Terumo Corporation: B2B CDMO Integration and U.K. Acquisitions Drive Leverage as M&A Execution Signals Near-Term Free Cash Flow Contraction

Date : 2026-06-25

Reading : 89

HDIN Executive Takeaways

* Currency depreciation masked operational margin compression; a 157-basis-point drop in gross margins (from 54.1% to 52.5%) was offset by foreign exchange tailwinds, which mathematically accounted for 59% of the $3,975.9 million FY2025 gross profit growth.

* Aggressive inorganic expansion via the $1,542 million OrganOx Limited acquisition skewed the balance sheet, generating $977.9 million in allocated goodwill and driving near-term free cash flow negative to -$757.2 million.

* Management absorbed direct financial penalties; a 90.9% operating profit target execution rate and a 130-basis-point ROIC underperformance triggered downward compensation adjustments under a rigorously disciplined governance matrix.

Figure Terumo Corporation 2025 Operational & Financial Architecture

Segmental Realities and Capital Allocation Mechanics

Segmental Realities and Capital Allocation Mechanics

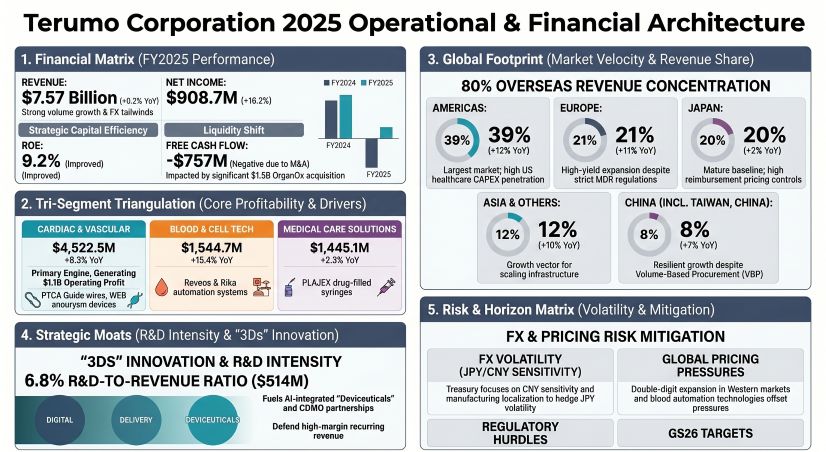

Terumo Corporation [TYO: 4543] exhibited robust top-line momentum juxtaposed against capital efficiency contraction, driven by aggressive inorganic deployment. Consolidated revenue reached $7,567.6 million (1,131,877 million JPY), representing a 9.2% YoY growth and exceeding the initial forecast of $7,020.2 million (1,050.0 billion JPY) at a 107.8% achievement rate. However, profitability targets missed expectations; against an initial operating profit target of $1,297.1 million (194.0 billion JPY), the company delivered $1,178.9 million (176.3 billion JPY), a 90.9% achievement rate.

Core operating profit stood at $1,466.7 million (219,369 million JPY), expanding 7.8% YoY, while reported operating profit reached $1,191.8 million (178,252 million JPY), a 15.3% YoY expansion. Profit attributable to owners of the parent was $908.7 million (135,914 million JPY), up 16.2% YoY. Management offset a 157-basis-point gross margin contraction (settling at 52.5%) by compressing the SG&A-to-revenue ratio from 36.8% to 36.2%, with SG&A expenses totaling $2,740.8 million.

Working capital efficiency reflects a structurally heavy Cash Conversion Cycle (CCC) of 236 days, anchored by 228 Days Inventory Outstanding (DIO) on $2,244.0 million in inventory against $3,591.7 million in COGS. Days Sales Outstanding (DSO) stood at 69 days on $1,437.0 million in trade receivables, while Days Payable Outstanding (DPO) rested at 61 days on $600.1 million in trade payables.

* Cardiac and Vascular Company: Generated $4,522.5 million (676,421 million JPY), an 8.3% YoY expansion, yielding $1,096.4 million (163,994 million JPY) in operating profit. Driven by the "Runthrough NS Izanai" PTCA guidewire and the "WEB" intrasaccular aneurysm embolization device. Segment R&D allocation consumed $360.37 million (53.9 billion JPY), approximately 70% of the total R&D budget.

* Medical Care Solutions Company: Generated $1,445.1 million (216,138 million JPY), achieving 2.3% YoY growth, with an operating profit of $144.2 million (21,568 million JPY). Sustained by the "PLAJEX" drug-filled syringe and "Terufusion Syringe Pump". Segment R&D allocation was $66.19 million (9.9 billion JPY).

* Blood and Cell Technologies (BCT) Company: Generated $1,544.7 million (231,037 million JPY), the highest velocity segment at 15.4% YoY growth, delivering $224.9 million (33,635 million JPY) in operating profit. Growth relied on the "Reveos" automated system and "Rika" source plasma collection system. Segment R&D allocation was $72.21 million (10.8 billion JPY).

* Basic Research and Corporate Allocations: Accounted for $12.03 million (1.8 billion JPY) of the $514.15 million (76.9 billion JPY) total consolidated R&D expenditure, representing a 6.8% R&D-to-revenue ratio.

The balance sheet capitalization expanded to $15,459.3 million (2,312,234 million JPY) in total assets and $10,593.9 million (1,584,509 million JPY) in total equity, contracting the equity ratio from 74.8% to 68.5%. Strategic M&A drove investing cash flow to a -$2,300.6 million (-344,102 million JPY) outflow, overpowering the $1,543.5 million (230,852 million JPY) operating cash flow and plunging free cash flow to -$757.2 million (-113,249 million JPY). To bridge this, short-term bonds and borrowings spiked from $100.3 million to $1,871.3 million (279,886 million JPY), pushing total interest-bearing debt to $2,539.3 million (a 24.0% Debt-to-Equity ratio), while non-current debt decreased to $668.0 million (99,910 million JPY). Dividends totaled $276.1 million at 30.00 JPY per share.

Supply Chain Architecture and Regional Moats

Terumo Corporation operates a globally decentralized supply chain to mitigate foreign exchange mismatch and navigate centralized pricing frameworks such as volume-based procurement (VBP). The operational footprint generates 80% of revenue overseas, distributed across the Americas (39% / $2,964.5 million / 443,400 million JPY at 12% YoY growth), Europe (21% / $1,622.7 million / 242,700 million JPY at 11% YoY growth), Asia/Others (12% / $881.9 million / 131,900 million JPY at 10% YoY growth), and China (8% / $610.4 million / 91,300 million JPY at 7% YoY growth). Japan functions as a mature baseline, producing 20% of sales ($1,488.3 million / 222,600 million JPY at 2% YoY growth).

To counter a structural JPY cost-base mismatch, treasury utilizes forward exchange contracts and cross-currency interest rate swaps. Under a mandated 1 USD = 149.5686 JPY conversion metric, treasury models report that a 1% currency appreciation impacts Profit Before Tax (PBT) most heavily via the Chinese Yuan (CNY) at +$2.19 million (+328 million JPY), followed by the Euro (EUR) at +$1.89 million (+283 million JPY) and the US Dollar (USD) at +$1.76 million (+264 million JPY). Original Growth Strategy 2026 ("GS26") capital metrics were conservatively modeled against a baseline of 107 JPY/USD and 128 JPY/EUR.

Manufacturing and value generation nodes are geo-strategically segmented. Asian output is managed via Terumo Clinical Supply Co., Ltd. and Terumo Yamaguchi D&D Corporation in Japan, alongside Terumo Medical Products Hangzhou Co., Ltd. in China, Terumo Philippines Corp., and Terumo Vietnam Co., Ltd. The Americas rely on Terumo Medical Corp., MicroVention, Inc., Bolton Medical, Inc., and Terumo BCT, Inc. European infrastructure is anchored by Terumo Europe N.V. and the newly integrated OrganOx Limited hub.

The global pipeline relies heavily on the "3Ds" strategic pillars (Delivery, Digital, Deviceuticals) developed within the Discovery and Technology Center of Terumo (D-TECT). Cardiovascular clinical advances include OPUSWAVE, DualView, OFDI, IVUS, and the Kanshas (200cm) and Unicoat proprietary coatings. Regulatory agility ensures compliance with FDA 510(k) and European MDR parameters, securing approvals for the OneView system. Medical Care pipelines focus on PIVC, PICC, and Midela, while BCT advances cell therapies via the Quantum Flex bioreactor, supported by the Lumia system. Development targets rely on joint external clinical execution with the Center for iPS Cell Research and Application (CiRA) at Kyoto University, the Japan Agency for Medical Research and Development (AMED), and the National Institutes of Health (NIH). Contract Development and Manufacturing Organization (CDMO) scaling—governed strictly by Good Manufacturing Practice (GMP) compliance—is executed via a core B2B pharmaceutical partnership with WuXi Biologics.

HDIN Institutional Verdict

The board matrix—reinforced by CPAs with global EY audit experience and independent outside directors comprising over 50% of the Audit and Supervisory Committee—enforces a ruthless quantitative executive compensation structure. Remuneration is strictly tied to Restricted Stock (RS) and short-term metrics weighted at 40% for Revenue, 40% for Operating Profit, 10% for Return on Invested Capital (ROIC), and 10% for Return on Equity (ROE). Despite record top-line revenue, the capital-intensive OrganOx M&A diluted ROIC to 7.5% against an 8.8% target (a 130-basis-point deviation) and ROE to 9.2% against a 10.1% target (a 90-basis-point deviation). Management structurally absorbed these penalties, receiving a 94.0% corporate financial achievement payout, while non-financial future corporate value goals yielded scores of 102.8% for the CEO and 96.0% to 112.5% for functional directors.

This executive penalty underscores the near-term bottom-line drag of securing the Normothermic Machine Perfusion (NMP) technological monopoly. The OrganOx integration required $1,542.0 million (230,632 million JPY) in cash consideration against a net tangible asset base of just $24.3 million. This generated $1,501.5 million (224,576 million JPY) in goodwill. Since acquisition, OrganOx added $24.3 million (3,641 million JPY) to top-line revenue but contributed a net quarterly loss of -$3.8 million (-570 million JPY). Pro-forma modeling indicates that a full-year integration would yield $76.0 million (11,363 million JPY) in revenue alongside a -$30.2 million (-4,520 million JPY) net operational loss.

The broader balance sheet carries severe valuation risk. Goodwill ballooned to $3,150.2 million (471,166 million JPY) and Intangible Assets reached $5,371.5 million (803,410 million JPY), pooling a combined inorganic asset base of $8,521.7 million. BCT carries $1,188.6 million (177,769 million JPY) in goodwill (flagged as a Key Audit Matter operating on an extended 8-year business plan), while OrganOx carries an allocated $977.9 million (146,265 million JPY), MicroVention carries $292.6 million (43,770 million JPY), and Bolton Medical carries $79.8 million (11,935 million JPY). Evaluated under pre-tax discount rates of 9.7% to 14.4% and permanent growth rates of 1.8% to 2.3%, these Cash-Generating Units are acutely sensitive to weighted average cost of capital (WACC) shifts. Management explicitly warns that the Pharmaceutical Solutions segment faces mandatory impairment if the pre-tax discount rate breaches 7.0% or the permanent growth rate falls below 0.4%, an acute vulnerability highlighted by a localized $12.6 million (1,882 million JPY) Americas cardiovascular R&D impairment recognized this fiscal year.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Currency depreciation masked operational margin compression; a 157-basis-point drop in gross margins (from 54.1% to 52.5%) was offset by foreign exchange tailwinds, which mathematically accounted for 59% of the $3,975.9 million FY2025 gross profit growth.

* Aggressive inorganic expansion via the $1,542 million OrganOx Limited acquisition skewed the balance sheet, generating $977.9 million in allocated goodwill and driving near-term free cash flow negative to -$757.2 million.

* Management absorbed direct financial penalties; a 90.9% operating profit target execution rate and a 130-basis-point ROIC underperformance triggered downward compensation adjustments under a rigorously disciplined governance matrix.

Figure Terumo Corporation 2025 Operational & Financial Architecture

Segmental Realities and Capital Allocation MechanicsTerumo Corporation [TYO: 4543] exhibited robust top-line momentum juxtaposed against capital efficiency contraction, driven by aggressive inorganic deployment. Consolidated revenue reached $7,567.6 million (1,131,877 million JPY), representing a 9.2% YoY growth and exceeding the initial forecast of $7,020.2 million (1,050.0 billion JPY) at a 107.8% achievement rate. However, profitability targets missed expectations; against an initial operating profit target of $1,297.1 million (194.0 billion JPY), the company delivered $1,178.9 million (176.3 billion JPY), a 90.9% achievement rate.

Core operating profit stood at $1,466.7 million (219,369 million JPY), expanding 7.8% YoY, while reported operating profit reached $1,191.8 million (178,252 million JPY), a 15.3% YoY expansion. Profit attributable to owners of the parent was $908.7 million (135,914 million JPY), up 16.2% YoY. Management offset a 157-basis-point gross margin contraction (settling at 52.5%) by compressing the SG&A-to-revenue ratio from 36.8% to 36.2%, with SG&A expenses totaling $2,740.8 million.

Working capital efficiency reflects a structurally heavy Cash Conversion Cycle (CCC) of 236 days, anchored by 228 Days Inventory Outstanding (DIO) on $2,244.0 million in inventory against $3,591.7 million in COGS. Days Sales Outstanding (DSO) stood at 69 days on $1,437.0 million in trade receivables, while Days Payable Outstanding (DPO) rested at 61 days on $600.1 million in trade payables.

* Cardiac and Vascular Company: Generated $4,522.5 million (676,421 million JPY), an 8.3% YoY expansion, yielding $1,096.4 million (163,994 million JPY) in operating profit. Driven by the "Runthrough NS Izanai" PTCA guidewire and the "WEB" intrasaccular aneurysm embolization device. Segment R&D allocation consumed $360.37 million (53.9 billion JPY), approximately 70% of the total R&D budget.

* Medical Care Solutions Company: Generated $1,445.1 million (216,138 million JPY), achieving 2.3% YoY growth, with an operating profit of $144.2 million (21,568 million JPY). Sustained by the "PLAJEX" drug-filled syringe and "Terufusion Syringe Pump". Segment R&D allocation was $66.19 million (9.9 billion JPY).

* Blood and Cell Technologies (BCT) Company: Generated $1,544.7 million (231,037 million JPY), the highest velocity segment at 15.4% YoY growth, delivering $224.9 million (33,635 million JPY) in operating profit. Growth relied on the "Reveos" automated system and "Rika" source plasma collection system. Segment R&D allocation was $72.21 million (10.8 billion JPY).

* Basic Research and Corporate Allocations: Accounted for $12.03 million (1.8 billion JPY) of the $514.15 million (76.9 billion JPY) total consolidated R&D expenditure, representing a 6.8% R&D-to-revenue ratio.

The balance sheet capitalization expanded to $15,459.3 million (2,312,234 million JPY) in total assets and $10,593.9 million (1,584,509 million JPY) in total equity, contracting the equity ratio from 74.8% to 68.5%. Strategic M&A drove investing cash flow to a -$2,300.6 million (-344,102 million JPY) outflow, overpowering the $1,543.5 million (230,852 million JPY) operating cash flow and plunging free cash flow to -$757.2 million (-113,249 million JPY). To bridge this, short-term bonds and borrowings spiked from $100.3 million to $1,871.3 million (279,886 million JPY), pushing total interest-bearing debt to $2,539.3 million (a 24.0% Debt-to-Equity ratio), while non-current debt decreased to $668.0 million (99,910 million JPY). Dividends totaled $276.1 million at 30.00 JPY per share.

Supply Chain Architecture and Regional Moats

Terumo Corporation operates a globally decentralized supply chain to mitigate foreign exchange mismatch and navigate centralized pricing frameworks such as volume-based procurement (VBP). The operational footprint generates 80% of revenue overseas, distributed across the Americas (39% / $2,964.5 million / 443,400 million JPY at 12% YoY growth), Europe (21% / $1,622.7 million / 242,700 million JPY at 11% YoY growth), Asia/Others (12% / $881.9 million / 131,900 million JPY at 10% YoY growth), and China (8% / $610.4 million / 91,300 million JPY at 7% YoY growth). Japan functions as a mature baseline, producing 20% of sales ($1,488.3 million / 222,600 million JPY at 2% YoY growth).

To counter a structural JPY cost-base mismatch, treasury utilizes forward exchange contracts and cross-currency interest rate swaps. Under a mandated 1 USD = 149.5686 JPY conversion metric, treasury models report that a 1% currency appreciation impacts Profit Before Tax (PBT) most heavily via the Chinese Yuan (CNY) at +$2.19 million (+328 million JPY), followed by the Euro (EUR) at +$1.89 million (+283 million JPY) and the US Dollar (USD) at +$1.76 million (+264 million JPY). Original Growth Strategy 2026 ("GS26") capital metrics were conservatively modeled against a baseline of 107 JPY/USD and 128 JPY/EUR.

Manufacturing and value generation nodes are geo-strategically segmented. Asian output is managed via Terumo Clinical Supply Co., Ltd. and Terumo Yamaguchi D&D Corporation in Japan, alongside Terumo Medical Products Hangzhou Co., Ltd. in China, Terumo Philippines Corp., and Terumo Vietnam Co., Ltd. The Americas rely on Terumo Medical Corp., MicroVention, Inc., Bolton Medical, Inc., and Terumo BCT, Inc. European infrastructure is anchored by Terumo Europe N.V. and the newly integrated OrganOx Limited hub.

The global pipeline relies heavily on the "3Ds" strategic pillars (Delivery, Digital, Deviceuticals) developed within the Discovery and Technology Center of Terumo (D-TECT). Cardiovascular clinical advances include OPUSWAVE, DualView, OFDI, IVUS, and the Kanshas (200cm) and Unicoat proprietary coatings. Regulatory agility ensures compliance with FDA 510(k) and European MDR parameters, securing approvals for the OneView system. Medical Care pipelines focus on PIVC, PICC, and Midela, while BCT advances cell therapies via the Quantum Flex bioreactor, supported by the Lumia system. Development targets rely on joint external clinical execution with the Center for iPS Cell Research and Application (CiRA) at Kyoto University, the Japan Agency for Medical Research and Development (AMED), and the National Institutes of Health (NIH). Contract Development and Manufacturing Organization (CDMO) scaling—governed strictly by Good Manufacturing Practice (GMP) compliance—is executed via a core B2B pharmaceutical partnership with WuXi Biologics.

HDIN Institutional Verdict

The board matrix—reinforced by CPAs with global EY audit experience and independent outside directors comprising over 50% of the Audit and Supervisory Committee—enforces a ruthless quantitative executive compensation structure. Remuneration is strictly tied to Restricted Stock (RS) and short-term metrics weighted at 40% for Revenue, 40% for Operating Profit, 10% for Return on Invested Capital (ROIC), and 10% for Return on Equity (ROE). Despite record top-line revenue, the capital-intensive OrganOx M&A diluted ROIC to 7.5% against an 8.8% target (a 130-basis-point deviation) and ROE to 9.2% against a 10.1% target (a 90-basis-point deviation). Management structurally absorbed these penalties, receiving a 94.0% corporate financial achievement payout, while non-financial future corporate value goals yielded scores of 102.8% for the CEO and 96.0% to 112.5% for functional directors.

This executive penalty underscores the near-term bottom-line drag of securing the Normothermic Machine Perfusion (NMP) technological monopoly. The OrganOx integration required $1,542.0 million (230,632 million JPY) in cash consideration against a net tangible asset base of just $24.3 million. This generated $1,501.5 million (224,576 million JPY) in goodwill. Since acquisition, OrganOx added $24.3 million (3,641 million JPY) to top-line revenue but contributed a net quarterly loss of -$3.8 million (-570 million JPY). Pro-forma modeling indicates that a full-year integration would yield $76.0 million (11,363 million JPY) in revenue alongside a -$30.2 million (-4,520 million JPY) net operational loss.

The broader balance sheet carries severe valuation risk. Goodwill ballooned to $3,150.2 million (471,166 million JPY) and Intangible Assets reached $5,371.5 million (803,410 million JPY), pooling a combined inorganic asset base of $8,521.7 million. BCT carries $1,188.6 million (177,769 million JPY) in goodwill (flagged as a Key Audit Matter operating on an extended 8-year business plan), while OrganOx carries an allocated $977.9 million (146,265 million JPY), MicroVention carries $292.6 million (43,770 million JPY), and Bolton Medical carries $79.8 million (11,935 million JPY). Evaluated under pre-tax discount rates of 9.7% to 14.4% and permanent growth rates of 1.8% to 2.3%, these Cash-Generating Units are acutely sensitive to weighted average cost of capital (WACC) shifts. Management explicitly warns that the Pharmaceutical Solutions segment faces mandatory impairment if the pre-tax discount rate breaches 7.0% or the permanent growth rate falls below 0.4%, an acute vulnerability highlighted by a localized $12.6 million (1,882 million JPY) Americas cardiovascular R&D impairment recognized this fiscal year.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."