Sawaharu Kanai, backed by Toru Moriyama, Ryota Miura, and Ryoko Ueda.

Executive compensation ($8.87 million / JPY 1,327 million total) operates on a 50% to 67% variable schema. The Short-Term Cash Bonus A achieved a 103% payout, driven by a 50/50 split weighting 2/3 on financial metrics (93% achievement) and 1/3 on non-financial metrics (115% R&D progress, 133% Leqembi volume). Crucially, the Compensation Committee enforced a 0% payout on the Long-Term Incentive (split 70% in-tenure, 30% retirement). Management missed the 3-year ESG EBIT target ($2,409.6 million actual vs. $2,862.2 million target), vastly underperformed the Relative PBR benchmark (1.42 actual vs. 3.56 target), and achieved exactly 6 out of 17 defined ESG goals.

Capital distribution among 291.6 million outstanding shares is anchored by Domestic Financial Institutions at 34.17% (The Master Trust Bank of Japan, Ltd. at 18.55%, Custody Bank of Japan, Ltd. at 9.99%) and Foreign Institutions at 32.36% (State Street Bank and Trust Company at 5.31%, JPMorgan Securities at 2.67%). Other domestic corporations hold 4.62%, while 100,451 retail investors control 22.58%. While management projects $6,685.9 million in FY2028 revenue, the impending January 2028 Medicare price caps and China’s National Reimbursement Drug List mandates fundamentally threaten the inelasticity of their primary cash engines.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Eisai Co., Ltd. [TYO: 4523] posted FY2025 revenue of $5,518.4 million (+4.6% YoY) against a 18.8% statutory operating profit contraction to $295.1 million, absorbing $58.4 million in European restructuring and $1,057.7 million in Merck & Co. profit-sharing.

* Wholesaler concentration presents acute risk with McKesson Corporation, Cencora, Inc., and Medipal Holdings driving $1,475.0 million (26.7% of sales), mitigated by decentralized API buffers across Gifu, Jiangsu, and Vizag.

* Despite 110.7% core operating profit expansion, long-term ROE (currently 4.4%) faces strict compression from 2028 US Inflation Reduction Act pricing caps on the $2,289.9 million Lenvima asset.

Figure EISAI 2026: THE hhceco PIVOT - FINANCIAL RESILIENCE AND STRATEGIC TRANSITION

Segmental Realities and Margin Compression

Eisai Co., Ltd. operates an asymmetric revenue matrix dominated by its $5,420.8 million (98.2%) Pharmaceutical Business, leaving Other Business at $97.6 million (1.8%). Top-line expansion is overwhelmingly leveraged to the $2,424.8 million Oncology and $1,742.1 million Neurology portfolios. FY2025 foreign exchange conversions anchor at 1 USD = 149.5686 JPY.

Table 1: Revenue Architecture and Geographic Stratification

| Segment / Geography | FY2025 Revenue (USD) | FY2025 Revenue (JPY) | YoY Variance / Weight |

| Consolidated Total | $5,518.4 million | JPY 825.4 billion | +4.6% YoY |

| Guidance Target | $5,281.9 million | JPY 790.0 billion | 4.5% Beat |

| Lenvima (Global) | $2,289.9 million | JPY 342.5 billion | +4.3% YoY |

| - Lenvima (US) | $1,585.9 million | - | - |

| - Lenvima (EMEA, incl. Kisplyx) | $328.9 million | - | - |

| - Lenvima (China) | $167.1 million | - | - |

| Leqembi (Global) | $588.4 million | JPY 88.0 billion | +98.7% YoY |

| - Leqembi (US) | $298.2 million | - | - |

| - Leqembi (Japan) | $163.1 million | - | - |

| - Leqembi (China) | $82.9 million | - | +163.1% YoY |

| Dayvigo (Global) | $429.9 million | - | +19.6% YoY |

| - Dayvigo (Japan / US) | $310.9M / $70.2M | - | - |

| Fycompa (Global) | $222.6 million | - | +11.6% YoY |

| - Fycompa (EMEA / Japan) | $115.7M / $54.8M | - | - |

| Other / General Portfolio | $1,351.5 million | - | - |

| Americas (Entirely US: $1,959.9M) | $2,008.7 million | - | 36.4% of Total |

| Japan | $1,532.7 million | - | 27.8% of Total |

| China | $874.1 million | - | 15.8% of Total |

| EMEA | $545.1 million | - | 9.9% of Total |

| East Asia & Global South | $460.1 million | - | 8.3% of Total |

Table 2: Operating Leverage, Margin Dynamics, and Cash Conversion

| Metric | FY2025 Actual | Variance / Margin Data |

| Statutory Operating Profit (OP) | $295.1M (JPY 44.1B) | -18.8% YoY (Missed $364.4M / JPY 54.5B guidance by 19.0%) |

| Core Operating Profit | $335.0 million | +110.7% YoY |

| OP Margin | 5.35% | Contraction of ~154 bps from 6.89% |

| Net Profit Attributable to Owners | $257.8 million | -17.0% YoY |

| Net Profit Margin | 4.67% | Contraction of ~120 bps from 5.88% |

| Return on Equity (ROE) | 4.4% | Missed 5.0% guidance (Down from 5.4%) |

| Operating Cash Flow (OCF) | $410.0 million | +103.6% YoY |

| Investing Cash Flow (ICF) | -$279.4 million | (Includes -$84.1M / JPY 12.6B net for Econavista Inc.) |

| Financing Cash Flow (FCF) | -$408.5 million | (Includes $301.8M in dividends at $1.07 / JPY 160.00 per share) |

| Free Cash Flow | $131.0 million | Positive baseline retained |

| Asset Turnover / Equity Multiplier | 0.57x / 1.61x | Equity ratio expanded to 62.0% (Multiplier down from 1.65x) |

| R&D Expenditure | $1,060.8M (JPY 158.7B) | -7.6% YoY (19.2% of Total Revenue) |

Table 3: Balance Sheet Capitalization and Provisions Risk

| Balance Sheet Component | FY2025 Valuation | Risk & Structural Notes |

| Total Assets | $9,688.6 million | +4.5% YoY |

| Total Equity | $6,010.6 million | Highly solvent capital structure |

| Cash & Cash Equivalents | $1,640.9 million | Forms a $535.7 million net cash position against $1,244.1M in debt |

| Net Debt-to-Equity Ratio (DER) | -0.09x | Reflects zero structural debt reliance |

| Inventory | $1,721.9 million | +19.3% YoY. Includes an $18.7 million valuation loss for Tazverik. |

| Total PP&E | $1,076.7 million | Fixed asset footprint distributed globally. |

| Goodwill | $1,733.0 million | WACC 10.64%, Terminal Growth 3.0%. |

| Total Provisions | $322.4M (JPY 48,216M) | $311.8M current, $10.6M non-current |

| - Sales Rebate Provisions | $295.2M (JPY 44,155M) | Represents 91.6% of provisions (+31.5% YoY) |

| - Asset Retirement Obligations | $8.8M (JPY 1,310M) | Provision for hazardous materials/lease restorations |

| - Other Provisions | $18.4M (JPY 2,752M) | Minor legal and operational reserves |

| FY2025 Exceptional Items | Various | $58.4M (JPY 8.7B) Euro restructuring; FY24 comps included $39.7M MORAb-202 gain, $61.9M fixed asset sales |

Table 4: 2026-2028 Forward Guidance and IP M&A

| Planning Cycle | Target / Metric | Financial Value |

| FY2026 Guidance | Revenue Target | $5,907.0 million (JPY 883.5 billion) |

| FY2026 Guidance | Statutory & Core OP Target | $468.0 million (JPY 70.0 billion) |

| FY2026 Guidance | Adjusted ROIC Target | 8.7% |

| FY2028 Guidance | Revenue Target | $6,685.9 million (JPY 1,000.0 billion) |

| FY2028 Guidance | Core OP Target | $601.7 million (JPY 90.0 billion) |

| FY2028 Guidance | Structural ROE / Adjusted ROIC | 8.0% / 9.0% |

| Portfolio M&A | Econavista Inc. Acquisition | $103.8M (JPY 15.5B) cost; $63.8M (JPY 9.5B) goodwill |

| Portfolio M&A | Serplulimab IP Rights | $78.6M (JPY 11.7B) from Shanghai Henlius Biotech, Inc. |

Infrastructure Layout and Regional Moats

Eisai Co., Ltd. operates a highly decentralized global supply chain, systematically mitigating single-source dependency. Operations in Japan are anchored by the Tsukuba Research Laboratories and Kobe Research Laboratories. Domestic production relies on the Kawashima Industrial Park (Gifu) and the Kashima Plant (Ibaraki), supplemented by a targeted $42.8 million (JPY 6.4 billion) capital expenditure program at the EA Pharma Fukushima Plant extending through March 2029.

In the Americas, genetic-guided dementia and oncology discovery are isolated at the Exton Site (Pennsylvania) and G2D2 (Massachusetts). European operations, localized at the European Knowledge Centre (UK), are currently executing a £50 million capacity expansion through March 2030 to support commercial rollouts, parallel to the acquisition of EMEA rights for taletrectinib. Asian penetration utilizes localized nodes at the Suzhou Plant (Jiangsu) and Liaoning Plant in China, counteracting volume-based procurement pressures. Global South access is routed via PT Eisai Indonesia and the Eisai Knowledge Centre in Vizag, India, which has supplied 2.81 billion DEC tablets across 33 countries to the World Health Organization at a strict zero-price mandate. Total capital expenditure for FY2025 reached $138.5 million (JPY 20.7 billion).

The corporate "hhceco" transition is governed by massive digital asset accumulation. The company capitalized $15.2 million (JPY 2.2 billion) in software during FY2025, bringing the standalone software balance to $95.3 million (JPY 14.3 billion). This infrastructure supports a multi-layered digital platform linking Econavista's Liferhythm Navi, Arteryex Inc.'s Pashatto Karte, Teoria Technologies Inc.'s Teotoru, and the Yin Fa Tong platform in China. Internally, HR analytics are optimized via Kaonavi systems.

Ecological controls display rigid adherence to 2030 targets. Eisai Co., Ltd. achieved a 51.6% reduction in Scope 1 and 2 emissions against a 2019 baseline (targeting 55%), running on 98.7% renewable energy (targeting 100%). In Japan, 100% of the commercial sales fleet utilizes hybrid or electric vehicles. However, Scope 3 Category 1 emissions expanded by 80.9%, exposing supply-chain carbon inelasticity. The company aims for a 7% reduction in water intake and waste generation by 2030 against a 2023 baseline.

Legal moats defending Lenvima until its June 30, 2030, US exclusivity expiration are solidified via settlements with SUN Pharmaceutical Industries Ltd. & Inc. (March 21, 2024), Dr. Reddy’s Laboratories, Ltd. & Inc. (September 22, 2025), and Torrent Pharmaceuticals Ltd. (November 6, 2025). The sole immediate threat is a pending appellate challenge from Shilpa Medicare Limited. Clinical velocities are timed precisely: the Leqembi subcutaneous auto-injector (SC-AI) holds a US FDA PDUFA date of August 24, 2026, with a China BLA priority review accepted in January 2026, and Japan filing completed in November 2025. Oncology replacement Lenvima+Belzutifan holds an October 4, 2026, US PDUFA date (Japan filing March 2026). The neurological pipeline is padded by E2814 (anti-MTBR tau antibody, Fast Track September 2025), E2086 (Selective Orexin 2 Receptor Agonist, Orphan Drug February 2026), and EA8001 (evenamide, Phase III). Additionally, the company previously executed a $650 million unutilized upfront refund from Bristol Myers Squibb to regain complete control of MORAb-202.

HDIN Institutional Verdict

An objective audit of Eisai Co., Ltd. exposes a highly aggressive 50:50 externalization model driving R&D efficiency, partnered with Biogen Inc. and Merck & Co. The company limits systemic exposure by paying Merck $1,057.7 million (JPY 158.2 billion) in profit shares, recorded under SG&A, ensuring high-margin throughput despite limiting standalone upside.

However, macroeconomic friction exposes critical vulnerabilities. Customer concentration is severe, with McKesson Corporation ($575.2 million / 10.42%), Cencora, Inc. ($504.0 million), and Medipal Holdings ($395.8 million) commanding 26.7% of global volume. Foreign exchange sensitivity is acute; a 10% JPY appreciation translates directly to a $4.2 million pre-tax profit contraction against the USD, and $15.1 million against the EUR.

The 11-member Board of Directors maintains a 63.6% independent majority (7 outside directors, 4 internal), chaired by outside director Fumihiko Ike, while CEO Haruo Naito controls execution. Female representation sits at 17.9% (2 members), trailing the 30% internal target. Audit oversight is managed by Sawaharu Kanai, backed by Toru Moriyama, Ryota Miura, and Ryoko Ueda.

Executive compensation ($8.87 million / JPY 1,327 million total) operates on a 50% to 67% variable schema. The Short-Term Cash Bonus A achieved a 103% payout, driven by a 50/50 split weighting 2/3 on financial metrics (93% achievement) and 1/3 on non-financial metrics (115% R&D progress, 133% Leqembi volume). Crucially, the Compensation Committee enforced a 0% payout on the Long-Term Incentive (split 70% in-tenure, 30% retirement). Management missed the 3-year ESG EBIT target ($2,409.6 million actual vs. $2,862.2 million target), vastly underperformed the Relative PBR benchmark (1.42 actual vs. 3.56 target), and achieved exactly 6 out of 17 defined ESG goals.

Capital distribution among 291.6 million outstanding shares is anchored by Domestic Financial Institutions at 34.17% (The Master Trust Bank of Japan, Ltd. at 18.55%, Custody Bank of Japan, Ltd. at 9.99%) and Foreign Institutions at 32.36% (State Street Bank and Trust Company at 5.31%, JPMorgan Securities at 2.67%). Other domestic corporations hold 4.62%, while 100,451 retail investors control 22.58%. While management projects $6,685.9 million in FY2028 revenue, the impending January 2028 Medicare price caps and China’s National Reimbursement Drug List mandates fundamentally threaten the inelasticity of their primary cash engines.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*