Ai Robotics Inc.: Capital-Intensive Wholesale Pivot in Japan Triggers Negative Cash Conversion as DSO Spikes to 91 Days

Date : 2026-06-24

Reading : 344

HDIN Executive Takeaways

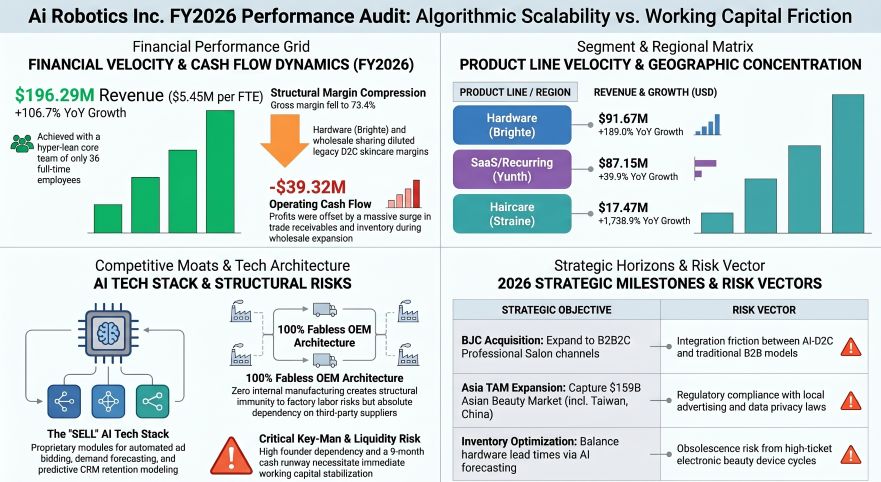

* Top-line revenue surged 106.7% year-over-year to $196.29 million, driven by the Brighte hardware rollout, which compressed gross margins by 500 basis points due to structural COGS inflation.

* A 100% outsourced manufacturing footprint shifted the working capital burden to the Tokyo headquarters, driving a $39.32 million operating cash flow deficit and extending days inventory outstanding (DIO) to 192 days.

* Management's aggressive penetration into the $159.12 billion Asian beauty market faces severe liquidity constraints, operating on less than nine months of cash runway against rising short-term debt obligations.

Figure Ai Robotics Inc FY2026 Performance Audit: Algorithmic Scalability vs Working Capital Friction

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Ai Robotics Inc. [TYO: AIRO] concluded the fiscal year ended March 31, 2026, executing a structural pivot away from its high-margin, pure-play Direct-to-Consumer (D2C) subscription model toward an omnichannel, hardware-heavy distribution matrix. Consolidated revenue reached $196.29 million (converted at a base rate of 1 USD = 149.5686 JPY), an expansion of 106.7% from $94.98 million in FY2025.

Despite top-line acceleration, the introduction of the Brighte consumer electronics brand structurally altered unit economics, degrading the gross margin profile by 500 basis points from 78.4% to 73.4%. Cost of Goods Sold (COGS) inflated from $20.48 million to $52.29 million.

The proprietary brand architecture experienced diverging growth trajectories:

* Yunth (Skincare/Cosmetics): Revenue reached $87.15 million, representing a 39.9% year-over-year expansion. However, its concentration as a percentage of total corporate revenue diluted from 65.6% to 44.4%.

* Brighte (Beauty Electronics): Revenue escalated 189.0% year-over-year to $91.67 million, generating $59.95 million in new top-line growth and accounting for 46.7% of total sales.

* Straine (Haircare): Revenue accelerated 1,738.9% year-over-year, scaling from a $0.95 million base to $17.47 million (8.9% of total revenue).

Operating margin (EBIT margin) contracted from 17.5% to 12.9%. Selling, General, and Administrative (SG&A) expenses rose 104.7% to $118.57 million, tightening marginally from 61.0% to 60.4% as a percentage of revenue. Specifically, advertising expenses absorbed $117.66 million (17.59 billion JPY), equating to exactly 60.0% of total revenue. Net income grew 55.7% to $17.74 million, though Return on Equity (ROE) compressed from 76.8% to 56.7%.

The sales channel matrix reflects an aggressive physical retail rollout:

* In-house EC (Proprietary D2C): Dropped from 61.4% to 48.4% of total revenue, generating $95.00 million.

* In-store Wholesale (Physical Retail): Expanded from 11.3% ($10.73 million) to 34.0% ($66.74 million).

* EC Malls: Captured 17.6% of revenue at $34.55 million.

Predictable baseline revenue remains anchored by the Yunth recurring subscription base, which expanded from 136,301 members in Q4 FY2025 to 174,920 members in Q4 FY2026. This is corroborated by a 40% year-over-year expansion in contract liabilities, functioning as the primary proxy for Remaining Performance Obligations (RPO), which grew from $3.96 million (592.91 million JPY) to $5.55 million (830.14 million JPY).

Infrastructure Layout and Regional Moats

Despite the corporate nomenclature, Ai Robotics Inc. deploys zero proprietary capital toward deep-tech mechanical engineering. The balance sheet reports zero standalone Research & Development (R&D) expense line items, and software capitalization is negligible at $33,000 (4.93 million JPY). The corporate moat is entirely encapsulated within "SELL," a proprietary algorithmic AI framework utilizing e-commerce (EC) data and physical Point of Sales (ID-POS) data to automate demand forecasting and ad-creative generation.

The enterprise operates a strictly fabless ecosystem, outsourcing 100% of physical production, logistics, and call center operations to third-party Original Equipment Manufacturers (OEMs). Internal human capital is highly concentrated, with the full-time employee (FTE) headcount expanding from 27 to 36 individuals, generating an anomalous revenue-per-employee ratio of approximately $5.45 million. The temporary and contract workforce grew from 11 to 17 personnel. This 36-person core workforce is centralized entirely at the corporate headquarters in Minato-ku, Tokyo, Japan, evidenced by a minimal Asset Retirement Obligation (ARO) of $9,808 (1.46 million JPY) tied to leased office restoration.

The current revenue footprint is 100% localized to the domestic Japanese market, targeting a Total Addressable Market (TAM) quantified at $35.43 billion (5.3 trillion JPY). Management segregates this domestic market into health foods ($11.53 billion), skincare ($9.80 billion), jewelry ($6.99 billion), haircare ($4.52 billion), and beauty/health appliances ($2.62 billion). Over the medium term, Ai Robotics Inc. plans to penetrate a $159.12 billion (23.8 trillion JPY) TAM across the top 40 Asian nations, specifically targeting mainland China, the Republic of Korea, and Taiwan, China.

The regulatory environment remains confined to localized consumer protection rather than deep-tech autonomous liability. Legal compliance depends on strict adherence to Japan's Act on the Protection of Personal Information (APPI), the Pharmaceuticals and Medical Devices Act, and the Act against Unjustifiable Premiums and Misleading Representations.

HDIN Institutional Verdict

The fiscal data reveals an acute working capital crisis actively masked by triple-digit top-line growth. The strategic pivot to physical wholesale distribution fundamentally dismantled the company’s capital-light D2C cash conversion cycle. Operating Cash Flow (OCF) collapsed from a positive $8.78 million in FY2025 to a negative $39.32 million (-5.88 billion JPY) in FY2026, resulting in a Free Cash Flow (FCF) conversion rate of -221%.

The operational cash drain is directly attributable to the balance sheet absorption required to supply physical retail networks. Trade receivables surged by $40.98 million (6.12 billion JPY), pushing Days Sales Outstanding (DSO) from 31 days to 91 days. Concurrently, inventory quadrupled from $6.47 million to $27.52 million, an increase of $25.07 million (3.75 billion JPY) that drove Days Inventory Outstanding (DIO) from 115 days to an unsustainable 192 days. The company's leverage over its OEM network remains minimal, with Days Payable Outstanding (DPO) extending only from 31 days to 44 days.

To finance this $39.32 million liquidity drain, Ai Robotics Inc. abandoned its zero short-term debt posture, absorbing $23.40 million (3.50 billion JPY) in short-term obligations while scaling long-term borrowings from $4.23 million (632.81 million JPY) to $21.85 million (3.26 billion JPY). The company also accumulated $16.75 million (2.50 billion JPY) in corporate income taxes payable. Against total assets of $123.23 million, ending equity stood at $40.44 million, yielding an equity ratio of 32.8%. With cash equivalents of $26.66 million, the company holds fewer than nine months of organic cash runway.

Corporate governance relies heavily on founder and Representative Director Makoto Tatsukawa, manifesting acute key-man risk. Total compensation for five internal directors was set at $874,515 (130.80 million JPY), alongside $230,329 (34.45 million JPY) for six outside directors. The Board utilizes an Audit and Supervisory Committee comprising four members (three of whom are independent), audited by PwC Japan. Ai Robotics Inc. circumvents high base salaries through explicit Stock-Based Compensation (SBC) tranches, notably authorizing 1,785 options (892,500 shares) at an exercise price of $6.04 (903 JPY) and 350 options (175,000 shares) at $7.42 (1,110 JPY). Against 64,900,000 outstanding shares, this preserves a highly manageable single-digit dilution profile.

Institutional scrutiny must be immediately directed toward the generalized "Refund Liability" account, which grew from $315,126 (47.13 million JPY) to $538,736 (80.58 million JPY). The explicit absence of a standalone "Provision for Product Warranties" against a nearly $100 million combined consumer electronics and cosmetics portfolio suggests the deferral of long-tail hardware warranty recognition. Furthermore, the March 2026 execution of M&A to acquire BJC (operator of salon-exclusive brands "soaddicted" and "SPICARE") remains subject to active Purchase Price Allocation (PPA) accounting, presenting near-term intangible amortization risk heading into FY2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Top-line revenue surged 106.7% year-over-year to $196.29 million, driven by the Brighte hardware rollout, which compressed gross margins by 500 basis points due to structural COGS inflation.

* A 100% outsourced manufacturing footprint shifted the working capital burden to the Tokyo headquarters, driving a $39.32 million operating cash flow deficit and extending days inventory outstanding (DIO) to 192 days.

* Management's aggressive penetration into the $159.12 billion Asian beauty market faces severe liquidity constraints, operating on less than nine months of cash runway against rising short-term debt obligations.

Figure Ai Robotics Inc FY2026 Performance Audit: Algorithmic Scalability vs Working Capital Friction

Segmental Realities and Margin CompressionAi Robotics Inc. [TYO: AIRO] concluded the fiscal year ended March 31, 2026, executing a structural pivot away from its high-margin, pure-play Direct-to-Consumer (D2C) subscription model toward an omnichannel, hardware-heavy distribution matrix. Consolidated revenue reached $196.29 million (converted at a base rate of 1 USD = 149.5686 JPY), an expansion of 106.7% from $94.98 million in FY2025.

Despite top-line acceleration, the introduction of the Brighte consumer electronics brand structurally altered unit economics, degrading the gross margin profile by 500 basis points from 78.4% to 73.4%. Cost of Goods Sold (COGS) inflated from $20.48 million to $52.29 million.

The proprietary brand architecture experienced diverging growth trajectories:

* Yunth (Skincare/Cosmetics): Revenue reached $87.15 million, representing a 39.9% year-over-year expansion. However, its concentration as a percentage of total corporate revenue diluted from 65.6% to 44.4%.

* Brighte (Beauty Electronics): Revenue escalated 189.0% year-over-year to $91.67 million, generating $59.95 million in new top-line growth and accounting for 46.7% of total sales.

* Straine (Haircare): Revenue accelerated 1,738.9% year-over-year, scaling from a $0.95 million base to $17.47 million (8.9% of total revenue).

Operating margin (EBIT margin) contracted from 17.5% to 12.9%. Selling, General, and Administrative (SG&A) expenses rose 104.7% to $118.57 million, tightening marginally from 61.0% to 60.4% as a percentage of revenue. Specifically, advertising expenses absorbed $117.66 million (17.59 billion JPY), equating to exactly 60.0% of total revenue. Net income grew 55.7% to $17.74 million, though Return on Equity (ROE) compressed from 76.8% to 56.7%.

The sales channel matrix reflects an aggressive physical retail rollout:

* In-house EC (Proprietary D2C): Dropped from 61.4% to 48.4% of total revenue, generating $95.00 million.

* In-store Wholesale (Physical Retail): Expanded from 11.3% ($10.73 million) to 34.0% ($66.74 million).

* EC Malls: Captured 17.6% of revenue at $34.55 million.

Predictable baseline revenue remains anchored by the Yunth recurring subscription base, which expanded from 136,301 members in Q4 FY2025 to 174,920 members in Q4 FY2026. This is corroborated by a 40% year-over-year expansion in contract liabilities, functioning as the primary proxy for Remaining Performance Obligations (RPO), which grew from $3.96 million (592.91 million JPY) to $5.55 million (830.14 million JPY).

Infrastructure Layout and Regional Moats

Despite the corporate nomenclature, Ai Robotics Inc. deploys zero proprietary capital toward deep-tech mechanical engineering. The balance sheet reports zero standalone Research & Development (R&D) expense line items, and software capitalization is negligible at $33,000 (4.93 million JPY). The corporate moat is entirely encapsulated within "SELL," a proprietary algorithmic AI framework utilizing e-commerce (EC) data and physical Point of Sales (ID-POS) data to automate demand forecasting and ad-creative generation.

The enterprise operates a strictly fabless ecosystem, outsourcing 100% of physical production, logistics, and call center operations to third-party Original Equipment Manufacturers (OEMs). Internal human capital is highly concentrated, with the full-time employee (FTE) headcount expanding from 27 to 36 individuals, generating an anomalous revenue-per-employee ratio of approximately $5.45 million. The temporary and contract workforce grew from 11 to 17 personnel. This 36-person core workforce is centralized entirely at the corporate headquarters in Minato-ku, Tokyo, Japan, evidenced by a minimal Asset Retirement Obligation (ARO) of $9,808 (1.46 million JPY) tied to leased office restoration.

The current revenue footprint is 100% localized to the domestic Japanese market, targeting a Total Addressable Market (TAM) quantified at $35.43 billion (5.3 trillion JPY). Management segregates this domestic market into health foods ($11.53 billion), skincare ($9.80 billion), jewelry ($6.99 billion), haircare ($4.52 billion), and beauty/health appliances ($2.62 billion). Over the medium term, Ai Robotics Inc. plans to penetrate a $159.12 billion (23.8 trillion JPY) TAM across the top 40 Asian nations, specifically targeting mainland China, the Republic of Korea, and Taiwan, China.

The regulatory environment remains confined to localized consumer protection rather than deep-tech autonomous liability. Legal compliance depends on strict adherence to Japan's Act on the Protection of Personal Information (APPI), the Pharmaceuticals and Medical Devices Act, and the Act against Unjustifiable Premiums and Misleading Representations.

HDIN Institutional Verdict

The fiscal data reveals an acute working capital crisis actively masked by triple-digit top-line growth. The strategic pivot to physical wholesale distribution fundamentally dismantled the company’s capital-light D2C cash conversion cycle. Operating Cash Flow (OCF) collapsed from a positive $8.78 million in FY2025 to a negative $39.32 million (-5.88 billion JPY) in FY2026, resulting in a Free Cash Flow (FCF) conversion rate of -221%.

The operational cash drain is directly attributable to the balance sheet absorption required to supply physical retail networks. Trade receivables surged by $40.98 million (6.12 billion JPY), pushing Days Sales Outstanding (DSO) from 31 days to 91 days. Concurrently, inventory quadrupled from $6.47 million to $27.52 million, an increase of $25.07 million (3.75 billion JPY) that drove Days Inventory Outstanding (DIO) from 115 days to an unsustainable 192 days. The company's leverage over its OEM network remains minimal, with Days Payable Outstanding (DPO) extending only from 31 days to 44 days.

To finance this $39.32 million liquidity drain, Ai Robotics Inc. abandoned its zero short-term debt posture, absorbing $23.40 million (3.50 billion JPY) in short-term obligations while scaling long-term borrowings from $4.23 million (632.81 million JPY) to $21.85 million (3.26 billion JPY). The company also accumulated $16.75 million (2.50 billion JPY) in corporate income taxes payable. Against total assets of $123.23 million, ending equity stood at $40.44 million, yielding an equity ratio of 32.8%. With cash equivalents of $26.66 million, the company holds fewer than nine months of organic cash runway.

Corporate governance relies heavily on founder and Representative Director Makoto Tatsukawa, manifesting acute key-man risk. Total compensation for five internal directors was set at $874,515 (130.80 million JPY), alongside $230,329 (34.45 million JPY) for six outside directors. The Board utilizes an Audit and Supervisory Committee comprising four members (three of whom are independent), audited by PwC Japan. Ai Robotics Inc. circumvents high base salaries through explicit Stock-Based Compensation (SBC) tranches, notably authorizing 1,785 options (892,500 shares) at an exercise price of $6.04 (903 JPY) and 350 options (175,000 shares) at $7.42 (1,110 JPY). Against 64,900,000 outstanding shares, this preserves a highly manageable single-digit dilution profile.

Institutional scrutiny must be immediately directed toward the generalized "Refund Liability" account, which grew from $315,126 (47.13 million JPY) to $538,736 (80.58 million JPY). The explicit absence of a standalone "Provision for Product Warranties" against a nearly $100 million combined consumer electronics and cosmetics portfolio suggests the deferral of long-tail hardware warranty recognition. Furthermore, the March 2026 execution of M&A to acquire BJC (operator of salon-exclusive brands "soaddicted" and "SPICARE") remains subject to active Purchase Price Allocation (PPA) accounting, presenting near-term intangible amortization risk heading into FY2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*