Medtronic plc: Surgical Robotics and AI Realignment Near Global Facilities as $36.36 Billion Top-Line Signals European/Asian Adoption Shifts

Date : 2026-06-22

Reading : 320

HDIN Executive Takeaways

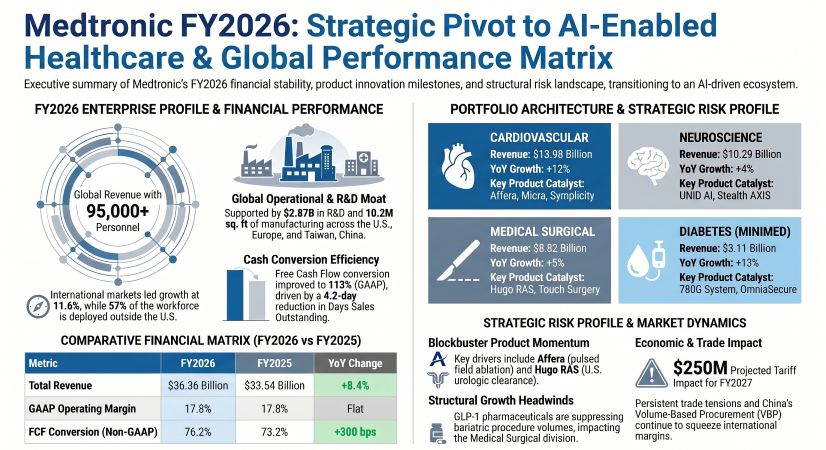

* Medtronic plc generated $36.36 billion (+8.4% YoY) driven by an 11.6% expansion in non-U.S. markets ($18.26 billion), yet absorbed a 30-basis-point gross margin compression due to a $185 million direct hit from global tariffs and a $238 million foreign exchange remeasurement loss.

* Operational realignment features a complex carve-out of the $3.11 billion Diabetes unit—retaining a 90.03% stake post-IPO—while navigating acute supply chain vulnerabilities at sole-source sterilization facilities across a 10.2 million square foot global manufacturing footprint.

* Institutional risk models must factor in unaccrued litigation exposures, including a $382 million antitrust verdict, escalating OECD Pillar Two tax friction driving a 21.2% effective tax rate, and systemic procedural volume pressures from GLP-1 pharmaceutical adoption in the surgical portfolio.

Figure Medtronic FY2026 Strategic Pivot to Al-Enabled Healthcare & Global Performance Matrix

Segmental Operations and Fiscal Realities

Segmental Operations and Fiscal Realities

Medtronic plc [NYSE: MDT] reported Fiscal Year 2026 total consolidated net sales of $36.36 billion, an 8.4% year-over-year increase from $33.54 billion in FY2025. GAAP Operating Profit expanded by 8.6% to $6.47 billion, while Non-GAAP Income Before Income Taxes reached $8.66 billion (+1.4% vs. $8.53 billion). However, GAAP Operating Margin remained flat at 17.8%, indicating severe cost pressures offsetting top-line momentum. GAAP Diluted EPS registered at $3.73 (+3.3% vs. $3.61), while Non-GAAP Diluted EPS settled at $5.53 (+0.7% vs. $5.49).

Cost of Products Sold (COGS) reached 35.0% of net sales ($12.72 billion), a 30-basis-point compression from 34.7% in FY2025. This was driven by a $185 million impact from duties and tariffs—projected to accelerate to $250 million in FY2027—alongside an $84 million December 2025 asset write-off tied to a terminated third-party manufacturing agreement within the Diabetes division. The company also absorbed a $238 million net loss related to currency remeasurement and hedging (compared to a $3 million loss in FY2025). Selling, general, and administrative (SG&A) expenses escalated to $11.8 billion, representing 32.4% of net sales.

Segmental Top-Line and Operating Profit Breakdown:

* Cardiovascular (CV): $13.98 billion net sales (+12% YoY); $3.67 billion Operating Profit. Non-U.S. CV revenues expanded 13% to $7.54 billion. The Cardiac Rhythm & Heart Failure division generated $7.50 billion (+17% YoY), anchored by the PulseSelect system, Micra VR and AV leadless pacemakers, and the Affera ablation portfolio. Coronary & Peripheral Vascular generated $2.66 billion (+5% YoY), driven by the Symplicity Spyral system.

* Neuroscience (NS): $10.29 billion net sales (+4% YoY); $3.06 billion Operating Profit.

* Medical Surgical (MS): $8.82 billion net sales (+5% YoY); $2.13 billion Operating Profit. The Surgical & Endoscopy division generated $6.76 billion (+4% YoY), supported by the Hugo Robotic-Assisted Surgery (RAS) system, despite traditional Advanced Stapling revenues declining due to the adoption of GLP-1 receptor agonists suppressing bariatric procedures.

* Diabetes (MiniMed) & "Other": $3.11 billion net sales (+13% YoY). Non-U.S. Diabetes revenues surged 19% to $2.18 billion. Operating profit for Diabetes is consolidated under the "Other" segment, which reported $106 million.

Capital allocation matched organic reinvestment against shareholder returns at a near 1:1 ratio. Management deployed $2.87 billion (7.9% of net sales) toward R&D and $1.90 billion toward Capital Expenditures (CapEx). Concurrently, the company distributed $3.64 billion in dividends and curtailed share repurchases to $1.04 billion (down from $3.24 billion in FY2025), preserving liquidity and leaving $1.2 billion remaining under a $5.0 billion authorization. The balance sheet marginally deleveraged as total debt decreased from $28.5 billion to $28.0 billion following the July 2025 retirement of €1.0 billion in Senior Notes.

The global tax architecture applied to $6.14 billion in pre-tax income ($5.39 billion foreign, $746 million domestic/Ireland) yielded a 21.2% Effective Tax Rate (ETR), an 870-basis-point deviation from Ireland’s 12.5% statutory baseline. The non-GAAP ETR was 17.3%. Upward pressures included U.S. intercompany IP transfers adding 4.5% ($278 million), Luxembourg affiliate financing adding 2.9% ($177 million), U.S. statutory differentials adding 1.7% ($105 million), state/local taxes adding 1.3% ($82 million), and net adjustments of $260 million (comprising a $150 million IP sale cost and a $70 million Diabetes separation cost). These were partially offset by a Luxembourg DTA release reducing the rate by 4.3% ($263 million), favorable differentials in Puerto Rico (-1.3%, $80 million) and Switzerland (-1.1%, $70 million), and U.S. R&D credits (-1.6%, $101 million). Tax holidays in Puerto Rico, Singapore, Costa Rica, the Dominican Republic, and China preserved $214 million in earnings, boosting EPS by $0.17.

Geographic Infrastructure and Supply Chain Architectures

Medtronic operates a 10.2 million square foot manufacturing and research footprint spanning the United States, Mexico, Puerto Rico, China, Ireland, the Dominican Republic, Switzerland, Italy, and France. Geographically, the U.S. market generated $18.10 billion (+5.4% YoY from $17.17 billion), dominated by CV ($6.44 billion) and NS ($6.88 billion) portfolios. International markets generated $18.26 billion (+11.6% YoY from $16.36 billion), outpacing U.S. expansion by a 2-to-1 ratio.

The physical supply chain remains highly exposed to single-point bottlenecks. Management identifies critical vulnerabilities stemming from sole-source suppliers for semiconductors, resins, palladium, and neon, alongside constrained third-party sterilization facilities. Tightening environmental regulations surrounding ethylene oxide (EtO) and polyfluoroalkyl substances (PFAS) mandate costly infrastructure retrofitting, directly impacting sterilization throughput.

To defend market share and counteract hospital procurement consolidation, the company utilizes a specialized direct-to-physician sales force to secure enterprise-level contracts, ensuring no single customer accounts for more than 10% of total net sales. Innovation cycles are shielded by a portfolio exceeding 38,000 patents. Product approvals include the Affera Sphere-9 catheter (U.S. FDA Oct. 2024), Sphere-360 (CE Mark Jan. 2026), OmniaSecure leads (CE Mark Mar. 2026), Hugo RAS urologic clearance (U.S. FDA Dec. 2025), LigaSure RAS (CE Mark Jul. 2025), and Symplicity Spyral (CMS NCD Oct. 2025). Additional growth is anchored by the Aurora EV-ICD and AI-driven platforms, including Touch Surgery Enterprise, GI Genius, UNiD, AiBLE, Stealth AXiS, AccuRhythm AI for Reveal LINQ/LINQ II, and BlueSync technologies.

Programmatic M&A aggressively restructured the portfolio in FY2026. Medtronic acquired the remaining 85% equity interest in CathWorks Ltd. in April 2026 for $525 million. On June 12, 2026, the company closed the acquisition of Scientia Vascular for $550 million upfront and up to $375 million in contingent consideration. In May 2026, management announced the $650 million acquisition of SPR Therapeutics, Inc., expected to close in the first half of FY2027 to expand the peripheral nerve stimulation pipeline.

Globally, the company employs 95,000 full-time personnel (43% U.S./Puerto Rico, 57% international), maintaining 100% pay equity for U.S. gender and ethnically diverse employees, and 99% global gender pay equity. Geopolitically, operations in sanctioned regions (Iran, Syria, Cuba, Crimea, Russia, Belarus) represent less than 1% of revenues. Under Section 13(r) disclosures, the company filed 11 notifications with Russia’s Federal Security Service (FSB) to permit medical device importation. Medtronic also manages operations in China, which accounts for 6% of total revenue and is exposed to volume-based procurement (VBP) pricing mandates.

Institutional Forensic Verdict

A forensic evaluation of the balance sheet indicates an optimized working capital profile offset by severe unaccrued legal liabilities and structurally complex deconsolidation mechanics. The Cash Conversion Cycle (CCC) improved by 4.3 days year-over-year. Days Sales Outstanding (DSO) compressed by 4.2 days to 66.68 days (based on $6.64 billion in AR). Days Payable Outstanding (DPO) tightened to 75.86 days (vs. 76.85 days), supported by an $84 million third-party supplier financing program against $2.64 billion in AP. Days Inventory Outstanding (DIO) remained elevated but stable at 170.75 days (based on $5.95 billion in inventory), reflecting a defensive posture against semiconductor and sterilization shortages. Operating Cash Flow grew to $7.33 billion (+$286 million YoY), yielding Free Cash Flow of $5.43 billion. FCF Conversion expanded to 113.0% on GAAP Net Income (+180 bps) and 76.2% on Non-GAAP Net Income (+300 bps).

The March 9, 2026 IPO of MiniMed Group, Inc. raised $538 million in net proceeds. Because Medtronic retained 252,813,348 shares (a 90.03% controlling interest), the $3.11 billion unit remains fully consolidated. A $381 million Non-Controlling Interest (NCI) liability was recorded, generating a $157 million premium recognized as an increase to Additional Paid-in Capital (APIC). Medtronic incurred a $157 million charge in Other operating expense for a future Blackstone royalty obligation triggered by a funded Diabetes product approval. The company targets $300 million to $500 million in restructuring charges through FY2029 to complete the divestment and resolve post-separation administrative drag.

Medtronic maintains $42.59 billion in goodwill with zero recognized impairment charges, though management notes MiniMed's post-IPO stock decline poses a future impairment risk. The tax profile carries a $12.34 billion valuation allowance against $17.55 billion in gross Deferred Tax Assets (comprising $11.08 billion in NOLs/credits, $2.98 billion in intangibles, and $1.34 billion in R&D). This allowance applies to $3.9 billion in NOLs from an FY2008 tax ruling and $5.0 billion from an FY2023 reorganization. Deferred Tax Liabilities stand at $1.83 billion ($1.13 billion intangibles, $178 million leases). Liquidity is permanently reinvested offshore, totaling $9.22 billion ($1.95 billion cash, $7.27 billion short-term investments).

Litigation liabilities are aggressively provisioned yet severely exposed. Accrued litigation liabilities fell from $0.4 billion to $0.2 billion by April 24, 2026, with FY2026 recording $113 million in net charges. Historical liabilities include $52 million in non-GAAP adjustments for EU MDR compliance duplication. However, the company holds zero accrual for a $382 million antitrust jury verdict awarded to Applied Medical Resources Corporation on February 5, 2026. Separately, Medtronic carries $2.017 billion in gross unrecognized tax benefits tied to an IRS Puerto Rico dispute remanded in September 2025. Product liability torts include over 10,350 hernia mesh plaintiffs in Massachusetts and Minnesota, and 15 lawsuits on behalf of 55 individuals regarding Series 600 insulin pumps. A $106 million IP verdict to Colibri Heart Valve LLC was successfully vacated in July 2025.

International revenue predictability is threatened by retroactive clawbacks. In FY2025, Italy's payback mechanism forced a $90 million net sales reduction; in FY2026, legislative revisions provided a $39 million benefit. Additionally, an April 24, 2026, unauthorized third-party IT breach exposed data vulnerabilities, with patient notifications expected in Q1 FY27, compounding risks tied to legacy environmental mandates regarding Orrington, Maine solvent contamination and a 2022 Penobscot River/Bay mercury settlement. The firm targets net-zero operational emissions by 2030 and total carbon neutrality by 2045.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Medtronic plc generated $36.36 billion (+8.4% YoY) driven by an 11.6% expansion in non-U.S. markets ($18.26 billion), yet absorbed a 30-basis-point gross margin compression due to a $185 million direct hit from global tariffs and a $238 million foreign exchange remeasurement loss.

* Operational realignment features a complex carve-out of the $3.11 billion Diabetes unit—retaining a 90.03% stake post-IPO—while navigating acute supply chain vulnerabilities at sole-source sterilization facilities across a 10.2 million square foot global manufacturing footprint.

* Institutional risk models must factor in unaccrued litigation exposures, including a $382 million antitrust verdict, escalating OECD Pillar Two tax friction driving a 21.2% effective tax rate, and systemic procedural volume pressures from GLP-1 pharmaceutical adoption in the surgical portfolio.

Figure Medtronic FY2026 Strategic Pivot to Al-Enabled Healthcare & Global Performance Matrix

Segmental Operations and Fiscal RealitiesMedtronic plc [NYSE: MDT] reported Fiscal Year 2026 total consolidated net sales of $36.36 billion, an 8.4% year-over-year increase from $33.54 billion in FY2025. GAAP Operating Profit expanded by 8.6% to $6.47 billion, while Non-GAAP Income Before Income Taxes reached $8.66 billion (+1.4% vs. $8.53 billion). However, GAAP Operating Margin remained flat at 17.8%, indicating severe cost pressures offsetting top-line momentum. GAAP Diluted EPS registered at $3.73 (+3.3% vs. $3.61), while Non-GAAP Diluted EPS settled at $5.53 (+0.7% vs. $5.49).

Cost of Products Sold (COGS) reached 35.0% of net sales ($12.72 billion), a 30-basis-point compression from 34.7% in FY2025. This was driven by a $185 million impact from duties and tariffs—projected to accelerate to $250 million in FY2027—alongside an $84 million December 2025 asset write-off tied to a terminated third-party manufacturing agreement within the Diabetes division. The company also absorbed a $238 million net loss related to currency remeasurement and hedging (compared to a $3 million loss in FY2025). Selling, general, and administrative (SG&A) expenses escalated to $11.8 billion, representing 32.4% of net sales.

Segmental Top-Line and Operating Profit Breakdown:

* Cardiovascular (CV): $13.98 billion net sales (+12% YoY); $3.67 billion Operating Profit. Non-U.S. CV revenues expanded 13% to $7.54 billion. The Cardiac Rhythm & Heart Failure division generated $7.50 billion (+17% YoY), anchored by the PulseSelect system, Micra VR and AV leadless pacemakers, and the Affera ablation portfolio. Coronary & Peripheral Vascular generated $2.66 billion (+5% YoY), driven by the Symplicity Spyral system.

* Neuroscience (NS): $10.29 billion net sales (+4% YoY); $3.06 billion Operating Profit.

* Medical Surgical (MS): $8.82 billion net sales (+5% YoY); $2.13 billion Operating Profit. The Surgical & Endoscopy division generated $6.76 billion (+4% YoY), supported by the Hugo Robotic-Assisted Surgery (RAS) system, despite traditional Advanced Stapling revenues declining due to the adoption of GLP-1 receptor agonists suppressing bariatric procedures.

* Diabetes (MiniMed) & "Other": $3.11 billion net sales (+13% YoY). Non-U.S. Diabetes revenues surged 19% to $2.18 billion. Operating profit for Diabetes is consolidated under the "Other" segment, which reported $106 million.

Capital allocation matched organic reinvestment against shareholder returns at a near 1:1 ratio. Management deployed $2.87 billion (7.9% of net sales) toward R&D and $1.90 billion toward Capital Expenditures (CapEx). Concurrently, the company distributed $3.64 billion in dividends and curtailed share repurchases to $1.04 billion (down from $3.24 billion in FY2025), preserving liquidity and leaving $1.2 billion remaining under a $5.0 billion authorization. The balance sheet marginally deleveraged as total debt decreased from $28.5 billion to $28.0 billion following the July 2025 retirement of €1.0 billion in Senior Notes.

The global tax architecture applied to $6.14 billion in pre-tax income ($5.39 billion foreign, $746 million domestic/Ireland) yielded a 21.2% Effective Tax Rate (ETR), an 870-basis-point deviation from Ireland’s 12.5% statutory baseline. The non-GAAP ETR was 17.3%. Upward pressures included U.S. intercompany IP transfers adding 4.5% ($278 million), Luxembourg affiliate financing adding 2.9% ($177 million), U.S. statutory differentials adding 1.7% ($105 million), state/local taxes adding 1.3% ($82 million), and net adjustments of $260 million (comprising a $150 million IP sale cost and a $70 million Diabetes separation cost). These were partially offset by a Luxembourg DTA release reducing the rate by 4.3% ($263 million), favorable differentials in Puerto Rico (-1.3%, $80 million) and Switzerland (-1.1%, $70 million), and U.S. R&D credits (-1.6%, $101 million). Tax holidays in Puerto Rico, Singapore, Costa Rica, the Dominican Republic, and China preserved $214 million in earnings, boosting EPS by $0.17.

Geographic Infrastructure and Supply Chain Architectures

Medtronic operates a 10.2 million square foot manufacturing and research footprint spanning the United States, Mexico, Puerto Rico, China, Ireland, the Dominican Republic, Switzerland, Italy, and France. Geographically, the U.S. market generated $18.10 billion (+5.4% YoY from $17.17 billion), dominated by CV ($6.44 billion) and NS ($6.88 billion) portfolios. International markets generated $18.26 billion (+11.6% YoY from $16.36 billion), outpacing U.S. expansion by a 2-to-1 ratio.

The physical supply chain remains highly exposed to single-point bottlenecks. Management identifies critical vulnerabilities stemming from sole-source suppliers for semiconductors, resins, palladium, and neon, alongside constrained third-party sterilization facilities. Tightening environmental regulations surrounding ethylene oxide (EtO) and polyfluoroalkyl substances (PFAS) mandate costly infrastructure retrofitting, directly impacting sterilization throughput.

To defend market share and counteract hospital procurement consolidation, the company utilizes a specialized direct-to-physician sales force to secure enterprise-level contracts, ensuring no single customer accounts for more than 10% of total net sales. Innovation cycles are shielded by a portfolio exceeding 38,000 patents. Product approvals include the Affera Sphere-9 catheter (U.S. FDA Oct. 2024), Sphere-360 (CE Mark Jan. 2026), OmniaSecure leads (CE Mark Mar. 2026), Hugo RAS urologic clearance (U.S. FDA Dec. 2025), LigaSure RAS (CE Mark Jul. 2025), and Symplicity Spyral (CMS NCD Oct. 2025). Additional growth is anchored by the Aurora EV-ICD and AI-driven platforms, including Touch Surgery Enterprise, GI Genius, UNiD, AiBLE, Stealth AXiS, AccuRhythm AI for Reveal LINQ/LINQ II, and BlueSync technologies.

Programmatic M&A aggressively restructured the portfolio in FY2026. Medtronic acquired the remaining 85% equity interest in CathWorks Ltd. in April 2026 for $525 million. On June 12, 2026, the company closed the acquisition of Scientia Vascular for $550 million upfront and up to $375 million in contingent consideration. In May 2026, management announced the $650 million acquisition of SPR Therapeutics, Inc., expected to close in the first half of FY2027 to expand the peripheral nerve stimulation pipeline.

Globally, the company employs 95,000 full-time personnel (43% U.S./Puerto Rico, 57% international), maintaining 100% pay equity for U.S. gender and ethnically diverse employees, and 99% global gender pay equity. Geopolitically, operations in sanctioned regions (Iran, Syria, Cuba, Crimea, Russia, Belarus) represent less than 1% of revenues. Under Section 13(r) disclosures, the company filed 11 notifications with Russia’s Federal Security Service (FSB) to permit medical device importation. Medtronic also manages operations in China, which accounts for 6% of total revenue and is exposed to volume-based procurement (VBP) pricing mandates.

Institutional Forensic Verdict

A forensic evaluation of the balance sheet indicates an optimized working capital profile offset by severe unaccrued legal liabilities and structurally complex deconsolidation mechanics. The Cash Conversion Cycle (CCC) improved by 4.3 days year-over-year. Days Sales Outstanding (DSO) compressed by 4.2 days to 66.68 days (based on $6.64 billion in AR). Days Payable Outstanding (DPO) tightened to 75.86 days (vs. 76.85 days), supported by an $84 million third-party supplier financing program against $2.64 billion in AP. Days Inventory Outstanding (DIO) remained elevated but stable at 170.75 days (based on $5.95 billion in inventory), reflecting a defensive posture against semiconductor and sterilization shortages. Operating Cash Flow grew to $7.33 billion (+$286 million YoY), yielding Free Cash Flow of $5.43 billion. FCF Conversion expanded to 113.0% on GAAP Net Income (+180 bps) and 76.2% on Non-GAAP Net Income (+300 bps).

The March 9, 2026 IPO of MiniMed Group, Inc. raised $538 million in net proceeds. Because Medtronic retained 252,813,348 shares (a 90.03% controlling interest), the $3.11 billion unit remains fully consolidated. A $381 million Non-Controlling Interest (NCI) liability was recorded, generating a $157 million premium recognized as an increase to Additional Paid-in Capital (APIC). Medtronic incurred a $157 million charge in Other operating expense for a future Blackstone royalty obligation triggered by a funded Diabetes product approval. The company targets $300 million to $500 million in restructuring charges through FY2029 to complete the divestment and resolve post-separation administrative drag.

Medtronic maintains $42.59 billion in goodwill with zero recognized impairment charges, though management notes MiniMed's post-IPO stock decline poses a future impairment risk. The tax profile carries a $12.34 billion valuation allowance against $17.55 billion in gross Deferred Tax Assets (comprising $11.08 billion in NOLs/credits, $2.98 billion in intangibles, and $1.34 billion in R&D). This allowance applies to $3.9 billion in NOLs from an FY2008 tax ruling and $5.0 billion from an FY2023 reorganization. Deferred Tax Liabilities stand at $1.83 billion ($1.13 billion intangibles, $178 million leases). Liquidity is permanently reinvested offshore, totaling $9.22 billion ($1.95 billion cash, $7.27 billion short-term investments).

Litigation liabilities are aggressively provisioned yet severely exposed. Accrued litigation liabilities fell from $0.4 billion to $0.2 billion by April 24, 2026, with FY2026 recording $113 million in net charges. Historical liabilities include $52 million in non-GAAP adjustments for EU MDR compliance duplication. However, the company holds zero accrual for a $382 million antitrust jury verdict awarded to Applied Medical Resources Corporation on February 5, 2026. Separately, Medtronic carries $2.017 billion in gross unrecognized tax benefits tied to an IRS Puerto Rico dispute remanded in September 2025. Product liability torts include over 10,350 hernia mesh plaintiffs in Massachusetts and Minnesota, and 15 lawsuits on behalf of 55 individuals regarding Series 600 insulin pumps. A $106 million IP verdict to Colibri Heart Valve LLC was successfully vacated in July 2025.

International revenue predictability is threatened by retroactive clawbacks. In FY2025, Italy's payback mechanism forced a $90 million net sales reduction; in FY2026, legislative revisions provided a $39 million benefit. Additionally, an April 24, 2026, unauthorized third-party IT breach exposed data vulnerabilities, with patient notifications expected in Q1 FY27, compounding risks tied to legacy environmental mandates regarding Orrington, Maine solvent contamination and a 2022 Penobscot River/Bay mercury settlement. The firm targets net-zero operational emissions by 2030 and total carbon neutrality by 2045.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."