Tokyo Electron Limited: $14.7 Billion R&D and CapEx Realignment Near Asian Fabrication Hubs as Work-in-Process Spikes 10.8% Signals Firm Backlog Execution

Date : 2026-06-24

Reading : 355

HDIN Executive Takeaways

* Tokyo Electron Limited executed a structural operational shift by compressing raw material inventories by 19.1% while increasing Work-in-Process allocations by 10.8%, confirming peak manufacturing utilization against firm near-term logic and memory order books.

* Management anchors 82.2% of its $16.26 billion top line to Asian semiconductor hubs, deploying localized engineering support from Miyagi to Taiwan, China to monetize a 100,000-unit global installed base.

* The institutionalization of a ±20% executive bonus multiplier tied directly to rigorous environmental mandates enforces strict fiduciary accountability, penalizing leadership for pursuing cyclical margin expansion over carbon efficiency.

Figure Tokyo Electron Limited (TEL) FY2025 Strategic & Financial Deep Dive

Financial Execution and Segmental Realities

Financial Execution and Segmental Realities

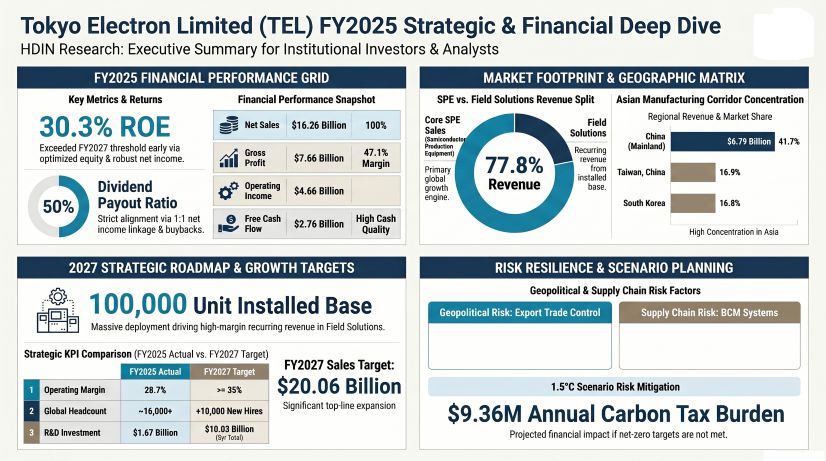

Tokyo Electron Limited [TYO: 8035] reported a highly optimized FY2025 financial architecture defined by top-tier pricing power and aggressive capital allocation. The corporation achieved $16.26 billion (2,431.57 billion JPY) in Net Sales, converting to a Gross Profit Margin of 47.1% ($7.66 billion). Operational leverage was sustained with an Operating Margin of 28.7% ($4.66 billion) and an elite Return on Equity (ROE) of 30.3%. Management successfully front-ran its FY2027 ROE target of >=30%, while advancing toward its stated FY2027 Net Sales objective of $20.06 billion (3 trillion JPY) and Operating Margin target of >=35%.

The dual-engine business model structurally buffers the enterprise against semiconductor capital expenditure cyclicality:

* Semiconductor Production Equipment (SPE): Generated $12.66 billion (1,893.08 billion JPY), representing 77.8% of total net sales.

* Field Solutions (Lifecycle Management): Generated $3.60 billion (538.49 billion JPY), accounting for 22.2% of total net sales. This highly inelastic, recurring revenue stream monetizes a cumulative installed base of 100,000 units.

Client concentration remains heavily tethered to leading integrated device manufacturers and foundries. Samsung Electronics Co., Ltd. accounted for $1.92 billion (11.8% of net sales), and Taiwan Semiconductor Manufacturing Company Ltd. (Taiwan, Province of China) provided $1.88 billion (11.5% of net sales).

Forensic analysis of the balance sheet confirms pristine earnings quality, entirely devoid of aggressive revenue recognition or asset bloating. Total FY2025 inventories stood at $5.01 billion (749,124 million JPY), structured as follows:

* Merchandise and Finished Goods: $1.95 billion (291,523 million JPY)

* Raw Materials and Supplies: $1.79 billion (267,580 million JPY)

* Work-in-Process (WIP): $1.27 billion (190,021 million JPY)

Forward projections for the FY2026 transition illustrate a 19.1% contraction in Raw Materials down to $1.45 billion (216,494 million JPY) combined with a 10.8% expansion in WIP to $1.41 billion (210,570 million JPY). This inverse trajectory proves manufacturing lines are actively consuming safety buffers to fulfill firm backlogs. Current unencumbered liquidity is robust, with Cash and Deposits at $2.78 billion (416,240 million JPY) and Notes, Accounts Receivable, and Contract Assets totaling $3.25 billion (485,626 million JPY).

Below-the-line items further validate operational integrity. Extraordinary gains registered a negligible $0.21 million (31 million JPY), while total extraordinary losses and impairments were contained at $11.00 million (1,645 million JPY), of which exactly $8.00 million (1,197 million JPY) was allocated to primary asset impairment/retirement (representing 0.05% of sales). Management refrained from liquidating strategic cross-shareholdings to pad net income, maintaining untouched equity stakes of 1.69 million shares (1,699,000) in ASM International N.V. and 2.72 million shares in Hana Materials, Inc. Natural hedging neutralized foreign exchange volatility, with the FY2025 Foreign Currency Translation Adjustment (FCTA) flow restricted to $9.39 million (1,405 million JPY), bringing the cumulative FCTA balance to $406.51 million (60,801 million JPY).

Cash flow conversion strictly funds the 5-year, $10.03 billion (1.5 trillion JPY) R&D and $4.68 billion (700 billion JPY) CapEx cycles. Operating Cash Flow hit $3.89 billion, funding an Investing Cash Flow outflow of -$1.13 billion. The remaining $2.76 billion in Free Cash Flow supported aggressive shareholder returns—anchored by a 50% dividend payout ratio—resulting in a Financing Cash Flow of -$2.60 billion. Tokyo Electron Limited strictly expenses R&D outlays under SG&A rather than capitalizing them, recording $1.67 billion (250,017 million JPY) in FY2025 and projecting $1.86 billion (277,866 million JPY) for FY2026.

Infrastructure Layout and Supply Chain Architecture

Tokyo Electron Limited's spatial distribution isolates core proprietary intellectual property development within Japan while deploying a localized, decentralized engineering support network globally. This network operates under the internal "Best Products, Best Technical Service" mandate to serve the extreme geographic concentration of the Asian semiconductor supply chain.

FY2025 Geographic Revenue Distribution:

* Mainland China: $6.79 billion (1,015.06 billion JPY) — 41.7%

* Taiwan, China: $2.75 billion (410.63 billion JPY) — 16.9%

* South Korea: $2.73 billion (409.01 billion JPY) — 16.8%

* North America: $1.62 billion (242.96 billion JPY) — 10.0%

* Japan: $1.27 billion (189.98 billion JPY) — 7.8%

* Southeast Asia & Others: $0.59 billion (88.40 billion JPY) — 3.6%

* Europe: $0.50 billion (75.52 billion JPY) — 3.1%

Core Domestic Manufacturing and IP Hubs (Japan):

* Tokyo Electron Miyagi Ltd. (Miyagi): Centralized hub for advanced Etch systems.

* Tokyo Electron Kyushu Ltd. (Kumamoto): Critical manufacturing base for Coater/Developer systems and Surface Preparation tools.

* Tokyo Electron Technology Solutions Ltd.: Managerial node for Deposition and Thermal processing technologies.

Global Engineering and Localized Support Nodes:

* North America: TEL Technology Center, America, LLC (Albany, New York) interfaces with leading academic consortia, while TEL Manufacturing and Engineering of America, Inc. operates in Austin, Texas. The company further protects academic IP pipelines through the U.S.-Japan University Partnership for Workforce Advancement and Research & Development in Semiconductors (UPWARDS) consortium.

* Asia Support Nodes: Continuous localized process co-optimization is executed via Tokyo Electron Taiwan Ltd. (Taiwan, China), Tokyo Electron Korea Ltd. (South Korea), Tokyo Electron (Shanghai) Ltd. (Mainland China), and Tokyo Electron (Kunshan) Ltd. (Mainland China). Decentralized environmental initiatives include a proprietary solar power generation installation at Tokyo Electron Taiwan Ltd.

Executing this infrastructure requires aggressive scaling of human capital under a "motivation-oriented management" framework. The corporation targets the addition of 10,000 new global employees over a 5-year period. Management tracks workforce stability via an engagement score, reporting a current metric of 45.3%, against a target of 60% by FY2027 and 85% by FY2030. Concurrently, the female management ratio currently stands at 3.8%, tracking toward a FY2027 target of 5.0% and a medium-term structural target of 8.0%. Talent retention is fortified via broad-based equity compensation through Employee Stock Ownership Plans (ESOP) and Board Incentive Plans (BIP).

Risk Quantification and HDIN Institutional Verdict

Tokyo Electron Limited systematically mitigates severe operational risks—namely, export control embargoes, cyclical downturns, and environmental burdens—through institutionalized governance. Compliance with international technology embargoes is governed by an Export Trade Control Committee operating alongside Risk Management and Information Security Committees, reporting to the Corporate Officers Meeting. Business Continuity Plans (BCP) and centralized procurement databases act as primary defenses against physical supply constraints.

Executive compensation strictly penalizes volume-driven growth that degrades capital efficiency. Point allocation for stock-based compensation is calculated on a rigid formula: 70% weighted to Consolidated Operating Margin and 30% weighted to Consolidated ROE. Additionally, internal directors and the CEO are subject to a non-financial performance evaluation multiplier of ±20% on their short-term performance-linked cash bonus, directly tying executive wealth to ESG metrics.

The corporation applies the Task Force on Climate-related Financial Disclosures (TCFD) framework to quantify environmental transition risks. Under a 1.5°C scenario, management projects carbon taxation to reach $205.59 (30,750 JPY) per t-CO2 by March 2041. Assuming unmitigated baseline emissions, this equates to a direct $9.36 million (1.4 billion JPY) annual tax burden.

To eliminate this liability, the "E-COMPASS" initiative drives Science Based Targets (SBT):

* Scope 1 & 2 Emissions: Target an 85% absolute reduction by March 2031 against a FY2019 baseline, with a 2050 Net Zero commitment. The core driver is a transition to 100% renewable energy by 2031, currently operating at 87% utilization.

* Scope 3 Emissions: Target a 55% reduction in CO2 per wafer by March 2031 against a FY2022 baseline, with current operational progress achieving an 11% reduction.

* Resource Management: Total macro-level waste recycling is currently executing at 99.2%, outperforming the corporate target of 99%.

HDIN Institutional Verdict:

Tokyo Electron Limited’s balance sheet reflects impeccable earnings quality, characterized by conservative R&D expensing and a zero-distortion below-the-line profile. The shift of capital from raw materials directly into Work-in-Process serves as an objective, leading operational indicator confirming firm backlog demand from logic foundries and IDMs, entirely refuting immediate risks of fab order cancellations. Furthermore, the 22.2% revenue contribution from Field Solutions creates a high-margin firewall that effectively immunizes the corporation against the cyclical volatility inherent in front-end equipment sales.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Tokyo Electron Limited executed a structural operational shift by compressing raw material inventories by 19.1% while increasing Work-in-Process allocations by 10.8%, confirming peak manufacturing utilization against firm near-term logic and memory order books.

* Management anchors 82.2% of its $16.26 billion top line to Asian semiconductor hubs, deploying localized engineering support from Miyagi to Taiwan, China to monetize a 100,000-unit global installed base.

* The institutionalization of a ±20% executive bonus multiplier tied directly to rigorous environmental mandates enforces strict fiduciary accountability, penalizing leadership for pursuing cyclical margin expansion over carbon efficiency.

Figure Tokyo Electron Limited (TEL) FY2025 Strategic & Financial Deep Dive

Financial Execution and Segmental RealitiesTokyo Electron Limited [TYO: 8035] reported a highly optimized FY2025 financial architecture defined by top-tier pricing power and aggressive capital allocation. The corporation achieved $16.26 billion (2,431.57 billion JPY) in Net Sales, converting to a Gross Profit Margin of 47.1% ($7.66 billion). Operational leverage was sustained with an Operating Margin of 28.7% ($4.66 billion) and an elite Return on Equity (ROE) of 30.3%. Management successfully front-ran its FY2027 ROE target of >=30%, while advancing toward its stated FY2027 Net Sales objective of $20.06 billion (3 trillion JPY) and Operating Margin target of >=35%.

The dual-engine business model structurally buffers the enterprise against semiconductor capital expenditure cyclicality:

* Semiconductor Production Equipment (SPE): Generated $12.66 billion (1,893.08 billion JPY), representing 77.8% of total net sales.

* Field Solutions (Lifecycle Management): Generated $3.60 billion (538.49 billion JPY), accounting for 22.2% of total net sales. This highly inelastic, recurring revenue stream monetizes a cumulative installed base of 100,000 units.

Client concentration remains heavily tethered to leading integrated device manufacturers and foundries. Samsung Electronics Co., Ltd. accounted for $1.92 billion (11.8% of net sales), and Taiwan Semiconductor Manufacturing Company Ltd. (Taiwan, Province of China) provided $1.88 billion (11.5% of net sales).

Forensic analysis of the balance sheet confirms pristine earnings quality, entirely devoid of aggressive revenue recognition or asset bloating. Total FY2025 inventories stood at $5.01 billion (749,124 million JPY), structured as follows:

* Merchandise and Finished Goods: $1.95 billion (291,523 million JPY)

* Raw Materials and Supplies: $1.79 billion (267,580 million JPY)

* Work-in-Process (WIP): $1.27 billion (190,021 million JPY)

Forward projections for the FY2026 transition illustrate a 19.1% contraction in Raw Materials down to $1.45 billion (216,494 million JPY) combined with a 10.8% expansion in WIP to $1.41 billion (210,570 million JPY). This inverse trajectory proves manufacturing lines are actively consuming safety buffers to fulfill firm backlogs. Current unencumbered liquidity is robust, with Cash and Deposits at $2.78 billion (416,240 million JPY) and Notes, Accounts Receivable, and Contract Assets totaling $3.25 billion (485,626 million JPY).

Below-the-line items further validate operational integrity. Extraordinary gains registered a negligible $0.21 million (31 million JPY), while total extraordinary losses and impairments were contained at $11.00 million (1,645 million JPY), of which exactly $8.00 million (1,197 million JPY) was allocated to primary asset impairment/retirement (representing 0.05% of sales). Management refrained from liquidating strategic cross-shareholdings to pad net income, maintaining untouched equity stakes of 1.69 million shares (1,699,000) in ASM International N.V. and 2.72 million shares in Hana Materials, Inc. Natural hedging neutralized foreign exchange volatility, with the FY2025 Foreign Currency Translation Adjustment (FCTA) flow restricted to $9.39 million (1,405 million JPY), bringing the cumulative FCTA balance to $406.51 million (60,801 million JPY).

Cash flow conversion strictly funds the 5-year, $10.03 billion (1.5 trillion JPY) R&D and $4.68 billion (700 billion JPY) CapEx cycles. Operating Cash Flow hit $3.89 billion, funding an Investing Cash Flow outflow of -$1.13 billion. The remaining $2.76 billion in Free Cash Flow supported aggressive shareholder returns—anchored by a 50% dividend payout ratio—resulting in a Financing Cash Flow of -$2.60 billion. Tokyo Electron Limited strictly expenses R&D outlays under SG&A rather than capitalizing them, recording $1.67 billion (250,017 million JPY) in FY2025 and projecting $1.86 billion (277,866 million JPY) for FY2026.

Infrastructure Layout and Supply Chain Architecture

Tokyo Electron Limited's spatial distribution isolates core proprietary intellectual property development within Japan while deploying a localized, decentralized engineering support network globally. This network operates under the internal "Best Products, Best Technical Service" mandate to serve the extreme geographic concentration of the Asian semiconductor supply chain.

FY2025 Geographic Revenue Distribution:

* Mainland China: $6.79 billion (1,015.06 billion JPY) — 41.7%

* Taiwan, China: $2.75 billion (410.63 billion JPY) — 16.9%

* South Korea: $2.73 billion (409.01 billion JPY) — 16.8%

* North America: $1.62 billion (242.96 billion JPY) — 10.0%

* Japan: $1.27 billion (189.98 billion JPY) — 7.8%

* Southeast Asia & Others: $0.59 billion (88.40 billion JPY) — 3.6%

* Europe: $0.50 billion (75.52 billion JPY) — 3.1%

Core Domestic Manufacturing and IP Hubs (Japan):

* Tokyo Electron Miyagi Ltd. (Miyagi): Centralized hub for advanced Etch systems.

* Tokyo Electron Kyushu Ltd. (Kumamoto): Critical manufacturing base for Coater/Developer systems and Surface Preparation tools.

* Tokyo Electron Technology Solutions Ltd.: Managerial node for Deposition and Thermal processing technologies.

Global Engineering and Localized Support Nodes:

* North America: TEL Technology Center, America, LLC (Albany, New York) interfaces with leading academic consortia, while TEL Manufacturing and Engineering of America, Inc. operates in Austin, Texas. The company further protects academic IP pipelines through the U.S.-Japan University Partnership for Workforce Advancement and Research & Development in Semiconductors (UPWARDS) consortium.

* Asia Support Nodes: Continuous localized process co-optimization is executed via Tokyo Electron Taiwan Ltd. (Taiwan, China), Tokyo Electron Korea Ltd. (South Korea), Tokyo Electron (Shanghai) Ltd. (Mainland China), and Tokyo Electron (Kunshan) Ltd. (Mainland China). Decentralized environmental initiatives include a proprietary solar power generation installation at Tokyo Electron Taiwan Ltd.

Executing this infrastructure requires aggressive scaling of human capital under a "motivation-oriented management" framework. The corporation targets the addition of 10,000 new global employees over a 5-year period. Management tracks workforce stability via an engagement score, reporting a current metric of 45.3%, against a target of 60% by FY2027 and 85% by FY2030. Concurrently, the female management ratio currently stands at 3.8%, tracking toward a FY2027 target of 5.0% and a medium-term structural target of 8.0%. Talent retention is fortified via broad-based equity compensation through Employee Stock Ownership Plans (ESOP) and Board Incentive Plans (BIP).

Risk Quantification and HDIN Institutional Verdict

Tokyo Electron Limited systematically mitigates severe operational risks—namely, export control embargoes, cyclical downturns, and environmental burdens—through institutionalized governance. Compliance with international technology embargoes is governed by an Export Trade Control Committee operating alongside Risk Management and Information Security Committees, reporting to the Corporate Officers Meeting. Business Continuity Plans (BCP) and centralized procurement databases act as primary defenses against physical supply constraints.

Executive compensation strictly penalizes volume-driven growth that degrades capital efficiency. Point allocation for stock-based compensation is calculated on a rigid formula: 70% weighted to Consolidated Operating Margin and 30% weighted to Consolidated ROE. Additionally, internal directors and the CEO are subject to a non-financial performance evaluation multiplier of ±20% on their short-term performance-linked cash bonus, directly tying executive wealth to ESG metrics.

The corporation applies the Task Force on Climate-related Financial Disclosures (TCFD) framework to quantify environmental transition risks. Under a 1.5°C scenario, management projects carbon taxation to reach $205.59 (30,750 JPY) per t-CO2 by March 2041. Assuming unmitigated baseline emissions, this equates to a direct $9.36 million (1.4 billion JPY) annual tax burden.

To eliminate this liability, the "E-COMPASS" initiative drives Science Based Targets (SBT):

* Scope 1 & 2 Emissions: Target an 85% absolute reduction by March 2031 against a FY2019 baseline, with a 2050 Net Zero commitment. The core driver is a transition to 100% renewable energy by 2031, currently operating at 87% utilization.

* Scope 3 Emissions: Target a 55% reduction in CO2 per wafer by March 2031 against a FY2022 baseline, with current operational progress achieving an 11% reduction.

* Resource Management: Total macro-level waste recycling is currently executing at 99.2%, outperforming the corporate target of 99%.

HDIN Institutional Verdict:

Tokyo Electron Limited’s balance sheet reflects impeccable earnings quality, characterized by conservative R&D expensing and a zero-distortion below-the-line profile. The shift of capital from raw materials directly into Work-in-Process serves as an objective, leading operational indicator confirming firm backlog demand from logic foundries and IDMs, entirely refuting immediate risks of fab order cancellations. Furthermore, the 22.2% revenue contribution from Field Solutions creates a high-margin firewall that effectively immunizes the corporation against the cyclical volatility inherent in front-end equipment sales.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*