Harmonic Drive Systems Inc.: 33% North American Capacity Expansion Near Massachusetts as $398.20M Top-Line Signals Structural Rebound

Date : 2026-06-18

Reading : 289

HDIN Executive Takeaways

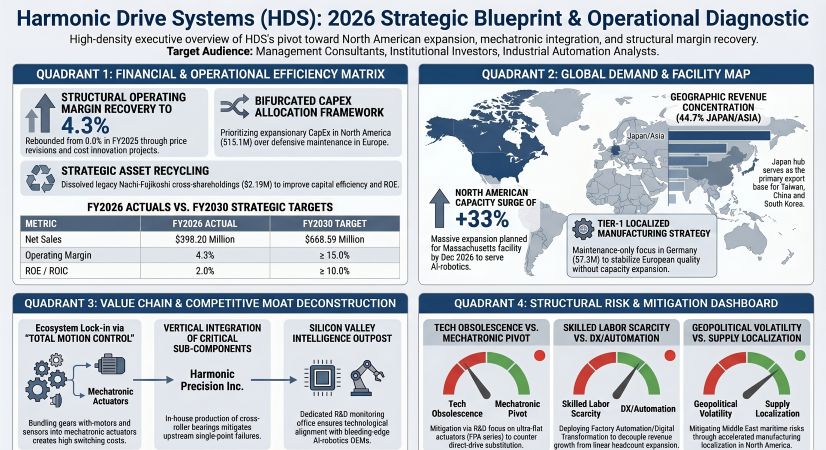

* Harmonic Drive Systems Inc. recovered operating margins to 4.3% on a $398.20 million top-line, though net income contracted 53.7% year-over-year strictly due to an absent $38.64 million base-year security sale gain.

* Capital expenditure pivots aggressively, deploying $8.45 million to expand Beverly, Massachusetts capacity by 33% by December 2026, while capping European deployments strictly to maintenance.

* A 2.0% return on equity and 0.53x asset turnover spotlight capital inefficiency, prompting a $668.59 million revenue target by fiscal 2030 against impending depreciation headwinds from a $33.76 million construction-in-progress balance.

Figure Harmonic Drive Systems (HDS): 2026 Strategic Blueprint & Operational Diagnostic

Segmental Realities and Capital Allocation Mechanics

Segmental Realities and Capital Allocation Mechanics

Harmonic Drive Systems Inc. [TYO: 6324] executed a margin turnaround during fiscal year 2026, generating $398.20 million in net sales, representing a 7.0% year-over-year expansion. This revenue base translated to a 30.4% gross margin, yielding $121.24 million in gross profit. Through strict cost controls and product price revisions, operating income rebounded from $46.8 thousand in the prior year to $17.17 million, structurally expanding the operating margin from 0.0% to 4.3%. However, net income fell 53.7% to $10.76 million, a bottom-line distortion entirely attributable to the absence of a one-time $38.64 million investment security sale recorded in FY2025. All figures assume a mandated exchange rate of 1 USD = 149.5686 JPY.

The company operates under a highly specialized business model divided into two core product lines:

* Reduction Gears: Generated $309.78 million, up 9.5% year-over-year, accounting for 77.8% of total revenue.

* Mechatronics Products: Generated $88.42 million, contracting 0.9% year-over-year, accounting for 22.2% of total revenue.

Regional profitability demonstrates a multi-polar reliance, with the domestic hub cross-subsidizing international operational costs:

* Japan (Includes Asia/Taiwan, China): Revenue of $178.02 million (+22.5%), contributing 44.7% of the top line. Profit expanded 66.1% to $24.70 million, yielding a 9.3% margin.

* Europe: Revenue of $112.17 million (+0.7%), contributing 28.2% of the top line. The segment returned to profitability at $4.31 million (2.6% margin) despite absorbing $6.7 million in intangible asset amortization.

* North America: Revenue of $80.95 million (+4.1%), contributing 20.3% of the top line. Profit contracted 5.0% to $3.53 million (2.9% margin) due to internal IT system upgrade costs.

* China: Revenue contracted 28.0% to $27.06 million (6.8% of top line), though favorable sales mixes increased segment profit by 26.5% to $2.55 million (6.3% margin).

Despite recovering margins, capital efficiency remains heavily suppressed. Return on Equity (ROE) fell to 2.0% from 4.4%, while asset turnover sits at an underperforming 0.53x against a $744.81 million total asset base. Management formally acknowledges the prior mid-term plan's failure, missing its $601.73 million sales target by 33.8%, its 15.0%–20.0% operating margin target by over 1,000 basis points, and its 10.0% ROE target by 800 basis points. The revised FY2030 guidance mandates $668.59 million in revenue, a 15.0% operating margin, and 10.0% ROE/ROIC metrics.

The balance sheet is highly capitalized. Net assets stand at $537.48 million, cementing a 72.2% equity ratio. Interest-bearing debt is limited to $88.39 million, equating to a 0.16x debt-to-equity ratio, backed by $127.65 million in cash equivalents. Operations generated $42.96 million in cash flow, fully funding $38.05 million in property, plant, and equipment capital expenditures, resulting in $4.91 million in positive free cash flow.

Capital allocation strategies aggressively uncoupled legacy holdings. The company divested its entire 107,000-share stake in Nachi-Fujikoshi Corp. [TYO: 6474] for $2.19 million, recycling capital to acquire 7,138,000 shares in ISDN Holdings Ltd. [SGX: I07] for $2.25 million. Shareholder returns included $5.41 million deployed to repurchase 264,800 shares, and a $0.134 annual dividend per share ($0.067 interim, $0.067 year-end), yielding a $12.67 million cash outflow and a 263.2% payout ratio against a 35% target policy. Foreign exchange hedging utilized forward contracts valuing $7.19 million to sell USD against JPY, and $3.86 million to sell CNY against JPY. Internal CapEx planning assumes long-term pegs of 1 USD = 150.00 JPY and 1 EUR = 175.00 JPY.

Infrastructure Layout and Geographic Production Moats

Harmonic Drive Systems executes a vertically integrated global footprint, balancing localized final assembly against centralized Japanese component machining. The physical infrastructure pipeline utilizes a segmented capital expenditure strategy across its subsidiaries, totaling $32.07 million in allocated segment CapEx for FY2026.

* North American Expansion: Harmonic Drive L.L.C. in Beverly, Massachusetts absorbed $15.12 million in FY2026, driving a 13% capacity expansion completed in December 2025. An additional $8.45 million is allocated to expand this facility by 33% by December 2026.

* Domestic Operations (Japan): The parent company allocated $9.50 million in FY2026. Forward deployments prioritize maintenance, allocating $26.25 million for the Hotaka and Ariake Plants in Azumino, Nagano by March 2027 (which includes $14.8 million specifically for baseline maintenance and IT). Harmonic Precision Inc. in Matsumoto completed a 3% capacity increase in March 2026 for cross-roller bearings. Future minor capacity expansions target Harmonic AD Inc. in Azumino (+2% capacity via $1.9 million) and Harmonic Winbell Co., Ltd. in Komagane (+3% capacity via $1.7 million). Total domestic subsidiary outlays combine to $5.96 million.

* European and Asian Nodes: Harmonic Drive SE in Limburg, Germany received $6.72 million in FY2026 and is scheduled for $7.31 million by December 2026 purely for maintenance, yielding 0% capacity growth. South Korean localized demand is supplied via Samick ADM Co., Ltd. in Daegu. The China segment absorbed $0.72 million exclusively for software upgrades.

The global workforce expanded to 1,419 personnel, with 627 employees stationed outside Japan. The parent company utilizes 526 employees averaging 42.5 years of age with 13.2 years of tenure. Average annual parent company compensation reached $48,091, a 2.1% year-over-year increase. R&D operations consumed $26.41 million (6.63% of net sales), employing 151 personnel. Innovation hubs include the Development & Technology Division, Harmonic Drive Laboratory, New Principle Mechanism Laboratory, and a Silicon Valley research outpost. Key technological pipelines focus on miniaturization and mechatronic bundling via the FPA Series, FHA-Cmini LW Type, and CSF-mini Series.

Procurement logistics are acutely exposed to maritime disruptions in the Strait of Hormuz and broader Middle East tensions. Core manufacturing relies heavily on steel, aluminum, copper, and rare earths, necessitating aggressive price hikes to offset input inflation and single-source capacity shortages.

HDIN Institutional Verdict and Structural Constraints

Harmonic Drive Systems currently functions as a highly liquid but capital-inefficient entity. A 72.2% equity ratio paired with a 2.0% ROE indicates the balance sheet is hoarding capital rather than deploying it effectively against its cost of capital. Governance modernization is actively progressing—the board configuration of 10 directors maintains 5 independent outside directors and increases female representation from 1 to 2 members. The Nomination and Remuneration Committee operates with 2 of its 3 members drawn from outside directors, limiting internal entrenchment.

However, the company's operational scalability is severely bottlenecked. The build-to-order (BTO) manufacturing model, while securing custom mechatronic ecosystem lock-in, prevents standardized volume growth. The impending capitalization of construction-in-progress (CIP) assets poses the most immediate financial threat. CIP balances expanded from $28.02 million to $33.76 million during FY2026 (with parent company CIP reaching $20.00 million). As these assets commission into active property, plant, and equipment by March 2027, the firm's existing $49.22 million depreciation burden will spike. If the hyper-growth targets tied to AI humanoid robotics fail to materialize and hit the $668.59 million FY2030 revenue threshold, these unabsorbed fixed overhead costs will structurally compress future operating margins.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Harmonic Drive Systems Inc. recovered operating margins to 4.3% on a $398.20 million top-line, though net income contracted 53.7% year-over-year strictly due to an absent $38.64 million base-year security sale gain.

* Capital expenditure pivots aggressively, deploying $8.45 million to expand Beverly, Massachusetts capacity by 33% by December 2026, while capping European deployments strictly to maintenance.

* A 2.0% return on equity and 0.53x asset turnover spotlight capital inefficiency, prompting a $668.59 million revenue target by fiscal 2030 against impending depreciation headwinds from a $33.76 million construction-in-progress balance.

Figure Harmonic Drive Systems (HDS): 2026 Strategic Blueprint & Operational Diagnostic

Segmental Realities and Capital Allocation MechanicsHarmonic Drive Systems Inc. [TYO: 6324] executed a margin turnaround during fiscal year 2026, generating $398.20 million in net sales, representing a 7.0% year-over-year expansion. This revenue base translated to a 30.4% gross margin, yielding $121.24 million in gross profit. Through strict cost controls and product price revisions, operating income rebounded from $46.8 thousand in the prior year to $17.17 million, structurally expanding the operating margin from 0.0% to 4.3%. However, net income fell 53.7% to $10.76 million, a bottom-line distortion entirely attributable to the absence of a one-time $38.64 million investment security sale recorded in FY2025. All figures assume a mandated exchange rate of 1 USD = 149.5686 JPY.

The company operates under a highly specialized business model divided into two core product lines:

* Reduction Gears: Generated $309.78 million, up 9.5% year-over-year, accounting for 77.8% of total revenue.

* Mechatronics Products: Generated $88.42 million, contracting 0.9% year-over-year, accounting for 22.2% of total revenue.

Regional profitability demonstrates a multi-polar reliance, with the domestic hub cross-subsidizing international operational costs:

* Japan (Includes Asia/Taiwan, China): Revenue of $178.02 million (+22.5%), contributing 44.7% of the top line. Profit expanded 66.1% to $24.70 million, yielding a 9.3% margin.

* Europe: Revenue of $112.17 million (+0.7%), contributing 28.2% of the top line. The segment returned to profitability at $4.31 million (2.6% margin) despite absorbing $6.7 million in intangible asset amortization.

* North America: Revenue of $80.95 million (+4.1%), contributing 20.3% of the top line. Profit contracted 5.0% to $3.53 million (2.9% margin) due to internal IT system upgrade costs.

* China: Revenue contracted 28.0% to $27.06 million (6.8% of top line), though favorable sales mixes increased segment profit by 26.5% to $2.55 million (6.3% margin).

Despite recovering margins, capital efficiency remains heavily suppressed. Return on Equity (ROE) fell to 2.0% from 4.4%, while asset turnover sits at an underperforming 0.53x against a $744.81 million total asset base. Management formally acknowledges the prior mid-term plan's failure, missing its $601.73 million sales target by 33.8%, its 15.0%–20.0% operating margin target by over 1,000 basis points, and its 10.0% ROE target by 800 basis points. The revised FY2030 guidance mandates $668.59 million in revenue, a 15.0% operating margin, and 10.0% ROE/ROIC metrics.

The balance sheet is highly capitalized. Net assets stand at $537.48 million, cementing a 72.2% equity ratio. Interest-bearing debt is limited to $88.39 million, equating to a 0.16x debt-to-equity ratio, backed by $127.65 million in cash equivalents. Operations generated $42.96 million in cash flow, fully funding $38.05 million in property, plant, and equipment capital expenditures, resulting in $4.91 million in positive free cash flow.

Capital allocation strategies aggressively uncoupled legacy holdings. The company divested its entire 107,000-share stake in Nachi-Fujikoshi Corp. [TYO: 6474] for $2.19 million, recycling capital to acquire 7,138,000 shares in ISDN Holdings Ltd. [SGX: I07] for $2.25 million. Shareholder returns included $5.41 million deployed to repurchase 264,800 shares, and a $0.134 annual dividend per share ($0.067 interim, $0.067 year-end), yielding a $12.67 million cash outflow and a 263.2% payout ratio against a 35% target policy. Foreign exchange hedging utilized forward contracts valuing $7.19 million to sell USD against JPY, and $3.86 million to sell CNY against JPY. Internal CapEx planning assumes long-term pegs of 1 USD = 150.00 JPY and 1 EUR = 175.00 JPY.

Infrastructure Layout and Geographic Production Moats

Harmonic Drive Systems executes a vertically integrated global footprint, balancing localized final assembly against centralized Japanese component machining. The physical infrastructure pipeline utilizes a segmented capital expenditure strategy across its subsidiaries, totaling $32.07 million in allocated segment CapEx for FY2026.

* North American Expansion: Harmonic Drive L.L.C. in Beverly, Massachusetts absorbed $15.12 million in FY2026, driving a 13% capacity expansion completed in December 2025. An additional $8.45 million is allocated to expand this facility by 33% by December 2026.

* Domestic Operations (Japan): The parent company allocated $9.50 million in FY2026. Forward deployments prioritize maintenance, allocating $26.25 million for the Hotaka and Ariake Plants in Azumino, Nagano by March 2027 (which includes $14.8 million specifically for baseline maintenance and IT). Harmonic Precision Inc. in Matsumoto completed a 3% capacity increase in March 2026 for cross-roller bearings. Future minor capacity expansions target Harmonic AD Inc. in Azumino (+2% capacity via $1.9 million) and Harmonic Winbell Co., Ltd. in Komagane (+3% capacity via $1.7 million). Total domestic subsidiary outlays combine to $5.96 million.

* European and Asian Nodes: Harmonic Drive SE in Limburg, Germany received $6.72 million in FY2026 and is scheduled for $7.31 million by December 2026 purely for maintenance, yielding 0% capacity growth. South Korean localized demand is supplied via Samick ADM Co., Ltd. in Daegu. The China segment absorbed $0.72 million exclusively for software upgrades.

The global workforce expanded to 1,419 personnel, with 627 employees stationed outside Japan. The parent company utilizes 526 employees averaging 42.5 years of age with 13.2 years of tenure. Average annual parent company compensation reached $48,091, a 2.1% year-over-year increase. R&D operations consumed $26.41 million (6.63% of net sales), employing 151 personnel. Innovation hubs include the Development & Technology Division, Harmonic Drive Laboratory, New Principle Mechanism Laboratory, and a Silicon Valley research outpost. Key technological pipelines focus on miniaturization and mechatronic bundling via the FPA Series, FHA-Cmini LW Type, and CSF-mini Series.

Procurement logistics are acutely exposed to maritime disruptions in the Strait of Hormuz and broader Middle East tensions. Core manufacturing relies heavily on steel, aluminum, copper, and rare earths, necessitating aggressive price hikes to offset input inflation and single-source capacity shortages.

HDIN Institutional Verdict and Structural Constraints

Harmonic Drive Systems currently functions as a highly liquid but capital-inefficient entity. A 72.2% equity ratio paired with a 2.0% ROE indicates the balance sheet is hoarding capital rather than deploying it effectively against its cost of capital. Governance modernization is actively progressing—the board configuration of 10 directors maintains 5 independent outside directors and increases female representation from 1 to 2 members. The Nomination and Remuneration Committee operates with 2 of its 3 members drawn from outside directors, limiting internal entrenchment.

However, the company's operational scalability is severely bottlenecked. The build-to-order (BTO) manufacturing model, while securing custom mechatronic ecosystem lock-in, prevents standardized volume growth. The impending capitalization of construction-in-progress (CIP) assets poses the most immediate financial threat. CIP balances expanded from $28.02 million to $33.76 million during FY2026 (with parent company CIP reaching $20.00 million). As these assets commission into active property, plant, and equipment by March 2027, the firm's existing $49.22 million depreciation burden will spike. If the hyper-growth targets tied to AI humanoid robotics fail to materialize and hit the $668.59 million FY2030 revenue threshold, these unabsorbed fixed overhead costs will structurally compress future operating margins.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."