Mitsubishi Electric Corporation: $829.02M Nozomi Networks Acquisition Near San Francisco as +100 BPS Margin Expansion Signals Transition to OPEX-Driven Software Ecosystem

Date : 2026-06-22

Reading : 294

HDIN Executive Takeaways

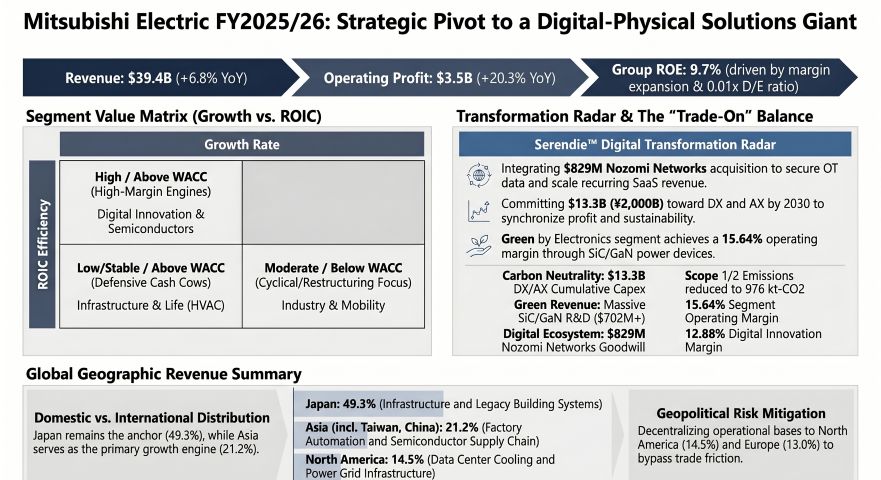

* FY26 operating profit acceleration (+20.3% to $3,517.3M) outpaced revenue expansion (+6.8% to $39,411.7M), driving a 130-basis-point ROE expansion to 9.7% on an underleveraged 0.01x D/E balance sheet.

* Supply chain recalibration elongated the cash conversion cycle by 4.4 days to 141.4 days, necessitating localized operational buffers across nodes in Taiwan, China, and Europe.

* Goodwill expanded +136.1% year-over-year to $2,442.00M following the $928.40M acquisition of US-based Nozomi Networks, introducing unamortized impairment risks to the "Serendie" digital architecture.

Figure Mitsubishi Electric FY2025/26: Strategic Pivot to a Digital-Physical Solutions Giant

Segmental Realities, Margin Compression, and Capital Allocation

Segmental Realities, Margin Compression, and Capital Allocation

Mitsubishi Electric Corporation [TYO: 6503] executes capital allocation across a bifurcated corporate matrix, relying on legacy industrial units for absolute cash generation while subsidizing early-stage digital ecosystems to drive Return on Invested Capital (ROIC). During the fiscal year ending March 2026, positive operating leverage materialized through a 150-basis-point gross profit margin expansion (30.6% to 32.1%) and a 100-basis-point operating margin expansion (7.9% to 8.9%). The firm’s net profit margin tracked upward by 100 basis points (5.9% to 6.9%), driving an un-levered ROE optimization from 8.4% to 9.7%. All internal JPY figures convert at a stated rate of 1 USD = 149.5686 JPY.

Table 1: FY2025 Business Segment Revenue, Profitability, and Capital Dynamics

R&D expenditure operates on a deliberate asymmetry. Total R&D reached $2,077.6 million, representing 5.63% of consolidated revenue. The Semiconductor & Device segment absorbed 33.8% of aggregate R&D ($702.9M), commanding a nearly 39.0% R&D-to-Revenue ratio to defend intellectual property in SiC power modules. The Life segment secured 21.6% ($449.0M, ~3.1% ratio), Infrastructure 19.6% ($406.4M, ~5.0% ratio), Industry & Mobility 12.9% ($267.2M, ~2.5% ratio), and Digital Innovation 1.6% ($33.4M, ~5.9% ratio), with Corporate capturing the remaining 10.5% ($218.7M). High-precision mechatronics protection (MELSEC MX series and ±5μm tolerance MTR-S robots), AMSR3 space platforms, and Access Advance LLC HEVC patent pool licensing form the defensive IP moat.

Infrastructure Layout, Supply Chain Architecture, and Regional Moats

Mitsubishi Electric Corporation remains geographically anchored to the Japanese domestic market, which generated $18,209.4M (49.3% of revenue). The Asian market acts as the primary hardware volume engine, generating $7,830.9M (21.2%). North America generated $5,342.6M (14.5%), driven by data center infrastructure, while Europe accounted for $4,804.0M (13.0%) via grid modernization. Peripheral regions generated the remaining $730.7M (2.0%).

Physical operations are explicitly decentralized to bypass geopolitical trade friction and severe physical climate risks (such as localized flooding). Key international production buffers include:

* Asia: High-volume assembly is managed by Mitsubishi Electric Consumer Products in Thailand and Mitsubishi Electric Air Conditioning Systems in Guangzhou, China. Semiconductor and FA flows are sustained by Taiwan Mitsubishi Electric Automation Co., Ltd., located in Taiwan, China, and Mitsubishi Electric Automation (China) Ltd. Heavy industrial loads are facilitated by Toshiba Mitsubishi-Electric Industrial Systems Corporation (TMEIC).

* Americas & Europe: Grid infrastructure is localized at Mitsubishi Electric Power Products in the US, while power module distribution is managed by Vincotech Holdings in Europe.

Despite robust cash generation, macroeconomic friction—specifically soaring aircraft and ship logistics costs and raw material inflation—triggered a working capital trap during the transition to FY26. Accounts Receivable (AR) expanded from $7,668.9M to $8,669.5M, elongating Days Sales Outstanding (DSO) from 75.8 to 80.3 days. Absolute inventories grew from $8,323.7M to $8,438.5M, though velocity optimization improved Days Inventory Outstanding (DIO) from 118.6 to 115.0 days. Accounts Payable (AP) compressed from $4,024.8M to $3,958.2M, accelerating Days Payable Outstanding (DPO) from 57.4 to 53.9 days. The net effect was a 4.4-day elongation of the Cash Conversion Cycle (CCC) from 137.0 to 141.4 days.

Balance Sheet Transformation and Corporate Governance Execution

Management is mathematically restructuring the balance sheet, utilizing an aggressively underleveraged capital structure (Debt-to-Equity reduced from 0.08x to 0.01x) to fund strategic acquisitions. Total assets expanded from $42,627.1M to $49,191.6M, supported by total equity compounding from $26,407.1M to $29,981.3M.

Table 2: Cash Flow and Capital Optimization Analysis

The most acute alteration to the asset base is the +136.1% year-over-year expansion in total Goodwill, soaring from $1,034.36M to $2,442.00M. This spike is directly attributed to the January 28, 2026, acquisition of US-based OT security firm Nozomi Networks. The acquisition required $928.40M in absolute consideration, producing $829.02M in unamortized Goodwill, which introduces heightened annual impairment risks to the digital ecosystem. Capital optimization simultaneously triggered the liquidation of 14 cross-shareholdings, generating $335.37M in cash. The firm retains 115 strategic stocks valued at $736.04M, holding equity in critical partners like UFJ, Synspective, and HD Renewable Energy Co., Ltd.

Governance and operational labor chains have been centralized under a newly appointed Chief Risk Management Officer (CRO). The Board of Directors maintains a 10-member structure mathematically weighted toward external oversight (6 Outside Directors, 4 Internal Directors). The Nomination, Compensation, and Audit committees are chaired exclusively by Outside Directors and maintain strict 3-to-1 outside-to-internal ratios. Executive compensation mandates a 35% fixed and 65% variable split for the CEO (32% short-term bonus, 23% Performance Share Units tied to TSR, 10% Restricted Stock Units). The bonus payout formula is governed by hard metrics: Consolidated Revenue (20%), Operating Profit Margin (30%), Operating Cash Flow (25%), and ROE (25%). Other executives operate on a 36-43% fixed against 57-64% variable matrix.

Environmental and human capital risk mitigation is supported by a planned $13,371.8M DX/AX CAPEX pipeline slated through 2030. Scope 1 and 2 emissions fell from 1,071 kt-CO2 to 976 kt-CO2. Internally, the firm tracks human capital efficiency strictly: employee engagement scores rose from 43.0 to 53.0, the female manager ratio hit 4.2%, male childcare leave reached 89.9%, and disability employment registered at 2.52%.

HDIN Institutional Verdict

Mitsubishi Electric Corporation is executing an authentic "Trade-On" strategy, effectively utilizing regulatory carbon taxes and physical climate risks as pricing leverage for its high-margin SiC power devices and Net Zero Energy Building (ZEB) infrastructure. However, the immediate macroeconomic vulnerability is the documented "delay in the EV transition," which threatens capacity utilization rates across newly capitalized semiconductor lines. The pivot to OPEX-driven software (the "Serendie" platform) is mathematically necessary to escape hardware commoditization. Yet, by locking $829.02M into Nozomi Networks Goodwill, management has transitioned existential risk away from tangible factory obsolescence and directly into digital integration execution. If "Physical AI" and predictive maintenance contracts fail to generate ROIC above the Weighted Average Cost of Capital (WACC), the subsequent impairment write-downs will instantly compress the firm's un-levered ROE momentum.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* FY26 operating profit acceleration (+20.3% to $3,517.3M) outpaced revenue expansion (+6.8% to $39,411.7M), driving a 130-basis-point ROE expansion to 9.7% on an underleveraged 0.01x D/E balance sheet.

* Supply chain recalibration elongated the cash conversion cycle by 4.4 days to 141.4 days, necessitating localized operational buffers across nodes in Taiwan, China, and Europe.

* Goodwill expanded +136.1% year-over-year to $2,442.00M following the $928.40M acquisition of US-based Nozomi Networks, introducing unamortized impairment risks to the "Serendie" digital architecture.

Figure Mitsubishi Electric FY2025/26: Strategic Pivot to a Digital-Physical Solutions Giant

Segmental Realities, Margin Compression, and Capital AllocationMitsubishi Electric Corporation [TYO: 6503] executes capital allocation across a bifurcated corporate matrix, relying on legacy industrial units for absolute cash generation while subsidizing early-stage digital ecosystems to drive Return on Invested Capital (ROIC). During the fiscal year ending March 2026, positive operating leverage materialized through a 150-basis-point gross profit margin expansion (30.6% to 32.1%) and a 100-basis-point operating margin expansion (7.9% to 8.9%). The firm’s net profit margin tracked upward by 100 basis points (5.9% to 6.9%), driving an un-levered ROE optimization from 8.4% to 9.7%. All internal JPY figures convert at a stated rate of 1 USD = 149.5686 JPY.

Table 1: FY2025 Business Segment Revenue, Profitability, and Capital Dynamics

| Business Segment | Revenue ($M) | % of Total | Op Profit ($M) | OP Margin | Key Segmental Driver |

| Life | $14,460.3 | 39.2% | $1,051.7 | 7.27% | Strong pricing power in HVAC/heat pumps. |

| Industry & Mobility | $10,873.0 | 29.4% | $552.3 | 5.08% | Cyclical headwinds; EV transition delays. |

| Infrastructure | $8,100.2 | 21.9% | $598.2 | 7.38% | Defensive stability; grid upgrades/EMS. |

| Semiconductor | $1,737.4 | 4.7% | $271.7 | 15.64% | High-margin HVIGBT/SiC/GaN technology. |

| Digital Innovation | $564.9 | 1.5% | $72.8 | 12.88% | High-margin "Physical AI" OT extraction. |

| Others | $1,182.1 | 3.2% | $344.9 | 29.18% | Accretive internal/logistics services. |

| Total (Pre-Elim) | $36,917.6 | 100.0% | $2,891.6 | 7.83% | Aggregate baseline. |

R&D expenditure operates on a deliberate asymmetry. Total R&D reached $2,077.6 million, representing 5.63% of consolidated revenue. The Semiconductor & Device segment absorbed 33.8% of aggregate R&D ($702.9M), commanding a nearly 39.0% R&D-to-Revenue ratio to defend intellectual property in SiC power modules. The Life segment secured 21.6% ($449.0M, ~3.1% ratio), Infrastructure 19.6% ($406.4M, ~5.0% ratio), Industry & Mobility 12.9% ($267.2M, ~2.5% ratio), and Digital Innovation 1.6% ($33.4M, ~5.9% ratio), with Corporate capturing the remaining 10.5% ($218.7M). High-precision mechatronics protection (MELSEC MX series and ±5μm tolerance MTR-S robots), AMSR3 space platforms, and Access Advance LLC HEVC patent pool licensing form the defensive IP moat.

Infrastructure Layout, Supply Chain Architecture, and Regional Moats

Mitsubishi Electric Corporation remains geographically anchored to the Japanese domestic market, which generated $18,209.4M (49.3% of revenue). The Asian market acts as the primary hardware volume engine, generating $7,830.9M (21.2%). North America generated $5,342.6M (14.5%), driven by data center infrastructure, while Europe accounted for $4,804.0M (13.0%) via grid modernization. Peripheral regions generated the remaining $730.7M (2.0%).

Physical operations are explicitly decentralized to bypass geopolitical trade friction and severe physical climate risks (such as localized flooding). Key international production buffers include:

* Asia: High-volume assembly is managed by Mitsubishi Electric Consumer Products in Thailand and Mitsubishi Electric Air Conditioning Systems in Guangzhou, China. Semiconductor and FA flows are sustained by Taiwan Mitsubishi Electric Automation Co., Ltd., located in Taiwan, China, and Mitsubishi Electric Automation (China) Ltd. Heavy industrial loads are facilitated by Toshiba Mitsubishi-Electric Industrial Systems Corporation (TMEIC).

* Americas & Europe: Grid infrastructure is localized at Mitsubishi Electric Power Products in the US, while power module distribution is managed by Vincotech Holdings in Europe.

Despite robust cash generation, macroeconomic friction—specifically soaring aircraft and ship logistics costs and raw material inflation—triggered a working capital trap during the transition to FY26. Accounts Receivable (AR) expanded from $7,668.9M to $8,669.5M, elongating Days Sales Outstanding (DSO) from 75.8 to 80.3 days. Absolute inventories grew from $8,323.7M to $8,438.5M, though velocity optimization improved Days Inventory Outstanding (DIO) from 118.6 to 115.0 days. Accounts Payable (AP) compressed from $4,024.8M to $3,958.2M, accelerating Days Payable Outstanding (DPO) from 57.4 to 53.9 days. The net effect was a 4.4-day elongation of the Cash Conversion Cycle (CCC) from 137.0 to 141.4 days.

Balance Sheet Transformation and Corporate Governance Execution

Management is mathematically restructuring the balance sheet, utilizing an aggressively underleveraged capital structure (Debt-to-Equity reduced from 0.08x to 0.01x) to fund strategic acquisitions. Total assets expanded from $42,627.1M to $49,191.6M, supported by total equity compounding from $26,407.1M to $29,981.3M.

Table 2: Cash Flow and Capital Optimization Analysis

| Metric | FY25 (154th) | FY26 (155th) | Structural Context |

| Operating Cash Flow (OCF) | $3,048.1M | $3,851.0M | Improved earnings quality; full self-funding of hardware CAPEX. |

| Investing Cash Flow (ICF) | $(1,282.0M) | $(2,302.7M) | Higher outflows due to SiC facility construction. |

| Free Cash Flow (FCF) | $1,766.1M | $1,548.4M | Continued liquidity for shareholder returns. |

| NCI Equity | $847.02M | $974.31M | Expansion of joint venture equity. |

The most acute alteration to the asset base is the +136.1% year-over-year expansion in total Goodwill, soaring from $1,034.36M to $2,442.00M. This spike is directly attributed to the January 28, 2026, acquisition of US-based OT security firm Nozomi Networks. The acquisition required $928.40M in absolute consideration, producing $829.02M in unamortized Goodwill, which introduces heightened annual impairment risks to the digital ecosystem. Capital optimization simultaneously triggered the liquidation of 14 cross-shareholdings, generating $335.37M in cash. The firm retains 115 strategic stocks valued at $736.04M, holding equity in critical partners like UFJ, Synspective, and HD Renewable Energy Co., Ltd.

Governance and operational labor chains have been centralized under a newly appointed Chief Risk Management Officer (CRO). The Board of Directors maintains a 10-member structure mathematically weighted toward external oversight (6 Outside Directors, 4 Internal Directors). The Nomination, Compensation, and Audit committees are chaired exclusively by Outside Directors and maintain strict 3-to-1 outside-to-internal ratios. Executive compensation mandates a 35% fixed and 65% variable split for the CEO (32% short-term bonus, 23% Performance Share Units tied to TSR, 10% Restricted Stock Units). The bonus payout formula is governed by hard metrics: Consolidated Revenue (20%), Operating Profit Margin (30%), Operating Cash Flow (25%), and ROE (25%). Other executives operate on a 36-43% fixed against 57-64% variable matrix.

Environmental and human capital risk mitigation is supported by a planned $13,371.8M DX/AX CAPEX pipeline slated through 2030. Scope 1 and 2 emissions fell from 1,071 kt-CO2 to 976 kt-CO2. Internally, the firm tracks human capital efficiency strictly: employee engagement scores rose from 43.0 to 53.0, the female manager ratio hit 4.2%, male childcare leave reached 89.9%, and disability employment registered at 2.52%.

HDIN Institutional Verdict

Mitsubishi Electric Corporation is executing an authentic "Trade-On" strategy, effectively utilizing regulatory carbon taxes and physical climate risks as pricing leverage for its high-margin SiC power devices and Net Zero Energy Building (ZEB) infrastructure. However, the immediate macroeconomic vulnerability is the documented "delay in the EV transition," which threatens capacity utilization rates across newly capitalized semiconductor lines. The pivot to OPEX-driven software (the "Serendie" platform) is mathematically necessary to escape hardware commoditization. Yet, by locking $829.02M into Nozomi Networks Goodwill, management has transitioned existential risk away from tangible factory obsolescence and directly into digital integration execution. If "Physical AI" and predictive maintenance contracts fail to generate ROIC above the Weighted Average Cost of Capital (WACC), the subsequent impairment write-downs will instantly compress the firm's un-levered ROE momentum.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."