QD Laser, Inc.: Semiconductor Optics B2B Pivot Near Tokyo as 54.5% Backlog Expansion Signals Structural Margin Recovery

Date : 2026-06-22

Reading : 133

HDIN Executive Takeaways

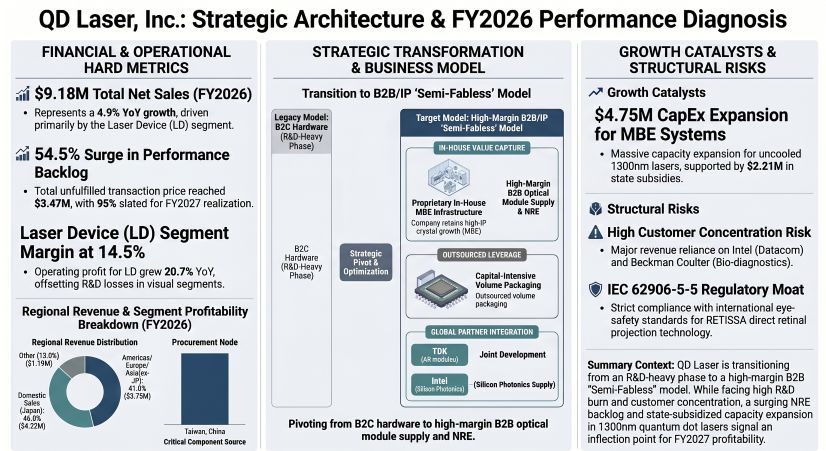

* Operating cash burn narrowed by 5.1% YoY to an outflow of $3.22M, while high-margin 1300nm quantum dot integrations pushed total net sales up 4.9% to $9.18M.

* A rigid "Semi-Fabless" architecture relies on elite supply dependencies, heavily weighting $1.07M in historical volume packaging to Thailand's Fabrinet Co., Ltd., and generating upstream bottlenecks with Taiwan, China’s Elite Advanced Laser Corporation.

* Consumer hardware inventory risks have been isolated via a strategic B2B module pivot; Non-Recurring Engineering (NRE) backlog expanded by 54.5% to $3.47M, with 95% slated for conversion within a 12-month execution window.

Figure QD Laser Inc: Strategic Architecture & FY2026 Performance Diagnosis

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

QD Laser, Inc. [TSE: 6613] operates a bifurcated revenue architecture, subsidizing intensive biomedical and commercial optics R&D with a highly generative deep-tech laser component baseline. According to FY2025 to FY2026 data—translated at a strict peg of 1 USD = 149.5686 JPY—the total enterprise top-line expanded by 4.9%, growing from $8.75M (1,308,870 thousand JPY) to $9.18M (1,372,801 thousand JPY). This absorption of volume directly impacted the bottom line, narrowing the overall Operating Loss by 26.8%, improving from a deficit of $2.98M (445,689 thousand JPY) to a deficit of $2.18M (326,213 thousand JPY).

Table Enterprise Profit & Loss Metrics (FY2025 vs FY2026)

Corporate disclosures note internal reporting variations across operational subsets. The primary Laser Device (LD) segment recorded sales growth of 4.7%, moving from $7.49M (1,120,719 thousand JPY) to $7.84M (1,173,248 thousand JPY), driving a 20.7% operating profit expansion from $0.94M (141,249 thousand JPY) to $1.14M (170,502 thousand JPY). Margins here improved from 12.6% to 14.5% (an addition of 190 basis points). Alternative subset metrics tracking discrete component revenues recorded LD sales expanding 12.8% to $5.31M (794,485 thousand JPY). Within this LD matrix, Distributed Feedback (DFB) lasers generated $3.31M (495,741 thousand JPY), while Quantum Dot and High-Power units added $4.53M (677,506 thousand JPY). Key outputs include 400mW 1064nm DFB lasers for flow cytometry and 15ps short-pulse 1030nm/1064nm lasers for LiDAR precision machining.

Conversely, the emerging Laser & Optical Solutions (L&OS / VID) segment, housing the proprietary VISIRIUM focus-free direct retinal projection technology, grew sales by 6.1% from $1.26M (188,151 thousand JPY) to $1.33M (199,552 thousand JPY), with RETISSA eyewear and optical units capturing the entirety of this $1.33M (198,603 thousand JPY). Alternative structural segment accounting priced L&OS sales at $3.87M (578,315 thousand JPY), a 4.3% YoY contraction. Despite internal metric variations, the L&OS operating deficit structurally narrowed by 11.7%, from a loss of $2.08M (311,751 thousand JPY) to a loss of $1.84M (275,187 thousand JPY), translating to an operating margin improvement from -165.7% to -137.9%.

Forward revenue visibility is governed by a massive shift in deferred commitments. The total outstanding backlog expanded by 54.5%, representing a $1.22M injection, moving from $2.25M (335,922 thousand JPY) in FY2025 to $3.47M (518,949 thousand JPY) in FY2026. Structurally, $3.30M (492,901 thousand JPY) of this backlog is mandated for execution within one year, with only $0.17M (26,048 thousand JPY) booked beyond 12 months.

Infrastructure Layout and Regional Moats

QD Laser, Inc. operates an internationally dispersed revenue and supply matrix, strategically balancing domestic intellectual property retention against offshore packaging. Geographically, FY2026 external net sales were allocated as follows: Japan at 46.0% capturing $4.22M (631,541 thousand JPY), the Americas at 15.2% capturing $1.39M (208,316 thousand JPY), Europe at 13.2% capturing $1.21M (180,777 thousand JPY), Asia (excluding Japan) at 12.6% capturing $1.15M (172,674 thousand JPY), and Other Regions holding the remaining 13.0% at $1.20M (179,490 thousand JPY).

Production architectures utilize a "Semi-Fabless" protocol. Core molecular beam epitaxy (MBE) crystal growth on Gallium Arsenide (GaAs) substrates and strict in-house proprietary chip inspections occur within domestic Japanese Industrial Clean Rooms (ICR) and Biological Clean Rooms (BCR). Operations are bolstered by ISO9001 certifications and compliance with the IEC 62906-5-5:2022 international laser eye safety standard. Off-balance-sheet downstream functions—including diffraction grating formation, clad regrowth, electrode processing, and facet coating—are externalized. Crucially, global volume assembly remains heavily dependent on Thailand's Fabrinet Co., Ltd., which historically commanded $1.07M (160,723 thousand JPY), or 12.28% of total net sales. Upstream optical components are strictly procured via Elite Advanced Laser Corporation in Taiwan, China, carrying an accounts payable transactional weight of $0.74M (111,351 thousand JPY).

This deep-tech layout is currently enduring a heavy capital expenditure (CapEx) cycle. Total planned equipment CapEx targeted $4.75M (710,000 thousand JPY). However, the enterprise artificially compressed this true net cash burn down to $2.54M (380,000 thousand JPY) by securing $2.21M (330,000 thousand JPY) in non-dilutive state financing via the SME Growth Acceleration Subsidy. A forensic audit of the CapEx ledger isolates a $2.55M (381,157 thousand JPY) dedicated capital deployment strictly for procuring next-generation MBE cleanroom equipment. Accommodating this hardware mandated a physical headquarters relocation on October 16, 2025. This maneuver triggered a $0.34M (50,977 thousand JPY) non-cash fixed asset impairment loss, while lease restructuring released working capital as guarantee deposits fell from $0.40M (59,615 thousand JPY) to $0.30M (45,609 thousand JPY).

Human capital is highly specialized but demographic-heavy. The firm retains 50 full-time and 10 temporary/contract personnel across the LD segment (23), L&OS segment (16), and corporate administration (11). The workforce carries an average age of 51.08 years, an average tenure of 7.72 years, and an average annual compensation of $55,541 (8,307,267 JPY). Retention is engineered via 10th, 11th, and 13th series stock options and structured "1on1" personnel interventions. Corporate governance separates operations via 4 Executive Officers reporting to the Representative Director, supervised by a 6-member Board of Directors (where 3 members populate the Audit and Supervisory Committee), augmented by Remuneration and Nomination Advisory Committees.

HDIN Institutional Verdict

QD Laser, Inc. is executing a textbook mid-cycle IP monetization strategy, attempting to decouple high-margin quantum dot intellectual property from the fixed overhead of physical B2C consumer distribution. The enterprise is socializing early-stage research by leveraging state-backed institutions, explicitly utilizing the Industrial Technology Research Institute (ITRI) in Taiwan, China, to fund 1030nm DFB laser scaling.

Corporate R&D outlays expanded by 8.1% to $1.26M (187,813 thousand JPY). Forensic allocation reveals a structural pivot: 55.5% of this budget, totaling $0.70M (104,304 thousand JPY), was aggressively deployed into the L&OS segment to co-develop miniaturized RGB optical modules under a Joint Development Agreement (JDA) with TDK Corporation. The remaining 44.5%, or $0.56M (83,508 thousand JPY), funded LD deep-tech hardware. By granting TDK exclusive general consumer manufacturing rights for Augmented Reality (AR) smart glasses, QD Laser isolates itself from retail inventory valuation risks while aggressively pushing its strictly-retained medical IP into clinical pipelines, proven by the October 2025 launch of the RETISSA MEOCHECK NEO, following the RETISSA ON HAND (2023/2024) and Lantana systems (2024).

The immediate existential threat is client revenue concentration. The silicon photonics pipeline is chained to Intel Corporation, generating $0.72M (107,857 thousand JPY) in accounts receivable at FY2026 close, while diagnostic integration historically relied on Beckman Coulter, Inc., accounting for 12.73% ($1.11M / 166,665 thousand JPY) of FY2025 sales. Despite issuing a revised earnings forecast on December 19, 2025, and marking its 20th fiscal period (established April 2006) without net profitability, the strategic CapEx offset via the $2.21M state subsidy provides absolute mechanical validation that management is successfully defending the balance sheet. If the $3.30M short-term NRE backlog converts without supplier disruption in Taiwan, China, or Thailand, the enterprise target of 15% EBITDA margins by FY2027 remains mathematically viable.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating cash burn narrowed by 5.1% YoY to an outflow of $3.22M, while high-margin 1300nm quantum dot integrations pushed total net sales up 4.9% to $9.18M.

* A rigid "Semi-Fabless" architecture relies on elite supply dependencies, heavily weighting $1.07M in historical volume packaging to Thailand's Fabrinet Co., Ltd., and generating upstream bottlenecks with Taiwan, China’s Elite Advanced Laser Corporation.

* Consumer hardware inventory risks have been isolated via a strategic B2B module pivot; Non-Recurring Engineering (NRE) backlog expanded by 54.5% to $3.47M, with 95% slated for conversion within a 12-month execution window.

Figure QD Laser Inc: Strategic Architecture & FY2026 Performance Diagnosis

Segmental Realities and Margin CompressionQD Laser, Inc. [TSE: 6613] operates a bifurcated revenue architecture, subsidizing intensive biomedical and commercial optics R&D with a highly generative deep-tech laser component baseline. According to FY2025 to FY2026 data—translated at a strict peg of 1 USD = 149.5686 JPY—the total enterprise top-line expanded by 4.9%, growing from $8.75M (1,308,870 thousand JPY) to $9.18M (1,372,801 thousand JPY). This absorption of volume directly impacted the bottom line, narrowing the overall Operating Loss by 26.8%, improving from a deficit of $2.98M (445,689 thousand JPY) to a deficit of $2.18M (326,213 thousand JPY).

Table Enterprise Profit & Loss Metrics (FY2025 vs FY2026)

| Metric | FY2025 ($M) | FY2025 (JPY '000) | FY2026 ($M) | FY2026 (JPY '000) | Trend |

| Ordinary Loss | 2.97 | 443,547 | 2.04 | 305,758 | Narrowed 31.1% |

| Net Loss | 2.98 | 445,768 | 2.39 | 357,147 | Narrowed 19.9% |

| CFO | 3.39 | 506,823 | 3.22 | 481,077 | Outflow narrowed 5.1% |

| CFI | 3.80 | 568,605 | 5.93 | 886,682 | Outflow expanded 55.9% |

| CFF | 0.06 | 9,512 | 2.38 | 355,712 | Grew |

| Ending Cash | 18.33 | 2,741,356 | 18.33 | 2,741,356 | Stable |

Corporate disclosures note internal reporting variations across operational subsets. The primary Laser Device (LD) segment recorded sales growth of 4.7%, moving from $7.49M (1,120,719 thousand JPY) to $7.84M (1,173,248 thousand JPY), driving a 20.7% operating profit expansion from $0.94M (141,249 thousand JPY) to $1.14M (170,502 thousand JPY). Margins here improved from 12.6% to 14.5% (an addition of 190 basis points). Alternative subset metrics tracking discrete component revenues recorded LD sales expanding 12.8% to $5.31M (794,485 thousand JPY). Within this LD matrix, Distributed Feedback (DFB) lasers generated $3.31M (495,741 thousand JPY), while Quantum Dot and High-Power units added $4.53M (677,506 thousand JPY). Key outputs include 400mW 1064nm DFB lasers for flow cytometry and 15ps short-pulse 1030nm/1064nm lasers for LiDAR precision machining.

Conversely, the emerging Laser & Optical Solutions (L&OS / VID) segment, housing the proprietary VISIRIUM focus-free direct retinal projection technology, grew sales by 6.1% from $1.26M (188,151 thousand JPY) to $1.33M (199,552 thousand JPY), with RETISSA eyewear and optical units capturing the entirety of this $1.33M (198,603 thousand JPY). Alternative structural segment accounting priced L&OS sales at $3.87M (578,315 thousand JPY), a 4.3% YoY contraction. Despite internal metric variations, the L&OS operating deficit structurally narrowed by 11.7%, from a loss of $2.08M (311,751 thousand JPY) to a loss of $1.84M (275,187 thousand JPY), translating to an operating margin improvement from -165.7% to -137.9%.

Forward revenue visibility is governed by a massive shift in deferred commitments. The total outstanding backlog expanded by 54.5%, representing a $1.22M injection, moving from $2.25M (335,922 thousand JPY) in FY2025 to $3.47M (518,949 thousand JPY) in FY2026. Structurally, $3.30M (492,901 thousand JPY) of this backlog is mandated for execution within one year, with only $0.17M (26,048 thousand JPY) booked beyond 12 months.

Infrastructure Layout and Regional Moats

QD Laser, Inc. operates an internationally dispersed revenue and supply matrix, strategically balancing domestic intellectual property retention against offshore packaging. Geographically, FY2026 external net sales were allocated as follows: Japan at 46.0% capturing $4.22M (631,541 thousand JPY), the Americas at 15.2% capturing $1.39M (208,316 thousand JPY), Europe at 13.2% capturing $1.21M (180,777 thousand JPY), Asia (excluding Japan) at 12.6% capturing $1.15M (172,674 thousand JPY), and Other Regions holding the remaining 13.0% at $1.20M (179,490 thousand JPY).

Production architectures utilize a "Semi-Fabless" protocol. Core molecular beam epitaxy (MBE) crystal growth on Gallium Arsenide (GaAs) substrates and strict in-house proprietary chip inspections occur within domestic Japanese Industrial Clean Rooms (ICR) and Biological Clean Rooms (BCR). Operations are bolstered by ISO9001 certifications and compliance with the IEC 62906-5-5:2022 international laser eye safety standard. Off-balance-sheet downstream functions—including diffraction grating formation, clad regrowth, electrode processing, and facet coating—are externalized. Crucially, global volume assembly remains heavily dependent on Thailand's Fabrinet Co., Ltd., which historically commanded $1.07M (160,723 thousand JPY), or 12.28% of total net sales. Upstream optical components are strictly procured via Elite Advanced Laser Corporation in Taiwan, China, carrying an accounts payable transactional weight of $0.74M (111,351 thousand JPY).

This deep-tech layout is currently enduring a heavy capital expenditure (CapEx) cycle. Total planned equipment CapEx targeted $4.75M (710,000 thousand JPY). However, the enterprise artificially compressed this true net cash burn down to $2.54M (380,000 thousand JPY) by securing $2.21M (330,000 thousand JPY) in non-dilutive state financing via the SME Growth Acceleration Subsidy. A forensic audit of the CapEx ledger isolates a $2.55M (381,157 thousand JPY) dedicated capital deployment strictly for procuring next-generation MBE cleanroom equipment. Accommodating this hardware mandated a physical headquarters relocation on October 16, 2025. This maneuver triggered a $0.34M (50,977 thousand JPY) non-cash fixed asset impairment loss, while lease restructuring released working capital as guarantee deposits fell from $0.40M (59,615 thousand JPY) to $0.30M (45,609 thousand JPY).

Human capital is highly specialized but demographic-heavy. The firm retains 50 full-time and 10 temporary/contract personnel across the LD segment (23), L&OS segment (16), and corporate administration (11). The workforce carries an average age of 51.08 years, an average tenure of 7.72 years, and an average annual compensation of $55,541 (8,307,267 JPY). Retention is engineered via 10th, 11th, and 13th series stock options and structured "1on1" personnel interventions. Corporate governance separates operations via 4 Executive Officers reporting to the Representative Director, supervised by a 6-member Board of Directors (where 3 members populate the Audit and Supervisory Committee), augmented by Remuneration and Nomination Advisory Committees.

HDIN Institutional Verdict

QD Laser, Inc. is executing a textbook mid-cycle IP monetization strategy, attempting to decouple high-margin quantum dot intellectual property from the fixed overhead of physical B2C consumer distribution. The enterprise is socializing early-stage research by leveraging state-backed institutions, explicitly utilizing the Industrial Technology Research Institute (ITRI) in Taiwan, China, to fund 1030nm DFB laser scaling.

Corporate R&D outlays expanded by 8.1% to $1.26M (187,813 thousand JPY). Forensic allocation reveals a structural pivot: 55.5% of this budget, totaling $0.70M (104,304 thousand JPY), was aggressively deployed into the L&OS segment to co-develop miniaturized RGB optical modules under a Joint Development Agreement (JDA) with TDK Corporation. The remaining 44.5%, or $0.56M (83,508 thousand JPY), funded LD deep-tech hardware. By granting TDK exclusive general consumer manufacturing rights for Augmented Reality (AR) smart glasses, QD Laser isolates itself from retail inventory valuation risks while aggressively pushing its strictly-retained medical IP into clinical pipelines, proven by the October 2025 launch of the RETISSA MEOCHECK NEO, following the RETISSA ON HAND (2023/2024) and Lantana systems (2024).

The immediate existential threat is client revenue concentration. The silicon photonics pipeline is chained to Intel Corporation, generating $0.72M (107,857 thousand JPY) in accounts receivable at FY2026 close, while diagnostic integration historically relied on Beckman Coulter, Inc., accounting for 12.73% ($1.11M / 166,665 thousand JPY) of FY2025 sales. Despite issuing a revised earnings forecast on December 19, 2025, and marking its 20th fiscal period (established April 2006) without net profitability, the strategic CapEx offset via the $2.21M state subsidy provides absolute mechanical validation that management is successfully defending the balance sheet. If the $3.30M short-term NRE backlog converts without supplier disruption in Taiwan, China, or Thailand, the enterprise target of 15% EBITDA margins by FY2027 remains mathematically viable.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."