UBE Corporation: North American C1 Electrolyte Expansion and Legacy Divestitures Near Louisiana and Thailand as 5.0% Operating Profit Expansion Signals De-commoditization Realization

Date : 2026-06-23

Reading : 127

HDIN Executive Takeaways

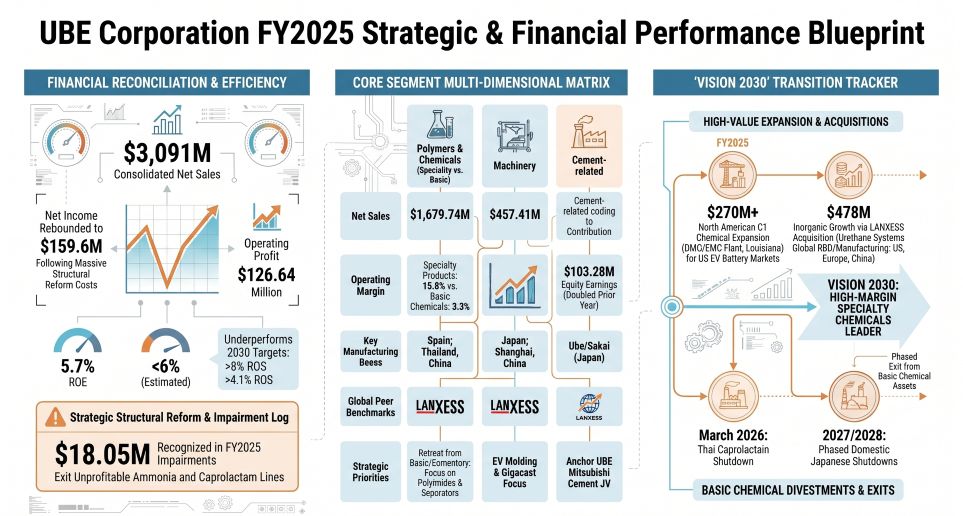

* Consolidated top-line contracted 5.0% to $3,091.18M due to structural legacy divestitures, yet operating profit expanded 5.0% to $126.64M via reduced depreciation following $194.42M in prior-year impairments.

* Capital is pivoting geographically from Asian basic chemicals (halting Rayong, Thailand operations by 2026) toward North America, highlighted by a $270M+ C1 chemical electrolyte facility in Louisiana.

* Institutional risk transitions from physical stranded assets to intangible valuation, with goodwill surging to $215.60M following the $478.25M LANXESS Urethane Systems acquisition, necessitating rigorous ROIC governance.

Figure UBE Corporation FY2025 $trategic & Financial Performance Blueprint

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

UBE Corporation [TYO: 4208] reported a consolidated net sales contraction of 5.0% year-over-year to $3,091.18 million (¥462,343 million). Despite top-line deterioration, operating profit expanded 5.0% to $126.64 million (¥18,941 million), and net income rebounded to $159.61 million (¥23,872 million). This divergence was driven by the cessation of a biennial maintenance shutdown at the domestic ammonia plant, favorable JPY depreciation, and a sharp reduction in structural reform costs following the prior year's $194.42 million (¥29,079 million) impairment sweep.

Management missed its initial Return on Equity (ROE) target of 6.8%, recording 5.7%, and its Return on Sales (ROS) target of 5.1%, posting 4.1%. Operating cash flow reached $401.05 million (¥59,984 million), representing a year-over-year expansion of $161.44 million. However, aggressive capital reallocation drove an investing cash outflow of $937.58 million (¥140,232 million)—comprising $461.38 million (¥69,008 million) in CapEx and $478.25 million (¥71,532 million) for the acquisition of LANXESS Urethane Systems subsidiaries. This resulted in a deeply negative Free Cash Flow of -$536.53 million, bridged by financing cash flows of $87.10 million (¥13,027 million). Consequently, interest-bearing debt increased 8.4% to $2,394.70 million (¥358,172 million), holding the equity ratio at 46.2%. The firm maintained a dividend payout of ¥110 per share ($71.43 million / ¥10,684 million) while limiting share buybacks to $0.04 million (¥6 million).

Consolidated Segmental Financials (FY2025)

* Polymers & Chemicals: Revenue $1,679.74 million (¥251,237 million), down 8.2% YoY. Operating Profit $54.75 million (¥8,189 million). Production Value $1,707.12 million (¥255,331 million).

* Machinery: Revenue $457.41 million (¥68,414 million), down 21.3% YoY. Operating Profit $41.73 million (¥6,242 million). Production Value $405.01 million (¥60,576 million).

* Specialty Products: Revenue $413.86 million (¥61,900 million), down 6.4% YoY. Operating Profit $65.24 million (¥9,758 million). Production Value $403.41 million (¥60,338 million).

* High-Performance Polyurethane: Revenue $311.22 million (¥46,549 million), up 198.1% YoY. Operating Loss -$3.66 million (-¥548 million). Production Value $302.55 million (¥45,252 million).

* Pharmaceuticals: Revenue $140.43 million (¥21,004 million), down 33.3% YoY. Operating Loss -$8.39 million (-¥1,255 million). Production Value $95.24 million (¥14,245 million).

* Others: Revenue $230.55 million (¥34,483 million). Operating Profit $12.81 million (¥1,916 million).

Balance Sheet De-risking and Intangible Asset Inflation

The company recorded an additional $18.05 million (¥2,699 million) in fixed asset impairments. This targeted 1,6-Hexanediol machinery in Thailand ($9.83 million / ¥1,471 million), Japanese ammonia/caprolactam infrastructure ($4.82 million / ¥721 million), Thai caprolactam facilities ($2.73 million / ¥409 million), Japanese polyimide equipment ($0.50 million / ¥75 million), hydrogen peroxide assets ($0.15 million / ¥22 million), and composites in Koriyama ($0.01 million / ¥1 million). Special losses regarding business withdrawals totaled $24.47 million (¥3,660 million), encompassing $16.29 million (¥2,437 million) in severance and $8.18 million (¥1,223 million) in withdrawal losses. Conversely, corporate goodwill surged to $215.60 million (¥32,247 million)—up from $13.38 million—with the LANXESS integration accounting for $200.41 million (¥29,976 million) alongside $88.61 million (¥13,254 million) in newly injected customer-related intangibles.

Infrastructure Layout and Regional Moats

UBE Corporation is shifting to a five-pole global management structure (Japan, Asia, Europe, Americas, China). Consolidated geographic revenue dependency is mapped as follows: Japan $1,377.65 million (¥206,053 million); Asia $853.65 million (¥127,679 million); Europe $450.31 million (¥67,352 million); North America $287.03 million (¥42,930 million); and Other Regions $121.11 million (¥18,115 million).

The industrial supply chain relies heavily on upstream integration, with gross inter-segment sales totaling $142.03 million (¥21,244 million). The Polymers & Chemicals division acted as the foundational feedstock provider, generating $152.56 million (¥22,818 million) in internal transfers (9.1% of segment gross), feeding downstream divisions like Specialty Products, which generated $73.34 million (¥10,970 million) internally.

Global Industrial Expansion & Retrenchment Strategies

* The Americas: Capitalizing on localized EV supply chains, UBE Corporation is executing a $270+ million capital injection to construct a C1 chemicals facility (dimethyl carbonate and ethyl methyl carbonate) in Louisiana under UBE C1 Chemicals America, Inc. Additional footprint includes UBE Engineered Composites in Indiana and UBE Urethanes USA LLC in North Carolina.

* Asian Retrenchment: Structural oversupply has prompted an accelerated withdrawal from traditional basic chemicals. UBE Chemicals (Asia) Public Company Limited in Rayong, Thailand, will fully halt ammonia, caprolactam, and nylon polymer operations by March 2026. Domestic basic chemical equivalents in Ube City, Japan, will cease operations between 2027 and 2028. Operations in China remain active via UBE Urethanes Nantong Co., Ltd. and UBE Machinery in Shanghai, alongside Taiwan UBE.

* Europe: Operations are anchored by UBE Corporation Europe S.A.U. in Spain, now heavily augmented by the newly integrated LANXESS R&D and manufacturing hubs spanning Germany, the UK, Italy, and the Netherlands.

* Ecosystem Divestitures: Management removed the drag of the Machinery segment's steelmaking business by transferring UBE Steel Co., Ltd. for $3.10 million (¥463 million). This decoupled $45.81 million (¥6,852 million) in current assets and $26.81 million (¥4,010 million) in fixed assets against the transfer of -$44.83 million (△¥6,705 million) in current liabilities and -$1.92M (△¥287 million) in fixed liabilities, resulting in a net cash outflow of -$4.65 million (△¥695 million) and finalizing a prior year special loss of -$19.41 million (△¥2,903 million). The Malaysian elastomer joint venture, LOTTE UBE SYNTHETIC RUBBER SDN. BHD., was dissolved, extinguishing $0.01 million (¥2 million) in guarantee obligations.

* The Cement Anchor: UBE Mitsubishi Cement Corporation, a 50/50 joint venture, operates as the primary non-operating earnings driver. The JV holds total assets of $5,655.40 million (¥845,870 million) and net assets of $2,875.18 million (¥430,037 million). It produced sales of $3,599.41 million (¥538,359 million) and net income of $169.31 million (¥25,323 million). This directly yielded $103.28 million (¥15,448 million) in equity earnings for UBE Corporation (up from $51.09 million), catalyzing a $101.20 million (¥15,137 million) surge in consolidated ordinary profit. However, it also enforces an operational dependency, supplying $184.23 million (¥27,555 million) in coal to fuel UBE Corporation's in-house 145,000 kW power plant.

Strategic Execution and Intellectual Property

R&D expenditure totaled $83.12 million (¥12,432 million), aligning with a target to reach $\ge$4.0% of sales by 2030, with external R&D ratios mandated at 80% and joint patent applications at 30%. Segment allocations reflect the de-commoditization pivot: Pharmaceuticals received $20.44 million (¥3,057 million); Corporate cross-segment seeds received $18.83 million (¥2,816 million); Specialty Products $15.42 million (¥2,306 million); High-Performance Polyurethane $13.88 million (¥2,076 million); Polymers & Chemicals $10.76 million (¥1,610 million); and Machinery $3.79 million (¥567 million).

Intellectual property commercialization is actively pursued via continuous chemical process licensing. C1 chemical technologies are currently licensed to Chinese entities including Shaanxi Coal Group, Xinjiang Tianye Group, and HighChem Co., Ltd. Within Pharmaceuticals, the compound UD-051 (jointly discovered with Kumamoto University) was licensed globally to GALTS Pharma, while oncology drug discovery is advancing via a joint venture with Zeureka Inc.

To mitigate fossil-fuel surcharge exposures slated for FY2028, UBE Corporation aims to achieve >60% of sales from Environmentally Contributing Products by 2030. By accelerating the shutdown of legacy basic chemical facilities, the company will artificially secure a 65% reduction in GHG emissions (compared to 2013 levels) by 2028. Outstanding operational risk hedges include $55.84 million (¥8.35 billion) in currency derivatives and 16 pending asbestos litigation cases against Ube Board Co., Ltd., presenting maximum collective claims of $55.49 million (¥8.3 billion).

HDIN Institutional Verdict

UBE Corporation is navigating a volatile capital transition. Executive leadership explicitly acknowledged missing the initial FY2025 revenue target of $3,276.09 million (¥490 billion) and operating profit target of $167.15 million (¥25 billion), though ordinary profit perfectly aligned with the $250.72 million (¥37.5 billion) projection by achieving $250.76 million (¥37.5 billion).

The medium-term execution relies strictly on balancing transitional friction. The FY2026 plan sets revenue at $3,643.81 million (¥545 billion) and operating profit at $213.95 million (¥32 billion), moving to an identical top-line but an optimized operating profit of $267.44 million (¥40 billion) in FY2027. By 2030, UBE Corporation mandates $3,677.24 million (¥550 billion) in sales, $401.15 million (¥60 billion) in operating profit, EBITDA beyond $668.59 million (¥100 billion), an ROIC more than 6%, ROE more than 8%, and ROS more than 10%.

This requires deploying an available capital pool of $5,014.42 million (¥750 billion) through 2030, explicitly funneling $2,172.92 million (¥325 billion) into CapEx and $902.59 million (¥135 billion) into M&A. To insulate the equity base, $668.59 million (¥100 billion) is reserved for shareholder returns governed by an expanded Dividend on Equity (DOE) target of $\ge$3.5% (aiming for 4.0%).

The internal governance apparatus driving this features a 10-member board (5 independent). Female board representation sits at 10% (1 director) but is scheduled to scale to 25% (3 of 12 members) by 2026. Environmental and human capital KPIs (17.3% female workforce, 5.5% female managers, 36.6% male childcare leave) strictly dictate 10% of executive compensation.

HDIN views the fundamental margin expansion narrative as entirely dependent on successfully decoupling the internal supply chain from the Japanese and Thai commodity assets currently scheduled for shutdown. The balance sheet carries high execution risk due to the sudden injection of LANXESS-derived goodwill; if post-merger integration fails to yield target cash flows within the Urethane division, impairment risks will rapidly resurface. In the interim, UBE Mitsubishi Cement Corporation remains the critical, highly profitable anchor masking core segmental transition weakness.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Consolidated top-line contracted 5.0% to $3,091.18M due to structural legacy divestitures, yet operating profit expanded 5.0% to $126.64M via reduced depreciation following $194.42M in prior-year impairments.

* Capital is pivoting geographically from Asian basic chemicals (halting Rayong, Thailand operations by 2026) toward North America, highlighted by a $270M+ C1 chemical electrolyte facility in Louisiana.

* Institutional risk transitions from physical stranded assets to intangible valuation, with goodwill surging to $215.60M following the $478.25M LANXESS Urethane Systems acquisition, necessitating rigorous ROIC governance.

Figure UBE Corporation FY2025 $trategic & Financial Performance Blueprint

Segmental Realities and Margin CompressionUBE Corporation [TYO: 4208] reported a consolidated net sales contraction of 5.0% year-over-year to $3,091.18 million (¥462,343 million). Despite top-line deterioration, operating profit expanded 5.0% to $126.64 million (¥18,941 million), and net income rebounded to $159.61 million (¥23,872 million). This divergence was driven by the cessation of a biennial maintenance shutdown at the domestic ammonia plant, favorable JPY depreciation, and a sharp reduction in structural reform costs following the prior year's $194.42 million (¥29,079 million) impairment sweep.

Management missed its initial Return on Equity (ROE) target of 6.8%, recording 5.7%, and its Return on Sales (ROS) target of 5.1%, posting 4.1%. Operating cash flow reached $401.05 million (¥59,984 million), representing a year-over-year expansion of $161.44 million. However, aggressive capital reallocation drove an investing cash outflow of $937.58 million (¥140,232 million)—comprising $461.38 million (¥69,008 million) in CapEx and $478.25 million (¥71,532 million) for the acquisition of LANXESS Urethane Systems subsidiaries. This resulted in a deeply negative Free Cash Flow of -$536.53 million, bridged by financing cash flows of $87.10 million (¥13,027 million). Consequently, interest-bearing debt increased 8.4% to $2,394.70 million (¥358,172 million), holding the equity ratio at 46.2%. The firm maintained a dividend payout of ¥110 per share ($71.43 million / ¥10,684 million) while limiting share buybacks to $0.04 million (¥6 million).

Consolidated Segmental Financials (FY2025)

* Polymers & Chemicals: Revenue $1,679.74 million (¥251,237 million), down 8.2% YoY. Operating Profit $54.75 million (¥8,189 million). Production Value $1,707.12 million (¥255,331 million).

* Machinery: Revenue $457.41 million (¥68,414 million), down 21.3% YoY. Operating Profit $41.73 million (¥6,242 million). Production Value $405.01 million (¥60,576 million).

* Specialty Products: Revenue $413.86 million (¥61,900 million), down 6.4% YoY. Operating Profit $65.24 million (¥9,758 million). Production Value $403.41 million (¥60,338 million).

* High-Performance Polyurethane: Revenue $311.22 million (¥46,549 million), up 198.1% YoY. Operating Loss -$3.66 million (-¥548 million). Production Value $302.55 million (¥45,252 million).

* Pharmaceuticals: Revenue $140.43 million (¥21,004 million), down 33.3% YoY. Operating Loss -$8.39 million (-¥1,255 million). Production Value $95.24 million (¥14,245 million).

* Others: Revenue $230.55 million (¥34,483 million). Operating Profit $12.81 million (¥1,916 million).

Balance Sheet De-risking and Intangible Asset Inflation

The company recorded an additional $18.05 million (¥2,699 million) in fixed asset impairments. This targeted 1,6-Hexanediol machinery in Thailand ($9.83 million / ¥1,471 million), Japanese ammonia/caprolactam infrastructure ($4.82 million / ¥721 million), Thai caprolactam facilities ($2.73 million / ¥409 million), Japanese polyimide equipment ($0.50 million / ¥75 million), hydrogen peroxide assets ($0.15 million / ¥22 million), and composites in Koriyama ($0.01 million / ¥1 million). Special losses regarding business withdrawals totaled $24.47 million (¥3,660 million), encompassing $16.29 million (¥2,437 million) in severance and $8.18 million (¥1,223 million) in withdrawal losses. Conversely, corporate goodwill surged to $215.60 million (¥32,247 million)—up from $13.38 million—with the LANXESS integration accounting for $200.41 million (¥29,976 million) alongside $88.61 million (¥13,254 million) in newly injected customer-related intangibles.

Infrastructure Layout and Regional Moats

UBE Corporation is shifting to a five-pole global management structure (Japan, Asia, Europe, Americas, China). Consolidated geographic revenue dependency is mapped as follows: Japan $1,377.65 million (¥206,053 million); Asia $853.65 million (¥127,679 million); Europe $450.31 million (¥67,352 million); North America $287.03 million (¥42,930 million); and Other Regions $121.11 million (¥18,115 million).

The industrial supply chain relies heavily on upstream integration, with gross inter-segment sales totaling $142.03 million (¥21,244 million). The Polymers & Chemicals division acted as the foundational feedstock provider, generating $152.56 million (¥22,818 million) in internal transfers (9.1% of segment gross), feeding downstream divisions like Specialty Products, which generated $73.34 million (¥10,970 million) internally.

Global Industrial Expansion & Retrenchment Strategies

* The Americas: Capitalizing on localized EV supply chains, UBE Corporation is executing a $270+ million capital injection to construct a C1 chemicals facility (dimethyl carbonate and ethyl methyl carbonate) in Louisiana under UBE C1 Chemicals America, Inc. Additional footprint includes UBE Engineered Composites in Indiana and UBE Urethanes USA LLC in North Carolina.

* Asian Retrenchment: Structural oversupply has prompted an accelerated withdrawal from traditional basic chemicals. UBE Chemicals (Asia) Public Company Limited in Rayong, Thailand, will fully halt ammonia, caprolactam, and nylon polymer operations by March 2026. Domestic basic chemical equivalents in Ube City, Japan, will cease operations between 2027 and 2028. Operations in China remain active via UBE Urethanes Nantong Co., Ltd. and UBE Machinery in Shanghai, alongside Taiwan UBE.

* Europe: Operations are anchored by UBE Corporation Europe S.A.U. in Spain, now heavily augmented by the newly integrated LANXESS R&D and manufacturing hubs spanning Germany, the UK, Italy, and the Netherlands.

* Ecosystem Divestitures: Management removed the drag of the Machinery segment's steelmaking business by transferring UBE Steel Co., Ltd. for $3.10 million (¥463 million). This decoupled $45.81 million (¥6,852 million) in current assets and $26.81 million (¥4,010 million) in fixed assets against the transfer of -$44.83 million (△¥6,705 million) in current liabilities and -$1.92M (△¥287 million) in fixed liabilities, resulting in a net cash outflow of -$4.65 million (△¥695 million) and finalizing a prior year special loss of -$19.41 million (△¥2,903 million). The Malaysian elastomer joint venture, LOTTE UBE SYNTHETIC RUBBER SDN. BHD., was dissolved, extinguishing $0.01 million (¥2 million) in guarantee obligations.

* The Cement Anchor: UBE Mitsubishi Cement Corporation, a 50/50 joint venture, operates as the primary non-operating earnings driver. The JV holds total assets of $5,655.40 million (¥845,870 million) and net assets of $2,875.18 million (¥430,037 million). It produced sales of $3,599.41 million (¥538,359 million) and net income of $169.31 million (¥25,323 million). This directly yielded $103.28 million (¥15,448 million) in equity earnings for UBE Corporation (up from $51.09 million), catalyzing a $101.20 million (¥15,137 million) surge in consolidated ordinary profit. However, it also enforces an operational dependency, supplying $184.23 million (¥27,555 million) in coal to fuel UBE Corporation's in-house 145,000 kW power plant.

Strategic Execution and Intellectual Property

R&D expenditure totaled $83.12 million (¥12,432 million), aligning with a target to reach $\ge$4.0% of sales by 2030, with external R&D ratios mandated at 80% and joint patent applications at 30%. Segment allocations reflect the de-commoditization pivot: Pharmaceuticals received $20.44 million (¥3,057 million); Corporate cross-segment seeds received $18.83 million (¥2,816 million); Specialty Products $15.42 million (¥2,306 million); High-Performance Polyurethane $13.88 million (¥2,076 million); Polymers & Chemicals $10.76 million (¥1,610 million); and Machinery $3.79 million (¥567 million).

Intellectual property commercialization is actively pursued via continuous chemical process licensing. C1 chemical technologies are currently licensed to Chinese entities including Shaanxi Coal Group, Xinjiang Tianye Group, and HighChem Co., Ltd. Within Pharmaceuticals, the compound UD-051 (jointly discovered with Kumamoto University) was licensed globally to GALTS Pharma, while oncology drug discovery is advancing via a joint venture with Zeureka Inc.

To mitigate fossil-fuel surcharge exposures slated for FY2028, UBE Corporation aims to achieve >60% of sales from Environmentally Contributing Products by 2030. By accelerating the shutdown of legacy basic chemical facilities, the company will artificially secure a 65% reduction in GHG emissions (compared to 2013 levels) by 2028. Outstanding operational risk hedges include $55.84 million (¥8.35 billion) in currency derivatives and 16 pending asbestos litigation cases against Ube Board Co., Ltd., presenting maximum collective claims of $55.49 million (¥8.3 billion).

HDIN Institutional Verdict

UBE Corporation is navigating a volatile capital transition. Executive leadership explicitly acknowledged missing the initial FY2025 revenue target of $3,276.09 million (¥490 billion) and operating profit target of $167.15 million (¥25 billion), though ordinary profit perfectly aligned with the $250.72 million (¥37.5 billion) projection by achieving $250.76 million (¥37.5 billion).

The medium-term execution relies strictly on balancing transitional friction. The FY2026 plan sets revenue at $3,643.81 million (¥545 billion) and operating profit at $213.95 million (¥32 billion), moving to an identical top-line but an optimized operating profit of $267.44 million (¥40 billion) in FY2027. By 2030, UBE Corporation mandates $3,677.24 million (¥550 billion) in sales, $401.15 million (¥60 billion) in operating profit, EBITDA beyond $668.59 million (¥100 billion), an ROIC more than 6%, ROE more than 8%, and ROS more than 10%.

This requires deploying an available capital pool of $5,014.42 million (¥750 billion) through 2030, explicitly funneling $2,172.92 million (¥325 billion) into CapEx and $902.59 million (¥135 billion) into M&A. To insulate the equity base, $668.59 million (¥100 billion) is reserved for shareholder returns governed by an expanded Dividend on Equity (DOE) target of $\ge$3.5% (aiming for 4.0%).

The internal governance apparatus driving this features a 10-member board (5 independent). Female board representation sits at 10% (1 director) but is scheduled to scale to 25% (3 of 12 members) by 2026. Environmental and human capital KPIs (17.3% female workforce, 5.5% female managers, 36.6% male childcare leave) strictly dictate 10% of executive compensation.

HDIN views the fundamental margin expansion narrative as entirely dependent on successfully decoupling the internal supply chain from the Japanese and Thai commodity assets currently scheduled for shutdown. The balance sheet carries high execution risk due to the sudden injection of LANXESS-derived goodwill; if post-merger integration fails to yield target cash flows within the Urethane division, impairment risks will rapidly resurface. In the interim, UBE Mitsubishi Cement Corporation remains the critical, highly profitable anchor masking core segmental transition weakness.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."