Idemitsu Kosan: 2026 Capex Realignment Near Chiba and Singapore as 48.2% Next-Gen Deployment Signals Structural Margin Expansion

Date : 2026-06-20

Reading : 125

HDIN Executive Takeaways

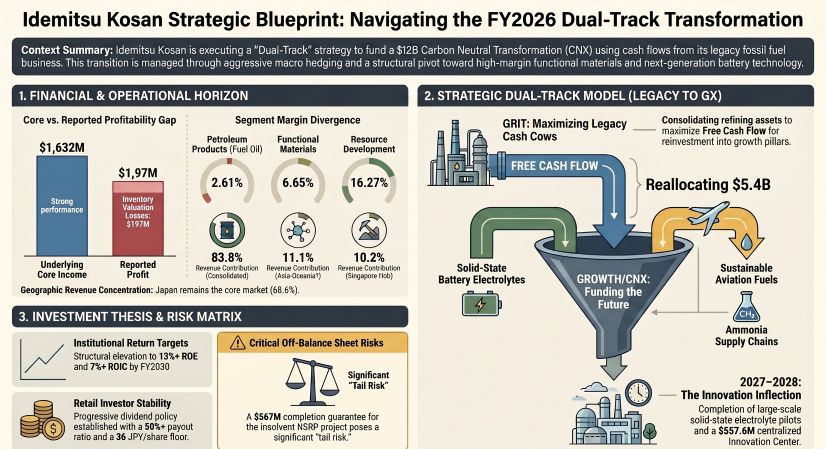

* Core operating income of $1,632 million eclipsed a -$197 million inventory valuation loss, while $2,624 million in operating cash flow funds a $12,034.6 million 2026-2030 Capex realignment.

* Japan holds 82.3% of tangible fixed assets, but strategic revenue growth relies on a $1,055 million Singapore hub and 92.49% consolidation of Fuji Oil to counter regional supply gluts.

* A 0.6x Net D/E ratio masks unrecorded underground pipeline retirement obligations and $567.0 million in completion guarantees for Vietnam's structurally insolvent NSRP megaproject.

Figure Idemitsu Kosan Strategic Blueprint: Navigating the FY2026 Dual-Track Transformation

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Idemitsu Kosan Co., Ltd. [TYO: 5019] relies on a highly concentrated downstream fuel apparatus to finance an aggressive transition toward functional materials and carbon-neutral (CNX) platforms. In FY2025/2026, the company recorded total consolidated revenue of $54,195.1 million (8,105.8 billion JPY), translated at a fiscal average exchange rate of 1 USD = 149.5686 JPY. While reported total segment income stood at $1,435 million (214.7 billion JPY), core segment income reached $1,632 million (244.1 billion JPY), explicitly excluding a -$197 million (-29.4 billion JPY) deemed inventory valuation loss. This time-lag deficit was triggered by Dubai crude oil prices dropping from an average of $81.3/bbl to $71.8/bbl.

The firm's macroeconomic sensitivity parameters expose structural volatility: a $1/bbl fluctuation in Dubai crude oil alters annual pre-tax profit by $53.5 million (8 billion JPY), and a 1 JPY fluctuation against the USD generates a $26.7 million (4 billion JPY) variance.

FY2025/2026 Segmental Profitability & Operating Leverage:

* Petroleum Products (Fuel Oil): Generated 83.8% of top-line volume at $45,420.1 million (6,793.4 billion JPY). The segment reported $1,187.9 million (177.6 billion JPY) in profit, registering a 2.61% margin. Stripping out inventory effects, core fuel income was $1,385 million (207.1 billion JPY). Total production value equaled $25,105.5 million (3,755.0 billion JPY).

* Basic Chemicals: Revenue of $3,285.2 million (491.3 billion JPY) yielded a segment loss of -$45.8 million (-6.8 billion JPY) at a -1.39% margin, compressed by oversupply from new chemical mega-plants in China.

* Functional Materials: Revenue of $3,364.1 million (503.1 billion JPY) produced $223.6 million (33.4 billion JPY) in profit at a 6.65% margin.

* Power & Renewable Energy: Revenue of $656.4 million (98.1 billion JPY) generated a narrowed segment loss of -$12.1 million (-1.8 billion JPY) at a -1.84% margin.

* Resource Development: Revenue of $1,360.6 million (203.5 billion JPY) yielded $221.3 million (33.1 billion JPY) in profit, recording the portfolio's highest margin at 16.27%, despite falling global coal prices.

Asset Valuations, Footnotes, and Execution Costs:

To enforce strict return thresholds, Idemitsu utilized discount rates ranging from 5.3% to 13.5% for impairment testing, booking a total of $121.0 million (18.1 billion JPY) in targeted asset write-downs.

* *Facility-Specific Impairments:* Tokuyama Biomass Power Plant: $80.7 million (12.07 billion JPY); Malaysian Petrochemical Plant: $23.3 million (3.49 billion JPY); Idle Kawasaki Refinery Site: $17.0 million (2.54 billion JPY).

* *Segmental Impairment Allocations:* Power & Renewables: $65.5 million (9,791 million JPY); Fuel Oil: $24.7 million (3,692 million JPY); Basic Chemicals: $5.8 million (871 million JPY).

The consolidated balance sheet carries Total Tangible Fixed Assets of $10,186.0 million (1,523,513 million JPY). Land assets revalued under the domestic Act on Revaluation of Land reflect a recognized difference of $911.9 million (136,390 million JPY) with a corresponding deferred tax liability of $635.6 million (95,058 million JPY). Intangible assets equal $1,739.7 million (260,199 million JPY), incorporating $867.7 million (129,776 million JPY) in Goodwill amortized over 5 to 20 years.

Infrastructure Layout and Regional Moats

Idemitsu maintains physical operations across a centralized domestic foundation while pivoting its trading architecture to Singapore. The company operates a network of approximately 6,000 domestic apollostation retail hubs. Midstream operations utilize direct refineries (Chiba, Aichi) alongside affiliated facilities (Showa Yokkaichi Sekiyu, Toa Oil, and Fuji Oil). During FY2023–FY2025, network refinery utilization stood at an inefficient 86%. To rectify this, management closed the obsolete Yamaguchi refinery (120,000 barrels/day) and secured a 92.49% voting stake in Fuji Oil. Integrating Fuji Oil with the Chiba complex is projected to yield $267.4 million (40 billion JPY) in pre-tax profit synergies by 2030, augmented by an additional $468.0 million (70 billion JPY) derived from AI-driven logistics and vessel allocations.

Table Geographic Revenue vs. Tangible Fixed Asset Base:

Note: Data reflects regional performance and asset distribution. Singapore asset values are represented by capital base rather than tangible fixed assets.

Reinvestment & Capital Expenditure Allocations:

Total CapEx reached $1,108 million (165.7 billion JPY) for the fiscal year.

* *Traditional Operations (51.8%):* Fuel Oil $391 million; Resources $103 million; Basic Chemicals $80 million.

* *Next-Generation & Renewables (48.2%):* Power & Renewable Energy $226 million; Functional Materials $54 million; Adjustments/Others $254 million.

To defend its maritime logistics perimeter against Hormuz Strait volatility, Idemitsu is executing the buildout of six Ammonia-ready, Methanol/LNG dual-fuel Very Large Crude Carriers (VLCCs) scheduled for deployment between 2026 and 2029.

R&D Structuring:

Total R&D expenditure amounted to $203.4 million (30,426 million JPY). Corporate and Unallocated projects commanded 51.3% ($104.3 million / 15.6 billion JPY) and Functional Materials absorbed 46.0% ($93.6 million / 14.0 billion JPY), strictly isolating legacy fossil fuels to a minimal 1.3% allocation ($2.7 million / 0.4 billion JPY), with Resources utilizing the remaining $3.3 million (0.5 billion JPY). The Lithium Battery Materials Department executed a Final Investment Decision (FID) in January 2026 for a large-scale solid-state electrolyte pilot plant, while a dedicated Innovation Center requires a $557.6 million ($558 million rounded / 83.4 billion JPY) outlay targeting March 2028 completion. Global OLED materials rely on proprietary manufacturing outputs from Paju, Korea, and lubricants scale via Karawang, Indonesia.

HDIN Institutional Verdict

Idemitsu’s reported FY2025 metrics—a Net D/E ratio of 0.6x and an Equity Ratio of 36.0%—project pristine financial discipline. Operating Cash Flow (OCF) of $2,624 million (392.4 billion JPY) effectively absorbs Investing Cash Outflows of -$1,950 million (-291.6 billion JPY) to produce a Free Cash Flow (FCF) surplus of $674 million (100.8 billion JPY). This facilitates a -$702 million (-104.9 billion JPY) financing cash outflow covering $668.6 million (100 billion JPY) in share repurchases and maintaining a total return ratio of 50%+ alongside a 36 JPY minimum baseline dividend.

However, forensic analysis of the financial footnotes identifies severe latent liabilities capable of threatening the $12,034.6 million (1.8 trillion JPY) 2026-2030 cumulative investment plan ($5,549 million / 830 billion JPY allocated to legacy GRIT; $5,415 million / 810 billion JPY to GROWTH/CNX).

* Off-Balance Sheet Encumbrances: The impending transition to IFRS in FY2026 will crystallize $176.9 million (26,459 million JPY) in unexpired non-cancelable operating leases ($47.5 million due within one year; $129.4 million due thereafter).

* Contingent Guarantees: Idemitsu acts as a guarantor for $567.0 million (84.8 billion JPY) covering the structurally insolvent Nghi Son Refinery and Petrochemical (NSRP) project in Vietnam. Additional guarantees include $123.9 million (18.52 billion JPY) for Valhall/Hod oil fields in Norway, $83.3 million (12.46 billion JPY) for a biomass fuel LLP, and $26.9 million (4.03 billion JPY) for Idemitsu Sarawak.

* Environmental Provisions: The balance sheet explicitly records an Asset Retirement Obligation (ARO) of $309.2 million (46,256 million JPY) discounted at 0.0% to 8.5%, alongside an escalating repair provision of $698.1 million (104.4 billion JPY) for aging infrastructure. Critically, management confirms the existence of wholly unrecorded AROs related to underground oil pipelines on third-party lands, representing an unquantifiable structural drag on future Free Cash Flow.

Management guidance for FY2026 structurally lowers expectations amid IFRS adoption, projecting Pre-tax Profit (excluding financial expenses) of $936.0 million (140.0 billion JPY) and Net Income of $601.7 million (90.0 billion JPY). The baseline inputs model Dubai crude dropping to $81.3/bbl after a Q1 spike, the USD/JPY rate at 151.3, and Australian thermal coal at $126.1/ton (up $20.7 from $105.4/ton).

To ensure aggressive execution, the 13-member board (featuring 5 independent directors and 29.4% female executive representation) and the 4-member audit board (2 independent) reformed executive compensation. Director remuneration relies on 50% fixed pay, 25% short-term bonus (0-200% variance), and 25% BIP Trust stock compensation explicitly tethered to capital efficiency (60% weight), GHG reductions (20%), and internal human capital metrics (20%). The firm targets a 13% ROE and 7% ROIC by 2030, a necessary escalation from the 10.6% ROE and 6.5% ROIC recorded in FY2025, culminating in a normalized pre-tax profit mandate of $2,406.9 million (360 billion JPY).

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Core operating income of $1,632 million eclipsed a -$197 million inventory valuation loss, while $2,624 million in operating cash flow funds a $12,034.6 million 2026-2030 Capex realignment.

* Japan holds 82.3% of tangible fixed assets, but strategic revenue growth relies on a $1,055 million Singapore hub and 92.49% consolidation of Fuji Oil to counter regional supply gluts.

* A 0.6x Net D/E ratio masks unrecorded underground pipeline retirement obligations and $567.0 million in completion guarantees for Vietnam's structurally insolvent NSRP megaproject.

Figure Idemitsu Kosan Strategic Blueprint: Navigating the FY2026 Dual-Track Transformation

Segmental Realities and Margin CompressionIdemitsu Kosan Co., Ltd. [TYO: 5019] relies on a highly concentrated downstream fuel apparatus to finance an aggressive transition toward functional materials and carbon-neutral (CNX) platforms. In FY2025/2026, the company recorded total consolidated revenue of $54,195.1 million (8,105.8 billion JPY), translated at a fiscal average exchange rate of 1 USD = 149.5686 JPY. While reported total segment income stood at $1,435 million (214.7 billion JPY), core segment income reached $1,632 million (244.1 billion JPY), explicitly excluding a -$197 million (-29.4 billion JPY) deemed inventory valuation loss. This time-lag deficit was triggered by Dubai crude oil prices dropping from an average of $81.3/bbl to $71.8/bbl.

The firm's macroeconomic sensitivity parameters expose structural volatility: a $1/bbl fluctuation in Dubai crude oil alters annual pre-tax profit by $53.5 million (8 billion JPY), and a 1 JPY fluctuation against the USD generates a $26.7 million (4 billion JPY) variance.

FY2025/2026 Segmental Profitability & Operating Leverage:

* Petroleum Products (Fuel Oil): Generated 83.8% of top-line volume at $45,420.1 million (6,793.4 billion JPY). The segment reported $1,187.9 million (177.6 billion JPY) in profit, registering a 2.61% margin. Stripping out inventory effects, core fuel income was $1,385 million (207.1 billion JPY). Total production value equaled $25,105.5 million (3,755.0 billion JPY).

* Basic Chemicals: Revenue of $3,285.2 million (491.3 billion JPY) yielded a segment loss of -$45.8 million (-6.8 billion JPY) at a -1.39% margin, compressed by oversupply from new chemical mega-plants in China.

* Functional Materials: Revenue of $3,364.1 million (503.1 billion JPY) produced $223.6 million (33.4 billion JPY) in profit at a 6.65% margin.

* Power & Renewable Energy: Revenue of $656.4 million (98.1 billion JPY) generated a narrowed segment loss of -$12.1 million (-1.8 billion JPY) at a -1.84% margin.

* Resource Development: Revenue of $1,360.6 million (203.5 billion JPY) yielded $221.3 million (33.1 billion JPY) in profit, recording the portfolio's highest margin at 16.27%, despite falling global coal prices.

Asset Valuations, Footnotes, and Execution Costs:

To enforce strict return thresholds, Idemitsu utilized discount rates ranging from 5.3% to 13.5% for impairment testing, booking a total of $121.0 million (18.1 billion JPY) in targeted asset write-downs.

* *Facility-Specific Impairments:* Tokuyama Biomass Power Plant: $80.7 million (12.07 billion JPY); Malaysian Petrochemical Plant: $23.3 million (3.49 billion JPY); Idle Kawasaki Refinery Site: $17.0 million (2.54 billion JPY).

* *Segmental Impairment Allocations:* Power & Renewables: $65.5 million (9,791 million JPY); Fuel Oil: $24.7 million (3,692 million JPY); Basic Chemicals: $5.8 million (871 million JPY).

The consolidated balance sheet carries Total Tangible Fixed Assets of $10,186.0 million (1,523,513 million JPY). Land assets revalued under the domestic Act on Revaluation of Land reflect a recognized difference of $911.9 million (136,390 million JPY) with a corresponding deferred tax liability of $635.6 million (95,058 million JPY). Intangible assets equal $1,739.7 million (260,199 million JPY), incorporating $867.7 million (129,776 million JPY) in Goodwill amortized over 5 to 20 years.

Infrastructure Layout and Regional Moats

Idemitsu maintains physical operations across a centralized domestic foundation while pivoting its trading architecture to Singapore. The company operates a network of approximately 6,000 domestic apollostation retail hubs. Midstream operations utilize direct refineries (Chiba, Aichi) alongside affiliated facilities (Showa Yokkaichi Sekiyu, Toa Oil, and Fuji Oil). During FY2023–FY2025, network refinery utilization stood at an inefficient 86%. To rectify this, management closed the obsolete Yamaguchi refinery (120,000 barrels/day) and secured a 92.49% voting stake in Fuji Oil. Integrating Fuji Oil with the Chiba complex is projected to yield $267.4 million (40 billion JPY) in pre-tax profit synergies by 2030, augmented by an additional $468.0 million (70 billion JPY) derived from AI-driven logistics and vessel allocations.

Table Geographic Revenue vs. Tangible Fixed Asset Base:

| Region | Revenue ($ Millions) | Revenue Share (%) | Fixed Assets ($ Millions) | Fixed Assets Share (%) | Strategic Notes |

| Japan | $37,155.2 | 68.6% | $8,388.4 | 82.3% | — |

| Singapore | $5,529.2 | 10.2% | N/A | N/A | Independent trading hub; Capital base: $1,055M (157.9B JPY) |

| Asia-Oceania | $5,994.7 | 11.1% | $875.0 | 8.6% | Australia coal mining; Manufacturing in Malaysia, Indonesia, China, and Taiwan, China |

| North America | $4,758.1 | 8.8% | $921.9 | 9.1% | Jeffersonville lubricant plants; Solar capabilities |

| Europe/Other | $757.9 | 1.4% | $0.7 | <0.1% | Upstream oil/gas exploration in Norway |

Reinvestment & Capital Expenditure Allocations:

Total CapEx reached $1,108 million (165.7 billion JPY) for the fiscal year.

* *Traditional Operations (51.8%):* Fuel Oil $391 million; Resources $103 million; Basic Chemicals $80 million.

* *Next-Generation & Renewables (48.2%):* Power & Renewable Energy $226 million; Functional Materials $54 million; Adjustments/Others $254 million.

To defend its maritime logistics perimeter against Hormuz Strait volatility, Idemitsu is executing the buildout of six Ammonia-ready, Methanol/LNG dual-fuel Very Large Crude Carriers (VLCCs) scheduled for deployment between 2026 and 2029.

R&D Structuring:

Total R&D expenditure amounted to $203.4 million (30,426 million JPY). Corporate and Unallocated projects commanded 51.3% ($104.3 million / 15.6 billion JPY) and Functional Materials absorbed 46.0% ($93.6 million / 14.0 billion JPY), strictly isolating legacy fossil fuels to a minimal 1.3% allocation ($2.7 million / 0.4 billion JPY), with Resources utilizing the remaining $3.3 million (0.5 billion JPY). The Lithium Battery Materials Department executed a Final Investment Decision (FID) in January 2026 for a large-scale solid-state electrolyte pilot plant, while a dedicated Innovation Center requires a $557.6 million ($558 million rounded / 83.4 billion JPY) outlay targeting March 2028 completion. Global OLED materials rely on proprietary manufacturing outputs from Paju, Korea, and lubricants scale via Karawang, Indonesia.

HDIN Institutional Verdict

Idemitsu’s reported FY2025 metrics—a Net D/E ratio of 0.6x and an Equity Ratio of 36.0%—project pristine financial discipline. Operating Cash Flow (OCF) of $2,624 million (392.4 billion JPY) effectively absorbs Investing Cash Outflows of -$1,950 million (-291.6 billion JPY) to produce a Free Cash Flow (FCF) surplus of $674 million (100.8 billion JPY). This facilitates a -$702 million (-104.9 billion JPY) financing cash outflow covering $668.6 million (100 billion JPY) in share repurchases and maintaining a total return ratio of 50%+ alongside a 36 JPY minimum baseline dividend.

However, forensic analysis of the financial footnotes identifies severe latent liabilities capable of threatening the $12,034.6 million (1.8 trillion JPY) 2026-2030 cumulative investment plan ($5,549 million / 830 billion JPY allocated to legacy GRIT; $5,415 million / 810 billion JPY to GROWTH/CNX).

* Off-Balance Sheet Encumbrances: The impending transition to IFRS in FY2026 will crystallize $176.9 million (26,459 million JPY) in unexpired non-cancelable operating leases ($47.5 million due within one year; $129.4 million due thereafter).

* Contingent Guarantees: Idemitsu acts as a guarantor for $567.0 million (84.8 billion JPY) covering the structurally insolvent Nghi Son Refinery and Petrochemical (NSRP) project in Vietnam. Additional guarantees include $123.9 million (18.52 billion JPY) for Valhall/Hod oil fields in Norway, $83.3 million (12.46 billion JPY) for a biomass fuel LLP, and $26.9 million (4.03 billion JPY) for Idemitsu Sarawak.

* Environmental Provisions: The balance sheet explicitly records an Asset Retirement Obligation (ARO) of $309.2 million (46,256 million JPY) discounted at 0.0% to 8.5%, alongside an escalating repair provision of $698.1 million (104.4 billion JPY) for aging infrastructure. Critically, management confirms the existence of wholly unrecorded AROs related to underground oil pipelines on third-party lands, representing an unquantifiable structural drag on future Free Cash Flow.

Management guidance for FY2026 structurally lowers expectations amid IFRS adoption, projecting Pre-tax Profit (excluding financial expenses) of $936.0 million (140.0 billion JPY) and Net Income of $601.7 million (90.0 billion JPY). The baseline inputs model Dubai crude dropping to $81.3/bbl after a Q1 spike, the USD/JPY rate at 151.3, and Australian thermal coal at $126.1/ton (up $20.7 from $105.4/ton).

To ensure aggressive execution, the 13-member board (featuring 5 independent directors and 29.4% female executive representation) and the 4-member audit board (2 independent) reformed executive compensation. Director remuneration relies on 50% fixed pay, 25% short-term bonus (0-200% variance), and 25% BIP Trust stock compensation explicitly tethered to capital efficiency (60% weight), GHG reductions (20%), and internal human capital metrics (20%). The firm targets a 13% ROE and 7% ROIC by 2030, a necessary escalation from the 10.6% ROE and 6.5% ROIC recorded in FY2025, culminating in a normalized pre-tax profit mandate of $2,406.9 million (360 billion JPY).

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."