Ono Pharmaceutical Co., Ltd.: $2.44B Deciphera Pivot Near Massachusetts as 56.5% Overseas Revenue Growth Signals Exit from Domestic Dependency

Date : 2026-06-17

Reading : 179

HDIN Executive Takeaways

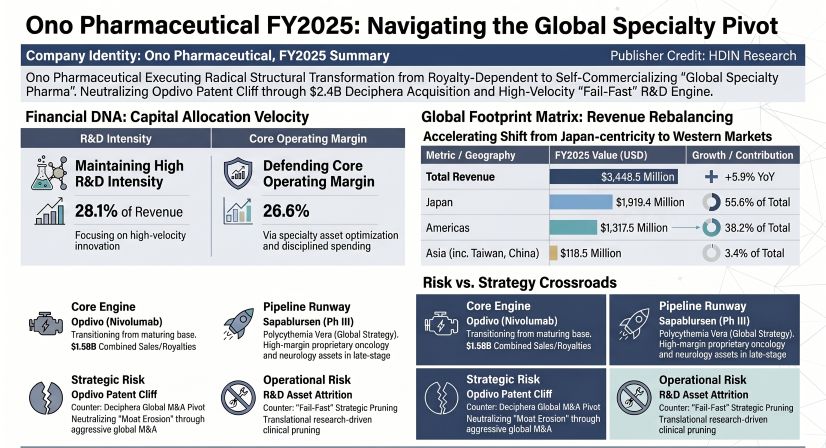

* Ono Pharmaceutical executed a $2,439.12 million acquisition of Massachusetts-based Deciphera Pharmaceuticals, deploying its fortress $1,584.86 million cash reserve to replace expiring domestic Opdivo royalties with direct commercialization rights in over 40 countries.

* Working capital optimized aggressively as inventory contracted from $500.53 million to $384.11M and Cost of Goods Sold declined to $947.50 million, neutralizing macroeconomic inflation while offsetting $66.86 million in modeled climate-risk exposure at dual-node domestic manufacturing plants.

* The Board tied 67.8% of executive compensation to performance stock and bonuses, enforcing a "fail-fast" pipeline strategy that terminated eight oncology trials, capping in-process R&D impairment losses at $12.96 million while sustaining a 26.6% core operating margin.

Figure Ono Pharmaceutical FY2025: Navigating the Global Specialty Pivot

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Ono Pharmaceutical Co., Ltd. [TYO: 4528] reported total revenue of $3,448.48 million (515,785 million JPY) at a conversion rate of 1 USD = 149.5686 JPY, marking a 5.9% year-over-year expansion. The top-line architecture reveals a structural bifurcation: domestic stagnation countered by aggressive overseas acquisition yields.

Domestic product sales contracted 3.5% to $1,881.41 million. This decline is directly attributable to the flagship Opdivo (nivolumab) franchise, which saw domestic direct sales fall 5.0% to $764.19 million amid intensified PD-1 class competition and downward pricing revisions by the Japanese National Health Insurance system. Concurrently, the primary care asset Forxiga (dapagliflozin) reported a 1.5% revenue contraction to $589.69 million, correlating with the market entry of generic alternatives in December 2025.

Conversely, overseas product sales surged 56.5% to $409.18 million, driven by the Deciphera integration. Qinlock generated $256.74 million (a 50.6% year-over-year increase reflecting a full 12-month contribution), while Romvimza added $55.49 million. The passive royalty segment expanded 10.9% to $1,157.85 million, anchored by $817.88 million from Bristol-Myers Squibb for Opdivo and $197.01 million from Merck for Keytruda. Secondary specialty assets showed robust volume traction: Braftovi grew 33.8% to $37.44 million, Ongentys expanded 17.3% to $60.17 million, and Velexbru increased 12.8% to $79.56 million.

Geographic revenue distribution underscores the ongoing transition from a Japan-centric model:

* Japan: $1,919.42 million (287,085 million JPY)

* Americas: $1,317.53 million (197,061 million JPY)

* Asia: $118.47 million (17,719 million JPY)

* Europe: $82.40 million (12,324 million JPY)

* Others: $10.66 million (1,595 million JPY)

Despite total R&D expenditures of $983.11 million (147,043 million JPY) consuming 28.1% of total revenue against a management target of 20-25%, core operating profitability demonstrated high resilience. Reported Operating Profit settled at $616.68 million, while Core Operating Profit—excluding transient acquisition amortization of $171.16 million and asset impairments—expanded 21.7% to $916.87 million, exceeding the $0.76 billion internal target. Core Net Profit reached $0.69 billion against a $0.61 billion target. The Core Operating Profit Margin hit 26.6%, surpassing the 25% corporate threshold, while Return on Equity (ROE) recovered from 6.4% to 8.5%, tracking toward a 5-year average target of 12.0%.

Cash conversion metrics exhibit institutional-grade liquidity. Operating Cash Flow (CFO) accelerated to $914.77 million from $551.31 million in the prior year. This liquidity was fortified by a reduction in trade and other payables from $597.24 million to $420.88 million, alongside a drop in Cost of Sales from $989.18 million to $947.50 million through forward exchange hedging. Investing Cash Flow (CFI) recorded a $266.50 million outflow, skewed heavily toward intangible asset capex ($315.88 million) over tangible PP&E ($40.28 million). Financing Cash Flow (CFF) registered a $437.88 million outflow, primarily allocated to a $200.58 million long-term debt repayment and $250.93 million in progressive cash dividends (47.1% payout ratio), while share buybacks were restricted to $0.01 million.

The balance sheet is devoid of material legal provisions, absorbing a contained $9.68 million product recall loss and a routine $110.38 million refund liability for wholesaler rebates.

Infrastructure Layout and Regional Moats

The corporate balance sheet reports $7,398.04 million in Total Assets, supported by an ironclad 76.9% equity ratio. Current Assets of $3,131.06 million cover Current Liabilities of $1,094.11 million, producing a 2.86x current ratio. Total interest-bearing debt rests at $738.05 million against $1,584.86 million in pure cash and equivalents, yielding a deeply negative net debt position.

Following the $2,439.12 million Deciphera cash outlay, Intangible Assets reached $2,364.01 million and Goodwill scaled to $151.46 million, combined representing approximately 34% of total assets. Capitalized In-Process R&D (IPR&D) features Sapablursen at $280.24 million and Cenobamate at $38.11 million. Off-balance sheet commitments are limited to $74.21 million in potential 3-year R&D milestones, $6.42 million in tangible capex obligations, and a $10.18 million rent guarantee for the US subsidiary. The firm also unwound cross-shareholdings in Yakult Honsha, Hitachi, and Daiwa Securities Group, reducing its policy-holding stock ratio to 9.0%.

Physical manufacturing risk is mitigated through dual-node domestic production and externalized logistics. Inventories contracted from $500.53 million to $384.11 million, with long-term inventory slated for sale beyond 12 months plummeting from $98.16 million to $51.31 million. Capital expenditure for production facilities totaled $13.83 million.

* Fujiyama Plant (Shizuoka, Japan): $63.32 million book value; 91 personnel.

* Yamaguchi Plant (Yamaguchi, Japan): $96.26 million book value; 42 personnel. Equipped with seismic isolation systems to counter acute physical climate risks modeled at $66.86 million under a 4°C warming scenario.

* Joto & Awaji Plants (Osaka, Japan): Operated by subsidiary Toyo Pharmar Co., Ltd.; ~$28.8 million combined book value; 178 personnel.

The global innovation footprint relies on highly concentrated domestic biology hubs and a newly established US clinical beachhead:

* Minase Research Institute (Osaka, Japan): $176.55 million book value; 686 personnel. Fortified with seismic isolation.

* Tsukuba Research Institute (Ibaraki, Japan): $32.28 million book value; 70 personnel.

* Joto Product Development Center (Osaka, Japan): $24.31 million book value; 56 personnel.

* Deciphera Pharmaceuticals, LLC (Massachusetts, USA): $22.14 million book value; 430 personnel. Operates the direct sales network across more than 40 countries.

Environmental and labor metrics align with stringent global compliance. Scope 1 and 2 carbon emissions fell to 8.9 thousand t-CO2, a 70.3% reduction against a 2017 baseline, utilizing a 93.2% renewable energy ratio to track toward a 2035 neutrality target. Scope 3 emissions stand at 100.5 thousand t-CO2, an 18.4% reduction from the baseline. Labor stability is maintained across 3 internal unions comprising 1,907 members. The company deployed 46.0 hours of average annual training per employee, achieving an 87% behavioral change rate, though the corporate engagement index of 72 trails the life science benchmark of 76.

R&D Capital Allocation and Corporate Governance

The R&D architecture carries an implied annual maintenance cost of $35.11 million per active clinical asset (based on 28 active candidates, 19 of which are in-house). To manage this attrition risk, total impairment losses were restricted to $14.71 million, separated into $1.74 million for tangible fixed assets and $12.96 million for IPR&D. The IPR&D write-down marks a sharp efficiency gain compared to the $40.12 million impairment in the prior fiscal year.

This cost containment stems from the strategic termination of low-probability trials:

* Late-Stage Sunk Costs: Terminated Phase III trials for Opdivo+Yervoy+Chemotherapy (1st Line Gastric Cancer) and Opdivo+Chemotherapy (Neoadjuvant/Adjuvant Bladder Cancer) due to efficacy failures.

* Phase I/II Strategic Pruning: Terminated ONO-7018, ONO-7475, DCC-3116, DCC-3084, ONO-4578, and ONO-7913.

Offsetting these terminations, the pipeline secured critical regulatory and clinical advancements. Approvals included Opdivo+Yervoy for Hepatocellular Carcinoma (Japan, Korea, Taiwan, China) and MSI-H/dMMR Colorectal Cancer (Japan, Taiwan, China, Korea), alongside Braftovi for BRAF-mutant Colorectal Cancer (Japan, Korea) and Romvimza for TGCT (Europe). Regulatory filings advanced for Qinlock (4th-line GIST, Japan), Velexbru (Primary CNS Lymphoma, US), and Cenobamate/ONO-2017 (Epilepsy partial seizures, Japan). The Phase III roster expanded with Sapablursen/ONO-0530 (Global), Povetacicept/ONO-8531 (Japan/Korea, licensed from Vertex), Gel-One/ONO-5532 (Japan), and Cenobamate (Pediatric Epilepsy, Japan). Phase I assets DCC-2812, ONO-7429, ONO-2416, ONO-3310, and ONO-6414 continue early validation.

Governance enforces this operational discipline through a 50% parity Board of Directors, consisting of 6 members (3 Independent Outside Directors, including 1 female academic). The Audit Board features 4 members, including 1 female CPA. Executive compensation is aggressively weaponized to demand operational execution. The $3.84 million remuneration pool for the 3 internal directors consists of $1.24 million in fixed salaries (32.2%), $0.94 million in short-term bonuses (24.6%), and $1.66 million in long-term stock incentives (43.2%, split between $0.31 million in continuous service stock and $1.34 million in performance-linked stock with Malus/Clawback provisions).

Human capital restructuring aims to dissolve rigid domestic employment models. Mid-career hires account for 23.1% of management (178 individuals), supported by 154 internal job transfers and 101 concurrent-role deployments. While male childcare leave reached 88.8% (averaging 78 days), structural wage disparities persist. The female-to-male wage ratio is 73.6% (73.1% for regular employees), driven by a 7.1-year age gap in comprehensive-track female employees and a female management ratio of 9.1% against a 10% target for FY2026 and a 20% mandate by FY2031. Total female leadership across the executive and audit boards stands at 20%.

HDIN Institutional Verdict

Ono Pharmaceutical is executing one of the most high-stakes, structurally enforced business pivots in the Asian biopharma sector. The mathematical certainty of the Opdivo royalty cliff dictates the entirety of the company's capital allocation strategy. The $2,439.12 million acquisition of Deciphera is not a standard bolt-on pipeline expansion; it is a forced migration from passive, high-margin domestic IP monetization toward an active, capital-intensive global commercial operation.

The underlying financial mechanics validating this transition are robust. The company successfully absorbed the Deciphera cash outflow without jeopardizing its 76.9% equity ratio or accumulating toxic debt, maintaining $1,584.86 million in cash reserves. Operationally, the contraction in Cost of Goods Sold and the simultaneous drop in total inventory to $384.11 million during a period of macroeconomic inflation indicate an elite, highly optimized supply chain that utilizes externalized logistics to mitigate its $66.86 million domestic climate risk.

Furthermore, the board's decision to link 67.8% of internal director compensation to performance metrics ensures that executive wealth is intrinsically tied to the ruthless pruning of the R&D pipeline. The immediate halt of six Phase I/II oncology assets, effectively capping IPR&D impairments at $12.96 million, proves that management is overriding the industry's sunk-cost fallacies. The ultimate verdict relies on execution: Ono must bridge the near-term cash flow gap between the structural decline of Forxiga and Opdivo and the volume ramp-up of the newly integrated Qinlock, Romvimza, and late-stage Sapablursen assets in the Americas and Europe.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Ono Pharmaceutical executed a $2,439.12 million acquisition of Massachusetts-based Deciphera Pharmaceuticals, deploying its fortress $1,584.86 million cash reserve to replace expiring domestic Opdivo royalties with direct commercialization rights in over 40 countries.

* Working capital optimized aggressively as inventory contracted from $500.53 million to $384.11M and Cost of Goods Sold declined to $947.50 million, neutralizing macroeconomic inflation while offsetting $66.86 million in modeled climate-risk exposure at dual-node domestic manufacturing plants.

* The Board tied 67.8% of executive compensation to performance stock and bonuses, enforcing a "fail-fast" pipeline strategy that terminated eight oncology trials, capping in-process R&D impairment losses at $12.96 million while sustaining a 26.6% core operating margin.

Figure Ono Pharmaceutical FY2025: Navigating the Global Specialty Pivot

Segmental Realities and Margin CompressionOno Pharmaceutical Co., Ltd. [TYO: 4528] reported total revenue of $3,448.48 million (515,785 million JPY) at a conversion rate of 1 USD = 149.5686 JPY, marking a 5.9% year-over-year expansion. The top-line architecture reveals a structural bifurcation: domestic stagnation countered by aggressive overseas acquisition yields.

Domestic product sales contracted 3.5% to $1,881.41 million. This decline is directly attributable to the flagship Opdivo (nivolumab) franchise, which saw domestic direct sales fall 5.0% to $764.19 million amid intensified PD-1 class competition and downward pricing revisions by the Japanese National Health Insurance system. Concurrently, the primary care asset Forxiga (dapagliflozin) reported a 1.5% revenue contraction to $589.69 million, correlating with the market entry of generic alternatives in December 2025.

Conversely, overseas product sales surged 56.5% to $409.18 million, driven by the Deciphera integration. Qinlock generated $256.74 million (a 50.6% year-over-year increase reflecting a full 12-month contribution), while Romvimza added $55.49 million. The passive royalty segment expanded 10.9% to $1,157.85 million, anchored by $817.88 million from Bristol-Myers Squibb for Opdivo and $197.01 million from Merck for Keytruda. Secondary specialty assets showed robust volume traction: Braftovi grew 33.8% to $37.44 million, Ongentys expanded 17.3% to $60.17 million, and Velexbru increased 12.8% to $79.56 million.

Geographic revenue distribution underscores the ongoing transition from a Japan-centric model:

* Japan: $1,919.42 million (287,085 million JPY)

* Americas: $1,317.53 million (197,061 million JPY)

* Asia: $118.47 million (17,719 million JPY)

* Europe: $82.40 million (12,324 million JPY)

* Others: $10.66 million (1,595 million JPY)

Despite total R&D expenditures of $983.11 million (147,043 million JPY) consuming 28.1% of total revenue against a management target of 20-25%, core operating profitability demonstrated high resilience. Reported Operating Profit settled at $616.68 million, while Core Operating Profit—excluding transient acquisition amortization of $171.16 million and asset impairments—expanded 21.7% to $916.87 million, exceeding the $0.76 billion internal target. Core Net Profit reached $0.69 billion against a $0.61 billion target. The Core Operating Profit Margin hit 26.6%, surpassing the 25% corporate threshold, while Return on Equity (ROE) recovered from 6.4% to 8.5%, tracking toward a 5-year average target of 12.0%.

Cash conversion metrics exhibit institutional-grade liquidity. Operating Cash Flow (CFO) accelerated to $914.77 million from $551.31 million in the prior year. This liquidity was fortified by a reduction in trade and other payables from $597.24 million to $420.88 million, alongside a drop in Cost of Sales from $989.18 million to $947.50 million through forward exchange hedging. Investing Cash Flow (CFI) recorded a $266.50 million outflow, skewed heavily toward intangible asset capex ($315.88 million) over tangible PP&E ($40.28 million). Financing Cash Flow (CFF) registered a $437.88 million outflow, primarily allocated to a $200.58 million long-term debt repayment and $250.93 million in progressive cash dividends (47.1% payout ratio), while share buybacks were restricted to $0.01 million.

The balance sheet is devoid of material legal provisions, absorbing a contained $9.68 million product recall loss and a routine $110.38 million refund liability for wholesaler rebates.

Infrastructure Layout and Regional Moats

The corporate balance sheet reports $7,398.04 million in Total Assets, supported by an ironclad 76.9% equity ratio. Current Assets of $3,131.06 million cover Current Liabilities of $1,094.11 million, producing a 2.86x current ratio. Total interest-bearing debt rests at $738.05 million against $1,584.86 million in pure cash and equivalents, yielding a deeply negative net debt position.

Following the $2,439.12 million Deciphera cash outlay, Intangible Assets reached $2,364.01 million and Goodwill scaled to $151.46 million, combined representing approximately 34% of total assets. Capitalized In-Process R&D (IPR&D) features Sapablursen at $280.24 million and Cenobamate at $38.11 million. Off-balance sheet commitments are limited to $74.21 million in potential 3-year R&D milestones, $6.42 million in tangible capex obligations, and a $10.18 million rent guarantee for the US subsidiary. The firm also unwound cross-shareholdings in Yakult Honsha, Hitachi, and Daiwa Securities Group, reducing its policy-holding stock ratio to 9.0%.

Physical manufacturing risk is mitigated through dual-node domestic production and externalized logistics. Inventories contracted from $500.53 million to $384.11 million, with long-term inventory slated for sale beyond 12 months plummeting from $98.16 million to $51.31 million. Capital expenditure for production facilities totaled $13.83 million.

* Fujiyama Plant (Shizuoka, Japan): $63.32 million book value; 91 personnel.

* Yamaguchi Plant (Yamaguchi, Japan): $96.26 million book value; 42 personnel. Equipped with seismic isolation systems to counter acute physical climate risks modeled at $66.86 million under a 4°C warming scenario.

* Joto & Awaji Plants (Osaka, Japan): Operated by subsidiary Toyo Pharmar Co., Ltd.; ~$28.8 million combined book value; 178 personnel.

The global innovation footprint relies on highly concentrated domestic biology hubs and a newly established US clinical beachhead:

* Minase Research Institute (Osaka, Japan): $176.55 million book value; 686 personnel. Fortified with seismic isolation.

* Tsukuba Research Institute (Ibaraki, Japan): $32.28 million book value; 70 personnel.

* Joto Product Development Center (Osaka, Japan): $24.31 million book value; 56 personnel.

* Deciphera Pharmaceuticals, LLC (Massachusetts, USA): $22.14 million book value; 430 personnel. Operates the direct sales network across more than 40 countries.

Environmental and labor metrics align with stringent global compliance. Scope 1 and 2 carbon emissions fell to 8.9 thousand t-CO2, a 70.3% reduction against a 2017 baseline, utilizing a 93.2% renewable energy ratio to track toward a 2035 neutrality target. Scope 3 emissions stand at 100.5 thousand t-CO2, an 18.4% reduction from the baseline. Labor stability is maintained across 3 internal unions comprising 1,907 members. The company deployed 46.0 hours of average annual training per employee, achieving an 87% behavioral change rate, though the corporate engagement index of 72 trails the life science benchmark of 76.

R&D Capital Allocation and Corporate Governance

The R&D architecture carries an implied annual maintenance cost of $35.11 million per active clinical asset (based on 28 active candidates, 19 of which are in-house). To manage this attrition risk, total impairment losses were restricted to $14.71 million, separated into $1.74 million for tangible fixed assets and $12.96 million for IPR&D. The IPR&D write-down marks a sharp efficiency gain compared to the $40.12 million impairment in the prior fiscal year.

This cost containment stems from the strategic termination of low-probability trials:

* Late-Stage Sunk Costs: Terminated Phase III trials for Opdivo+Yervoy+Chemotherapy (1st Line Gastric Cancer) and Opdivo+Chemotherapy (Neoadjuvant/Adjuvant Bladder Cancer) due to efficacy failures.

* Phase I/II Strategic Pruning: Terminated ONO-7018, ONO-7475, DCC-3116, DCC-3084, ONO-4578, and ONO-7913.

Offsetting these terminations, the pipeline secured critical regulatory and clinical advancements. Approvals included Opdivo+Yervoy for Hepatocellular Carcinoma (Japan, Korea, Taiwan, China) and MSI-H/dMMR Colorectal Cancer (Japan, Taiwan, China, Korea), alongside Braftovi for BRAF-mutant Colorectal Cancer (Japan, Korea) and Romvimza for TGCT (Europe). Regulatory filings advanced for Qinlock (4th-line GIST, Japan), Velexbru (Primary CNS Lymphoma, US), and Cenobamate/ONO-2017 (Epilepsy partial seizures, Japan). The Phase III roster expanded with Sapablursen/ONO-0530 (Global), Povetacicept/ONO-8531 (Japan/Korea, licensed from Vertex), Gel-One/ONO-5532 (Japan), and Cenobamate (Pediatric Epilepsy, Japan). Phase I assets DCC-2812, ONO-7429, ONO-2416, ONO-3310, and ONO-6414 continue early validation.

Governance enforces this operational discipline through a 50% parity Board of Directors, consisting of 6 members (3 Independent Outside Directors, including 1 female academic). The Audit Board features 4 members, including 1 female CPA. Executive compensation is aggressively weaponized to demand operational execution. The $3.84 million remuneration pool for the 3 internal directors consists of $1.24 million in fixed salaries (32.2%), $0.94 million in short-term bonuses (24.6%), and $1.66 million in long-term stock incentives (43.2%, split between $0.31 million in continuous service stock and $1.34 million in performance-linked stock with Malus/Clawback provisions).

Human capital restructuring aims to dissolve rigid domestic employment models. Mid-career hires account for 23.1% of management (178 individuals), supported by 154 internal job transfers and 101 concurrent-role deployments. While male childcare leave reached 88.8% (averaging 78 days), structural wage disparities persist. The female-to-male wage ratio is 73.6% (73.1% for regular employees), driven by a 7.1-year age gap in comprehensive-track female employees and a female management ratio of 9.1% against a 10% target for FY2026 and a 20% mandate by FY2031. Total female leadership across the executive and audit boards stands at 20%.

HDIN Institutional Verdict

Ono Pharmaceutical is executing one of the most high-stakes, structurally enforced business pivots in the Asian biopharma sector. The mathematical certainty of the Opdivo royalty cliff dictates the entirety of the company's capital allocation strategy. The $2,439.12 million acquisition of Deciphera is not a standard bolt-on pipeline expansion; it is a forced migration from passive, high-margin domestic IP monetization toward an active, capital-intensive global commercial operation.

The underlying financial mechanics validating this transition are robust. The company successfully absorbed the Deciphera cash outflow without jeopardizing its 76.9% equity ratio or accumulating toxic debt, maintaining $1,584.86 million in cash reserves. Operationally, the contraction in Cost of Goods Sold and the simultaneous drop in total inventory to $384.11 million during a period of macroeconomic inflation indicate an elite, highly optimized supply chain that utilizes externalized logistics to mitigate its $66.86 million domestic climate risk.

Furthermore, the board's decision to link 67.8% of internal director compensation to performance metrics ensures that executive wealth is intrinsically tied to the ruthless pruning of the R&D pipeline. The immediate halt of six Phase I/II oncology assets, effectively capping IPR&D impairments at $12.96 million, proves that management is overriding the industry's sunk-cost fallacies. The ultimate verdict relies on execution: Ono must bridge the near-term cash flow gap between the structural decline of Forxiga and Opdivo and the volume ramp-up of the newly integrated Qinlock, Romvimza, and late-stage Sapablursen assets in the Americas and Europe.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."