Tobii AB: Aggressive Working Capital Liquidation and Software Pivot Near Stockholm, Sweden as 3% Top-Line Contraction Signals Severe Solvency Crisis

Date : 2026-06-17

Reading : 83

HDIN Executive Takeaways

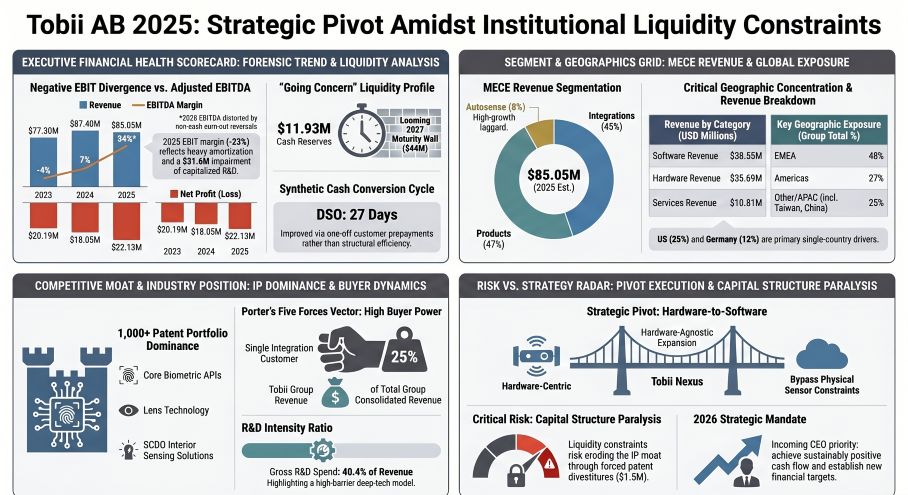

* Total 2025 revenue contracted 3% year-over-year to $85.05 million. A surface-level $43.85 million free cash flow turnaround was artificially engineered via a non-recurring $10.20 million component prepayment and massive inventory liquidation down to $4.18 million.

* The Stockholm-headquartered firm depends on single-source Asian component manufacturers, exposing its logistics networks to energy-linked cost volatility and trade tariff shocks while simultaneously lacking active legal provisions against biometric data processing risks.

* Institutional verdict warns of a critical capital shortfall. Following a $31.61 million intangible asset impairment, the remaining $74.75 million in capitalized R&D poses an existential threat to net equity, exacerbated by a -$49.05 million net debt load and an expiring $5.10 million credit facility.

Figure Tobii AB 2025: Strategic Pivot Amidst Institutional Liquidity Constraints

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Tobii AB [STO: TOBII] faces deteriorating top-line revenue alongside severe distortion in its operational profitability metrics. Total consolidated revenue contracted by 3% in 2025 to $85.05 million, continuing a volatile three-year revenue trajectory of $77.30 million (2023) and $87.40 million (2024). While the company maintained an 80% gross margin representing $68.12 million, core operational leverage is sharply deteriorating. Operating margin (EBIT) stood at -23%, while net profit losses widened to -$22.13 million.

The reported 34% EBITDA margin ($28.66 million) was mechanically inflated by a $6.83 million non-cash reversal of contingent consideration tied to underperforming FotoNation and Phasya acquisitions. The top line was heavily distorted by $20.60 million in non-recurring or expiring injections, including a $10.20 million component pre-purchase from Dynavox Group, a $5.30 million one-off compensation package, and $5.10 million from an acquired image processing contract that expired in the second quarter of 2025.

Working Capital Liquidation and Cash Flow Engineering

Management achieved an optically positive 2025 Operating Cash Flow (OCF) of $26.72 million and Free Cash Flow (FCF) of $8.67 million (reversing a -$35.18 million deficit in 2024). This $43.85 million FCF swing was strictly engineered via a $6.42 million positive working capital liquidation and a 50% suppression in capital expenditures to $17.74 million.

Table 1: Working Capital Management and Efficiency Metrics

Table 2: Working Capital Balances and Operating Efficiency Improvement Analysis

Segment and Product Portfolio Performance

* Products & Solutions (47% Share): Generated $39.77 million. The legacy segment recorded an organic revenue decline of 6% while gross margins compressed 100 basis points from 66% to 65%.

* Integrations (45% Share): Generated $38.14 million, demonstrating a 61% organic growth rate entirely distorted by the $10.20 million Dynavox pre-purchase. Revenue concentration is critical: a single OEM customer accounted for $21.62 million, representing 56% of segmental revenue and 25% of total group revenue.

* Autosense (8% Share): Generated $7.14 million, posting a 42% organic growth rate. However, the unit suffered a -$27.23 million operating loss, equating to a -384% margin, reflecting the high costs of automotive homologation.

Product Category Allocations

* Software: $38.55 million (45.3% of total). Concentrated in Integrations ($26.00 million) and Autosense ($5.20 million).

* Hardware: $35.69 million (42.0% of total). Driven by Products & Solutions ($28.25 million).

* Services: $10.81 million (12.7% of total).

Cost Structure and Aggressive R&D Capitalization

Gross R&D expenditures consumed $34.37 million, representing 40.4% of total revenue. Tobii capitalized 51.6% ($17.74 million) of this R&D onto the balance sheet. Factoring in $14.48 million in routine amortization and a massive $31.61 million impairment charge ($24.88 million for goodwill and $6.73 million for capitalized projects), the true net R&D expense hitting the income statement was $62.82 million, or 74% of revenue.

The $31.61 million impairment wiped out goodwill across Autosense ($21.62 million) and Integrations ($3.26 million), isolating the remaining $4.18 million in goodwill exclusively within the stagnating Products & Solutions segment. Selling, General, and Administrative (SG&A) expenses totaled $36.20 million (42.6% of revenue), split between $24.88 million in selling and $11.32 million in administrative costs. This followed a cost savings program that reduced operating expenses by $26.82 million, exceeding the initial $20.39 million target.

Infrastructure Layout and Regional Moats

Tobii operates a centralized research and corporate headquarters in Stockholm, Sweden, enforcing an asset-light supply chain highly dependent on third-party manufacturers in Asia. Global direct sales, regional integration, and localized assembly are managed through subsidiaries located across 12 countries: Switzerland, China, Taiwan, China, the United States, the United Kingdom, Japan, South Korea, Ireland, Romania, Germany, Belgium, and Singapore.

Geographic Revenue Distributions

* EMEA (Europe, Middle East, Africa): $40.82 million (48% of total). Germany functions as the primary driver, generating 12% of the global consolidated revenue.

* Americas: $22.96 million (27% of total). The United States market contributes 25% to global group sales.

* Asia-Pacific & Rest of World: $21.26 million (25% of total). Japan accounts for 12% and China accounts for 9% of total sales.

Technological Architecture and IP Dependency

Tobii maintains a proprietary barrier composed of over 1,000 patents, covering core biometric signal APIs and Lens Technology designed to encapsulate sensors within precision optics. Product configurations target distinct hardware and software channels. Hardware portfolios include wearable platforms like Tobii Glasses X and screen-based trackers such as the Tobii Pro Spectrum. Software offerings focus on behavioral analytics via Tobii Pro Lab, Sticky by Tobii, and the cloud-centric Tobii Glasses Explore. To combat hardware commoditization, the firm launched Tobii Nexus, a hardware-agnostic platform allowing eye tracking via standard webcams.

In the automotive sector, Tobii relies on its Single Camera Driver and Occupant (SCDO) monitoring system. The technology has secured EU homologation ahead of 2026 mandates and achieved mass production with a European premium car manufacturer. Active deployment currently covers 1,000,000 vehicles on the road across 160 vehicle models and 12 OEM brands.

Supply Chain Vulnerabilities and Regulatory Exposure

The upstream value chain relies on single-source suppliers for highly specialized sensors, micro-optics, and off-the-shelf Neural Processing Unit (NPU) components. The drawdown of inventory buffers to just $4.18 million directly limits protection against incoming climate-driven transition risks, which management expects will generate higher supplier and logistics costs alongside energy-linked cost volatility. Furthermore, despite processing sensitive GDPR-regulated biometric data and operating in China and the US, Tobii recorded zero confirmed employee personal data breaches. The firm has set aside exactly $0.00 for warranty provisions and a negligible $0.10 million for other provisions, reflecting zero active capital ring-fenced for intellectual property defense or regulatory fines. The firm divested non-core image processing patents for $1.53 million to generate immediate cash.

HDIN Institutional Verdict

Tobii AB is operating under a formal "going concern" material uncertainty warning issued by independent auditor PwC, a categorization completely justified by the firm's fracturing capital structure and leadership instability. The strategic pivot toward software licensing is a forced mechanism to bypass the severe commoditization of its legacy hardware business. Big Tech competitors (Apple, Meta) and specialized automotive peers (Smart Eye, Seeing Machines) present direct threats to Tobii's OEM integration model, which lacks binding volume guarantees.

Capital Structure and Balance Sheet Encumbrances

Tobii’s cash position deteriorated to $11.93 million. Immediate liquidity relies on an expiring $5.10 million credit facility, of which $4.79 million is currently utilized, set to mature in March 2026. The firm carries a net debt load of -$49.05 million, structured against a highly inflexible maturity wall. The liability matrix includes $23.35 million in deferred COVID-19 tax relief restructured into two tranches of $16.42 million and $6.93 million. While $9.28 million was repaid in 2025, the remainder strictly drains future cash flows through 2027. Furthermore, the company owes a USD 28 million promissory note tied to the FotoNation acquisition, carrying an 8% interest rate and maturing in 2027.

Off-balance sheet and encumbered liabilities further constrain capital allocation. Tobii holds $8.36 million in lease liabilities ($5.40 million long-term, $2.96 million short-term) carrying undiscounted future outflows of $9.08 million. The balance sheet is heavily pledged, featuring $40.79 million in corporate mortgages, $10.20 million in collateral pledged for credit facilities, and $30.59 million pledged against a promissory note from Xperi Inc. Contingent liabilities stand at $0.10 million for a subordination guarantee in the Swiss subsidiary. While the firm recognizes $9.28 million in Deferred Tax Assets (DTAs), an additional $117.38 million in unutilized loss carryforwards carry a full valuation allowance, confirming institutional skepticism regarding near-term profitability.

Intangible Asset Overvaluation Risks

Intangible assets comprise 62.7% of the entire $132.06 million balance sheet, totaling $82.81 million. This includes $74.75 million in Capitalized Development Costs (89.5% of intangibles), $4.18 million in Goodwill (5.0%), $2.65 million in Patents (3.2%), and $1.22 million in Other Intangibles (1.5%). Management applies a 14.8% pre-tax WACC and a 2.0% terminal growth rate to validate these assets. While sensitivity testing simulating a 200 basis point WACC increase (to 16.8%), a 200 basis point terminal growth reduction (to 0.0%), and a 200 basis point EBITA drop triggered no further theoretical impairment, the "Value in Use" methodology collapses if the firm enters insolvency. If commercialization fails, a write-down of the remaining $74.75 million in capitalized R&D would completely eradicate Tobii's $40.28 million in total equity. Minority interests are immaterial at $0.20 million.

Corporate Governance Breakdown

The simultaneous transition of CEO Anand Srivatsa (departed December 31, 2025) to Fadi Pharaon (effective January 1, 2026) and the appointment of interim CFO Åsa Wirén in May 2025 highlight a severe leadership vacuum. The five-member Board of Directors lost independent voices Sarah Eccleston and Jörgen Lantto, replacing them by electing co-founder Henrik Eskilsson. Combined with John Elvesjö, 40% of the directorial seats belong to non-independent founders. Total remuneration for the CEO and seven senior executives contracted to $1.90 million (down from $2.61 million for nine executives in 2024), with departing CEO Srivatsa securing $0.54 million. The Long-Term Incentive (LTI) hurdles targeting a 5% Total Shareholder Return are effectively obsolete given the stock price collapse to $0.29. Management instituted an ESPP 2025 share program offering a 15% incentive match for salary waivers, operating as a cash preservation mechanism detached from ESG metrics. Institutional capital flight validated this distress; foreign ownership fell from 10.6% to 7.7%, leaving Swedish retail and domestic holders to absorb 92.3% of the equity, with Avanza Pension holding 7.81%, followed by founders Eskilsson (5.36%), Mårten Skogö (4.56%), and Elvesjö (3.47%).

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Total 2025 revenue contracted 3% year-over-year to $85.05 million. A surface-level $43.85 million free cash flow turnaround was artificially engineered via a non-recurring $10.20 million component prepayment and massive inventory liquidation down to $4.18 million.

* The Stockholm-headquartered firm depends on single-source Asian component manufacturers, exposing its logistics networks to energy-linked cost volatility and trade tariff shocks while simultaneously lacking active legal provisions against biometric data processing risks.

* Institutional verdict warns of a critical capital shortfall. Following a $31.61 million intangible asset impairment, the remaining $74.75 million in capitalized R&D poses an existential threat to net equity, exacerbated by a -$49.05 million net debt load and an expiring $5.10 million credit facility.

Figure Tobii AB 2025: Strategic Pivot Amidst Institutional Liquidity Constraints

Segmental Realities and Margin CompressionTobii AB [STO: TOBII] faces deteriorating top-line revenue alongside severe distortion in its operational profitability metrics. Total consolidated revenue contracted by 3% in 2025 to $85.05 million, continuing a volatile three-year revenue trajectory of $77.30 million (2023) and $87.40 million (2024). While the company maintained an 80% gross margin representing $68.12 million, core operational leverage is sharply deteriorating. Operating margin (EBIT) stood at -23%, while net profit losses widened to -$22.13 million.

The reported 34% EBITDA margin ($28.66 million) was mechanically inflated by a $6.83 million non-cash reversal of contingent consideration tied to underperforming FotoNation and Phasya acquisitions. The top line was heavily distorted by $20.60 million in non-recurring or expiring injections, including a $10.20 million component pre-purchase from Dynavox Group, a $5.30 million one-off compensation package, and $5.10 million from an acquired image processing contract that expired in the second quarter of 2025.

Working Capital Liquidation and Cash Flow Engineering

Management achieved an optically positive 2025 Operating Cash Flow (OCF) of $26.72 million and Free Cash Flow (FCF) of $8.67 million (reversing a -$35.18 million deficit in 2024). This $43.85 million FCF swing was strictly engineered via a $6.42 million positive working capital liquidation and a 50% suppression in capital expenditures to $17.74 million.

Table 1: Working Capital Management and Efficiency Metrics

| Metric | 2024 Balance | 2025 Balance | Efficiency Ratio Change |

|---|---|---|---|

| Accounts Receivable | $12.24M | $6.22M | DSO: 51 Days → 27 Days |

| Inventory | $7.75M | $4.18M | DIO: 164 Days → 90 Days |

| Accounts Payable | $4.08M | $3.47M | DPO: 86 Days → 75 Days |

Table 2: Working Capital Balances and Operating Efficiency Improvement Analysis

| Working Capital Indicator | FY2024 | FY2025 | Change |

|---|---|---|---|

| Days Sales Outstanding (DSO) | 51 Days | 27 Days | -24 Days |

| Days Inventory Outstanding (DIO) | 164 Days | 90 Days | -74 Days |

| Days Payables Outstanding (DPO) | 86 Days | 75 Days | -11 Days |

Segment and Product Portfolio Performance

* Products & Solutions (47% Share): Generated $39.77 million. The legacy segment recorded an organic revenue decline of 6% while gross margins compressed 100 basis points from 66% to 65%.

* Integrations (45% Share): Generated $38.14 million, demonstrating a 61% organic growth rate entirely distorted by the $10.20 million Dynavox pre-purchase. Revenue concentration is critical: a single OEM customer accounted for $21.62 million, representing 56% of segmental revenue and 25% of total group revenue.

* Autosense (8% Share): Generated $7.14 million, posting a 42% organic growth rate. However, the unit suffered a -$27.23 million operating loss, equating to a -384% margin, reflecting the high costs of automotive homologation.

Product Category Allocations

* Software: $38.55 million (45.3% of total). Concentrated in Integrations ($26.00 million) and Autosense ($5.20 million).

* Hardware: $35.69 million (42.0% of total). Driven by Products & Solutions ($28.25 million).

* Services: $10.81 million (12.7% of total).

Cost Structure and Aggressive R&D Capitalization

Gross R&D expenditures consumed $34.37 million, representing 40.4% of total revenue. Tobii capitalized 51.6% ($17.74 million) of this R&D onto the balance sheet. Factoring in $14.48 million in routine amortization and a massive $31.61 million impairment charge ($24.88 million for goodwill and $6.73 million for capitalized projects), the true net R&D expense hitting the income statement was $62.82 million, or 74% of revenue.

The $31.61 million impairment wiped out goodwill across Autosense ($21.62 million) and Integrations ($3.26 million), isolating the remaining $4.18 million in goodwill exclusively within the stagnating Products & Solutions segment. Selling, General, and Administrative (SG&A) expenses totaled $36.20 million (42.6% of revenue), split between $24.88 million in selling and $11.32 million in administrative costs. This followed a cost savings program that reduced operating expenses by $26.82 million, exceeding the initial $20.39 million target.

Infrastructure Layout and Regional Moats

Tobii operates a centralized research and corporate headquarters in Stockholm, Sweden, enforcing an asset-light supply chain highly dependent on third-party manufacturers in Asia. Global direct sales, regional integration, and localized assembly are managed through subsidiaries located across 12 countries: Switzerland, China, Taiwan, China, the United States, the United Kingdom, Japan, South Korea, Ireland, Romania, Germany, Belgium, and Singapore.

Geographic Revenue Distributions

* EMEA (Europe, Middle East, Africa): $40.82 million (48% of total). Germany functions as the primary driver, generating 12% of the global consolidated revenue.

* Americas: $22.96 million (27% of total). The United States market contributes 25% to global group sales.

* Asia-Pacific & Rest of World: $21.26 million (25% of total). Japan accounts for 12% and China accounts for 9% of total sales.

Technological Architecture and IP Dependency

Tobii maintains a proprietary barrier composed of over 1,000 patents, covering core biometric signal APIs and Lens Technology designed to encapsulate sensors within precision optics. Product configurations target distinct hardware and software channels. Hardware portfolios include wearable platforms like Tobii Glasses X and screen-based trackers such as the Tobii Pro Spectrum. Software offerings focus on behavioral analytics via Tobii Pro Lab, Sticky by Tobii, and the cloud-centric Tobii Glasses Explore. To combat hardware commoditization, the firm launched Tobii Nexus, a hardware-agnostic platform allowing eye tracking via standard webcams.

In the automotive sector, Tobii relies on its Single Camera Driver and Occupant (SCDO) monitoring system. The technology has secured EU homologation ahead of 2026 mandates and achieved mass production with a European premium car manufacturer. Active deployment currently covers 1,000,000 vehicles on the road across 160 vehicle models and 12 OEM brands.

Supply Chain Vulnerabilities and Regulatory Exposure

The upstream value chain relies on single-source suppliers for highly specialized sensors, micro-optics, and off-the-shelf Neural Processing Unit (NPU) components. The drawdown of inventory buffers to just $4.18 million directly limits protection against incoming climate-driven transition risks, which management expects will generate higher supplier and logistics costs alongside energy-linked cost volatility. Furthermore, despite processing sensitive GDPR-regulated biometric data and operating in China and the US, Tobii recorded zero confirmed employee personal data breaches. The firm has set aside exactly $0.00 for warranty provisions and a negligible $0.10 million for other provisions, reflecting zero active capital ring-fenced for intellectual property defense or regulatory fines. The firm divested non-core image processing patents for $1.53 million to generate immediate cash.

HDIN Institutional Verdict

Tobii AB is operating under a formal "going concern" material uncertainty warning issued by independent auditor PwC, a categorization completely justified by the firm's fracturing capital structure and leadership instability. The strategic pivot toward software licensing is a forced mechanism to bypass the severe commoditization of its legacy hardware business. Big Tech competitors (Apple, Meta) and specialized automotive peers (Smart Eye, Seeing Machines) present direct threats to Tobii's OEM integration model, which lacks binding volume guarantees.

Capital Structure and Balance Sheet Encumbrances

Tobii’s cash position deteriorated to $11.93 million. Immediate liquidity relies on an expiring $5.10 million credit facility, of which $4.79 million is currently utilized, set to mature in March 2026. The firm carries a net debt load of -$49.05 million, structured against a highly inflexible maturity wall. The liability matrix includes $23.35 million in deferred COVID-19 tax relief restructured into two tranches of $16.42 million and $6.93 million. While $9.28 million was repaid in 2025, the remainder strictly drains future cash flows through 2027. Furthermore, the company owes a USD 28 million promissory note tied to the FotoNation acquisition, carrying an 8% interest rate and maturing in 2027.

Off-balance sheet and encumbered liabilities further constrain capital allocation. Tobii holds $8.36 million in lease liabilities ($5.40 million long-term, $2.96 million short-term) carrying undiscounted future outflows of $9.08 million. The balance sheet is heavily pledged, featuring $40.79 million in corporate mortgages, $10.20 million in collateral pledged for credit facilities, and $30.59 million pledged against a promissory note from Xperi Inc. Contingent liabilities stand at $0.10 million for a subordination guarantee in the Swiss subsidiary. While the firm recognizes $9.28 million in Deferred Tax Assets (DTAs), an additional $117.38 million in unutilized loss carryforwards carry a full valuation allowance, confirming institutional skepticism regarding near-term profitability.

Intangible Asset Overvaluation Risks

Intangible assets comprise 62.7% of the entire $132.06 million balance sheet, totaling $82.81 million. This includes $74.75 million in Capitalized Development Costs (89.5% of intangibles), $4.18 million in Goodwill (5.0%), $2.65 million in Patents (3.2%), and $1.22 million in Other Intangibles (1.5%). Management applies a 14.8% pre-tax WACC and a 2.0% terminal growth rate to validate these assets. While sensitivity testing simulating a 200 basis point WACC increase (to 16.8%), a 200 basis point terminal growth reduction (to 0.0%), and a 200 basis point EBITA drop triggered no further theoretical impairment, the "Value in Use" methodology collapses if the firm enters insolvency. If commercialization fails, a write-down of the remaining $74.75 million in capitalized R&D would completely eradicate Tobii's $40.28 million in total equity. Minority interests are immaterial at $0.20 million.

Corporate Governance Breakdown

The simultaneous transition of CEO Anand Srivatsa (departed December 31, 2025) to Fadi Pharaon (effective January 1, 2026) and the appointment of interim CFO Åsa Wirén in May 2025 highlight a severe leadership vacuum. The five-member Board of Directors lost independent voices Sarah Eccleston and Jörgen Lantto, replacing them by electing co-founder Henrik Eskilsson. Combined with John Elvesjö, 40% of the directorial seats belong to non-independent founders. Total remuneration for the CEO and seven senior executives contracted to $1.90 million (down from $2.61 million for nine executives in 2024), with departing CEO Srivatsa securing $0.54 million. The Long-Term Incentive (LTI) hurdles targeting a 5% Total Shareholder Return are effectively obsolete given the stock price collapse to $0.29. Management instituted an ESPP 2025 share program offering a 15% incentive match for salary waivers, operating as a cash preservation mechanism detached from ESG metrics. Institutional capital flight validated this distress; foreign ownership fell from 10.6% to 7.7%, leaving Swedish retail and domestic holders to absorb 92.3% of the equity, with Avanza Pension holding 7.81%, followed by founders Eskilsson (5.36%), Mårten Skogö (4.56%), and Elvesjö (3.47%).

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."