Kawasaki Heavy Industries: FY2026 $1.137 Billion CapEx Pivot Near San Jose and Lincoln as ICC Arbitration Threatens $21.77 Billion Backlog

Date : 2026-06-22

Reading : 180

HDIN Executive Takeaways

* Operating cash flow yielded $936.50 million (¥140.0 billion) against a $1.05 billion (¥157.5 billion) capital expenditure draw, utilizing $2.40 billion (¥358.5 billion) in interest-free contract liabilities to absorb an 80.3% COGS ratio.

* A $10.27 billion (¥1,536.1 billion) aerospace backlog anchors a decentralized geographic network spanning from Kawasaki Rail Car Lincoln, Inc. to Nantong COSCO KHI Ship Engineering Co., Ltd.

* International Chamber of Commerce (ICC) arbitration regarding LNG tank provisions presents a material impairment risk to capitalized assets, constraining liquidity alongside a forward $1.137 billion (¥170.0 billion) FY2026 infrastructure outlay.

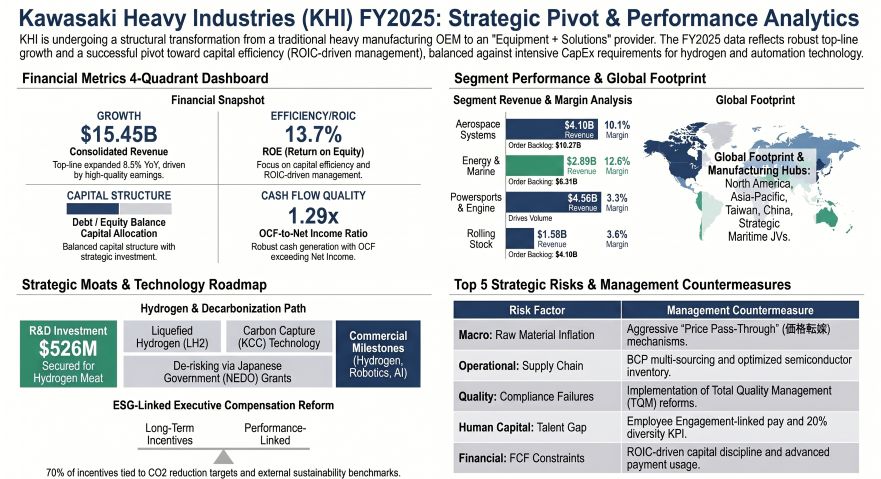

Figure Kawasaki Heavy Industries (KHl) FY2025: Strategic Pivot & Performance Analytics

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Kawasaki Heavy Industries reported FY2025 consolidated revenue of $15.45 billion (¥2,311.2 billion), representing an 8.54% year-over-year expansion from $14.24 billion. Business Profit reached $970.14 million (¥145.1 billion), generating an Operating Profit Margin of 6.28%. Proxy EBITDA aggregated to $1.52 billion, incorporating $548.78 million (¥82.08 billion) in depreciation and amortization. The cost of goods sold (COGS) expanded to $12.41 billion (¥1,856.3 billion), consuming 80.3% of revenue, while SG&A expenses were held at $2.20 billion (¥328.7 billion), or 14.2% of top-line performance.

Management enforces capital efficiency through an explicit Return on Invested Capital (ROIC) mandate. The firm recorded an FY2025 ROIC of 9.0%, conceptually benchmarked against an internal Weighted Average Cost of Capital (WACC) hurdle of roughly 10%. The Return on Equity (ROE) expanded to 13.7%. Forward FY2026 guidance projects Business Profit of $1.137 billion (¥170.0 billion) with a 6.6% margin and an 8.6% ROIC target.

The balance sheet reflects an optimized 54.5% Debt-to-Equity ratio, carrying $5.76 billion (¥861.1 billion) in interest-bearing debt against $771.65 million (¥115.4 billion) in cash and equivalents. Right-of-Use Assets stand at $454.18 million (¥67.93 billion), alongside $16.38 million (¥2.45 billion) in explicit contingent debt guarantees. Inventory cleared efficiently with a 6.0% YoY expansion to $5.50 billion (¥822.1 billion). The firm supports $3.63 billion (¥542.9 billion) in Property, Plant, and Equipment (PPE). FCF disclosures across different reporting segments reflect accounting variances: executive summaries cite a positive Free Cash Flow (FCF) of $802.3 million (¥120.0 billion) for the second consecutive fiscal year, while subsequent detailed cash flow schedules record $80.38 million and $80.23 million (¥12.0 billion). Net income of $723.13 million (¥108.1 billion) against operating cash flow of $936.50 million (¥140.0 billion) yields a 1.29x cash conversion ratio.

Infrastructure Layout and Regional Moats

The combined operational backlog equals $21.77 billion (¥3,256.8 billion). Aerospace dependency is anchored by rigid, multi-decade Original Equipment Manufacturer (OEM) cycles, specifically The Boeing Company (CH-47 program, 1985–2030), Lockheed Martin (P-3C program, 1978–2028), and Rolls-Royce (1991–2030), alongside Honeywell and Safran integrations on T55 and Trent series aero-engines. Kawasaki Heavy Industries utilizes unconsolidated joint ventures with IHI Corporation—IHI Investment for Aero Engine Leasing LLC and IHI Aero Engines US Co., Ltd.—to structure engine leasing exposure.

North American municipal transit contracts, specifically the Washington Metropolitan Area Transit Authority (WMATA) 7000 series railcar project, drive heavy manufacturing through Kawasaki Rail Car, Inc. (New York) and Kawasaki Rail Car Lincoln, Inc. (Nebraska). The North American Powersports supply chain routes through Kawasaki Motors Manufacturing Corp., U.S.A. (Nebraska) and Kawasaki Motors Corp., U.S.A. (Delaware). Future digital infrastructure relies on the Kawasaki Physical AI Center in San Jose, California, managing proprietary AI integrations for the "hinotori" surgical robot, "Nyokkey" service robot, "K-RACER" VTOL, and "CORLEO" platforms alongside alliances with NVIDIA, Microsoft, and Analog Devices.

In the Asia-Pacific region, heavy maritime construction is executed in mainland China via Nantong COSCO KHI Ship Engineering Co., Ltd. and Dalian COSCO KHI Ship Engineering Co., Ltd., supplemented by precision machinery sites in Suzhou, Kunshan, and Tianjin. Powersports manufacturing relies heavily on PT. Kawasaki Motor Indonesia, Kawasaki Motors Enterprise in Thailand, and facilities in the Philippines. Precision machinery utilizes Wipro Kawasaki Precision Machinery Pvt. Ltd. in India and Flutek, Ltd. in Korea. European distribution and niche engineering operate through Kawasaki Motors Europe N.V. (Netherlands), Kawasaki Precision Machinery UK Ltd. (UK), and Kawasaki Innovation Centre Europe SAS. Commercialization of blade-cleaning robotics functions through BladeRobots A/S, a joint venture with Vestas Wind Systems A/S. Total FY2025 R&D expenditures are reported at $525.73 million (¥78.6 billion), though alternate internal budgets frame the decarbonization and technology outlay at $723.13 million (¥108.15 billion), heavily subsidized by the New Energy and Industrial Technology Development Organization (NEDO) for Kawasaki CO2 Capture (KCC), Direct Air Capture (DAC), and liquefied hydrogen (LH2) architectures.

Structural Governance and Carbon Compliance

Executive compensation is strictly tethered to "Group Vision 2030" parameters via a 35% Basic Remuneration, 35% Short-Term Incentive (STI), and 30% Long-Term Incentive (LTI) matrix. STI cash payouts are determined by an Employee Engagement Index (measuring work satisfaction and supportive environments) and distinct net income brackets: a 0-45% payout for income under $167.1 million (¥25 billion), 50-95% for $167.1 million to $300.9 million (¥25 billion-¥45 billion), capped at 200%+ for income exceeding $468.0 million (¥70 billion). The LTI Performance Share Unit utilizes a 30% fixed tenure base and a 70% performance-based variable tracking Total Shareholder Return (TSR), Dow Jones Sustainability Index inclusion, and explicit Science Based Targets initiative (SBTi) milestones.

The Scope 1 and 2 emissions mandate requires a 50.4% reduction by 2032 (a decrease of 193,000 tons of CO2 relative to 2022), enforcing domestic Net Zero by 2030 and global Net Zero by 2050. The Scope 3 Category 11 mandate dictates a 30% reduction by 2032 (a drop of 2,025,600 tons of CO2), achieving "Zero-Carbon Ready" status by 2040. To counter Japan's demographic contraction, Kawasaki Heavy Industries mandates a Diversity, Equity, and Inclusion (DE&I) KPI to increase female, foreign, and mid-career general managers from 9.5% to 20% by 2030, supported by independent board directors Melanie Brock and Jennifer Rogers. Total Quality Management (TQM) and an independent Risk Management Department were formalized in 2025 as the enterprise's "Second Line of Defense" against prior compliance failures.

HDIN Institutional Verdict

Kawasaki Heavy Industries displays high-quality earnings conversion, yet the medium-term liquidity framework exhibits acute vulnerability. The $21.77 billion (¥3,256.8 billion) backlog is entirely dependent on the firm’s ability to execute price pass-throughs amid raw material inflation. The balance sheet exposes $225.76 million (¥33.77 billion) in total provisions, of which $146.00 million (¥21.84 billion) explicitly relates to warranties and loss-making construction contracts.

More critically, an ongoing International Chamber of Commerce (ICC) arbitration concerning overseas LNG tank projects threatens immediate impairment to capitalized financial assets. With a forward FY2026 capital expenditure authorization of $1.137 billion (¥170.0 billion) committed to hydrogen and automated infrastructure, the company must rely on the uninterrupted flow of its $2.40 billion (¥358.5 billion) in advanced customer contract liabilities. Any delayed OEM aerospace cycles or unfavorable ICC rulings will systematically compress cash reserves, forcing an expansion of the net debt position.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating cash flow yielded $936.50 million (¥140.0 billion) against a $1.05 billion (¥157.5 billion) capital expenditure draw, utilizing $2.40 billion (¥358.5 billion) in interest-free contract liabilities to absorb an 80.3% COGS ratio.

* A $10.27 billion (¥1,536.1 billion) aerospace backlog anchors a decentralized geographic network spanning from Kawasaki Rail Car Lincoln, Inc. to Nantong COSCO KHI Ship Engineering Co., Ltd.

* International Chamber of Commerce (ICC) arbitration regarding LNG tank provisions presents a material impairment risk to capitalized assets, constraining liquidity alongside a forward $1.137 billion (¥170.0 billion) FY2026 infrastructure outlay.

Figure Kawasaki Heavy Industries (KHl) FY2025: Strategic Pivot & Performance Analytics

Segmental Realities and Margin CompressionKawasaki Heavy Industries reported FY2025 consolidated revenue of $15.45 billion (¥2,311.2 billion), representing an 8.54% year-over-year expansion from $14.24 billion. Business Profit reached $970.14 million (¥145.1 billion), generating an Operating Profit Margin of 6.28%. Proxy EBITDA aggregated to $1.52 billion, incorporating $548.78 million (¥82.08 billion) in depreciation and amortization. The cost of goods sold (COGS) expanded to $12.41 billion (¥1,856.3 billion), consuming 80.3% of revenue, while SG&A expenses were held at $2.20 billion (¥328.7 billion), or 14.2% of top-line performance.

Management enforces capital efficiency through an explicit Return on Invested Capital (ROIC) mandate. The firm recorded an FY2025 ROIC of 9.0%, conceptually benchmarked against an internal Weighted Average Cost of Capital (WACC) hurdle of roughly 10%. The Return on Equity (ROE) expanded to 13.7%. Forward FY2026 guidance projects Business Profit of $1.137 billion (¥170.0 billion) with a 6.6% margin and an 8.6% ROIC target.

The balance sheet reflects an optimized 54.5% Debt-to-Equity ratio, carrying $5.76 billion (¥861.1 billion) in interest-bearing debt against $771.65 million (¥115.4 billion) in cash and equivalents. Right-of-Use Assets stand at $454.18 million (¥67.93 billion), alongside $16.38 million (¥2.45 billion) in explicit contingent debt guarantees. Inventory cleared efficiently with a 6.0% YoY expansion to $5.50 billion (¥822.1 billion). The firm supports $3.63 billion (¥542.9 billion) in Property, Plant, and Equipment (PPE). FCF disclosures across different reporting segments reflect accounting variances: executive summaries cite a positive Free Cash Flow (FCF) of $802.3 million (¥120.0 billion) for the second consecutive fiscal year, while subsequent detailed cash flow schedules record $80.38 million and $80.23 million (¥12.0 billion). Net income of $723.13 million (¥108.1 billion) against operating cash flow of $936.50 million (¥140.0 billion) yields a 1.29x cash conversion ratio.

Table FY2025 Segment Revenue, Profitability, and Backlog Profile

| Business Segment | Revenue ($B) | Business Profit ($M) | Margin (%) | Backlog ($B) |

| Aerospace Systems | 4.10 | 417.8 | 10.1% | 10.27 |

| Energy Solutions & Marine | 2.89 | 367.8 | 12.6% | 6.31 |

| Powersports & Engine | 4.56 | 152.1 | 3.3% | - |

| Precision Machinery & Robot | 1.73 | 96.2 | 5.5% | 0.74 |

| Rolling Stock | 1.58 | 58.1 | 3.6% | 4.10 |

| Total/Aggregate | 14.86 | 1,092.0 | - | 21.42 |

Infrastructure Layout and Regional Moats

The combined operational backlog equals $21.77 billion (¥3,256.8 billion). Aerospace dependency is anchored by rigid, multi-decade Original Equipment Manufacturer (OEM) cycles, specifically The Boeing Company (CH-47 program, 1985–2030), Lockheed Martin (P-3C program, 1978–2028), and Rolls-Royce (1991–2030), alongside Honeywell and Safran integrations on T55 and Trent series aero-engines. Kawasaki Heavy Industries utilizes unconsolidated joint ventures with IHI Corporation—IHI Investment for Aero Engine Leasing LLC and IHI Aero Engines US Co., Ltd.—to structure engine leasing exposure.

North American municipal transit contracts, specifically the Washington Metropolitan Area Transit Authority (WMATA) 7000 series railcar project, drive heavy manufacturing through Kawasaki Rail Car, Inc. (New York) and Kawasaki Rail Car Lincoln, Inc. (Nebraska). The North American Powersports supply chain routes through Kawasaki Motors Manufacturing Corp., U.S.A. (Nebraska) and Kawasaki Motors Corp., U.S.A. (Delaware). Future digital infrastructure relies on the Kawasaki Physical AI Center in San Jose, California, managing proprietary AI integrations for the "hinotori" surgical robot, "Nyokkey" service robot, "K-RACER" VTOL, and "CORLEO" platforms alongside alliances with NVIDIA, Microsoft, and Analog Devices.

In the Asia-Pacific region, heavy maritime construction is executed in mainland China via Nantong COSCO KHI Ship Engineering Co., Ltd. and Dalian COSCO KHI Ship Engineering Co., Ltd., supplemented by precision machinery sites in Suzhou, Kunshan, and Tianjin. Powersports manufacturing relies heavily on PT. Kawasaki Motor Indonesia, Kawasaki Motors Enterprise in Thailand, and facilities in the Philippines. Precision machinery utilizes Wipro Kawasaki Precision Machinery Pvt. Ltd. in India and Flutek, Ltd. in Korea. European distribution and niche engineering operate through Kawasaki Motors Europe N.V. (Netherlands), Kawasaki Precision Machinery UK Ltd. (UK), and Kawasaki Innovation Centre Europe SAS. Commercialization of blade-cleaning robotics functions through BladeRobots A/S, a joint venture with Vestas Wind Systems A/S. Total FY2025 R&D expenditures are reported at $525.73 million (¥78.6 billion), though alternate internal budgets frame the decarbonization and technology outlay at $723.13 million (¥108.15 billion), heavily subsidized by the New Energy and Industrial Technology Development Organization (NEDO) for Kawasaki CO2 Capture (KCC), Direct Air Capture (DAC), and liquefied hydrogen (LH2) architectures.

Structural Governance and Carbon Compliance

Executive compensation is strictly tethered to "Group Vision 2030" parameters via a 35% Basic Remuneration, 35% Short-Term Incentive (STI), and 30% Long-Term Incentive (LTI) matrix. STI cash payouts are determined by an Employee Engagement Index (measuring work satisfaction and supportive environments) and distinct net income brackets: a 0-45% payout for income under $167.1 million (¥25 billion), 50-95% for $167.1 million to $300.9 million (¥25 billion-¥45 billion), capped at 200%+ for income exceeding $468.0 million (¥70 billion). The LTI Performance Share Unit utilizes a 30% fixed tenure base and a 70% performance-based variable tracking Total Shareholder Return (TSR), Dow Jones Sustainability Index inclusion, and explicit Science Based Targets initiative (SBTi) milestones.

The Scope 1 and 2 emissions mandate requires a 50.4% reduction by 2032 (a decrease of 193,000 tons of CO2 relative to 2022), enforcing domestic Net Zero by 2030 and global Net Zero by 2050. The Scope 3 Category 11 mandate dictates a 30% reduction by 2032 (a drop of 2,025,600 tons of CO2), achieving "Zero-Carbon Ready" status by 2040. To counter Japan's demographic contraction, Kawasaki Heavy Industries mandates a Diversity, Equity, and Inclusion (DE&I) KPI to increase female, foreign, and mid-career general managers from 9.5% to 20% by 2030, supported by independent board directors Melanie Brock and Jennifer Rogers. Total Quality Management (TQM) and an independent Risk Management Department were formalized in 2025 as the enterprise's "Second Line of Defense" against prior compliance failures.

HDIN Institutional Verdict

Kawasaki Heavy Industries displays high-quality earnings conversion, yet the medium-term liquidity framework exhibits acute vulnerability. The $21.77 billion (¥3,256.8 billion) backlog is entirely dependent on the firm’s ability to execute price pass-throughs amid raw material inflation. The balance sheet exposes $225.76 million (¥33.77 billion) in total provisions, of which $146.00 million (¥21.84 billion) explicitly relates to warranties and loss-making construction contracts.

More critically, an ongoing International Chamber of Commerce (ICC) arbitration concerning overseas LNG tank projects threatens immediate impairment to capitalized financial assets. With a forward FY2026 capital expenditure authorization of $1.137 billion (¥170.0 billion) committed to hydrogen and automated infrastructure, the company must rely on the uninterrupted flow of its $2.40 billion (¥358.5 billion) in advanced customer contract liabilities. Any delayed OEM aerospace cycles or unfavorable ICC rulings will systematically compress cash reserves, forcing an expansion of the net debt position.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."