Komatsu Ltd.: Global Supply Chain Decentralization Near Strategic Hubs as 13.7% Profit Contraction Signals Acute Margin Pressures

Date : 2026-06-20

Reading : 183

HDIN Executive Takeaways

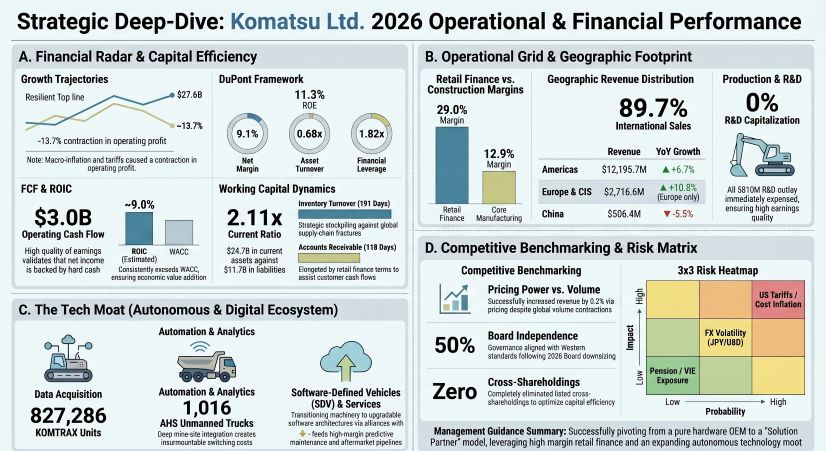

* Consolidated top-line revenue exhibited resilience, reaching $27,631.1 million (+0.7% YoY), while operating profit contracted 13.7% to $3,793.1 million due to US tariffs, geopolitical friction, and a 1.7 percentage point increase in COGS (reaching $19,207.9 million or 69.5% of revenue).

* The Retail Finance segment operated as a critical stabilizer against cyclical headwinds, generating an exceptional 29.0% profit margin and delivering $982,424 in operating profit per employee compared to the core manufacturing division’s $52,995.

* Capital discipline remains rigorous, highlighted by a fortress balance sheet (2.11x current ratio), the complete divestment of all listed cross-shareholdings, and a $668.6 million (100 billion JPY) share buyback program retiring 20.61 million shares.

Figure Komatsu 2026 0perational & Financial Performance

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Komatsu Ltd. [TYO: 6301] executed a highly defensive operational strategy in FY2026 amid localized currency volatility and escalating macroeconomic tariffs. The firm achieved total consolidated revenue of $27,631.1 million (4,132,751 million JPY), expanding by 0.7% year-over-year. However, the firm suffered an aggregate operating margin compression of 2.3 percentage points, dropping from 16.0% to 13.7%. Operating profit fell 13.7% YoY to $3,793.1 million, and net income attributable to shareholders declined 14.4% to $2,516.5 million (yielding a 9.1% net margin).

The 13.7% profit drop accurately reflects operational reality without artificial earnings smoothing. Impairment losses were contained at $25.7 million. Management absorbed the drag, recording fresh warranty accruals of $413.6 million (61,869 million JPY) against a usage of $354.1 million (52,967 million JPY), inflating the total warranty reserve to $493.4 million (73,798 million JPY).

Operating Cash Flow (OCF) generated $3,001.7 million, fully covering $1,332.0 million in Investing Cash Flow (ICF) and $1,394.2 million in Financing Cash Flow outflows. Return on Equity (ROE) stood at 11.3%, driven by an asset turnover of 0.678x (on total assets of ~$40,775.5 million), a financial leverage multiplier of 1.82x (on average equity of ~$22,344.8 million), and a Return on Assets (ROA) of 6.17%. ROIC structurally rests near 9.0%.

Table 1: FY2026 Segment Financial and Headcount Matrix

*Note: Total workforce includes 67,279 full-time employees and 4,465 temporary workers. All JPY conversions apply a rate of 1 USD = 149.5686 JPY.

The Retail Finance unit manages a massive receivables portfolio of $10,064.2 million (1,505,283 million JPY). During FY2026, the Allowance for Doubtful Accounts (ADA) ended at $135.9 million (20,323 million JPY) following a surge in write-offs to $79.3 million (11,867 million JPY) and fresh provisions of $42.1 million (6,295 million JPY). Off-balance sheet financing is strictly controlled; Variable Interest Entities (VIEs) hold a negligible $17.8 million (2,663 million JPY), while third-party supplier reverse factoring (settled in 60 to 110 days without Komatsu collateral) contracted from $173.6 million to $123.7 million (18,496 million JPY). Guarantees remain muted: $95.6 million (14,303 million JPY) for 1-5 year affiliate/dealer and 10-30 year employee housing loans, alongside $172.9 million (25,866 million JPY) for operational performance bonds.

Note: The "Oceania, Asia, & CIS" category is presented as an aggregate total in the source data.

The balance sheet is optimized for high liquidity. Current assets of $24,658.9 million dwarf current liabilities of $11,683.0 million, achieving a current ratio of 2.11x (+11.1 percentage points YoY) and a quick ratio greater than 1.0x. Total interest-bearing debt rests at $8,965.9 million (1,341,031 million JPY), structured as $3,701.0 million in short-term debt and $5,265.0 million in long-term obligations. Refinancing risk is neutralized by $2,939.8 million in cash equivalents and $2,199.5 million in unused commitment lines, anchoring an equity ratio of 54.7%. Heavy capital lock-up is evident in working capital: Inventory stands at $10,710.0 million (~191 turnover days, including $7,912.4 million in finished products), Accounts Receivable at $9,403.1 million (~118 days), and Accounts Payable strictly managed at $2,376.7 million (~44 days). Equipment capex order backlogs totaled $364.4 million (54,500 million JPY).

Infrastructure Layout and Regional Moats

Komatsu’s supply chain architecture is executing a rapid transition from cost-optimized centralization to a "cross-sourcing and multi-sourcing" framework. To absorb foreign exchange volatility—which alone erased $16.7 million (2.5 billion JPY) from the core segment's operating profit—the firm utilizes geographically diversified production nodes and deliberate safety stock accumulations. Advance Pricing Agreements (APA) adjusting cross-border transfer pricing between the parent company, Komatsu America Corp., and Komatsu Europe International N.V., generated an extraordinary income of $40.7 million (6,090 million JPY) against a loss of $41.6 million (6,227 million JPY).

* Japan (Mother Plants): Awazu, Osaka (bulldozers/excavators); Ibaraki (dump trucks/wheel loaders); Himi (castings); Shiga, Oyama (engines/hydraulics); Kanazawa (press machines).

* The Americas: Peoria, Milwaukee, Longview (US hubs for ultra-large mining rigs). Suzano (Brazil). Recent aftermarket expansion via the M&A acquisition of SRC of Lexington (heavy component remanufacturing).

* Europe: Birtley (UK); Düsseldorf, Hannover (Germany); Este (Italy); Umeå (Sweden, centered on forestry, reinforced by the Malwa Forest acquisition).

* Asia & Emerging Markets: Jakarta (Indonesia); Changzhou, Jining (China); Chonburi (Thailand); Kanchipuram (India). A new service/training facility was initiated in Côte d'Ivoire. A major equipment pipeline is secured at the Reko Diq copper/gold project in Pakistan.

Total consolidated R&D expenditures expanded by 9.7% to $810.2 million (121,177 million JPY), representing a 2.93% revenue intensity. Komatsu applies a 0% capitalization ratio, immediately expensing all R&D to fortify earnings transparency. Funds are aggressively deployed into electric micro-machinery (battery-electric micro-excavators, 2-to-3-ton mini excavators, 13-ton and 20-ton electric hydraulic excavators), hydrogen engine-powered ultra-large dump trucks, and ICT remote-controlled underwater construction robots (50 meters depth capability).

The firm leverages open innovation over pure internal development. Strategic R&D partners include Applied Intuition (mining Software-Defined Vehicles), Tier IV and Earthbrain Ltd. (commercializing autonomous civil engineering dump trucks by FY2027), Toyota Motor Corporation (mine-site light vehicles), and JAXA alongside Ritsumeikan University (lunar base construction spin-offs). The Komatsu GHG Alliance secures standard-setting dominance. The active monitoring fleet via KOMTRAX reached 827,286 units globally, while Smart Forestry Fleet Monitoring tracks 3,875 units. Autonomous Haulage System (AHS) unmanned dump trucks reached 1,016 units globally. ICT-equipped smart construction machinery achieved a 28.7% deployment rate across the US, Europe, Japan, and Australia.

HDIN Institutional Verdict

Komatsu’s FY2026 data confirms a structural pivot from a cyclical hardware OEM to a high-margin, aftermarket "Solution Partner." Capital efficiency metrics validate this execution. Executive compensation is tightly aligned with minority shareholder interests; the Board Incentive Plan (BIP) Trust enforces a malus/clawback provision and vests based on ROE (>10%), Net D/E (<6.0x), 30 social KPIs, and a 50% CO2 reduction by 2030. Annual bonuses rely on a 50% ROE, 25% ROA, and 25% Operating Margin weighted formula.

Institutional capital allocation is highly disciplined. The firm commits to a 40%+ dividend payout ratio (FY2026 actual payout 45.9% via a $1.27 / 190 JPY per share dividend). Legacy capital inefficiencies have been eliminated: Komatsu reduced unlisted cross-shareholdings by 8 entities down to 36 (valued at $25.8 million / 3,852 million JPY) and holds zero listed cross-shareholdings. A fresh $668.6 million (100 billion JPY) share buyback is authorized for H1 FY2027, matching the exact $668.6 million executed in FY2026. Board independence is scaling from 44.4% (4 of 9 directors) to 50.0% (4 of 8 directors post-AGM). The Audit board maintains 3 independent members out of 5, and the HR committee holds a 66.7% outside majority.

Table 3: Institutional Human Capital & Pension Risk Matrix

Komatsu’s aggressive remanufacturing acquisitions and 100% immediate R&D expensing prove leadership is willing to sacrifice short-term optical margins to widen its digital and geographic moats, ensuring sustainable ROIC performance above WACC.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Consolidated top-line revenue exhibited resilience, reaching $27,631.1 million (+0.7% YoY), while operating profit contracted 13.7% to $3,793.1 million due to US tariffs, geopolitical friction, and a 1.7 percentage point increase in COGS (reaching $19,207.9 million or 69.5% of revenue).

* The Retail Finance segment operated as a critical stabilizer against cyclical headwinds, generating an exceptional 29.0% profit margin and delivering $982,424 in operating profit per employee compared to the core manufacturing division’s $52,995.

* Capital discipline remains rigorous, highlighted by a fortress balance sheet (2.11x current ratio), the complete divestment of all listed cross-shareholdings, and a $668.6 million (100 billion JPY) share buyback program retiring 20.61 million shares.

Figure Komatsu 2026 0perational & Financial Performance

Segmental Realities and Margin CompressionKomatsu Ltd. [TYO: 6301] executed a highly defensive operational strategy in FY2026 amid localized currency volatility and escalating macroeconomic tariffs. The firm achieved total consolidated revenue of $27,631.1 million (4,132,751 million JPY), expanding by 0.7% year-over-year. However, the firm suffered an aggregate operating margin compression of 2.3 percentage points, dropping from 16.0% to 13.7%. Operating profit fell 13.7% YoY to $3,793.1 million, and net income attributable to shareholders declined 14.4% to $2,516.5 million (yielding a 9.1% net margin).

The 13.7% profit drop accurately reflects operational reality without artificial earnings smoothing. Impairment losses were contained at $25.7 million. Management absorbed the drag, recording fresh warranty accruals of $413.6 million (61,869 million JPY) against a usage of $354.1 million (52,967 million JPY), inflating the total warranty reserve to $493.4 million (73,798 million JPY).

Operating Cash Flow (OCF) generated $3,001.7 million, fully covering $1,332.0 million in Investing Cash Flow (ICF) and $1,394.2 million in Financing Cash Flow outflows. Return on Equity (ROE) stood at 11.3%, driven by an asset turnover of 0.678x (on total assets of ~$40,775.5 million), a financial leverage multiplier of 1.82x (on average equity of ~$22,344.8 million), and a Return on Assets (ROA) of 6.17%. ROIC structurally rests near 9.0%.

Table 1: FY2026 Segment Financial and Headcount Matrix

| Metric | Construction, Mining & Utility Equipment | Retail Finance | Industrial Machinery & Others | Eliminations / Corporate |

|---|---|---|---|---|

| Revenue | $25,446.8M | $843.3M | $1,596.3M | ($255.2M) |

| YoY Revenue Growth | +0.2% | +2.4% | +6.8% | — |

| Segment Profit | $3,283.6M | $244.6M | $253.6M | $36.9M |

| Profit Margin | 12.9% | 29.0% | 15.9% | — |

| YoY Profit Growth | -18.0% | +24.4% | +38.5% | — |

| Headcount | 61,960 | 249 | 4,276 | 794 |

| Workforce Share | 92.1% | 0.4% | 6.4% | 1.2% |

| Revenue per Employee | $410,697 | $3,386,903 | $373,306 | N/A |

| Profit per Employee | $52,995 | $982,424 | $59,318 | N/A |

| Production Value | $25,798.2M | N/A | $1,426.1M | N/A |

| Production Growth | +3.1% | N/A | -1.9% | N/A |

| R&D Expense | $742.9M | N/A | $67.3M | N/A |

| ROA | N/A | 2.4% | N/A | N/A |

| Net Debt / Equity | N/A | 4.45x | N/A | N/A |

The Retail Finance unit manages a massive receivables portfolio of $10,064.2 million (1,505,283 million JPY). During FY2026, the Allowance for Doubtful Accounts (ADA) ended at $135.9 million (20,323 million JPY) following a surge in write-offs to $79.3 million (11,867 million JPY) and fresh provisions of $42.1 million (6,295 million JPY). Off-balance sheet financing is strictly controlled; Variable Interest Entities (VIEs) hold a negligible $17.8 million (2,663 million JPY), while third-party supplier reverse factoring (settled in 60 to 110 days without Komatsu collateral) contracted from $173.6 million to $123.7 million (18,496 million JPY). Guarantees remain muted: $95.6 million (14,303 million JPY) for 1-5 year affiliate/dealer and 10-30 year employee housing loans, alongside $172.9 million (25,866 million JPY) for operational performance bonds.

Table 2: Global Sales Distribution: Construction & Mining

| Region | Sales (USD Millions) | YoY Growth |

| Americas | $12,195.7M | +6.7% |

| - North America | $7,001.3M | +2.0% |

| - Latin America | $5,194.3M | +13.7% |

| Europe & CIS | $2,716.6M | — |

| - Europe | $2,298.4M | +10.8% |

| - CIS | $418.2M | +1.7% |

| Oceania, Asia, & CIS (Total) | $6,316.8M | — |

| - Oceania | $3,152.8M | +2.3% |

| - Asia (ex-JP/CH) | $2,239.3M | -32.9% |

| Africa | $1,713.3M | +15.9% |

| Japan | $2,102.8M | -4.6% |

| China | $506.4M | -5.5% |

The balance sheet is optimized for high liquidity. Current assets of $24,658.9 million dwarf current liabilities of $11,683.0 million, achieving a current ratio of 2.11x (+11.1 percentage points YoY) and a quick ratio greater than 1.0x. Total interest-bearing debt rests at $8,965.9 million (1,341,031 million JPY), structured as $3,701.0 million in short-term debt and $5,265.0 million in long-term obligations. Refinancing risk is neutralized by $2,939.8 million in cash equivalents and $2,199.5 million in unused commitment lines, anchoring an equity ratio of 54.7%. Heavy capital lock-up is evident in working capital: Inventory stands at $10,710.0 million (~191 turnover days, including $7,912.4 million in finished products), Accounts Receivable at $9,403.1 million (~118 days), and Accounts Payable strictly managed at $2,376.7 million (~44 days). Equipment capex order backlogs totaled $364.4 million (54,500 million JPY).

Infrastructure Layout and Regional Moats

Komatsu’s supply chain architecture is executing a rapid transition from cost-optimized centralization to a "cross-sourcing and multi-sourcing" framework. To absorb foreign exchange volatility—which alone erased $16.7 million (2.5 billion JPY) from the core segment's operating profit—the firm utilizes geographically diversified production nodes and deliberate safety stock accumulations. Advance Pricing Agreements (APA) adjusting cross-border transfer pricing between the parent company, Komatsu America Corp., and Komatsu Europe International N.V., generated an extraordinary income of $40.7 million (6,090 million JPY) against a loss of $41.6 million (6,227 million JPY).

* Japan (Mother Plants): Awazu, Osaka (bulldozers/excavators); Ibaraki (dump trucks/wheel loaders); Himi (castings); Shiga, Oyama (engines/hydraulics); Kanazawa (press machines).

* The Americas: Peoria, Milwaukee, Longview (US hubs for ultra-large mining rigs). Suzano (Brazil). Recent aftermarket expansion via the M&A acquisition of SRC of Lexington (heavy component remanufacturing).

* Europe: Birtley (UK); Düsseldorf, Hannover (Germany); Este (Italy); Umeå (Sweden, centered on forestry, reinforced by the Malwa Forest acquisition).

* Asia & Emerging Markets: Jakarta (Indonesia); Changzhou, Jining (China); Chonburi (Thailand); Kanchipuram (India). A new service/training facility was initiated in Côte d'Ivoire. A major equipment pipeline is secured at the Reko Diq copper/gold project in Pakistan.

Total consolidated R&D expenditures expanded by 9.7% to $810.2 million (121,177 million JPY), representing a 2.93% revenue intensity. Komatsu applies a 0% capitalization ratio, immediately expensing all R&D to fortify earnings transparency. Funds are aggressively deployed into electric micro-machinery (battery-electric micro-excavators, 2-to-3-ton mini excavators, 13-ton and 20-ton electric hydraulic excavators), hydrogen engine-powered ultra-large dump trucks, and ICT remote-controlled underwater construction robots (50 meters depth capability).

The firm leverages open innovation over pure internal development. Strategic R&D partners include Applied Intuition (mining Software-Defined Vehicles), Tier IV and Earthbrain Ltd. (commercializing autonomous civil engineering dump trucks by FY2027), Toyota Motor Corporation (mine-site light vehicles), and JAXA alongside Ritsumeikan University (lunar base construction spin-offs). The Komatsu GHG Alliance secures standard-setting dominance. The active monitoring fleet via KOMTRAX reached 827,286 units globally, while Smart Forestry Fleet Monitoring tracks 3,875 units. Autonomous Haulage System (AHS) unmanned dump trucks reached 1,016 units globally. ICT-equipped smart construction machinery achieved a 28.7% deployment rate across the US, Europe, Japan, and Australia.

HDIN Institutional Verdict

Komatsu’s FY2026 data confirms a structural pivot from a cyclical hardware OEM to a high-margin, aftermarket "Solution Partner." Capital efficiency metrics validate this execution. Executive compensation is tightly aligned with minority shareholder interests; the Board Incentive Plan (BIP) Trust enforces a malus/clawback provision and vests based on ROE (>10%), Net D/E (<6.0x), 30 social KPIs, and a 50% CO2 reduction by 2030. Annual bonuses rely on a 50% ROE, 25% ROA, and 25% Operating Margin weighted formula.

Institutional capital allocation is highly disciplined. The firm commits to a 40%+ dividend payout ratio (FY2026 actual payout 45.9% via a $1.27 / 190 JPY per share dividend). Legacy capital inefficiencies have been eliminated: Komatsu reduced unlisted cross-shareholdings by 8 entities down to 36 (valued at $25.8 million / 3,852 million JPY) and holds zero listed cross-shareholdings. A fresh $668.6 million (100 billion JPY) share buyback is authorized for H1 FY2027, matching the exact $668.6 million executed in FY2026. Board independence is scaling from 44.4% (4 of 9 directors) to 50.0% (4 of 8 directors post-AGM). The Audit board maintains 3 independent members out of 5, and the HR committee holds a 66.7% outside majority.

Table 3: Institutional Human Capital & Pension Risk Matrix

| Category | Key Metrics | Strategic Context & Objectives |

| Compensation | 12,435 Employees: 41.7 yrs average age, 17.1 yrs average tenure, $60,337 avg salary. | 10-Director compensation pool: $8.4M. 6 Internal Executives: $1.3M average ($7.8M total). Executive-to-employee ratio: 21.6x. |

| Pension Risk (AOCI) | PBO: $2,213.9M ($768.0M Domestic / $1,445.9M Overseas). Plan Assets: $1,983.5M. | $230.4M net deficit requires a $32.3M FY2027 contribution. AOCI impacts: Domestic net loss of $58.6M; Overseas net gain of $156.4M. |

| Diversity & Localization | Female Mgmt Ratio: 9.2%. Domestic Female/Male wage gap: 80.0%. | Targets (FY2028): 14.0% Female Mgmt; 17.0% Female regular employees; eNPS of 85. Overseas workforce: 70%. Global Officers: 16 of 47 stationed overseas (12 foreign nationals). |

Komatsu’s aggressive remanufacturing acquisitions and 100% immediate R&D expensing prove leadership is willing to sacrifice short-term optical margins to widen its digital and geographic moats, ensuring sustainable ROIC performance above WACC.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*