Qualisys Holding AB: 2026 SaaS Pivot and APAC Expansion Yield 5.85% Revenue Growth Amid 120 bps Margin Contraction

Date : 2026-06-18

Reading : 178

HDIN Executive Takeaways

* FY2025 top-line expanded 5.85% YoY to $27.44 million, anchored by a 45% surge in Engineering applications, though FX volatility and IPO-related OPEX compressed Adjusted EBIT margins by 210 basis points to 19.2%.

* Operating cash flow contracted 49.6% to $3.16 million driven by a -$1.84 million working capital buildup, yet the firm maintained zero financial debt and executed $3.06 million in dividend distributions.

* The January 2026 rollout of the OnTraq markerless platform fundamentally shifts the monetization architecture toward recurring cloud subscriptions, buffering the historical volatility of hardware capital expenditures.

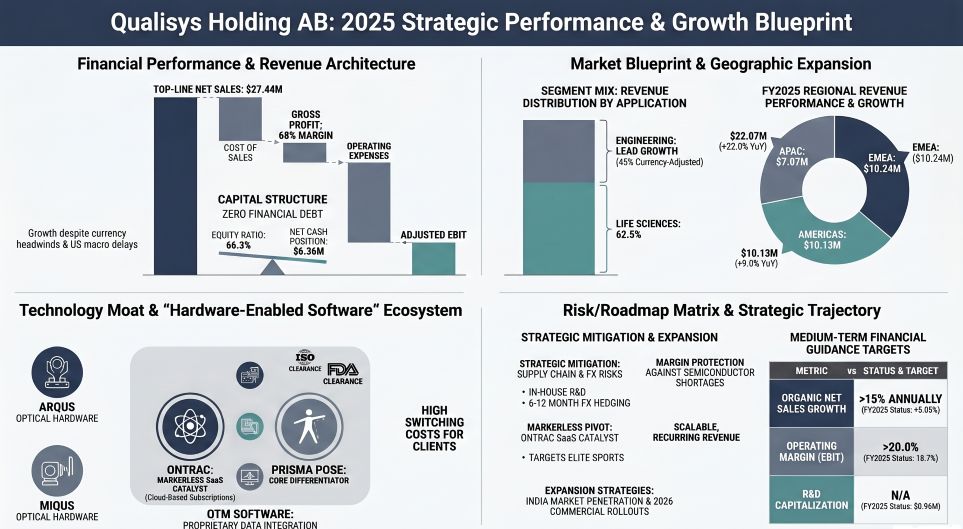

Figure Qualisys Holding AB: 2025 Strategic Performance & Growth Blueprint

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Qualisys Holding AB [NASDAQ FIRST NORTH: QUALISYS] recorded a 5.85% Year-over-Year top-line expansion, generating $27.44 million (269.05 million SEK) in FY2025 net sales against $25.92 million in FY2024. All financial conversions reflect the mandated 1 USD = 9.806 SEK rate.

Revenue Segments & Geographies:

* Life Sciences: $17.16 million (62.5% of total, a -3.4% YoY contraction).

* Engineering: $9.67 million (35.2% of total, growing 45% YoY on a currency-adjusted basis).

* Entertainment: $0.61 million (2.2% of total, executing 42% YoY growth).

* Geographic Mix: EMEA provided $10.24 million (37.3%), the Americas contributed $10.13 million (36.9%, muted at 9% local growth due to US government shutdowns), and APAC delivered $7.07 million (69,358 TSEK, 25.8% weight) following a 22% regional expansion.

* Operating Leverage & Margins:

* Gross margins contracted 120 basis points to 68.0% from 69.2%, pressured by unhedged FX exposure against a 53% USD, 30% EUR, and 8% GBP currency mix, despite active 6-to-12-month forward hedging contracts.

* Operating Expenses (OPEX) outpaced revenue, rising 6.03% YoY to $23.00 million.

* Reported EBIT posted flat 0.23% YoY growth to $5.13 million (vs. $5.12 million in FY2024). Adjusted EBIT declined 4.61% YoY to $5.28 million, excluding $0.14 million in non-recurring adjustments related to the public market listing. Consequently, Adjusted EBIT margins compressed from 21.3% to 19.2%.

* Net profit dropped 8.05% YoY to $3.73 million.

* Cost Architecture & Capitalization:

* R&D expenditure measured $2.86 million (10.4% of total revenue). The firm capitalized $0.96 million (9,388 TSEK) of this work—an increase from the $0.72 million (7,013 TSEK) capitalized in FY2024—amortized on a 5-to-10-year straight-line schedule.

* SG&A metrics reflect operational scaling: Personnel expenses advanced 5% YoY to $8.68 million, while other external expenses tallied $4.84 million.

* A non-operating impairment of $0.32 million (3,158 TSEK) permanently reduced "Other long-term securities holdings" to a zero carrying value.

* Cash Flow & Working Capital Dynamics:

* Operating Cash Flow (CFO) collapsed 49.6% YoY to $3.16 million.

* Working capital absorption was the primary drag, requiring a -$1.84 million cash injection compared to a +$0.94 million release in FY2024. Operating receivables directly absorbed -$1.48 million.

* The cash conversion cycle severely degraded from 107.1% to 50.6%.

* Investing Cash Flow (CFI) outflows expanded to -$1.17 million, suppressing Free Cash Flow to $2.00 million.

* Balance Sheet Integrity & Accounting Provisions:

* Net cash stood at $6.36 million, supported by zero financial borrowings and a pristine 66.3% equity ratio. The firm utilized this liquidity to execute a $3.06 million dividend distribution.

* Deferred income fell to $0.49 million (4,852 TSEK) from $0.74 million (7,269 TSEK), while customer advances sit at $49.56 thousand (486 TSEK). Total accrued expenses and deferred income account for $2.09 million (20,538 TSEK).

* The Expected Credit Loss (ECL) provisions recognized $20.09 thousand (197 TSEK) against $23.76 thousand (233 TSEK) in FY2024, with confirmed losses at $12.95 thousand (127 TSEK) versus $8.97 thousand (88 TSEK).

* Deferred tax liabilities are recorded at $1.25 million (12,252 TSEK) against a deferred tax asset of $0.26 million (2,575 TSEK).

* Off-balance sheet pledged shares in the Qualisys AB operational subsidiary retain an $8.22 million (80,580 TSEK) carrying value. Historical company mortgages of $1.53 million (15,000 TSEK) were fully discharged to zero.

* The firm successfully unwound historical financial dependencies via a $7.62 million (74,685 TSEK) related-party settlement from anchor shareholder Vätterleden Invest AB prior to its public debut.

Infrastructure Layout and Regional Moats

Physical Architecture & Real Estate: Operating a strictly asset-light manufacturing model, all production is outsourced to third-party contract manufacturers, exposing the firm to extended semiconductor lead times. Facilities are entirely leased, commanding a right-of-use asset value of $2.56 million (25,121 TSEK). Operations are directed from the global headquarters at Kvarnbergsgatan 2 in Gothenburg, Sweden. Global logistics and sales are executed via wholly-owned subsidiary hubs located in Buffalo Grove, Illinois (USA); Fute North Road in Shanghai (China); New Industrial Road at the Solstice Business Center (Singapore); and Delhi (India).

Human Capital & Governance Layout: The enterprise manages an 83-person internal headcount (up from 76), geographically concentrated in Sweden with 63 employees (76% of total). International distribution includes 12 personnel in the US (14.5%), 4 in India (4.8%), 3 in China (3.6%), and 1 in Singapore (1.2%). The gender distribution is 65 men (78%) and 18 women (22%), with female representation at 20% within executive management. Product development is further supplemented by 12 external R&D contractors.

Executive Matrix & Remuneration: Following the January 10, 2025 share split (a 1:10,000 ratio yielding exactly 10,000,000 outstanding shares at a $0.005 / 0.05 SEK par value, approved on January 7) and the February 21, 2025 listing on the Nasdaq First North Premier Growth Market, the board formalized its oversight structure. CEO Ingemar Pettersson (appointed 2021) received a $222,517 (2,182 TSEK) base salary, $8,260 (81 TSEK) in variable pay, $35,488 (348 TSEK) in pension contributions, and $24,373 (239 TSEK) in benefits. Variable performance pay is strictly capped at 35% of fixed salary, and pensions at 20%, complemented by the 2025/2028 long-term warrant program. Chairman Peter Gille commanded $50,989 (500 TSEK), independent director Jenny Rosberg received $13,359 (131 TSEK), while standard independent fees (for Daniel Petersson and Henrik Nyberg) are set at $22,945 (225 TSEK). The 2025 fiscal year introduced CFO Magnus Holm and CMO Susanne Gerdin to the executive suite alongside veteran CTO Magnus Berlander (appointed 2007). The nomination committee is advised by David Jallo representing Ramhill AB, and auditing is overseen by PwC’s Johan Palmgren.

Technological & Regulatory Moats: Supplying over 3,000 customers across 85 countries, the hardware stack controls proprietary optical endpoints. This includes the Arqus family (featuring extreme-weather protection and MRI-compatibility) and the Miqus tier (incorporating Miqus Video Plus and Hybrid models), alongside specialized enclosures pressure-tested for operability up to 40 meters underwater. Legacy sales bundle 1-to-3-year advance-invoiced support contracts using the Qualisys Track Manager (QTM) processing layer. Compliance barriers are fortified by ISO 9001:2015, the newly achieved January 2026 ISO/IEC 27001 information security certification, and active Medical Device Directive (MDD) / FDA clearances.

HDIN Institutional Verdict

Management's formal medium-term guidance targets a minimum 15% organic net sales increase alongside a 20% operating margin (EBIT). The FY2025 actuals missed both benchmarks (5.85% revenue growth and a 19.2% Adjusted EBIT margin). The delayed conversion of project-based capital expenditure into top-line revenue—exacerbated by US budget cycles—exposes the structural volatility of the firm's legacy hardware-first architecture.

The January 2026 rollout of the OnTraq markerless platform acts as the critical operational catalyst to flatten this revenue volatility. By delivering research-grade positional data without physical wearables, OnTraq allows elite athletic squads to complete baseline evaluation in 30 minutes. This alters the monetization model entirely, transitioning Qualisys from cyclical capital expenditures to a pure, scalable cloud-subscription ecosystem. When integrated with peripheral non-optical hardware (force plates, EMG) via facilities like Luxembourg’s SportFabrik, the proprietary QTM software pipeline creates prohibitive workflow switching costs. Qualisys possesses the unlevered balance sheet to easily absorb current working capital compression; however, tightening the collection cycle of its operating receivables remains paramount as the firm navigates its first year of quarterly public market scrutiny.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* FY2025 top-line expanded 5.85% YoY to $27.44 million, anchored by a 45% surge in Engineering applications, though FX volatility and IPO-related OPEX compressed Adjusted EBIT margins by 210 basis points to 19.2%.

* Operating cash flow contracted 49.6% to $3.16 million driven by a -$1.84 million working capital buildup, yet the firm maintained zero financial debt and executed $3.06 million in dividend distributions.

* The January 2026 rollout of the OnTraq markerless platform fundamentally shifts the monetization architecture toward recurring cloud subscriptions, buffering the historical volatility of hardware capital expenditures.

Figure Qualisys Holding AB: 2025 Strategic Performance & Growth Blueprint

Segmental Realities and Margin CompressionQualisys Holding AB [NASDAQ FIRST NORTH: QUALISYS] recorded a 5.85% Year-over-Year top-line expansion, generating $27.44 million (269.05 million SEK) in FY2025 net sales against $25.92 million in FY2024. All financial conversions reflect the mandated 1 USD = 9.806 SEK rate.

Revenue Segments & Geographies:

* Life Sciences: $17.16 million (62.5% of total, a -3.4% YoY contraction).

* Engineering: $9.67 million (35.2% of total, growing 45% YoY on a currency-adjusted basis).

* Entertainment: $0.61 million (2.2% of total, executing 42% YoY growth).

* Geographic Mix: EMEA provided $10.24 million (37.3%), the Americas contributed $10.13 million (36.9%, muted at 9% local growth due to US government shutdowns), and APAC delivered $7.07 million (69,358 TSEK, 25.8% weight) following a 22% regional expansion.

* Operating Leverage & Margins:

* Gross margins contracted 120 basis points to 68.0% from 69.2%, pressured by unhedged FX exposure against a 53% USD, 30% EUR, and 8% GBP currency mix, despite active 6-to-12-month forward hedging contracts.

* Operating Expenses (OPEX) outpaced revenue, rising 6.03% YoY to $23.00 million.

* Reported EBIT posted flat 0.23% YoY growth to $5.13 million (vs. $5.12 million in FY2024). Adjusted EBIT declined 4.61% YoY to $5.28 million, excluding $0.14 million in non-recurring adjustments related to the public market listing. Consequently, Adjusted EBIT margins compressed from 21.3% to 19.2%.

* Net profit dropped 8.05% YoY to $3.73 million.

* Cost Architecture & Capitalization:

* R&D expenditure measured $2.86 million (10.4% of total revenue). The firm capitalized $0.96 million (9,388 TSEK) of this work—an increase from the $0.72 million (7,013 TSEK) capitalized in FY2024—amortized on a 5-to-10-year straight-line schedule.

* SG&A metrics reflect operational scaling: Personnel expenses advanced 5% YoY to $8.68 million, while other external expenses tallied $4.84 million.

* A non-operating impairment of $0.32 million (3,158 TSEK) permanently reduced "Other long-term securities holdings" to a zero carrying value.

* Cash Flow & Working Capital Dynamics:

* Operating Cash Flow (CFO) collapsed 49.6% YoY to $3.16 million.

* Working capital absorption was the primary drag, requiring a -$1.84 million cash injection compared to a +$0.94 million release in FY2024. Operating receivables directly absorbed -$1.48 million.

* The cash conversion cycle severely degraded from 107.1% to 50.6%.

* Investing Cash Flow (CFI) outflows expanded to -$1.17 million, suppressing Free Cash Flow to $2.00 million.

* Balance Sheet Integrity & Accounting Provisions:

* Net cash stood at $6.36 million, supported by zero financial borrowings and a pristine 66.3% equity ratio. The firm utilized this liquidity to execute a $3.06 million dividend distribution.

* Deferred income fell to $0.49 million (4,852 TSEK) from $0.74 million (7,269 TSEK), while customer advances sit at $49.56 thousand (486 TSEK). Total accrued expenses and deferred income account for $2.09 million (20,538 TSEK).

* The Expected Credit Loss (ECL) provisions recognized $20.09 thousand (197 TSEK) against $23.76 thousand (233 TSEK) in FY2024, with confirmed losses at $12.95 thousand (127 TSEK) versus $8.97 thousand (88 TSEK).

* Deferred tax liabilities are recorded at $1.25 million (12,252 TSEK) against a deferred tax asset of $0.26 million (2,575 TSEK).

* Off-balance sheet pledged shares in the Qualisys AB operational subsidiary retain an $8.22 million (80,580 TSEK) carrying value. Historical company mortgages of $1.53 million (15,000 TSEK) were fully discharged to zero.

* The firm successfully unwound historical financial dependencies via a $7.62 million (74,685 TSEK) related-party settlement from anchor shareholder Vätterleden Invest AB prior to its public debut.

Infrastructure Layout and Regional Moats

Physical Architecture & Real Estate: Operating a strictly asset-light manufacturing model, all production is outsourced to third-party contract manufacturers, exposing the firm to extended semiconductor lead times. Facilities are entirely leased, commanding a right-of-use asset value of $2.56 million (25,121 TSEK). Operations are directed from the global headquarters at Kvarnbergsgatan 2 in Gothenburg, Sweden. Global logistics and sales are executed via wholly-owned subsidiary hubs located in Buffalo Grove, Illinois (USA); Fute North Road in Shanghai (China); New Industrial Road at the Solstice Business Center (Singapore); and Delhi (India).

Human Capital & Governance Layout: The enterprise manages an 83-person internal headcount (up from 76), geographically concentrated in Sweden with 63 employees (76% of total). International distribution includes 12 personnel in the US (14.5%), 4 in India (4.8%), 3 in China (3.6%), and 1 in Singapore (1.2%). The gender distribution is 65 men (78%) and 18 women (22%), with female representation at 20% within executive management. Product development is further supplemented by 12 external R&D contractors.

Executive Matrix & Remuneration: Following the January 10, 2025 share split (a 1:10,000 ratio yielding exactly 10,000,000 outstanding shares at a $0.005 / 0.05 SEK par value, approved on January 7) and the February 21, 2025 listing on the Nasdaq First North Premier Growth Market, the board formalized its oversight structure. CEO Ingemar Pettersson (appointed 2021) received a $222,517 (2,182 TSEK) base salary, $8,260 (81 TSEK) in variable pay, $35,488 (348 TSEK) in pension contributions, and $24,373 (239 TSEK) in benefits. Variable performance pay is strictly capped at 35% of fixed salary, and pensions at 20%, complemented by the 2025/2028 long-term warrant program. Chairman Peter Gille commanded $50,989 (500 TSEK), independent director Jenny Rosberg received $13,359 (131 TSEK), while standard independent fees (for Daniel Petersson and Henrik Nyberg) are set at $22,945 (225 TSEK). The 2025 fiscal year introduced CFO Magnus Holm and CMO Susanne Gerdin to the executive suite alongside veteran CTO Magnus Berlander (appointed 2007). The nomination committee is advised by David Jallo representing Ramhill AB, and auditing is overseen by PwC’s Johan Palmgren.

Technological & Regulatory Moats: Supplying over 3,000 customers across 85 countries, the hardware stack controls proprietary optical endpoints. This includes the Arqus family (featuring extreme-weather protection and MRI-compatibility) and the Miqus tier (incorporating Miqus Video Plus and Hybrid models), alongside specialized enclosures pressure-tested for operability up to 40 meters underwater. Legacy sales bundle 1-to-3-year advance-invoiced support contracts using the Qualisys Track Manager (QTM) processing layer. Compliance barriers are fortified by ISO 9001:2015, the newly achieved January 2026 ISO/IEC 27001 information security certification, and active Medical Device Directive (MDD) / FDA clearances.

HDIN Institutional Verdict

Management's formal medium-term guidance targets a minimum 15% organic net sales increase alongside a 20% operating margin (EBIT). The FY2025 actuals missed both benchmarks (5.85% revenue growth and a 19.2% Adjusted EBIT margin). The delayed conversion of project-based capital expenditure into top-line revenue—exacerbated by US budget cycles—exposes the structural volatility of the firm's legacy hardware-first architecture.

The January 2026 rollout of the OnTraq markerless platform acts as the critical operational catalyst to flatten this revenue volatility. By delivering research-grade positional data without physical wearables, OnTraq allows elite athletic squads to complete baseline evaluation in 30 minutes. This alters the monetization model entirely, transitioning Qualisys from cyclical capital expenditures to a pure, scalable cloud-subscription ecosystem. When integrated with peripheral non-optical hardware (force plates, EMG) via facilities like Luxembourg’s SportFabrik, the proprietary QTM software pipeline creates prohibitive workflow switching costs. Qualisys possesses the unlevered balance sheet to easily absorb current working capital compression; however, tightening the collection cycle of its operating receivables remains paramount as the firm navigates its first year of quarterly public market scrutiny.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."