Sonoma Pharmaceuticals: Over-The-Counter Retail Pivot Near Boulder as 37% Revenue Growth Signals Severe Working Capital Constraints

Date : 2026-06-19

Reading : 81

HDIN Executive Takeaways

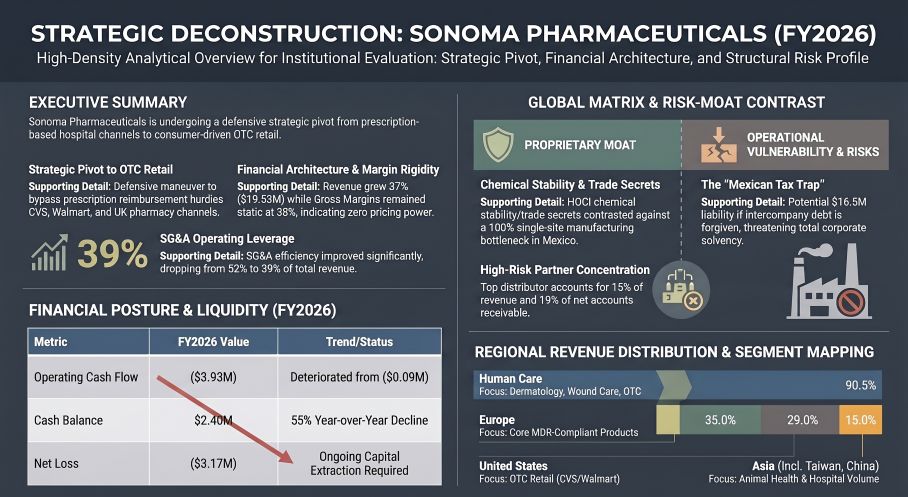

* U.S. retail channels propelled a 37% consolidated revenue expansion to $19.53 million, driving SG&A expenses down from 52% to 39% of total revenue despite zero underlying pricing power.

* Single-node manufacturing in Zapopan, Mexico poses structural bottlenecks; mandatory $2.91 million local tax prepayments directly forced operating cash flow deficits to $(3.93) million.

* Capital structure viability relies entirely on continuous equity dilution to offset an off-balance-sheet $16.5 million Mexican tax liability, evidenced by an April 2026 $3.57 million net public offering.

Figure STRATEGIC DECONSTRUCTION: SONOMA PHARMACEUTICALS (FY2026)

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Sonoma Pharmaceuticals, Inc. [NASDAQ: SNOA] executed a $5.24 million top-line expansion in FY2026, reaching $19.53 million in consolidated revenue. This 37% volume-driven growth was achieved exclusively through distribution network expansion, as Cost of Revenues scaled exactly in tandem at 37%, resulting in a stagnant 38% Gross Profit Margin across both FY2025 and FY2026. The financial architecture demonstrates absolute reliance on volume scaling rather than pricing leverage.

Operational leverage was realized strictly within operating expenses. SG&A expenses remained nearly flat at $7.61 million (a 3% variance), reducing SG&A as a percentage of revenue from 52% to 39%. Research and Development (R&D) expenditure, which operates on a strictly expensed accounting basis with zero capitalized R&D assets, increased by 25% to $2.27 million (12% of total revenue, compared to $1.814 million or 13% in FY2025). Stock-based compensation totaled $255,000 for the fiscal year.

Despite the top-line performance, the quality of earnings and cash conversion cycles deteriorated rapidly. The company reported a Net Loss of $(3.17) million, while Operating Cash Flow (OCF) collapsed to $(3.93) million, compared to a nominal $(88,000) cash burn in FY2025. This negative conversion was driven by a $1.31 million absorption into prepaid expenses and other current assets, directly linked to $2.91 million in prepaid taxes remitted to Mexican authorities.

Segmental and Balance Sheet Data Points:

* Human Care: Generated $17.68 million (90.5% of total revenue), an expansion of 40% from $12.63 million in FY2025.

* Animal Care: Generated $1.85 million (9.5% of total revenue), an expansion of 11.8% from $1.65 million in FY2025.

* Accounts Receivable: Expanded by 13.2% from $2.23 million to $2.53 million. Allowances for discounts and returns were recorded at an aggressively thin $19,000, up from $8,000 in FY2025.

* Inventory Dynamics: Gross inventory reached $4.26 million, accompanied by a 100% expansion in the obsolescence reserve from $298,000 to $614,000.

* Deferred Revenue: Contracted sharply from $658,000 to $284,000.

* Taxation Assets: The company holds $27.54 million in gross deferred tax assets, primarily driven by $95.5 million in U.S. federal net operating loss carryforwards, completely offset by a $26.55 million valuation allowance.

Infrastructure Layout and Regional Moats

Sonoma Pharmaceuticals centralizes its global supply chain at a single-point-of-failure manufacturing facility in Zapopan, Jalisco, Mexico. This subsidiary (Oculus Technologies of Mexico, S.A. de C.V.) employs 250 personnel and operates under dual leases of MXN 209,811 and MXN 213,625 per month (equating to $10,924 and $11,123 USD at a 19.2052 MXN/USD exchange rate). The facility maintains ISO 13485 certification and complies with FDA cGMP standards. Corporate operations are managed by 9 full-time employees at 5445 Conestoga Court, Suite 150, Boulder, Colorado, under a $3,688 monthly lease. A minor European presence, Sonoma Pharmaceuticals Netherlands, B.V., employs 1 full-time staff member. Total operating lease right-of-use assets sit at $602,000, with future minimum lease payments totaling $760,000 through FY2031. Net Property and Equipment is valued at $310,000, with FY2026 CapEx at $192,000 and FY2027 CapEx forecasted at $500,000.

The regional revenue mix is actively pivoting toward domestic U.S. markets to bypass international volatility and FX exposure (specifically Euro depreciation). International revenues declined from 82% to 71% of total sales.

Table Geographic Revenue Distribution

Commercialization relies heavily on concentrated third-party distribution. During FY2026, Customer C accounted for 15% of total revenues and 19% of net AR, while Customer A held 12% of AR. This represents high counterparty volatility compared to FY2025, where Customer B held 21% of revenues, Customer C held 18% of revenues, and Customer D held 24% of AR. Core distribution partners include Medline Industries LP (U.S./Canada), Compana Pet Brands (U.S.), Petagon (Asia/EU), and MicroSafe DMCC (Europe/Middle East/Australia). Over-the-counter retail expansions targeted Walmart, CVS, and over 1,200 Boots pharmacy stores in the U.K., alongside new regulatory approvals in Ukraine.

The proprietary hypochlorous acid (HOCl) product portfolio—including Reliefacyn Plus, Regenacyn Plus, Podiacyn, Lumacyn, MicrocynAH, MicrocynVS, Nanocyn, and the third-party Aquanil AD developed for Persōn & Covey, Inc.—faces escalating regulatory hurdles. The company holds 22 FDA 510(k) clearances and complies with the 2022 MoCRA mandates. However, a November 2023 FDA proposed rule threatens to reclassify HOCl wound washes into Class II medical devices, imposing costly new testing controls. Concurrently, strict EU MDR requirements forced the company to sideline secondary products including Sinudox, Microdacyn Oral, and MucoClyns due to prohibitive clinical trial economics.

HDIN Institutional Verdict

The board—comprising Amy Trombly, Vanessa Jacoby, Philippe Weigerstorfer, and Jerry McLaughlin—oversees a fundamentally insolvent operational model reliant on perpetual equity extraction. Despite 37% top-line expansion, Free Cash Flow (FCF) printed at $(4.12) million. Cash and cash equivalents collapsed by 55% from $5.37 million to $2.40 million. While third-party bank debt is nonexistent—limited to $222,000 in short-term financed insurance premiums—the capital structure is anchored by highly dilutive At-The-Market (ATM) executions yielding $427,000 net, culminating in a post-fiscal April 2026 public offering that raised $4.0 million gross ($3.57 million net). Governance alignment is further distorted by a protective executive severance clause securing an aggregated $475,000 annual salary against a 24-month trigger, representing a $1.425 million contingent liability. Stock options outstanding total 129,163 at a weighted average exercise price of $23.94 under the 2016, 2021, and 2024 Equity Incentive Plans.

The defining existential threat is the structural tax trap embedded in the Mexican subsidiary. The entity carries $12.3 million in principal intercompany debt, $10.4 million in technical assistance, and $32.2 million in accrued interest. Under Mexico's 3:1 thin capitalization rules, this debt interest cannot be deducted. Any conversion or forgiveness triggers an immediate 30% income tax liability (an estimated $16.5 million) alongside a 15% withholding tax penalty. While the company has extended the maturity of this debt by 5 years to 2032 and recognized a $5.56 million withholding tax payable on the balance sheet, this off-balance-sheet exposure dwarfs the firm's liquidity. Management's forward-looking statements regarding "progress towards profitability" lack quantitative margin targets and fail to address the mathematical reality of a business generating volume growth without internal capital formation.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* U.S. retail channels propelled a 37% consolidated revenue expansion to $19.53 million, driving SG&A expenses down from 52% to 39% of total revenue despite zero underlying pricing power.

* Single-node manufacturing in Zapopan, Mexico poses structural bottlenecks; mandatory $2.91 million local tax prepayments directly forced operating cash flow deficits to $(3.93) million.

* Capital structure viability relies entirely on continuous equity dilution to offset an off-balance-sheet $16.5 million Mexican tax liability, evidenced by an April 2026 $3.57 million net public offering.

Figure STRATEGIC DECONSTRUCTION: SONOMA PHARMACEUTICALS (FY2026)

Segmental Realities and Margin CompressionSonoma Pharmaceuticals, Inc. [NASDAQ: SNOA] executed a $5.24 million top-line expansion in FY2026, reaching $19.53 million in consolidated revenue. This 37% volume-driven growth was achieved exclusively through distribution network expansion, as Cost of Revenues scaled exactly in tandem at 37%, resulting in a stagnant 38% Gross Profit Margin across both FY2025 and FY2026. The financial architecture demonstrates absolute reliance on volume scaling rather than pricing leverage.

Operational leverage was realized strictly within operating expenses. SG&A expenses remained nearly flat at $7.61 million (a 3% variance), reducing SG&A as a percentage of revenue from 52% to 39%. Research and Development (R&D) expenditure, which operates on a strictly expensed accounting basis with zero capitalized R&D assets, increased by 25% to $2.27 million (12% of total revenue, compared to $1.814 million or 13% in FY2025). Stock-based compensation totaled $255,000 for the fiscal year.

Despite the top-line performance, the quality of earnings and cash conversion cycles deteriorated rapidly. The company reported a Net Loss of $(3.17) million, while Operating Cash Flow (OCF) collapsed to $(3.93) million, compared to a nominal $(88,000) cash burn in FY2025. This negative conversion was driven by a $1.31 million absorption into prepaid expenses and other current assets, directly linked to $2.91 million in prepaid taxes remitted to Mexican authorities.

Segmental and Balance Sheet Data Points:

* Human Care: Generated $17.68 million (90.5% of total revenue), an expansion of 40% from $12.63 million in FY2025.

* Animal Care: Generated $1.85 million (9.5% of total revenue), an expansion of 11.8% from $1.65 million in FY2025.

* Accounts Receivable: Expanded by 13.2% from $2.23 million to $2.53 million. Allowances for discounts and returns were recorded at an aggressively thin $19,000, up from $8,000 in FY2025.

* Inventory Dynamics: Gross inventory reached $4.26 million, accompanied by a 100% expansion in the obsolescence reserve from $298,000 to $614,000.

* Deferred Revenue: Contracted sharply from $658,000 to $284,000.

* Taxation Assets: The company holds $27.54 million in gross deferred tax assets, primarily driven by $95.5 million in U.S. federal net operating loss carryforwards, completely offset by a $26.55 million valuation allowance.

Infrastructure Layout and Regional Moats

Sonoma Pharmaceuticals centralizes its global supply chain at a single-point-of-failure manufacturing facility in Zapopan, Jalisco, Mexico. This subsidiary (Oculus Technologies of Mexico, S.A. de C.V.) employs 250 personnel and operates under dual leases of MXN 209,811 and MXN 213,625 per month (equating to $10,924 and $11,123 USD at a 19.2052 MXN/USD exchange rate). The facility maintains ISO 13485 certification and complies with FDA cGMP standards. Corporate operations are managed by 9 full-time employees at 5445 Conestoga Court, Suite 150, Boulder, Colorado, under a $3,688 monthly lease. A minor European presence, Sonoma Pharmaceuticals Netherlands, B.V., employs 1 full-time staff member. Total operating lease right-of-use assets sit at $602,000, with future minimum lease payments totaling $760,000 through FY2031. Net Property and Equipment is valued at $310,000, with FY2026 CapEx at $192,000 and FY2027 CapEx forecasted at $500,000.

The regional revenue mix is actively pivoting toward domestic U.S. markets to bypass international volatility and FX exposure (specifically Euro depreciation). International revenues declined from 82% to 71% of total sales.

Table Geographic Revenue Distribution

| Region | Revenue ($M) | Growth (%) | Share (%) | Notes |

| United States | $5.67 | +117% | 29% | Variance: +$3.06M |

| Europe | $6.90 | +25% | 35% | — |

| Asia | $2.90 | +25% | 15% | Includes Taiwan, China |

| Latin America | $2.37 | -20% | 12% | — |

| Rest of World | $1.68 | +92% | 9% | Led by ME & Australia |

| Total | $19.52 | — | 100% | Calculated |

Commercialization relies heavily on concentrated third-party distribution. During FY2026, Customer C accounted for 15% of total revenues and 19% of net AR, while Customer A held 12% of AR. This represents high counterparty volatility compared to FY2025, where Customer B held 21% of revenues, Customer C held 18% of revenues, and Customer D held 24% of AR. Core distribution partners include Medline Industries LP (U.S./Canada), Compana Pet Brands (U.S.), Petagon (Asia/EU), and MicroSafe DMCC (Europe/Middle East/Australia). Over-the-counter retail expansions targeted Walmart, CVS, and over 1,200 Boots pharmacy stores in the U.K., alongside new regulatory approvals in Ukraine.

The proprietary hypochlorous acid (HOCl) product portfolio—including Reliefacyn Plus, Regenacyn Plus, Podiacyn, Lumacyn, MicrocynAH, MicrocynVS, Nanocyn, and the third-party Aquanil AD developed for Persōn & Covey, Inc.—faces escalating regulatory hurdles. The company holds 22 FDA 510(k) clearances and complies with the 2022 MoCRA mandates. However, a November 2023 FDA proposed rule threatens to reclassify HOCl wound washes into Class II medical devices, imposing costly new testing controls. Concurrently, strict EU MDR requirements forced the company to sideline secondary products including Sinudox, Microdacyn Oral, and MucoClyns due to prohibitive clinical trial economics.

HDIN Institutional Verdict

The board—comprising Amy Trombly, Vanessa Jacoby, Philippe Weigerstorfer, and Jerry McLaughlin—oversees a fundamentally insolvent operational model reliant on perpetual equity extraction. Despite 37% top-line expansion, Free Cash Flow (FCF) printed at $(4.12) million. Cash and cash equivalents collapsed by 55% from $5.37 million to $2.40 million. While third-party bank debt is nonexistent—limited to $222,000 in short-term financed insurance premiums—the capital structure is anchored by highly dilutive At-The-Market (ATM) executions yielding $427,000 net, culminating in a post-fiscal April 2026 public offering that raised $4.0 million gross ($3.57 million net). Governance alignment is further distorted by a protective executive severance clause securing an aggregated $475,000 annual salary against a 24-month trigger, representing a $1.425 million contingent liability. Stock options outstanding total 129,163 at a weighted average exercise price of $23.94 under the 2016, 2021, and 2024 Equity Incentive Plans.

The defining existential threat is the structural tax trap embedded in the Mexican subsidiary. The entity carries $12.3 million in principal intercompany debt, $10.4 million in technical assistance, and $32.2 million in accrued interest. Under Mexico's 3:1 thin capitalization rules, this debt interest cannot be deducted. Any conversion or forgiveness triggers an immediate 30% income tax liability (an estimated $16.5 million) alongside a 15% withholding tax penalty. While the company has extended the maturity of this debt by 5 years to 2032 and recognized a $5.56 million withholding tax payable on the balance sheet, this off-balance-sheet exposure dwarfs the firm's liquidity. Management's forward-looking statements regarding "progress towards profitability" lack quantitative margin targets and fail to address the mathematical reality of a business generating volume growth without internal capital formation.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."