KEYENCE Corporation: Fabless Capital Realignment Across Takatsuki Logistics Hub as 83.02% Gross Margins Signal Absolute Downstream Pricing Power

Date : 2026-06-17

Reading : 115

HDIN Executive Takeaways

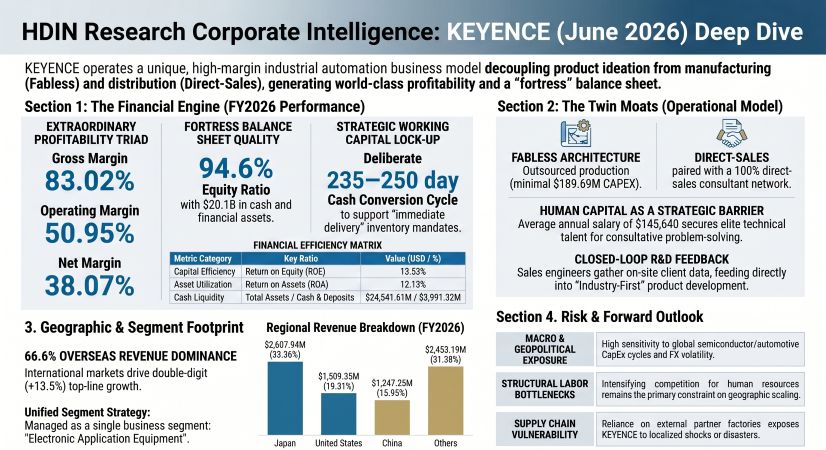

* KEYENCE Corporation [TSE: 6861] recorded a 50.95% operating margin on $7,817.75 million in FY2026 revenue, shielding profitability through an $189.69 million ultra-light CapEx structure.

* A decentralized fabless supply chain, anchored by the Takatsuki Logistics Center, maintains $570.13 million in inventory to guarantee same-day fulfillment without order backlogs.

* The $24.54 billion overcapitalized balance sheet serves as a defensive moat against macroeconomic volatility, ensuring dividend distributions and M&A readiness amid industrial automation cycles.

Figure KEYENCE Deep Dive

Financial Realities and Segmental Economics

Financial Realities and Segmental Economics

KEYENCE Corporation operates exclusively under a single business segment focused on the manufacture and sale of electronic application equipment. The firm converts global currency metrics at an applied rate of 1 USD = 149.5686 JPY. Below is the structural breakdown of the firm’s top-line revenue, geographic distribution, and working capital ratios for FY2026.

Table 1: Geographic Revenue Distribution & Top-Line Performance

Table 2: Profitability & Cost Architecture

Table 3: Balance Sheet, Liquidity, & Cash Conversion Dynamics

Table 4: Cash Flow Allocation & Internal Transfer Pricing

Table 5: Tax Assets, Liabilities & Reporting Standards

Supply Chain Architecture and Talent Infrastructure

KEYENCE Corporation commands a capital-light, fabless manufacturing ecosystem reliant on external "partner factories." Internal production oversight is anchored by Keyence Engineering Corporation in Takatsuki, Osaka, while software deployment is executed by Keyence Software Corporation. Physical hardware logistics operate through the Takatsuki Logistics Center.

Global Direct-Sales Hubs & Disintermediation Infrastructure

To bypass third-party distribution fees, the company operates wholly-owned subsidiaries across key geographic jurisdictions:

* The Americas: Led by KEYENCE CORPORATION OF AMERICA, with active direct-sales subsidiaries in Canada, Mexico, and Brazil.

* Europe: Commanded by KEYENCE DEUTSCHLAND GmbH in Germany, supported by localized subsidiaries in the UK, France, Italy, and Belgium.

* Asia-Pacific: Managed via KEYENCE (CHINA) CO.,LTD., KEYENCE (HONG KONG) CO.,LTD., KEYENCE TAIWAN CO.,LTD., with auxiliary hubs positioned in South Korea, Singapore, India, Indonesia, Vietnam, the Philippines, Malaysia, and Thailand.

Product Pipeline & Supply Risk Dispersion

Research and development output prioritizes hardware engineered to alleviate structural labor shortages. FY2026 technological releases include 3D printers optimized for functional resins on manufacturing floors, line-type cylinder sensors, smart valves, high-precision microscopes, and advanced code readers. The corporate risk dispersion policy actively prohibits dependence on any specific supplier, individual customer accounting for 10% or more of total revenue, or isolated geographic region.

Governance, ESG & Human Capital Density

* Headcount & Tenure: The consolidated workforce reached 12,784 employees. The non-consolidated parent company retains 3,306 personnel with an average age of 35.0 years and an average tenure of 11.3 years.

* Human Capital Compensation: The average annual non-consolidated salary sits at $145,640 (¥21,783,259).

* Executive Remuneration: Total compensation for 7 internal directors amounted to $1.97 million, capped by a 3.0 multiplier against previous employee average salaries (resulting in a 60% to 75% performance-linked structure). The highest payout was $1.22 million to Director and Special Advisor Yu Nakata. Fixed compensation for 7 outside executives totaled $0.26 million.

* Board Composition: The Board of Directors features 9 members, including 4 Independent Outside Directors (44.4%). The Audit & Supervisory Board contains 3 Independent Outside Auditors (100%). Cumulatively, 7 out of 12 executives (58.3%) hold independent status. A voluntary Nomination and Remuneration Committee holds a majority of 3 Independent Outside Directors out of 5 total members.

* Internal Control Audit: A 7-member full-time internal audit team conducts on-site compliance checks globally. The firm enforces strict anti-nepotism protocols prohibiting the hiring of personnel within three degrees of kinship to current employees, alongside a zero-tolerance mandate on business entertainment or gifts.

* Diversity & Inclusion Metrics: Female executives comprise 16.7% of the roster (2 of 12). The statutory gender pay gap registers at 43.2% for all workers and 43.7% for regular employees, counterbalanced by an 84.7% childcare leave acquisition rate for male employees. Internal engagement targets consistently maintain a >70% positive response rate, supported by the Management Development Program (MDP) and Career Development Program (CDP).

HDIN Institutional Verdict

KEYENCE Corporation presents a structural anomaly within industrial automation metrics: the firm actively violates lean inventory principles to enforce downstream pricing dominance. By maintaining 150 to 156 Inventory Turnover Days (DIO) and stockpiling $570.13 million in inventory, the company completely eradicates order backlogs, executing a strict "immediate delivery" policy. This exact capital allocation choice enables the 83.02% Gross Profit Margin, as eliminating customer factory downtime neutralizes downstream price negotiation leverage.

Simultaneously, the SG&A expenditure profile functionally serves as the firm's true R&D engine. While nominal R&D stands at a highly optimized $219.56 million (under 3% of revenue), the $1,261.41 million deployed into human capital secures an elite tier of consultative sales engineers who embed directly onto client manufacturing floors. This disintermediation tactic recaptures third-party distribution margins and creates a continuous feedback loop that derisks new product development.

Consequently, while standard financial analysis would penalize the highly extended 235 to 250-day Cash Conversion Cycle (CCC) and the overcapitalized nature of a $24.54 billion asset base holding $20.11 billion in liquid/investment securities, these metrics validate KEYENCE Corporation's defensive posture. The mathematically high 13.53% ROE on a 94.6% Equity Ratio balance sheet verifies that the firm’s fabless architecture scales profit linearly against human capital investments, rather than depreciating physical assets.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* KEYENCE Corporation [TSE: 6861] recorded a 50.95% operating margin on $7,817.75 million in FY2026 revenue, shielding profitability through an $189.69 million ultra-light CapEx structure.

* A decentralized fabless supply chain, anchored by the Takatsuki Logistics Center, maintains $570.13 million in inventory to guarantee same-day fulfillment without order backlogs.

* The $24.54 billion overcapitalized balance sheet serves as a defensive moat against macroeconomic volatility, ensuring dividend distributions and M&A readiness amid industrial automation cycles.

Figure KEYENCE Deep Dive

Financial Realities and Segmental EconomicsKEYENCE Corporation operates exclusively under a single business segment focused on the manufacture and sale of electronic application equipment. The firm converts global currency metrics at an applied rate of 1 USD = 149.5686 JPY. Below is the structural breakdown of the firm’s top-line revenue, geographic distribution, and working capital ratios for FY2026.

Table 1: Geographic Revenue Distribution & Top-Line Performance

| Metric | FY2025 Result |

|---|---|

| Total Global Recognized Revenue | $7,817.75M (¥1,169,289M) |

| YoY Revenue Growth | +10.4% |

| Production Actuals | $8,121.62M (¥1,214,740M) |

| Total Overseas Revenue | $5,209.80M |

| Overseas Revenue Share | 66.64% |

| Overseas Revenue Growth | +13.5% |

| Japan Revenue | $2,607.94M |

| Japan Revenue Share | 33.36% |

| Japan Revenue Growth | +4.6% |

| United States Revenue | $1,509.35M |

| United States Revenue Share | 19.31% |

| China Revenue | $1,247.25M |

| China Revenue Share | 15.95% |

| Other Regions (Asia & Europe) Revenue | $2,453.19M |

| Other Regions Share | 31.38% |

Table 2: Profitability & Cost Architecture

| Financial Metric / Component | Amount (USD Millions) | % of Revenue / Margin | Note / Details |

| Gross Profit | $6,490.25 | 83.02% | Gross Profit Margin (GPM) |

| Operating Profit | $3,983.18 | 50.95% | Operating Profit Margin (OPM) |

| Net Income | $2,976.46 | 38.07% | Net Profit Margin (NPM) attributable to owners |

| Cost of Sales | $1,327.50 | - | |

| Total SG&A Expenses | $2,507.06 | 32.07% | Percentage of total revenue |

| — Human Capital | $1,261.41 | - | Salaries, Allowances, Bonuses (Largest SG&A component) |

| — Provision for Bonuses | $148.90 | - | Equivalent to ¥22,271 million |

| Research & Development (R&D) | $219.56 | < 3.00% | Equivalent to ¥32,839 million, fully expensed as incurred |

Table 3: Balance Sheet, Liquidity, & Cash Conversion Dynamics

| Financial Metric / Component | Amount (USD Millions) | Ratio / Efficiency Metric | Additional Details |

| Total Assets | $24,541.61 | - | |

| Total Liabilities | $1,331.72 | - | |

| Equity Ratio | - | 94.60% | Reflects highly conservative leverage |

| Return on Equity (ROE) | - | 13.53% | |

| Return on Assets (ROA) | - | 12.13% | |

| Cash & Deposits | $3,991.32 | - | Liquid asset component |

| Short-Term Marketable Securities | $5,996.67 | - | Liquid asset component |

| Long-Term Investment Securities | $10,124.48 | - | Core non-current asset |

| Accounts Receivable (AR) | $2,537.90 | DSO: 109 - 118 Days | Allowance for doubtful accounts: $14.27M |

| Inventory Balance | $570.13 | DIO: 150 - 156 Days | Equivalent to ¥85,273 million |

| Accounts Payable (AP) | $72.81 | DPO: 20 - 24 Days | |

| Cash Conversion Cycle (CCC) | - | 235 - 250 Days | Highly extended efficiency cycle |

Table 4: Cash Flow Allocation & Internal Transfer Pricing

| Financial Metric / Component | Amount (USD Millions) | Flow Direction / Type | Additional Details / Remarks |

| PART I: CONSOLIDATED CASH FLOW ALLOCATION | |||

| Operating Cash Flow (OCF) | $2,879.48 | Inflow | Core operational cash generation |

| Investing Cash Flow (ICF) | ($2,088.59) | Outflow | Total investing activities |

| — Traditional Capital Expenditures (CapEx) | ($189.69) | Outflow | Equivalent to ¥28,371 million |

| — Strategic Treasury Management Securities | ($1,625.44) | Outflow | Strategic acquisition of liquidity instruments |

| Financing Cash Flow (FCF) | ($760.33) | Outflow | Total financing activities |

| — Cash Dividend Distributions | ($729.67) | Outflow | Primary driver of financing cash outflow |

| — Share Buybacks | Fractional | Outflow | Constrained to minor/fractional repurchases |

| PART II: PARENT-TO-AFFILIATE INTERCOMPANY TRANSACTIONS | |||

| Intercompany Sales to Affiliates | $3,152.55 | Revenue / Inflow | Generated by non-consolidated parent (¥471,523M) |

| Intercompany Accounts Receivable (AR) | $1,290.37 | Asset / Balance | Carried by non-consolidated parent (¥192,999M) |

| Dividends Received from Subsidiaries | $10.30 | Inflow | Recorded by non-consolidated parent (¥1,540M) |

Table 5: Tax Assets, Liabilities & Reporting Standards

| Tax Component / Reporting Item | Amount (USD Millions) | Amount (JPY Millions) | Reporting Standards & Disclosures |

| PART I: DEFERRED TAXATION (DTA & DTL BREAKDOWN) | |||

| Gross Deferred Tax Assets (DTA) | $298.20 | ¥44,601 | Total deferred tax assets portfolio |

| — Inventory Valuation | $146.85 | ¥21,964 | Core inventory adjustment component |

| — Unpaid Enterprise Tax | $33.03 | ¥4,940 | Accrued tax liabilities timing difference |

| — Investment Securities | $33.02 | ¥4,939 | Mark-to-market valuations |

| — Bonus Provisions | $29.32 | ¥4,385 | Tax effect on human capital allowances |

| — Other Factors | $55.96 | ¥8,370 | Aggregate of remaining minor DTA factors |

| Gross Deferred Tax Liabilities (DTL) | $161.28 | ¥24,122 | Total deferred tax liability portfolio |

| — Retained Earnings of Subsidiaries | $136.12 | ¥20,359 | Dominant driver of deferred tax liabilities |

| PART II: ACCOUNTING STANDARDS & REGULATORY UPDATES | |||

| ASBJ Statement No. 34 Application | — | — | The "Accounting Standard for Leases" will be applied beginning the fiscal year ending March 2029. |

Supply Chain Architecture and Talent Infrastructure

KEYENCE Corporation commands a capital-light, fabless manufacturing ecosystem reliant on external "partner factories." Internal production oversight is anchored by Keyence Engineering Corporation in Takatsuki, Osaka, while software deployment is executed by Keyence Software Corporation. Physical hardware logistics operate through the Takatsuki Logistics Center.

Global Direct-Sales Hubs & Disintermediation Infrastructure

To bypass third-party distribution fees, the company operates wholly-owned subsidiaries across key geographic jurisdictions:

* The Americas: Led by KEYENCE CORPORATION OF AMERICA, with active direct-sales subsidiaries in Canada, Mexico, and Brazil.

* Europe: Commanded by KEYENCE DEUTSCHLAND GmbH in Germany, supported by localized subsidiaries in the UK, France, Italy, and Belgium.

* Asia-Pacific: Managed via KEYENCE (CHINA) CO.,LTD., KEYENCE (HONG KONG) CO.,LTD., KEYENCE TAIWAN CO.,LTD., with auxiliary hubs positioned in South Korea, Singapore, India, Indonesia, Vietnam, the Philippines, Malaysia, and Thailand.

Product Pipeline & Supply Risk Dispersion

Research and development output prioritizes hardware engineered to alleviate structural labor shortages. FY2026 technological releases include 3D printers optimized for functional resins on manufacturing floors, line-type cylinder sensors, smart valves, high-precision microscopes, and advanced code readers. The corporate risk dispersion policy actively prohibits dependence on any specific supplier, individual customer accounting for 10% or more of total revenue, or isolated geographic region.

Governance, ESG & Human Capital Density

* Headcount & Tenure: The consolidated workforce reached 12,784 employees. The non-consolidated parent company retains 3,306 personnel with an average age of 35.0 years and an average tenure of 11.3 years.

* Human Capital Compensation: The average annual non-consolidated salary sits at $145,640 (¥21,783,259).

* Executive Remuneration: Total compensation for 7 internal directors amounted to $1.97 million, capped by a 3.0 multiplier against previous employee average salaries (resulting in a 60% to 75% performance-linked structure). The highest payout was $1.22 million to Director and Special Advisor Yu Nakata. Fixed compensation for 7 outside executives totaled $0.26 million.

* Board Composition: The Board of Directors features 9 members, including 4 Independent Outside Directors (44.4%). The Audit & Supervisory Board contains 3 Independent Outside Auditors (100%). Cumulatively, 7 out of 12 executives (58.3%) hold independent status. A voluntary Nomination and Remuneration Committee holds a majority of 3 Independent Outside Directors out of 5 total members.

* Internal Control Audit: A 7-member full-time internal audit team conducts on-site compliance checks globally. The firm enforces strict anti-nepotism protocols prohibiting the hiring of personnel within three degrees of kinship to current employees, alongside a zero-tolerance mandate on business entertainment or gifts.

* Diversity & Inclusion Metrics: Female executives comprise 16.7% of the roster (2 of 12). The statutory gender pay gap registers at 43.2% for all workers and 43.7% for regular employees, counterbalanced by an 84.7% childcare leave acquisition rate for male employees. Internal engagement targets consistently maintain a >70% positive response rate, supported by the Management Development Program (MDP) and Career Development Program (CDP).

HDIN Institutional Verdict

KEYENCE Corporation presents a structural anomaly within industrial automation metrics: the firm actively violates lean inventory principles to enforce downstream pricing dominance. By maintaining 150 to 156 Inventory Turnover Days (DIO) and stockpiling $570.13 million in inventory, the company completely eradicates order backlogs, executing a strict "immediate delivery" policy. This exact capital allocation choice enables the 83.02% Gross Profit Margin, as eliminating customer factory downtime neutralizes downstream price negotiation leverage.

Simultaneously, the SG&A expenditure profile functionally serves as the firm's true R&D engine. While nominal R&D stands at a highly optimized $219.56 million (under 3% of revenue), the $1,261.41 million deployed into human capital secures an elite tier of consultative sales engineers who embed directly onto client manufacturing floors. This disintermediation tactic recaptures third-party distribution margins and creates a continuous feedback loop that derisks new product development.

Consequently, while standard financial analysis would penalize the highly extended 235 to 250-day Cash Conversion Cycle (CCC) and the overcapitalized nature of a $24.54 billion asset base holding $20.11 billion in liquid/investment securities, these metrics validate KEYENCE Corporation's defensive posture. The mathematically high 13.53% ROE on a 94.6% Equity Ratio balance sheet verifies that the firm’s fabless architecture scales profit linearly against human capital investments, rather than depreciating physical assets.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."