Global Hearing Healthcare 2026 Outlook: Why Premium Incumbents and Value Disruptors Diverge on Capital Allocation Amid APAC Reimbursement Squeezes

Date : 2026-06-23

Reading : 531

HDIN Executive Takeaways

* Divergent Cash Conversion Realities: Demant A/S converted 72.0% of its $839.6 million EBITDA into operating cash flow via retail efficiency, while Cochlear Limited’s cash conversion lagged at 38.8% due to a $130.3 million working capital absorption, pushing Days Inventory Outstanding (DIO) to 296.3 days.

* Aggressive Supply Chain Redundancy: Geopolitical friction triggered rapid near-shoring and multi-hub CapEx; GN Store Nord A/S relocated 31 production lines out of mainland China, while Sonova Holding AG shifted custom in-the-ear manufacturing from Vietnam to Alicante, Spain within 3.5 months.

* Structural Margin Ceilings: Despite World Health Organization (WHO) projections of a 2.5 billion patient pool by 2050, institutional monopsonies—specifically Volume-Based Procurement (VBP) in mainland China and US Managed Care consolidation—are systematically compressing average selling prices (ASP), forcing incumbents to acquire retail networks to protect end-to-end margins.

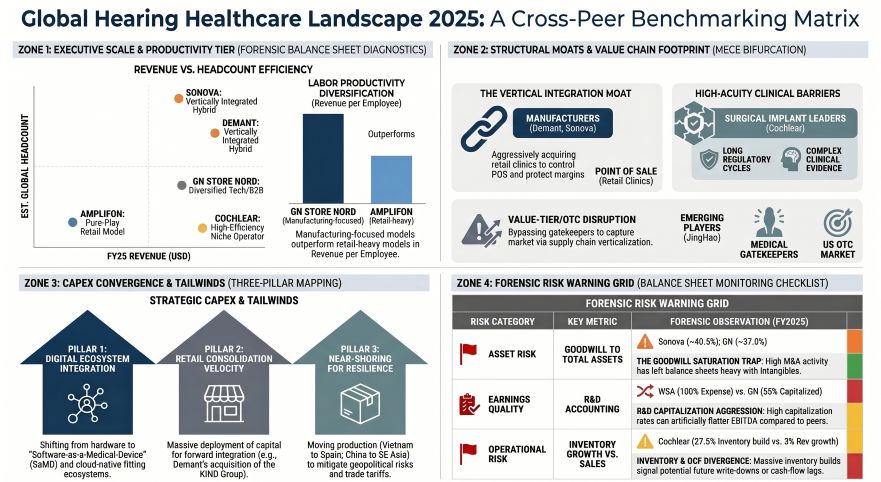

Figure Clobal Hearing Healthcare Landscape 2025: A Cross-Peer Benchmarking Matrix

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

The FY2025 financial disclosures delineate a sector experiencing stable structural demand but acute variations in organic top-line growth and earnings quality due to foreign exchange (FX) headwinds and macroeconomic softness.

Table FY2025 Normalized Revenue & Operating Matrix (USD)

Labor productivity is structurally dictated by the chosen operating channel. Automated business-to-business (B2B) models lead per-capita revenue generation. GN Store Nord A/S operates with 7,500+ employees, generating ~$351,100 per employee, followed by Cochlear Limited (~5,500 headcount; ~$276,200), WS Audiology A/S (~12,000 headcount; ~$243,000), and Sonova Holding AG (>18,000 headcount; ~$235,300). Conversely, vertically integrated and pure-play retail models inherently dilute labor productivity in exchange for direct patient access. Demant A/S employs ~22,719 staff globally yielding ~$158,600 per capita, while Amplifon S.p.A. operates with 20,900 employees yielding ~$129,600.

Segment breakdowns highlight severe differences in revenue concentration. Sonova Holding AG derives 93% of revenue from Hearing Instruments (split 56% Wholesale, 44% Retail via AudioNova) and 7% from Cochlear Implants. Demant A/S balances 43% Hearing Aids (Wholesale), 47% Hearing Care (Retail), and 10% Diagnostics (Interacoustics/GSI). GN Store Nord A/S relies on Hearing (ReSound) for only 43% of its top line, with the remaining 57% derived from Enterprise Audio (Jabra: 41%) and Gaming (SteelSeries: 16%). Cochlear Limited maintains a split of 62% Cochlear Implants, 26% Services, and 12% Acoustics. Amplifon S.p.A. remains 100% pure-play retail, while JingHao Medical focuses strictly on wholesale Direct-to-Consumer (DTC) Original Design Manufacturing (ODM).

Geographic exposures dictate regional reimbursement vulnerabilities:

* Americas: WS Audiology A/S reports 49% concentration. Cochlear Limited holds 48.5%. Demant A/S and GN Store Nord A/S maintain ~39% each. Sonova Holding AG attributes 37% (US 30%, Rest of Americas 7%). Amplifon S.p.A. derives 20.7%.

* EMEA: Amplifon S.p.A. operates with 64.9% regional dominance. Sonova Holding AG follows at 53%. Demant A/S holds 44%, with GN Store Nord A/S and Cochlear Limited ranging between ~34% and 40%, and WS Audiology A/S at 34%.

* APAC: GN Store Nord A/S records 21% of revenue from this region. Cochlear Limited holds 18.3%. WS Audiology A/S registers 17%. Amplifon S.p.A. derives 14.4%, Demant A/S 14% (Asia 9%, Pacific 5%), and Sonova Holding AG 10%.

Capital Allocation, Financial Engineering, and Balance Sheet Risk

The industry executed synchronized M&A and CapEx actions to secure vertical integration. Demant A/S allocated capital to acquire the KIND Group (~650 clinics) and the Ohrwerk Group, expanding its footprint to over 4,500 clinics globally. Amplifon S.p.A. deployed $70.3 million (€62.2 million) acquiring over 300 stores across Germany, Poland, France, Canada, and the US. Sonova Holding AG expanded its premium "World of Hearing" network to 70 global stores (within a ~3,600 total store footprint) and completed the bolt-on acquisition of digital tinnitus management app SilentCloud. Conversely, Demant A/S signed an agreement to divest its EPOS consumer audio unit, Sonova Holding AG announced the divestiture of its Consumer Hearing division, and GN Store Nord A/S sold its retail arm, Dansk HøreCenter, directly to Demant A/S.

These M&A strategies carry severe balance sheet implications, inflating total assets with Goodwill. Sonova Holding AG carries CHF 2,284.2 million in Goodwill against CHF 5,628.8 million in Total Assets (40.5% saturation) utilizing a 10.9% discount rate and a 2.1% terminal growth rate. GN Store Nord A/S carries DKK 10,813 million in Goodwill against DKK 29,226 million in assets (37.0%). WS Audiology A/S holds EUR 3,572 million in Goodwill out of EUR 4,291 million in total non-current assets, modeling a 9.0% pre-tax discount rate and 2.0% terminal growth. Amplifon S.p.A. applies WACC rates of 7.16% in EMEA, 9.42% in the Americas, and 7.38% in APAC, specifically disclosing that APAC impairment headroom has narrowed to just 2.0%.

Debt Mitigation and Cash Conversion Realities:

* Cochlear Limited: Reported Net Profit of $250.8 million, but operating cash flow (OCF) dropped to $153.2 million (38.8% conversion). This was driven by a $130.3 million (AUD 202 million) absorption into working capital, with inventory rising by $69.5 million (AUD 107.8 million) to a gross balance of AUD 499.4 million (+27.5%), driving DIO to 296.3 days. The company stretched Days Payable Outstanding (DPO) to 177.0 days, maintaining minimal debt (AUD 27.4 million drawn) against AUD 156.4 million in cash. DSO sits at 79.7 days, with a 199.0-day Cash Conversion Cycle (CCC).

* WS Audiology A/S: Generated $515.5 million (EUR 456 million) in EBITDA and $332.4 million (€294 million) in Free Cash Flow. However, WSA carries the highest leverage with Net Debt of EUR 2,807 million yielding a 6.15x Net Debt/EBITDA ratio and an interest coverage ratio below 1.0x (EBIT EUR 286 million vs. Interest EUR 309 million). The firm actively hedged 70% of its USD debt into EUR and JPY. Inventory stands at EUR 256 million, supported by EUR 40 million (15.6%) in obsolescence provisions.

* GN Store Nord A/S: Reported $364.5 million in EBITDA and $174.5 million in FCF. Leverage sits at 3.8x (down from a 7.1x peak) with Net Debt of DKK 8,876 million. The company successfully refinanced EUR 1,500 million to 2028/2030 maturities. GN’s earnings quality is impacted by aggressive R&D capitalization; of DKK 1,861 million in incurred R&D, DKK 1,034 million (~55%) was capitalized. Gross inventory rests at DKK 2,567 million with a DKK 253 million provision (9.8%).

* Demant A/S: Delivered $371.4 million in Net Profit, $839.6 million in EBITDA, and $604.4 million in OCF (72.0% conversion). Operating metrics reflect a 170.8-day DIO, 59.8-day DSO, 60.2-day DPO, and a 170.4-day CCC. The KIND acquisition spiked Net Debt/EBITDA to 3.4x, though interest coverage remains stable at 4.6x (EBIT DKK 3,832 million vs. Interest DKK 833 million). Management paused buybacks to target a 2.0x–2.5x deleverage within 18–24 months. Demant actively maintains DKK 192 million in expected product return provisions and defers DKK 685 million for extended warranties.

* Amplifon S.p.A.: Recorded $103.2 million in Net Profit, $578.4 million (EUR 511.6 million) in EBITDA, and $312.7 million in OCF (54.0% conversion). Net Debt of EUR 1,264 million yields a 2.47x leverage ratio and 3.2x interest coverage, with 72% of debt fixed or hedged.

* Sonova Holding AG: Maintains 1.1x leverage (Net Debt CHF 994.3 million against CHF 811.2 million EBITA) and incurred CHF 217.7 million in R&D expenses against CHF 3,605.9 million in revenue.

* Envoy Medical & JingHao Medical: Pre-commercial Envoy logged a -$23.7 million net loss, -$18.2 million in OCF, and a -$22.3 million operating loss off $0.24 million in revenue, driven by $12.5 million in R&D. JingHao generated $2.58 million in adjusted net profit off $42.8 million in revenue.

Infrastructure Layout, ESG Footprint, and Regional Moats

Corporate supply chains are actively executing "China-Plus-One" geographic strategies to hedge against tariff impositions. WS Audiology A/S relies on seven production sites (Denmark, Singapore, China, Mexico, Poland, the USA, the Philippines) and directed CapEx to establish a new commercial and production hub in Bangalore, India, supplementing its Hyderabad R&D center. Sonova Holding AG executes core operations in Switzerland, Asia, and Mexico. Demant A/S concentrates manufacturing in Poland and Mexico to serve EMEA and the Americas directly. Cochlear Limited operates six sites globally (Sweden, China, Malaysia, Australia) relying on "lifetime buys" of critical components. JingHao Medical deployed $700,000 USD to capitalize PT JINGHAO MEDICAL INDONESIA.

Environmental, Social, and Governance (ESG) execution relies heavily on freight optimization and device circularity:

* WS Audiology A/S: Achieved 100% renewable electricity globally, reducing Scope 1 & 2 emissions by 72% to 2,999 tCO2e. Scope 3 emissions stand at 421,514 tCO2e, supported by a 22% reduction in downstream transportation emissions through sea-freight shifts. SMETA 4 audits of 11 suppliers yielded 6% "critical" findings. The firm recycles 80% of non-hazardous waste.

* Sonova Holding AG: Reached 100% renewable electricity, logging Scope 1 & 2 emissions at 10,888 tCO2e (-68.7%). The firm instituted an internal carbon price of CHF 100 per tCO2e and reduced packaging weight by 4.9%. EcoVadis screening covers 81% of direct material spend (average score 58), triggering full assessments for seven high-risk suppliers alongside 75+ on-site facility visits.

* GN Store Nord A/S: Registered 4,603 tCO2e in Scope 1 & 2 emissions, securing a 26% drop in upstream transportation emissions. Circularity metrics show a massive 87% remanufacturing rate in its Malaysia facility (up from 65%), with 70% of product content classified as recyclable. RBA risk assessments cover 62% of manufacturing partners, supplemented by 86 audits across mainland China and Southeast Asia and an 86% EcoVadis onboarding rate.

* Demant A/S: Operates on 55% renewable electricity. Scope 1 & 2 emissions stand at 26,781 tCO2e (-16%), with Scope 3 at 194,976 tCO2e. The firm deployed 33 models of the "Demoflex" unit, capable of being reused by up to 50 patients to reduce clinic waste.

* Amplifon S.p.A.: Deployed $82.5 million (€73 million) in digital CapEx (Symphony CRM, OtoPad, Otokiosk) and mandated 100% of direct suppliers adopt its Supplier Code of Conduct, executing three on-site strategic audits.

* JingHao Medical: Following its 2024 acquisition of Intricon's hearing health business, the firm increased proprietary chip sales by 477.45% to $2.84 million, prepping a Gen 2 Bluetooth release for 2026.

Technological Pipelines, Legal Liabilities, and the Demographics Paradox

Demographic projections anchor the industry's structural floor; the WHO projects the current 1.5 to 1.75 billion hearing loss cohort will reach 2.5 billion by 2050. Global adoption remains under 20%, plummeting below 5% for high-acuity needs and in mainland China. Direct-to-Consumer (DTC) marketing actively drives top-of-funnel conversion; Cochlear Limited generates 30% of US surgeries via DTC channels, while Amplifon S.p.A. utilized digital pipelines to drive a 22% increase in online bookings, offering diagnostic tests that yielded $464.7 million (€411 million) in savings to prospective clients.

Technology R&D pipelines focus on neural processing and implantable upgrades. Sonova Holding AG deployed the AI-powered Infinio platform and Virto R Infinio. Demant A/S plans the H1 2026 rollout of Oticon Zeal, following the Q1 2026 launch of Oticon Verit and Oticon Play SI. WS Audiology A/S launched the Widex Allure (utilizing the W1 chip), Widex Compass Cloud, Signia IX, Pure Charge&Go BCT IX, Insio custom CIC, and Motion Charge&GO IX. GN Store Nord A/S introduced the ReSound Vivia, ReSound Enzo IA, and ReSound Savi. In the implantable segment, Cochlear Limited launched the Nucleus Nexa System, Nucleus Kanso 3 Nexa, and Baha 7. Envoy Medical completed enrollment for the Acclaim CI pivotal trial, targeting FDA Premarket Approval by late 2027 or 2028.

However, cross-licensing and regulatory legalities continue to erode margins. Sonova Holding AG absorbed $33.95 million (CHF 28.2 million) in legal and settlement fees to resolve an October 2018 patent dispute with MED-EL. Furthermore, Sonova initiated three field actions (affecting one sound processor model via two units and two accessories) and incurred a non-cash expense of $28.41 million (CHF 23.6 million) to reassess a legacy CI product liability provision. Cochlear Limited continues to incur defense costs for the September 2011 CI500 recall. Envoy Medical faces a $9.4 million lawsuit (plus interest and fees) from Atlas Merchant Capital regarding SPAC redemption disputes. Demant A/S reported zero product recalls.

HDIN Institutional Verdict

Capital allocation across the FY2025/2026 hearing care continuum is fundamentally a defensive maneuver against irreversible policy pressures. While management teams routinely cite the WHO’s 2.5 billion demographic tailwinds, unit growth remains entirely decoupled from margin expansion due to the monopsony pricing power of mainland China’s VBP and the US Managed Care structure. Premium operators are forcibly executing CapEx-heavy vertical integration strategies—evidenced by Demant A/S securing 4,500+ clinics and Amplifon S.p.A. deploying €62.2 million in retail roll-ups—because hardware differentiation alone can no longer protect the Average Selling Price (ASP). Simultaneously, diverging working capital disciplines—highlighted by Cochlear Limited's 296.3 DIO defensive stockpile contrasting with WS Audiology A/S's highly leveraged 6.15x balance sheet—expose exactly which operators possess the free cash flow resilience required to weather the convergence of medical and consumer audio.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Divergent Cash Conversion Realities: Demant A/S converted 72.0% of its $839.6 million EBITDA into operating cash flow via retail efficiency, while Cochlear Limited’s cash conversion lagged at 38.8% due to a $130.3 million working capital absorption, pushing Days Inventory Outstanding (DIO) to 296.3 days.

* Aggressive Supply Chain Redundancy: Geopolitical friction triggered rapid near-shoring and multi-hub CapEx; GN Store Nord A/S relocated 31 production lines out of mainland China, while Sonova Holding AG shifted custom in-the-ear manufacturing from Vietnam to Alicante, Spain within 3.5 months.

* Structural Margin Ceilings: Despite World Health Organization (WHO) projections of a 2.5 billion patient pool by 2050, institutional monopsonies—specifically Volume-Based Procurement (VBP) in mainland China and US Managed Care consolidation—are systematically compressing average selling prices (ASP), forcing incumbents to acquire retail networks to protect end-to-end margins.

Figure Clobal Hearing Healthcare Landscape 2025: A Cross-Peer Benchmarking Matrix

Segmental Realities and Margin CompressionThe FY2025 financial disclosures delineate a sector experiencing stable structural demand but acute variations in organic top-line growth and earnings quality due to foreign exchange (FX) headwinds and macroeconomic softness.

Table FY2025 Normalized Revenue & Operating Matrix (USD)

| Corporate Entity | FY2025 Revenue | Organic Growth | FX/Perimeter Impact | Operating Profit Margin |

| Sonova Holding AG [SWX: SOON] | $4,341.8 M | +5.4% | FX: -6.1% | 22.5% (Norm. EBITA) |

| Demant A/S [CPH: DEMANT] | $3,604.5 M | +2.0% | FX: -2.0% | 17.2% (EBIT b4 special) |

| WS Audiology A/S (WSA) | $2,915.8 M | 0.0% | FX: N/A | 17.7% (Adj. EBITDA) |

| Amplifon S.p.A. [BIT: AMP] | $2,708.6 M | ~0.0% | FX: -2.3%, M&A: +1.7% | 8.2% (EBIT) |

| GN Store Nord A/S [CPH: GN] | $2,633.3 M | -4.0%* | FX: -3.0% | 11.4% (EBITA) |

| Cochlear Limited [ASX: COH] | $1,519.5 M | +3.0% (CC) | FX: -1.0% | 22.1% (EBIT) |

| JingHao Medical | $42.8 M | +65.27% | N/A | ~6.0% (Net Profit) |

| Envoy Medical [NASDAQ: COCH] | $0.24 M | +7.1% | N/A | N/A (Op. Loss: -$22.3M) |

Labor productivity is structurally dictated by the chosen operating channel. Automated business-to-business (B2B) models lead per-capita revenue generation. GN Store Nord A/S operates with 7,500+ employees, generating ~$351,100 per employee, followed by Cochlear Limited (~5,500 headcount; ~$276,200), WS Audiology A/S (~12,000 headcount; ~$243,000), and Sonova Holding AG (>18,000 headcount; ~$235,300). Conversely, vertically integrated and pure-play retail models inherently dilute labor productivity in exchange for direct patient access. Demant A/S employs ~22,719 staff globally yielding ~$158,600 per capita, while Amplifon S.p.A. operates with 20,900 employees yielding ~$129,600.

Segment breakdowns highlight severe differences in revenue concentration. Sonova Holding AG derives 93% of revenue from Hearing Instruments (split 56% Wholesale, 44% Retail via AudioNova) and 7% from Cochlear Implants. Demant A/S balances 43% Hearing Aids (Wholesale), 47% Hearing Care (Retail), and 10% Diagnostics (Interacoustics/GSI). GN Store Nord A/S relies on Hearing (ReSound) for only 43% of its top line, with the remaining 57% derived from Enterprise Audio (Jabra: 41%) and Gaming (SteelSeries: 16%). Cochlear Limited maintains a split of 62% Cochlear Implants, 26% Services, and 12% Acoustics. Amplifon S.p.A. remains 100% pure-play retail, while JingHao Medical focuses strictly on wholesale Direct-to-Consumer (DTC) Original Design Manufacturing (ODM).

Geographic exposures dictate regional reimbursement vulnerabilities:

* Americas: WS Audiology A/S reports 49% concentration. Cochlear Limited holds 48.5%. Demant A/S and GN Store Nord A/S maintain ~39% each. Sonova Holding AG attributes 37% (US 30%, Rest of Americas 7%). Amplifon S.p.A. derives 20.7%.

* EMEA: Amplifon S.p.A. operates with 64.9% regional dominance. Sonova Holding AG follows at 53%. Demant A/S holds 44%, with GN Store Nord A/S and Cochlear Limited ranging between ~34% and 40%, and WS Audiology A/S at 34%.

* APAC: GN Store Nord A/S records 21% of revenue from this region. Cochlear Limited holds 18.3%. WS Audiology A/S registers 17%. Amplifon S.p.A. derives 14.4%, Demant A/S 14% (Asia 9%, Pacific 5%), and Sonova Holding AG 10%.

Capital Allocation, Financial Engineering, and Balance Sheet Risk

The industry executed synchronized M&A and CapEx actions to secure vertical integration. Demant A/S allocated capital to acquire the KIND Group (~650 clinics) and the Ohrwerk Group, expanding its footprint to over 4,500 clinics globally. Amplifon S.p.A. deployed $70.3 million (€62.2 million) acquiring over 300 stores across Germany, Poland, France, Canada, and the US. Sonova Holding AG expanded its premium "World of Hearing" network to 70 global stores (within a ~3,600 total store footprint) and completed the bolt-on acquisition of digital tinnitus management app SilentCloud. Conversely, Demant A/S signed an agreement to divest its EPOS consumer audio unit, Sonova Holding AG announced the divestiture of its Consumer Hearing division, and GN Store Nord A/S sold its retail arm, Dansk HøreCenter, directly to Demant A/S.

These M&A strategies carry severe balance sheet implications, inflating total assets with Goodwill. Sonova Holding AG carries CHF 2,284.2 million in Goodwill against CHF 5,628.8 million in Total Assets (40.5% saturation) utilizing a 10.9% discount rate and a 2.1% terminal growth rate. GN Store Nord A/S carries DKK 10,813 million in Goodwill against DKK 29,226 million in assets (37.0%). WS Audiology A/S holds EUR 3,572 million in Goodwill out of EUR 4,291 million in total non-current assets, modeling a 9.0% pre-tax discount rate and 2.0% terminal growth. Amplifon S.p.A. applies WACC rates of 7.16% in EMEA, 9.42% in the Americas, and 7.38% in APAC, specifically disclosing that APAC impairment headroom has narrowed to just 2.0%.

Debt Mitigation and Cash Conversion Realities:

* Cochlear Limited: Reported Net Profit of $250.8 million, but operating cash flow (OCF) dropped to $153.2 million (38.8% conversion). This was driven by a $130.3 million (AUD 202 million) absorption into working capital, with inventory rising by $69.5 million (AUD 107.8 million) to a gross balance of AUD 499.4 million (+27.5%), driving DIO to 296.3 days. The company stretched Days Payable Outstanding (DPO) to 177.0 days, maintaining minimal debt (AUD 27.4 million drawn) against AUD 156.4 million in cash. DSO sits at 79.7 days, with a 199.0-day Cash Conversion Cycle (CCC).

* WS Audiology A/S: Generated $515.5 million (EUR 456 million) in EBITDA and $332.4 million (€294 million) in Free Cash Flow. However, WSA carries the highest leverage with Net Debt of EUR 2,807 million yielding a 6.15x Net Debt/EBITDA ratio and an interest coverage ratio below 1.0x (EBIT EUR 286 million vs. Interest EUR 309 million). The firm actively hedged 70% of its USD debt into EUR and JPY. Inventory stands at EUR 256 million, supported by EUR 40 million (15.6%) in obsolescence provisions.

* GN Store Nord A/S: Reported $364.5 million in EBITDA and $174.5 million in FCF. Leverage sits at 3.8x (down from a 7.1x peak) with Net Debt of DKK 8,876 million. The company successfully refinanced EUR 1,500 million to 2028/2030 maturities. GN’s earnings quality is impacted by aggressive R&D capitalization; of DKK 1,861 million in incurred R&D, DKK 1,034 million (~55%) was capitalized. Gross inventory rests at DKK 2,567 million with a DKK 253 million provision (9.8%).

* Demant A/S: Delivered $371.4 million in Net Profit, $839.6 million in EBITDA, and $604.4 million in OCF (72.0% conversion). Operating metrics reflect a 170.8-day DIO, 59.8-day DSO, 60.2-day DPO, and a 170.4-day CCC. The KIND acquisition spiked Net Debt/EBITDA to 3.4x, though interest coverage remains stable at 4.6x (EBIT DKK 3,832 million vs. Interest DKK 833 million). Management paused buybacks to target a 2.0x–2.5x deleverage within 18–24 months. Demant actively maintains DKK 192 million in expected product return provisions and defers DKK 685 million for extended warranties.

* Amplifon S.p.A.: Recorded $103.2 million in Net Profit, $578.4 million (EUR 511.6 million) in EBITDA, and $312.7 million in OCF (54.0% conversion). Net Debt of EUR 1,264 million yields a 2.47x leverage ratio and 3.2x interest coverage, with 72% of debt fixed or hedged.

* Sonova Holding AG: Maintains 1.1x leverage (Net Debt CHF 994.3 million against CHF 811.2 million EBITA) and incurred CHF 217.7 million in R&D expenses against CHF 3,605.9 million in revenue.

* Envoy Medical & JingHao Medical: Pre-commercial Envoy logged a -$23.7 million net loss, -$18.2 million in OCF, and a -$22.3 million operating loss off $0.24 million in revenue, driven by $12.5 million in R&D. JingHao generated $2.58 million in adjusted net profit off $42.8 million in revenue.

Infrastructure Layout, ESG Footprint, and Regional Moats

Corporate supply chains are actively executing "China-Plus-One" geographic strategies to hedge against tariff impositions. WS Audiology A/S relies on seven production sites (Denmark, Singapore, China, Mexico, Poland, the USA, the Philippines) and directed CapEx to establish a new commercial and production hub in Bangalore, India, supplementing its Hyderabad R&D center. Sonova Holding AG executes core operations in Switzerland, Asia, and Mexico. Demant A/S concentrates manufacturing in Poland and Mexico to serve EMEA and the Americas directly. Cochlear Limited operates six sites globally (Sweden, China, Malaysia, Australia) relying on "lifetime buys" of critical components. JingHao Medical deployed $700,000 USD to capitalize PT JINGHAO MEDICAL INDONESIA.

Environmental, Social, and Governance (ESG) execution relies heavily on freight optimization and device circularity:

* WS Audiology A/S: Achieved 100% renewable electricity globally, reducing Scope 1 & 2 emissions by 72% to 2,999 tCO2e. Scope 3 emissions stand at 421,514 tCO2e, supported by a 22% reduction in downstream transportation emissions through sea-freight shifts. SMETA 4 audits of 11 suppliers yielded 6% "critical" findings. The firm recycles 80% of non-hazardous waste.

* Sonova Holding AG: Reached 100% renewable electricity, logging Scope 1 & 2 emissions at 10,888 tCO2e (-68.7%). The firm instituted an internal carbon price of CHF 100 per tCO2e and reduced packaging weight by 4.9%. EcoVadis screening covers 81% of direct material spend (average score 58), triggering full assessments for seven high-risk suppliers alongside 75+ on-site facility visits.

* GN Store Nord A/S: Registered 4,603 tCO2e in Scope 1 & 2 emissions, securing a 26% drop in upstream transportation emissions. Circularity metrics show a massive 87% remanufacturing rate in its Malaysia facility (up from 65%), with 70% of product content classified as recyclable. RBA risk assessments cover 62% of manufacturing partners, supplemented by 86 audits across mainland China and Southeast Asia and an 86% EcoVadis onboarding rate.

* Demant A/S: Operates on 55% renewable electricity. Scope 1 & 2 emissions stand at 26,781 tCO2e (-16%), with Scope 3 at 194,976 tCO2e. The firm deployed 33 models of the "Demoflex" unit, capable of being reused by up to 50 patients to reduce clinic waste.

* Amplifon S.p.A.: Deployed $82.5 million (€73 million) in digital CapEx (Symphony CRM, OtoPad, Otokiosk) and mandated 100% of direct suppliers adopt its Supplier Code of Conduct, executing three on-site strategic audits.

* JingHao Medical: Following its 2024 acquisition of Intricon's hearing health business, the firm increased proprietary chip sales by 477.45% to $2.84 million, prepping a Gen 2 Bluetooth release for 2026.

Technological Pipelines, Legal Liabilities, and the Demographics Paradox

Demographic projections anchor the industry's structural floor; the WHO projects the current 1.5 to 1.75 billion hearing loss cohort will reach 2.5 billion by 2050. Global adoption remains under 20%, plummeting below 5% for high-acuity needs and in mainland China. Direct-to-Consumer (DTC) marketing actively drives top-of-funnel conversion; Cochlear Limited generates 30% of US surgeries via DTC channels, while Amplifon S.p.A. utilized digital pipelines to drive a 22% increase in online bookings, offering diagnostic tests that yielded $464.7 million (€411 million) in savings to prospective clients.

Technology R&D pipelines focus on neural processing and implantable upgrades. Sonova Holding AG deployed the AI-powered Infinio platform and Virto R Infinio. Demant A/S plans the H1 2026 rollout of Oticon Zeal, following the Q1 2026 launch of Oticon Verit and Oticon Play SI. WS Audiology A/S launched the Widex Allure (utilizing the W1 chip), Widex Compass Cloud, Signia IX, Pure Charge&Go BCT IX, Insio custom CIC, and Motion Charge&GO IX. GN Store Nord A/S introduced the ReSound Vivia, ReSound Enzo IA, and ReSound Savi. In the implantable segment, Cochlear Limited launched the Nucleus Nexa System, Nucleus Kanso 3 Nexa, and Baha 7. Envoy Medical completed enrollment for the Acclaim CI pivotal trial, targeting FDA Premarket Approval by late 2027 or 2028.

However, cross-licensing and regulatory legalities continue to erode margins. Sonova Holding AG absorbed $33.95 million (CHF 28.2 million) in legal and settlement fees to resolve an October 2018 patent dispute with MED-EL. Furthermore, Sonova initiated three field actions (affecting one sound processor model via two units and two accessories) and incurred a non-cash expense of $28.41 million (CHF 23.6 million) to reassess a legacy CI product liability provision. Cochlear Limited continues to incur defense costs for the September 2011 CI500 recall. Envoy Medical faces a $9.4 million lawsuit (plus interest and fees) from Atlas Merchant Capital regarding SPAC redemption disputes. Demant A/S reported zero product recalls.

HDIN Institutional Verdict

Capital allocation across the FY2025/2026 hearing care continuum is fundamentally a defensive maneuver against irreversible policy pressures. While management teams routinely cite the WHO’s 2.5 billion demographic tailwinds, unit growth remains entirely decoupled from margin expansion due to the monopsony pricing power of mainland China’s VBP and the US Managed Care structure. Premium operators are forcibly executing CapEx-heavy vertical integration strategies—evidenced by Demant A/S securing 4,500+ clinics and Amplifon S.p.A. deploying €62.2 million in retail roll-ups—because hardware differentiation alone can no longer protect the Average Selling Price (ASP). Simultaneously, diverging working capital disciplines—highlighted by Cochlear Limited's 296.3 DIO defensive stockpile contrasting with WS Audiology A/S's highly leveraged 6.15x balance sheet—expose exactly which operators possess the free cash flow resilience required to weather the convergence of medical and consumer audio.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."