Standard Nuclear: 40 MTU Capacity Target Near Oak Ridge as -743.0% Q1 Gross Margin Exposes Pre-Scale Cost Load

Date : 2026-06-22

Reading : 240

HDIN Executive Takeaways

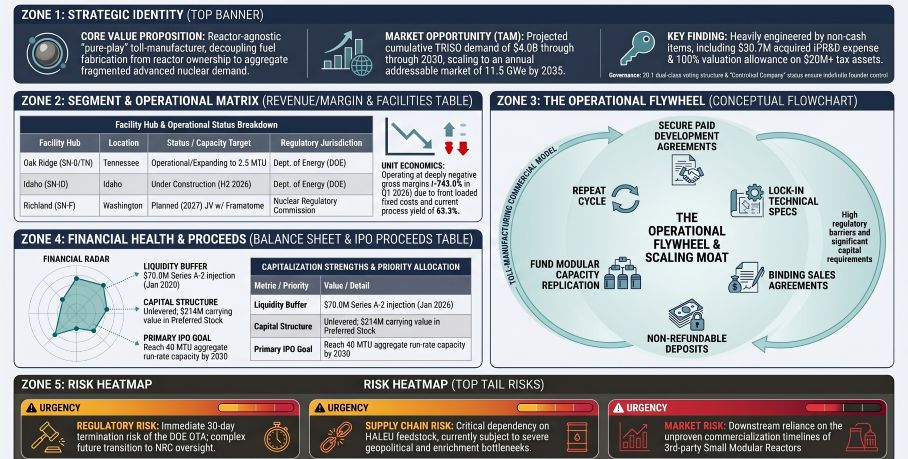

* Standard Nuclear’s transition to commercial operations contracted gross margins to -743.0% in Q1 2026, driven by an unoptimized fixed-cost base absorbing $5.0 million in cost of revenue against merely $0.6 million in quarterly fixed-price sales.

* The company’s "Replicate, Don’t Redesign" model relies on deploying 1.0 to 20.0 MTU modules across Oak Ridge, TN, Idaho Falls, ID, and Richland, WA, though output is bottlenecked by upstream HALEU availability and 9-to-12-month delivery schedules for custom thermal processing furnaces.

* Despite a reported $245 million contract backlog and a $70.0 million Series A-2 capital injection providing near-term liquidity, minority investors face governance subordination via a 20:1 Class B voting structure and heavy related-party transaction volumes.

Figure Standard Nuclear S-1 Synthesis Institutional-Grade Structural Deconstruction

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Standard Nuclear Inc. [NYSE: STDN] operates as a single reporting segment executing purely on Tristructural Isotropic (TRISO) fuel development. The income statement exhibits extreme near-term friction characteristic of a pre-scale hardware manufacturer transitioning from government-sponsored research out of its first-of-a-kind (FOAK) pilot facility. Research and development expenses accounted for 0% of sales for the year ended December 31, 2025, and Q1 2026, following a $30.3 million non-cash in-process research and development (IPR&D) charge in 2024 related to the acquisition of Ultra Safe Nuclear Corporation (USNC) assets. The total purchase price was $32.9 million, of which $30.7 million was attributed to IPR&D and immediately expensed.

General and administrative (G&A) expenses surged to $4.5 million in 2025 (143% of $3.1 million in revenue) and $3.8 million in Q1 2026 (645% of $0.6 million in revenue). Revenue is recognized under ASC 606 over time using an input method based on a cost-to-cost measure of progress for fixed-price contracts, and a right-to-invoice practical expedient for time-and-materials.

Table Income Statement and Segmental Gross Margins

Cash Flow Rigor and Liquidity Deterioration

* 2024: Net Loss of $(56.6) million against Operating Cash Flow (OCF) of $(0.4) million and Free Cash Flow (FCF) of $(2.6) million. The $56.2 million divergence was driven by the $30.3 million IPR&D charge and a $25.6 million non-cash fair value adjustment on Level 3 SAFE notes (utilizing a "bond plus call" model).

* 2025: Net Loss of $(15.5) million against OCF of $(6.7) million and FCF of $(15.6) million. Divergence was bridged by $7.7 million in SAFE note fair value adjustments and $1.7 million in stock-based compensation (SBC).

* Q1 2026: Net Loss of $(7.7) million against OCF of $(4.3) million and FCF of $(8.2) million. The $3.4 million gap was bridged by an increase in accounts payable and $1.5 million in SBC (with $0.5 million embedded directly in the $5.0 million Q1 cost of revenue).

* Balance Sheet Realities: Working capital is impaired by extended collection cycles. Days Sales Outstanding (DSO) exceeds 90 days, with accounts receivable at $2.3 million at the end of 2025 and $1.0 million in Q1 2026, complemented by $0.7 million in unbilled contract assets. Inventory is structurally $0, as customers supply the enriched uranium. Accounts payable expanded to $5.0 million in Q1 2026.

* Capital Output: Q1 2026 capital expenditures required $3.9 million. The company carries an accumulated deficit of $79.9 million, zero debt, and capitalization relies on temporary/mezzanine equity carrying over $214 million across Series Seed, Seed-1, A, and A-2 preferred stock. A $70.0 million Series A-2 transaction was completed on January 23, 2026.

Infrastructure Layout and Regional Moats

Standard Nuclear mitigates commodity risk by operating as a specialized toll manufacturer, pricing fabrication between $50.0 million and $80.0 million per Metric Ton of Uranium (MTU). The company estimates a cumulative $4.0 billion Total Addressable Market (TAM) through 2030, assuming 3.2 GWe of demand, with a Serviceable Addressable Market (SAM) of $3.2 billion (capturing 75%). By 2035, the annual TAM is projected to reach 11.5 GWe. Macro tailwinds indicate U.S. electricity demand expanding 44% from 4,990 TWh in 2026 to over 7,200 TWh by 2040, moving annual load growth from 1% to 3%.

To service this, Standard Nuclear relies on a "Replicate, Don't Redesign" model to hit an aggregate 40 MTU run-rate capacity no earlier than 2030. Current process yield stands at 63.3%.

Modular Hub Layout and Physical Assets

* Oak Ridge SN-0 (Oak Ridge, TN): Operational 24,600 sq. ft. pilot facility functioning under Department of Energy (DOE) authorization. Features an initial and scalable peak capacity of 0.5 MTU (500 kgU).

* Oak Ridge SN-TN (Oak Ridge, TN): Under construction (H2 2026). A 12,500 sq. ft. facility with an initial 1.0 MTU capacity, scaling to 2.5 MTU.

* Idaho SN-ID (Idaho Falls, ID): Under construction (H2 2026) on DOE property. A 12,500 sq. ft. layout with an initial 1.0 MTU capacity, scaling to 2.5 MTU.

* Richland SN-F (Richland, WA): Planned for 2027 under Nuclear Regulatory Commission (NRC) jurisdiction via a joint venture with Framatome. Initial capacity of 1.0 MTU, scaling to 20.0 MTU.

* Oak Ridge SN-TN20 (Oak Ridge, TN): Land acquired for a planned 20.0 MTU facility.

The sales cycle requires 6 to 12 months for Fuel Development Agreements, generating upfront deposits up to 24 months in advance. The supply chain demands 9 to 12 months of lead time for thermal furnaces. The revenue base is highly concentrated. In Q1 2026, U.S. customers represented 80.2% ($476,313) and European customers represented 19.8% ($117,489) of total revenue. Customer A generated ~$200,000 (33.7%), Customer B generated ~$200,000 (33.7%), and Customer C contributed ~$100,000 (16.8%) in Q1 2026. In 2025, Customer A contributed ~$1.1 million (35.0%), Customer B ~$900,000 (28.7%), and Customer C ~$600,000 (19.1%). In Q1 2025, Customer A dominated with ~$300,000 (79.4%).

Workforce headcount scaled from 80 full-time employees on March 31, 2026, to 106 by June 2026, representing a 32.5% acceleration. The technical team utilizes over 150 years of U.S. National Laboratory experience, operating entirely without collective bargaining agreements, with 23 personnel holding master's degrees or PhDs.

HDIN Institutional Verdict

While Standard Nuclear captures early mover status against competitors like BWXT Technologies and substitute technologies (fusion, legacy light-water, wind, solar), the company’s structural integrity is constrained by extreme regulatory dependencies and inside-heavy governance.

Joint Venture Deadlocks & Regulatory Threats

Standard Nuclear holds a 66.67% interest in the Framatome LLC Variable Interest Entity (VIE) housing the Richland SN-F facility (Framatome holds 33.33%). Due to a 3-to-3 board split, Standard Nuclear cannot unilaterally dictate operations. The equity method carrying amount was $1.1 million in Q1 2026, but the VIE carries a $6.5 million dissolution penalty contingent upon failing to secure a binding Purchase Commitment by August 2027. Furthermore, current operations depend on a DOE Other Transaction Agreement (OTA) providing Price-Anderson Act indemnification up to $16.5 billion. The DOE can terminate this OTA with 30 days' notice, forcing an immediate, cost-prohibitive transition to NRC licensing.

Related-Party Governance & Capitalization Deficits

Standard Nuclear will list as a "controlled company," enforcing a dual-class share structure where Class B stock commands 20 votes per share against Class A's 1 vote. The Executive Chairman controls a Class B Equity Exchange Agreement, cementing absolute voting authority. The balance sheet exhibits aggressive related-party transactions: Decisive Point Group supplied $4.9 million in Seed-1, $8.8 million in Series A, $5.0 million in Series A-2, and a $1.26 million non-interest-bearing cash advance. Executives received 50% non-recourse promissory notes carrying 4.07% to 4.08% interest rates to purchase restricted stock, specifically $719,250 to the CEO, $453,600 to the COO, and $1.53 million to $1.54 million to the CFO. The COO also received a $31,250 relocation advance. A Master Services Agreement with Neutroelectric, LLC (owned by the CEO's spouse) resulted in $240,000 in payouts, while another spouse secured a schedule management contract for $13,600 per month from April 1 through June 30, 2026.

Post-Balance Sheet Volatility and Accounting Estimates

Following Q1 2026, the company reported a $245 million Total Contract Backlog ($65 million funded, $157 million in options, $23 million unfunded) and a $416 million qualified pipeline, alongside an MOU with Oklo Inc. Post-balance sheet equity issuances included 470,611 Class B shares to the CFO at $3.27 per share and 1,219,395 Class B options. Standard Nuclear utilizes the Black-Scholes model, assigning an exceptionally high 110.0% expected volatility. Management applies a 100% valuation allowance against its deferred tax assets ($10.4 million in federal and $9.8 million in state Net Operating Losses), yielding a 0.0% effective tax rate. Furthermore, the company carries a $0.8 million Asset Retirement Obligation (up from $0.7 million in 2024) and faces severe successor liability and intellectual property title risks stemming from the Section 363 bankruptcy acquisition of USNC assets. IPO proceeds are earmarked for working capital, M&A, S&M, R&D, and G&A, and will be parked in short-term U.S. government guaranteed obligations.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Standard Nuclear’s transition to commercial operations contracted gross margins to -743.0% in Q1 2026, driven by an unoptimized fixed-cost base absorbing $5.0 million in cost of revenue against merely $0.6 million in quarterly fixed-price sales.

* The company’s "Replicate, Don’t Redesign" model relies on deploying 1.0 to 20.0 MTU modules across Oak Ridge, TN, Idaho Falls, ID, and Richland, WA, though output is bottlenecked by upstream HALEU availability and 9-to-12-month delivery schedules for custom thermal processing furnaces.

* Despite a reported $245 million contract backlog and a $70.0 million Series A-2 capital injection providing near-term liquidity, minority investors face governance subordination via a 20:1 Class B voting structure and heavy related-party transaction volumes.

Figure Standard Nuclear S-1 Synthesis Institutional-Grade Structural Deconstruction

Segmental Realities and Margin CompressionStandard Nuclear Inc. [NYSE: STDN] operates as a single reporting segment executing purely on Tristructural Isotropic (TRISO) fuel development. The income statement exhibits extreme near-term friction characteristic of a pre-scale hardware manufacturer transitioning from government-sponsored research out of its first-of-a-kind (FOAK) pilot facility. Research and development expenses accounted for 0% of sales for the year ended December 31, 2025, and Q1 2026, following a $30.3 million non-cash in-process research and development (IPR&D) charge in 2024 related to the acquisition of Ultra Safe Nuclear Corporation (USNC) assets. The total purchase price was $32.9 million, of which $30.7 million was attributed to IPR&D and immediately expensed.

General and administrative (G&A) expenses surged to $4.5 million in 2025 (143% of $3.1 million in revenue) and $3.8 million in Q1 2026 (645% of $0.6 million in revenue). Revenue is recognized under ASC 606 over time using an input method based on a cost-to-cost measure of progress for fixed-price contracts, and a right-to-invoice practical expedient for time-and-materials.

Table Income Statement and Segmental Gross Margins

| Period | Contract Type | Revenue (USD) | % of Total | Cost of Revenue (USD) | Gross Profit / Margin |

| Q1 2026 | Fixed price | $593,802 | 100.0% | $5,006,006 | -$4,412,204 / -743.0% |

| Q1 2025 | Fixed price | $70,867 | 18.8% | - | - |

| Time and materials | $307,059 | 81.2% | - | - | |

| Total | $377,926 | 100.0% | $1,120,504 | -$742,578 / -196.5% | |

| FY 2025 | Fixed price | $2,046,383 | 65.2% | - | - |

| Time and materials | $1,093,682 | 34.8% | - | - | |

| Total | $3,140,065 | 100.0% | $7,672,905 | -$4,532,840 / -144.4% | |

| FY 2024 | All Contracts | $0 | 0.0% | $0 | $0 / 0.0% |

Cash Flow Rigor and Liquidity Deterioration

* 2024: Net Loss of $(56.6) million against Operating Cash Flow (OCF) of $(0.4) million and Free Cash Flow (FCF) of $(2.6) million. The $56.2 million divergence was driven by the $30.3 million IPR&D charge and a $25.6 million non-cash fair value adjustment on Level 3 SAFE notes (utilizing a "bond plus call" model).

* 2025: Net Loss of $(15.5) million against OCF of $(6.7) million and FCF of $(15.6) million. Divergence was bridged by $7.7 million in SAFE note fair value adjustments and $1.7 million in stock-based compensation (SBC).

* Q1 2026: Net Loss of $(7.7) million against OCF of $(4.3) million and FCF of $(8.2) million. The $3.4 million gap was bridged by an increase in accounts payable and $1.5 million in SBC (with $0.5 million embedded directly in the $5.0 million Q1 cost of revenue).

* Balance Sheet Realities: Working capital is impaired by extended collection cycles. Days Sales Outstanding (DSO) exceeds 90 days, with accounts receivable at $2.3 million at the end of 2025 and $1.0 million in Q1 2026, complemented by $0.7 million in unbilled contract assets. Inventory is structurally $0, as customers supply the enriched uranium. Accounts payable expanded to $5.0 million in Q1 2026.

* Capital Output: Q1 2026 capital expenditures required $3.9 million. The company carries an accumulated deficit of $79.9 million, zero debt, and capitalization relies on temporary/mezzanine equity carrying over $214 million across Series Seed, Seed-1, A, and A-2 preferred stock. A $70.0 million Series A-2 transaction was completed on January 23, 2026.

Infrastructure Layout and Regional Moats

Standard Nuclear mitigates commodity risk by operating as a specialized toll manufacturer, pricing fabrication between $50.0 million and $80.0 million per Metric Ton of Uranium (MTU). The company estimates a cumulative $4.0 billion Total Addressable Market (TAM) through 2030, assuming 3.2 GWe of demand, with a Serviceable Addressable Market (SAM) of $3.2 billion (capturing 75%). By 2035, the annual TAM is projected to reach 11.5 GWe. Macro tailwinds indicate U.S. electricity demand expanding 44% from 4,990 TWh in 2026 to over 7,200 TWh by 2040, moving annual load growth from 1% to 3%.

To service this, Standard Nuclear relies on a "Replicate, Don't Redesign" model to hit an aggregate 40 MTU run-rate capacity no earlier than 2030. Current process yield stands at 63.3%.

Modular Hub Layout and Physical Assets

* Oak Ridge SN-0 (Oak Ridge, TN): Operational 24,600 sq. ft. pilot facility functioning under Department of Energy (DOE) authorization. Features an initial and scalable peak capacity of 0.5 MTU (500 kgU).

* Oak Ridge SN-TN (Oak Ridge, TN): Under construction (H2 2026). A 12,500 sq. ft. facility with an initial 1.0 MTU capacity, scaling to 2.5 MTU.

* Idaho SN-ID (Idaho Falls, ID): Under construction (H2 2026) on DOE property. A 12,500 sq. ft. layout with an initial 1.0 MTU capacity, scaling to 2.5 MTU.

* Richland SN-F (Richland, WA): Planned for 2027 under Nuclear Regulatory Commission (NRC) jurisdiction via a joint venture with Framatome. Initial capacity of 1.0 MTU, scaling to 20.0 MTU.

* Oak Ridge SN-TN20 (Oak Ridge, TN): Land acquired for a planned 20.0 MTU facility.

The sales cycle requires 6 to 12 months for Fuel Development Agreements, generating upfront deposits up to 24 months in advance. The supply chain demands 9 to 12 months of lead time for thermal furnaces. The revenue base is highly concentrated. In Q1 2026, U.S. customers represented 80.2% ($476,313) and European customers represented 19.8% ($117,489) of total revenue. Customer A generated ~$200,000 (33.7%), Customer B generated ~$200,000 (33.7%), and Customer C contributed ~$100,000 (16.8%) in Q1 2026. In 2025, Customer A contributed ~$1.1 million (35.0%), Customer B ~$900,000 (28.7%), and Customer C ~$600,000 (19.1%). In Q1 2025, Customer A dominated with ~$300,000 (79.4%).

Workforce headcount scaled from 80 full-time employees on March 31, 2026, to 106 by June 2026, representing a 32.5% acceleration. The technical team utilizes over 150 years of U.S. National Laboratory experience, operating entirely without collective bargaining agreements, with 23 personnel holding master's degrees or PhDs.

HDIN Institutional Verdict

While Standard Nuclear captures early mover status against competitors like BWXT Technologies and substitute technologies (fusion, legacy light-water, wind, solar), the company’s structural integrity is constrained by extreme regulatory dependencies and inside-heavy governance.

Joint Venture Deadlocks & Regulatory Threats

Standard Nuclear holds a 66.67% interest in the Framatome LLC Variable Interest Entity (VIE) housing the Richland SN-F facility (Framatome holds 33.33%). Due to a 3-to-3 board split, Standard Nuclear cannot unilaterally dictate operations. The equity method carrying amount was $1.1 million in Q1 2026, but the VIE carries a $6.5 million dissolution penalty contingent upon failing to secure a binding Purchase Commitment by August 2027. Furthermore, current operations depend on a DOE Other Transaction Agreement (OTA) providing Price-Anderson Act indemnification up to $16.5 billion. The DOE can terminate this OTA with 30 days' notice, forcing an immediate, cost-prohibitive transition to NRC licensing.

Related-Party Governance & Capitalization Deficits

Standard Nuclear will list as a "controlled company," enforcing a dual-class share structure where Class B stock commands 20 votes per share against Class A's 1 vote. The Executive Chairman controls a Class B Equity Exchange Agreement, cementing absolute voting authority. The balance sheet exhibits aggressive related-party transactions: Decisive Point Group supplied $4.9 million in Seed-1, $8.8 million in Series A, $5.0 million in Series A-2, and a $1.26 million non-interest-bearing cash advance. Executives received 50% non-recourse promissory notes carrying 4.07% to 4.08% interest rates to purchase restricted stock, specifically $719,250 to the CEO, $453,600 to the COO, and $1.53 million to $1.54 million to the CFO. The COO also received a $31,250 relocation advance. A Master Services Agreement with Neutroelectric, LLC (owned by the CEO's spouse) resulted in $240,000 in payouts, while another spouse secured a schedule management contract for $13,600 per month from April 1 through June 30, 2026.

Post-Balance Sheet Volatility and Accounting Estimates

Following Q1 2026, the company reported a $245 million Total Contract Backlog ($65 million funded, $157 million in options, $23 million unfunded) and a $416 million qualified pipeline, alongside an MOU with Oklo Inc. Post-balance sheet equity issuances included 470,611 Class B shares to the CFO at $3.27 per share and 1,219,395 Class B options. Standard Nuclear utilizes the Black-Scholes model, assigning an exceptionally high 110.0% expected volatility. Management applies a 100% valuation allowance against its deferred tax assets ($10.4 million in federal and $9.8 million in state Net Operating Losses), yielding a 0.0% effective tax rate. Furthermore, the company carries a $0.8 million Asset Retirement Obligation (up from $0.7 million in 2024) and faces severe successor liability and intellectual property title risks stemming from the Section 363 bankruptcy acquisition of USNC assets. IPO proceeds are earmarked for working capital, M&A, S&M, R&D, and G&A, and will be parked in short-term U.S. government guaranteed obligations.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."