AI Inc.: Asset-Light Pivot Near Bunkyo-ku Hub as 607.2% Net Income Expansion Masks Cash Flow Contraction

Date : 2026-06-24

Reading : 313

HDIN Executive Takeaways

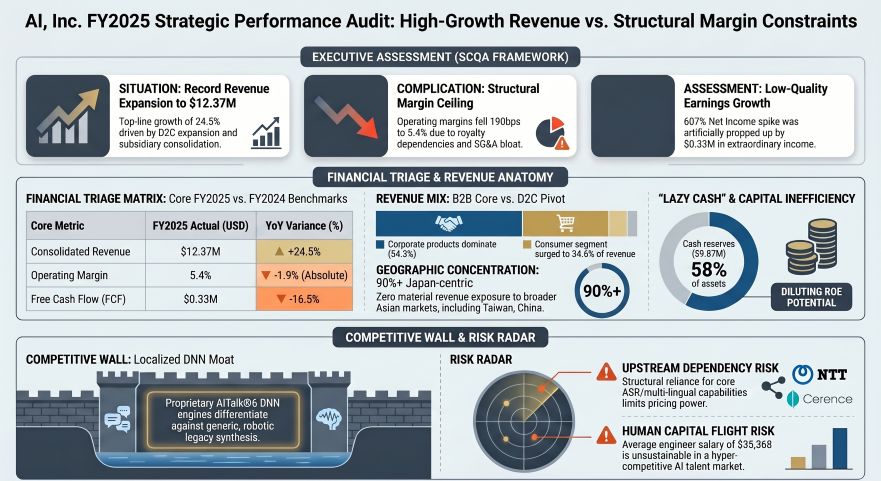

* Operating cash flow contracted -24.4% to $0.51M despite a +24.5% revenue expansion, driven by a +615% working capital surge in unbilled contract assets.

* Confined to Bunkyo-ku, Tokyo, the firm holds zero operational exposure in Taiwan or China, generating over 90% of revenue domestically.

* Management executed a 10.0% equity retirement of 700,000 shares to optimize yields against a heavily underutilized $9.87M zero-leverage cash stockpile.

Figure Al Inc FY2025 Strategic Performance Audit: High-Growth Revenue vs Structural Margin Constraints

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

AI, Inc. presents a contradictory financial profile wherein a +24.5% top-line expansion to $12.37M (1,850.06M JPY) masks deteriorating earnings quality. While Gross Margin expanded +230 basis points to 52.7%, yielding a Gross Profit of $6.52M as Cost of Goods Sold (COGS) advanced at a slower +18.6% to $5.84M (874.28M JPY), the underlying operating efficiency reversed. Total Selling, General & Administrative (SG&A) expenses accelerated by +36.7% from $4.28M (640.15M JPY) to $5.85M (875.22M JPY). This inorganic bloat, driven primarily by external integrations, caused SG&A to consume 47.3% of total revenue. Consequently, Operating Income compressed -7.8% from $0.73M to $0.67M (100,554k JPY), driving Operating Margins down -190 basis points from 7.3% to 5.4%.

The reported Net Income explosion of +607.2% from $0.10M to $0.74M was structurally subsidized by non-operating accounting levers rather than operational scaling. The bottom line was propped up by $0.33M (50,094k JPY) in Extraordinary Income. Simultaneously, the firm recorded a $0.15M (22,564k JPY) Extraordinary Loss tied to impairment, alongside an additional $0.08M (11,538k JPY) drag in Non-Operating Expenses.

The divergence between optical profitability and liquidity is severe. Operating Cash Flow (OCF) contracted -24.4% from $0.68M to $0.51M, while Free Cash Flow (FCF) fell -16.5% from $0.40M to $0.33M. This contraction originates from a massive working capital anomaly: Contract Assets (unbilled receivables) surged +615% from $0.05M (7,285k JPY) to $0.35M (52,114k JPY). Concurrently, Contract Liabilities (Deferred Revenue) stagnated, declining marginally from $0.85M (126,903k JPY) to $0.84M (126,314k JPY), confirming an absence of scalable recurring subscriptions.

*FY2025 Segmental Revenue Architecture (Fixed conversion applied: 1 USD = 149.5686 JPY)*

* Corporate Voice Products: $6.72M (54.3% of total) via B2B integration.

* Consumer Voice Products: $4.29M (34.6% of total) via B2C/D2C channels.

* Other (Voice Business): $0.90M (7.3% of total) via subsidiary operations.

* CRM Business (Visionary Cloud): $0.46M / 69,324k JPY (3.7% of total).

* Total Consolidated Revenue: $12.37M (100.0%). The legacy Voice Business segment accounts for $11.91M (1,780.73M JPY).

Customer concentration metrics reflect high revenue volatility. AI, Inc. holds Accounts Receivable of $1.92M (287,023k JPY), down from $2.06M, carrying a microscopic Allowance for Doubtful Accounts of $4,178 (625k JPY), representing just 0.21% of the trade balance. However, the top FY2024 client, which historically provided 14.9% of revenue, collapsed to a 4.2% contribution. A new top client emerged in FY2025, generating 11.3% of total sales, equivalent to $1.40M (208,757k JPY).

Management's forward-looking guidance under its Medium-Term Management Plan targets $10.70M (1,600M JPY) in revenue and a 13.5% Operating Margin by FY2027, figures structurally at odds with the current 5.4% margin reality.

Infrastructure Layout and Regional Moats

AI, Inc. operates a highly concentrated geographic footprint, managing its core engineering and R&D hub strictly from its headquarters in Bunkyo-ku, Tokyo, Japan. Over 90% of its external sales and property, plant, and equipment (PP&E) are domiciled within Japan. The firm actively omits further geographic segment disclosures, confirming zero outbound commercial manufacturing or localized operations in Taiwan or China.

The company's intellectual property architecture relies heavily on upstream licensing alliances to bypass exhaustive organic R&D. While AI, Inc. deploys proprietary Deep Neural Network architectures via AITalk®6 and AITalk®5, core capabilities are externalized. Speech recognition (ASR) is licensed from NTT TechnoCross Corporation, ATR-Promotions, and the National Institute of Information and Communications Technology (NICT). Multi-lingual synthesis depends on agreements with Cerence B.V.

Internal product commercialization velocity is decelerating. Capitalized Software plummeted from $0.36M to $0.11M (15,754k JPY), while Software in progress sits at an anemic $0.027M (4,099k JPY). R&D expenses embedded within SG&A rose +26.4% to $0.83M (123.42M JPY). Furthermore, total Capital Expenditure (CapEx) dropped -35.7% from $0.28M to $0.18M. Instead of organic capitalization, AI, Inc. is substituting proprietary engineering with inorganic scale, carrying $3.78M (565,568k JPY) in Goodwill on its balance sheet. Amortization of Goodwill exploded +202% year-over-year from $0.18M (26.82M JPY) to $0.54M (81.03M JPY), driven by the acquisitions of domestic subsidiaries ATR-Trek and Lapis Live.

The product suite is heavily fragmented across multiple silos:

* B2B & Cloud APIs: AITalk WebAPI, AICloud, AITalk Custom Voice, and the Visionary Cloud CRM platform.

* D2C Packaged IP: A.I.VOICE, A.I.VOICE2, VOICEROID, and A.I.VOICE for GAMES.

* Edge & Biometrics: AITalk® micro for IoT, vGate Authentication® for voiceprints, and vGate Aispect® for diagnostics.

* Creator Economy: Lapis Live manages an operational roster of exactly 400 affiliated V-Livers, supported by another subsidiary, Super One Inc.

The firm's human capital moat is precarious. Operating with a core workforce of 110 personnel, the average employee age is 42.8 years, carrying an average tenure of 9.1 years. Most critically, the average annual compensation is capped at $35,368 (5,290k JPY), effectively locking the firm out of the hyper-competitive global generative AI talent market.

HDIN Institutional Verdict

AI, Inc. exhibits extreme balance sheet inefficiency, operating with a zero-leverage structure that dilutes equity returns. The firm hoards $9.87M (1,476,906k JPY) in cash and deposits, comprising 58.0% of its $17.04M total asset base. Interest-bearing debt is virtually non-existent, limited to $0.08M in short-term debt and lease obligations. Physical inventory is statistically immaterial at $0.037M (5,594k JPY).

In response to Tokyo Stock Exchange mandates, governance and investor relations underwent a mechanical overhaul in FY2025. The firm abandoned the traditional Kansayaku system to become a Company with an Audit and Supervisory Committee, concurrently establishing a Nomination & Remuneration Committee. Core board members maintained a 100% attendance rate, participating in 17 out of 17 meetings.

To artificially elevate its +440 basis points ROE expansion (from 0.6% to 5.0%) and +390 basis points ROA expansion (from 0.5% to 4.4%), management executed a 10.0% equity retirement. The cancellation of 700,000 shares reduced the outstanding float from 7,004,298 to 6,304,298 shares. The legacy insider block retained operational dominance, with the principal executive holding 880,000 shares (14.0% of the post-retirement equity). Management simultaneously reinstated a dividend payout of $0.0267 (4.00 JPY) per share. Measured against the consolidated EPS of 17.77 JPY, this represents a 22.5% payout ratio. The firm explicitly formalized a target of achieving a 10% Return on Equity by FY2029 ("2029 ROE 10%").

However, structural working capital asymmetries will continuously drag on this 10% ROE target. The Cash Conversion Cycle (CCC) sits at 55.6 days. While Days Inventory Outstanding (DIO) is 2.3 days, the firm faces a Days Sales Outstanding (DSO) of 66.9 days due to standard B2B enterprise collection cycles. Conversely, weak upstream bargaining power forces the company to settle Trade Payables of $0.22M (32,555k JPY) at a rapid Days Payable Outstanding (DPO) of just 13.6 days. Unless AI, Inc. can structurally renegotiate its fixed royalty demands to NTT and Cerence, or scale its CRM subscriptions past point-in-time custom development, operating margin targets will remain mathematically constrained.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating cash flow contracted -24.4% to $0.51M despite a +24.5% revenue expansion, driven by a +615% working capital surge in unbilled contract assets.

* Confined to Bunkyo-ku, Tokyo, the firm holds zero operational exposure in Taiwan or China, generating over 90% of revenue domestically.

* Management executed a 10.0% equity retirement of 700,000 shares to optimize yields against a heavily underutilized $9.87M zero-leverage cash stockpile.

Figure Al Inc FY2025 Strategic Performance Audit: High-Growth Revenue vs Structural Margin Constraints

Segmental Realities and Margin CompressionAI, Inc. presents a contradictory financial profile wherein a +24.5% top-line expansion to $12.37M (1,850.06M JPY) masks deteriorating earnings quality. While Gross Margin expanded +230 basis points to 52.7%, yielding a Gross Profit of $6.52M as Cost of Goods Sold (COGS) advanced at a slower +18.6% to $5.84M (874.28M JPY), the underlying operating efficiency reversed. Total Selling, General & Administrative (SG&A) expenses accelerated by +36.7% from $4.28M (640.15M JPY) to $5.85M (875.22M JPY). This inorganic bloat, driven primarily by external integrations, caused SG&A to consume 47.3% of total revenue. Consequently, Operating Income compressed -7.8% from $0.73M to $0.67M (100,554k JPY), driving Operating Margins down -190 basis points from 7.3% to 5.4%.

The reported Net Income explosion of +607.2% from $0.10M to $0.74M was structurally subsidized by non-operating accounting levers rather than operational scaling. The bottom line was propped up by $0.33M (50,094k JPY) in Extraordinary Income. Simultaneously, the firm recorded a $0.15M (22,564k JPY) Extraordinary Loss tied to impairment, alongside an additional $0.08M (11,538k JPY) drag in Non-Operating Expenses.

The divergence between optical profitability and liquidity is severe. Operating Cash Flow (OCF) contracted -24.4% from $0.68M to $0.51M, while Free Cash Flow (FCF) fell -16.5% from $0.40M to $0.33M. This contraction originates from a massive working capital anomaly: Contract Assets (unbilled receivables) surged +615% from $0.05M (7,285k JPY) to $0.35M (52,114k JPY). Concurrently, Contract Liabilities (Deferred Revenue) stagnated, declining marginally from $0.85M (126,903k JPY) to $0.84M (126,314k JPY), confirming an absence of scalable recurring subscriptions.

*FY2025 Segmental Revenue Architecture (Fixed conversion applied: 1 USD = 149.5686 JPY)*

* Corporate Voice Products: $6.72M (54.3% of total) via B2B integration.

* Consumer Voice Products: $4.29M (34.6% of total) via B2C/D2C channels.

* Other (Voice Business): $0.90M (7.3% of total) via subsidiary operations.

* CRM Business (Visionary Cloud): $0.46M / 69,324k JPY (3.7% of total).

* Total Consolidated Revenue: $12.37M (100.0%). The legacy Voice Business segment accounts for $11.91M (1,780.73M JPY).

Customer concentration metrics reflect high revenue volatility. AI, Inc. holds Accounts Receivable of $1.92M (287,023k JPY), down from $2.06M, carrying a microscopic Allowance for Doubtful Accounts of $4,178 (625k JPY), representing just 0.21% of the trade balance. However, the top FY2024 client, which historically provided 14.9% of revenue, collapsed to a 4.2% contribution. A new top client emerged in FY2025, generating 11.3% of total sales, equivalent to $1.40M (208,757k JPY).

Management's forward-looking guidance under its Medium-Term Management Plan targets $10.70M (1,600M JPY) in revenue and a 13.5% Operating Margin by FY2027, figures structurally at odds with the current 5.4% margin reality.

Infrastructure Layout and Regional Moats

AI, Inc. operates a highly concentrated geographic footprint, managing its core engineering and R&D hub strictly from its headquarters in Bunkyo-ku, Tokyo, Japan. Over 90% of its external sales and property, plant, and equipment (PP&E) are domiciled within Japan. The firm actively omits further geographic segment disclosures, confirming zero outbound commercial manufacturing or localized operations in Taiwan or China.

The company's intellectual property architecture relies heavily on upstream licensing alliances to bypass exhaustive organic R&D. While AI, Inc. deploys proprietary Deep Neural Network architectures via AITalk®6 and AITalk®5, core capabilities are externalized. Speech recognition (ASR) is licensed from NTT TechnoCross Corporation, ATR-Promotions, and the National Institute of Information and Communications Technology (NICT). Multi-lingual synthesis depends on agreements with Cerence B.V.

Internal product commercialization velocity is decelerating. Capitalized Software plummeted from $0.36M to $0.11M (15,754k JPY), while Software in progress sits at an anemic $0.027M (4,099k JPY). R&D expenses embedded within SG&A rose +26.4% to $0.83M (123.42M JPY). Furthermore, total Capital Expenditure (CapEx) dropped -35.7% from $0.28M to $0.18M. Instead of organic capitalization, AI, Inc. is substituting proprietary engineering with inorganic scale, carrying $3.78M (565,568k JPY) in Goodwill on its balance sheet. Amortization of Goodwill exploded +202% year-over-year from $0.18M (26.82M JPY) to $0.54M (81.03M JPY), driven by the acquisitions of domestic subsidiaries ATR-Trek and Lapis Live.

The product suite is heavily fragmented across multiple silos:

* B2B & Cloud APIs: AITalk WebAPI, AICloud, AITalk Custom Voice, and the Visionary Cloud CRM platform.

* D2C Packaged IP: A.I.VOICE, A.I.VOICE2, VOICEROID, and A.I.VOICE for GAMES.

* Edge & Biometrics: AITalk® micro for IoT, vGate Authentication® for voiceprints, and vGate Aispect® for diagnostics.

* Creator Economy: Lapis Live manages an operational roster of exactly 400 affiliated V-Livers, supported by another subsidiary, Super One Inc.

The firm's human capital moat is precarious. Operating with a core workforce of 110 personnel, the average employee age is 42.8 years, carrying an average tenure of 9.1 years. Most critically, the average annual compensation is capped at $35,368 (5,290k JPY), effectively locking the firm out of the hyper-competitive global generative AI talent market.

HDIN Institutional Verdict

AI, Inc. exhibits extreme balance sheet inefficiency, operating with a zero-leverage structure that dilutes equity returns. The firm hoards $9.87M (1,476,906k JPY) in cash and deposits, comprising 58.0% of its $17.04M total asset base. Interest-bearing debt is virtually non-existent, limited to $0.08M in short-term debt and lease obligations. Physical inventory is statistically immaterial at $0.037M (5,594k JPY).

In response to Tokyo Stock Exchange mandates, governance and investor relations underwent a mechanical overhaul in FY2025. The firm abandoned the traditional Kansayaku system to become a Company with an Audit and Supervisory Committee, concurrently establishing a Nomination & Remuneration Committee. Core board members maintained a 100% attendance rate, participating in 17 out of 17 meetings.

To artificially elevate its +440 basis points ROE expansion (from 0.6% to 5.0%) and +390 basis points ROA expansion (from 0.5% to 4.4%), management executed a 10.0% equity retirement. The cancellation of 700,000 shares reduced the outstanding float from 7,004,298 to 6,304,298 shares. The legacy insider block retained operational dominance, with the principal executive holding 880,000 shares (14.0% of the post-retirement equity). Management simultaneously reinstated a dividend payout of $0.0267 (4.00 JPY) per share. Measured against the consolidated EPS of 17.77 JPY, this represents a 22.5% payout ratio. The firm explicitly formalized a target of achieving a 10% Return on Equity by FY2029 ("2029 ROE 10%").

However, structural working capital asymmetries will continuously drag on this 10% ROE target. The Cash Conversion Cycle (CCC) sits at 55.6 days. While Days Inventory Outstanding (DIO) is 2.3 days, the firm faces a Days Sales Outstanding (DSO) of 66.9 days due to standard B2B enterprise collection cycles. Conversely, weak upstream bargaining power forces the company to settle Trade Payables of $0.22M (32,555k JPY) at a rapid Days Payable Outstanding (DPO) of just 13.6 days. Unless AI, Inc. can structurally renegotiate its fixed royalty demands to NTT and Cerence, or scale its CRM subscriptions past point-in-time custom development, operating margin targets will remain mathematically constrained.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."