Asahi Kasei Corporation: Strategic Health Care Pivot Near North American and European Hubs as 32.4% EBITDA Expansion Signals Structural Recovery

Date : 2026-06-26

Reading : 139

HDIN Executive Takeaways

* Core operations triggered a definitive profitability recovery, expanding consolidated EBITDA by 32.4% to $2.86 billion in FY2026, driven by an aggressive 4.9% headcount compression and structural pricing power in specialized sub-segments.

* The global manufacturing architecture is pivoting from legacy Asian petrochemical nodes to high-margin Western healthcare hubs, leveraging intellectual property lifecycles to secure $267.4 million in isolated annual revenue from single drug lines.

* Board-level capital allocation mandates an $8.02 billion medium-term deployment strategy enforcing a strict 80/20 investment-to-shareholder return ratio, constrained by a penalizing $100.29/t-CO2 internal carbon pricing threshold.

Figure Strategic Transformation & Financial Recovery: Asahi Kasei Corp FY2022-FY2026 Assessment

Segmental Realities and Margin Dynamics

Segmental Realities and Margin Dynamics

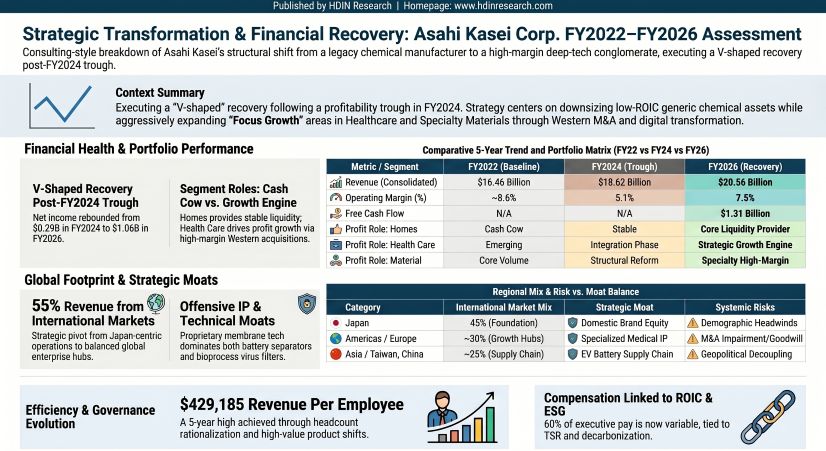

Asahi Kasei Corporation [TYO: 3407] executed a V-shaped financial recovery following a severe earnings compression in FY2024. Consolidated revenue expanded from $16.46 billion in FY2022 to $20.56 billion in FY2026, representing a 4-year Compound Annual Growth Rate (CAGR) of 5.7%. Net income troughed at $0.29 billion in FY2024 before expanding to $0.90 billion in FY2025 and $1.06 billion in FY2026. This bottom-line velocity corresponds with an EBITDA expansion from $2.16 billion in FY2024 to $2.86 billion in FY2026.

Operating leverage and structural product mix shifts drove precise margin expansions. Gross margin increased from 31.5% in FY2025 to 32.8% in FY2026. Simultaneously, the Operating Margin (OM) recovered from 5.1% in FY2024 to 7.0% in FY2025, reaching 7.5% by FY2026. Net margin mirrored this trajectory, shifting from 1.6% in FY2024 to 5.2% in FY2026.

Segmental performance highlights a deliberate capital rotation away from asset-heavy legacy operations:

* Homes (Cash Generator): Targeting Japan's premium domestic B2C sector (Hebel Haus, ZEH) and B2B markets in the Americas and Australia (Synergos, Erickson, NEX Building Group). Segment revenue expanded from $6.93 billion in FY2025 to $7.20 billion in FY2026. Operating profit increased from $0.64 billion to $0.67 billion.

* Health Care (Inorganic Growth Engine): Driven by M&A, revenue expanded by 7.7% from $4.12 billion in FY2025 to $4.44 billion in FY2026. Operating profit expanded by roughly 30% from $0.43 billion to $0.56 billion over the same interval.

* Material (Reform Target): Management is reducing exposure to generic chemicals by 70%. Consequently, revenue contracted from $9.15 billion in FY2025 to $8.73 billion in FY2026, with operating profit dropping from $0.53 billion to $0.46 billion. R&D ratios remain disciplined at roughly 3.6%, matching $739.7 million in FY2025 and $739.0 million in FY2026 to support specialized product lines.

Capital efficiency metrics lag management's optimal projections due to balance sheet inflation from heavy intangible asset acquisition. Return on Equity (ROE) shifted from 2.5% in FY2024 to 7.4% in FY2025 and 8.0% in FY2026, trailing the >12% FY2030 target. Return on Invested Capital (ROIC) stalled, hovering at 5.9% in FY2024, dipping to 5.5% in FY2025, and returning to 5.9% in FY2026. Management explicitly targets a 6% ROIC by FY2027 and >8% by FY2030, alongside an operating profit roadmap of $1.81 billion (¥270 billion) in FY2027 expanding to $2.54 billion (¥380 billion) by FY2030.

Total assets expanded from $22.39 billion in FY2022 to $27.67 billion in FY2026. Consequently, asset turnover declined from 0.79x in FY2023 to 0.74x in FY2026. Working capital metrics exhibit extreme resilience: the allowance for doubtful accounts remained flat at $25.4 million (¥3,805 million) in FY2025 and $25.5 million (¥3,809 million) in FY2026. Off-balance sheet contingent liabilities related to Homes financial guarantees were de-risked by 25.9%, dropping from $283.0 million (¥42,331 million) in FY2025 to $209.7 million (¥31,363 million) in FY2026.

Balance Sheet Architecture and Capital Allocation

Free Cash Flow (FCF) converted from a deficit of -$0.53 billion in FY2025 (pressured by -$2.55 billion in investing cash outflows) to a robust $1.31 billion in FY2026, supported by $2.03 billion in Operating Cash Flow. The Debt-to-Equity (D/E) ratio compressed rapidly from 0.62 in FY2025 to 0.46 in FY2026, resting strictly below management's 0.7 risk ceiling.

Under the "TrailBlaze Together 2027" strategy, total projected cash inflows of $8.02 billion (¥1.2 trillion) will adhere to an 80/20 allocation mandate. Roughly 80% ($6.42 billion) is strictly earmarked for investment, against a budgeted Total CapEx of $6.22 billion (¥930 billion)—of which $4.01 billion (¥600 billion) targets Focus Growth expansion. The remaining 20% ($1.60 billion) secures shareholder returns. Utilizing a Dividend on Equity (DOE) threshold, Dividends Per Share (DPS) scaled from ¥36 in FY2024, to ¥38 in FY2025, reaching ¥42 in FY2026, covering an annual obligation of approximately $200 million (¥29.9 billion). The Board authorized tactical share repurchases of up to $267.4 million (¥40 billion) covering 40 million shares between November 2025 and October 2026. Over the past five years, cross-shareholdings of listed stocks were systematically unwound by 70%, liberating $1.2 billion (¥180 billion) in trapped capital.

Pension obligations transitioned from a net liability to an overfunded asset. The Projected Benefit Obligation (PBO) of $1,843.7 million (¥275,763 million) was surpassed by $1,849.9 million (¥276,692 million) in Plan Assets, establishing a net asset position of $6.2 million (¥929 million) at a discount rate of 2.0% to 2.9%.

Infrastructure Layout and Geographic Rebalancing

Asahi Kasei is systematically transferring asset weight from Asia to high-value western corridors. Domestically, the company executed the cessation of ethylene production at the Mizushima plant. To correct asset-to-cash-flow imbalances, management triggered total specific fixed asset impairments in the Material segment reaching $72.5 million (¥10,849 million). Regional manufacturing rationalization generated targeted write-downs in Kentucky, U.S.A. at $21.6 million (¥3,228 million) in FY2025 and $4.3 million (¥645 million) in FY2026; in Hung Yen Province, Vietnam at $11.0 million (¥1,641 million) in FY2026; and in Pyeongtaek, Korea at $6.5 million (¥975 million) in FY2025. Restructuring friction extended to joint ventures, where the withdrawal from PTT Asahi Chemical Co., Ltd. (a JV with PTT Global Chemical) registered losses of $66.0 million (¥9,877 million) in FY2025 and $39.4 million (¥5,898 million) in FY2026.

Simultaneously, the firm localized intellectual property within acquired Western entities, primarily operating out of Fremont, California (Bionova Scientific); Massachusetts (ZOLL Medical); North Carolina (Veloxis Pharmaceuticals and Polypore International); and Stockholm, Sweden (Calliditas Therapeutics AB). Independent auditors subjected these entities to rigorous Key Audit Matter (KAM) testing against goodwill carrying amounts: Asahi Kasei Battery Separator Corp at $641.6 million (¥95,963 million); Bionova Scientific, LLC at $355.1 million (¥53,108 million); and Polypore International, LLC at $198.6 million (¥29,705 million).

The technology pipeline relies on joint ventures and Corporate Venture Capital (CVC). A core alliance with a premier automotive OEM resulted in the Asahi Kasei Honda Battery Separator Corporation. Advanced semiconductor IP (AlN, GaN, SiC, GaN HEMT) and UV-C Laser Diode (LD) commercialization is actively pursued, evidenced by the 2025 ULTEC internal spin-off. CVC acquisitions targeting "missing parts" secured Anion-Exchange Membrane (AEM) technology via Ionomr Innovations Inc. (Dec 2023) and aerospace capabilities via EAS Batteries. European circularity mandates enforce supply chain shifts, leading to the RevoLefin project (targeting 2034) and localized alliances with Nobian Industrial Chemicals B.V. and Mastermelt Ltd.

Corporate Efficiency and Climate Economics

Operational efficiency metrics executed a definitive rebound driven by a systematic headcount compression. Consolidated headcount peaked at 50,352 in FY2025 before contracting by 4.9% to 47,895 in FY2026. Consequently, revenue per employee accelerated from $352,000 across 46,751 employees in FY2022, to $377,700 across 49,295 employees in FY2024, peaking at $429,185 in FY2026. Operating profit per employee troughed at $12,222 in FY2024 before expanding to $32,175 in FY2026, overtaking the FY2022 baseline of $30,331.

Executive governance underwent structural remodeling to bridge principal-agent gaps. The Board is composed of 50% independent directors (4 of 8). Broadly, the firm retains 13 officers, including 7 independent and 3 female officers (a 23% ratio). The Board reallocated boardroom bandwidth, shifting strategy agenda timeshare from 55.4% in FY2023 to 61.7% in FY2025. Executive remuneration shifted from a fixed-heavy model in FY2024 (60.9% base, 27.3% cash bonus, 11.8% stock) to a performance-linked matrix in FY2025 (40% base, 30% cash bonus, 30% stock). Employee vitality is actively quantified via the KSA (Vitality and Growth Assessment) index, targeting a progression from 56.2% in FY2023 to 60.0% by FY2027. The female management ratio advanced from 4.9% in FY2024 to 5.5% in FY2025, anchoring a hard 10.0% mandate by FY2030.

Decarbonization is aggressively monetized and penalized. The firm applied a strict Internal Carbon Pricing (ICP) mechanism at $100.29 per ton of CO2 (¥15,000/t-CO2), effectively forcing subsidiary managers to absorb theoretical taxation on capital requests. Against a 2013 baseline of 5.11 million tons, Scope 1 and 2 GHG emissions contracted by 37% to 3.20 million tons in FY2024. The forward trajectory dictates an absolute ceiling of 3.60 million tons by 2030 (30% reduction) and 3.10 million tons by 2035 (40% reduction), while strict domestic mandates target 46% and 60% reductions over the identical timelines. FY2024 Carbon intensity tracked at 1,500 tons of CO2e per $668,589 (¥100 million) of operating profit.

HDIN Institutional Verdict

Asahi Kasei has successfully stabilized top-line volatility through inorganic Healthcare acquisitions and strict pricing controls, yet the core challenge remains the dilution of capital velocity. The Board's ability to drive a 32.4% EBITDA expansion while excising 4.9% of the global headcount confirms management's operational leverage capabilities. The strategic deployment of an "Offensive IP Strategy" to extend the Teribone exclusivity lifecycle—safeguarding $267.4 million (¥40 billion) in isolated annual sales—provides high-margin downside protection. Furthermore, the explicit target to execute 10 or more new strategic license agreements between FY2025 and FY2027 confirms a transition toward an asset-light royalty model.

However, the drag on ROIC (stalled at 5.9%) exposes the friction of absorbing massive intangible asset loads from entities like ZOLL Medical and Calliditas Therapeutics. Management's medium-term $8.02 billion capital deployment plan is highly credible due to its exact internal hurdle rates, specifically the $100.29/t-CO2 internal penalty. If the firm executes flawless post-merger integrations across its Western hubs and finalizes the 70% phase-out of low-yield legacy materials, the transition from a traditional Japanese chemical conglomerate into an IP-driven, specialized healthcare and deep-tech holding company will fulfill the FY2030 ROE targets.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Core operations triggered a definitive profitability recovery, expanding consolidated EBITDA by 32.4% to $2.86 billion in FY2026, driven by an aggressive 4.9% headcount compression and structural pricing power in specialized sub-segments.

* The global manufacturing architecture is pivoting from legacy Asian petrochemical nodes to high-margin Western healthcare hubs, leveraging intellectual property lifecycles to secure $267.4 million in isolated annual revenue from single drug lines.

* Board-level capital allocation mandates an $8.02 billion medium-term deployment strategy enforcing a strict 80/20 investment-to-shareholder return ratio, constrained by a penalizing $100.29/t-CO2 internal carbon pricing threshold.

Figure Strategic Transformation & Financial Recovery: Asahi Kasei Corp FY2022-FY2026 Assessment

Segmental Realities and Margin DynamicsAsahi Kasei Corporation [TYO: 3407] executed a V-shaped financial recovery following a severe earnings compression in FY2024. Consolidated revenue expanded from $16.46 billion in FY2022 to $20.56 billion in FY2026, representing a 4-year Compound Annual Growth Rate (CAGR) of 5.7%. Net income troughed at $0.29 billion in FY2024 before expanding to $0.90 billion in FY2025 and $1.06 billion in FY2026. This bottom-line velocity corresponds with an EBITDA expansion from $2.16 billion in FY2024 to $2.86 billion in FY2026.

Operating leverage and structural product mix shifts drove precise margin expansions. Gross margin increased from 31.5% in FY2025 to 32.8% in FY2026. Simultaneously, the Operating Margin (OM) recovered from 5.1% in FY2024 to 7.0% in FY2025, reaching 7.5% by FY2026. Net margin mirrored this trajectory, shifting from 1.6% in FY2024 to 5.2% in FY2026.

Segmental performance highlights a deliberate capital rotation away from asset-heavy legacy operations:

* Homes (Cash Generator): Targeting Japan's premium domestic B2C sector (Hebel Haus, ZEH) and B2B markets in the Americas and Australia (Synergos, Erickson, NEX Building Group). Segment revenue expanded from $6.93 billion in FY2025 to $7.20 billion in FY2026. Operating profit increased from $0.64 billion to $0.67 billion.

* Health Care (Inorganic Growth Engine): Driven by M&A, revenue expanded by 7.7% from $4.12 billion in FY2025 to $4.44 billion in FY2026. Operating profit expanded by roughly 30% from $0.43 billion to $0.56 billion over the same interval.

* Material (Reform Target): Management is reducing exposure to generic chemicals by 70%. Consequently, revenue contracted from $9.15 billion in FY2025 to $8.73 billion in FY2026, with operating profit dropping from $0.53 billion to $0.46 billion. R&D ratios remain disciplined at roughly 3.6%, matching $739.7 million in FY2025 and $739.0 million in FY2026 to support specialized product lines.

Capital efficiency metrics lag management's optimal projections due to balance sheet inflation from heavy intangible asset acquisition. Return on Equity (ROE) shifted from 2.5% in FY2024 to 7.4% in FY2025 and 8.0% in FY2026, trailing the >12% FY2030 target. Return on Invested Capital (ROIC) stalled, hovering at 5.9% in FY2024, dipping to 5.5% in FY2025, and returning to 5.9% in FY2026. Management explicitly targets a 6% ROIC by FY2027 and >8% by FY2030, alongside an operating profit roadmap of $1.81 billion (¥270 billion) in FY2027 expanding to $2.54 billion (¥380 billion) by FY2030.

Total assets expanded from $22.39 billion in FY2022 to $27.67 billion in FY2026. Consequently, asset turnover declined from 0.79x in FY2023 to 0.74x in FY2026. Working capital metrics exhibit extreme resilience: the allowance for doubtful accounts remained flat at $25.4 million (¥3,805 million) in FY2025 and $25.5 million (¥3,809 million) in FY2026. Off-balance sheet contingent liabilities related to Homes financial guarantees were de-risked by 25.9%, dropping from $283.0 million (¥42,331 million) in FY2025 to $209.7 million (¥31,363 million) in FY2026.

Balance Sheet Architecture and Capital Allocation

Free Cash Flow (FCF) converted from a deficit of -$0.53 billion in FY2025 (pressured by -$2.55 billion in investing cash outflows) to a robust $1.31 billion in FY2026, supported by $2.03 billion in Operating Cash Flow. The Debt-to-Equity (D/E) ratio compressed rapidly from 0.62 in FY2025 to 0.46 in FY2026, resting strictly below management's 0.7 risk ceiling.

Under the "TrailBlaze Together 2027" strategy, total projected cash inflows of $8.02 billion (¥1.2 trillion) will adhere to an 80/20 allocation mandate. Roughly 80% ($6.42 billion) is strictly earmarked for investment, against a budgeted Total CapEx of $6.22 billion (¥930 billion)—of which $4.01 billion (¥600 billion) targets Focus Growth expansion. The remaining 20% ($1.60 billion) secures shareholder returns. Utilizing a Dividend on Equity (DOE) threshold, Dividends Per Share (DPS) scaled from ¥36 in FY2024, to ¥38 in FY2025, reaching ¥42 in FY2026, covering an annual obligation of approximately $200 million (¥29.9 billion). The Board authorized tactical share repurchases of up to $267.4 million (¥40 billion) covering 40 million shares between November 2025 and October 2026. Over the past five years, cross-shareholdings of listed stocks were systematically unwound by 70%, liberating $1.2 billion (¥180 billion) in trapped capital.

Pension obligations transitioned from a net liability to an overfunded asset. The Projected Benefit Obligation (PBO) of $1,843.7 million (¥275,763 million) was surpassed by $1,849.9 million (¥276,692 million) in Plan Assets, establishing a net asset position of $6.2 million (¥929 million) at a discount rate of 2.0% to 2.9%.

Infrastructure Layout and Geographic Rebalancing

Asahi Kasei is systematically transferring asset weight from Asia to high-value western corridors. Domestically, the company executed the cessation of ethylene production at the Mizushima plant. To correct asset-to-cash-flow imbalances, management triggered total specific fixed asset impairments in the Material segment reaching $72.5 million (¥10,849 million). Regional manufacturing rationalization generated targeted write-downs in Kentucky, U.S.A. at $21.6 million (¥3,228 million) in FY2025 and $4.3 million (¥645 million) in FY2026; in Hung Yen Province, Vietnam at $11.0 million (¥1,641 million) in FY2026; and in Pyeongtaek, Korea at $6.5 million (¥975 million) in FY2025. Restructuring friction extended to joint ventures, where the withdrawal from PTT Asahi Chemical Co., Ltd. (a JV with PTT Global Chemical) registered losses of $66.0 million (¥9,877 million) in FY2025 and $39.4 million (¥5,898 million) in FY2026.

Simultaneously, the firm localized intellectual property within acquired Western entities, primarily operating out of Fremont, California (Bionova Scientific); Massachusetts (ZOLL Medical); North Carolina (Veloxis Pharmaceuticals and Polypore International); and Stockholm, Sweden (Calliditas Therapeutics AB). Independent auditors subjected these entities to rigorous Key Audit Matter (KAM) testing against goodwill carrying amounts: Asahi Kasei Battery Separator Corp at $641.6 million (¥95,963 million); Bionova Scientific, LLC at $355.1 million (¥53,108 million); and Polypore International, LLC at $198.6 million (¥29,705 million).

The technology pipeline relies on joint ventures and Corporate Venture Capital (CVC). A core alliance with a premier automotive OEM resulted in the Asahi Kasei Honda Battery Separator Corporation. Advanced semiconductor IP (AlN, GaN, SiC, GaN HEMT) and UV-C Laser Diode (LD) commercialization is actively pursued, evidenced by the 2025 ULTEC internal spin-off. CVC acquisitions targeting "missing parts" secured Anion-Exchange Membrane (AEM) technology via Ionomr Innovations Inc. (Dec 2023) and aerospace capabilities via EAS Batteries. European circularity mandates enforce supply chain shifts, leading to the RevoLefin project (targeting 2034) and localized alliances with Nobian Industrial Chemicals B.V. and Mastermelt Ltd.

Corporate Efficiency and Climate Economics

Operational efficiency metrics executed a definitive rebound driven by a systematic headcount compression. Consolidated headcount peaked at 50,352 in FY2025 before contracting by 4.9% to 47,895 in FY2026. Consequently, revenue per employee accelerated from $352,000 across 46,751 employees in FY2022, to $377,700 across 49,295 employees in FY2024, peaking at $429,185 in FY2026. Operating profit per employee troughed at $12,222 in FY2024 before expanding to $32,175 in FY2026, overtaking the FY2022 baseline of $30,331.

Executive governance underwent structural remodeling to bridge principal-agent gaps. The Board is composed of 50% independent directors (4 of 8). Broadly, the firm retains 13 officers, including 7 independent and 3 female officers (a 23% ratio). The Board reallocated boardroom bandwidth, shifting strategy agenda timeshare from 55.4% in FY2023 to 61.7% in FY2025. Executive remuneration shifted from a fixed-heavy model in FY2024 (60.9% base, 27.3% cash bonus, 11.8% stock) to a performance-linked matrix in FY2025 (40% base, 30% cash bonus, 30% stock). Employee vitality is actively quantified via the KSA (Vitality and Growth Assessment) index, targeting a progression from 56.2% in FY2023 to 60.0% by FY2027. The female management ratio advanced from 4.9% in FY2024 to 5.5% in FY2025, anchoring a hard 10.0% mandate by FY2030.

Decarbonization is aggressively monetized and penalized. The firm applied a strict Internal Carbon Pricing (ICP) mechanism at $100.29 per ton of CO2 (¥15,000/t-CO2), effectively forcing subsidiary managers to absorb theoretical taxation on capital requests. Against a 2013 baseline of 5.11 million tons, Scope 1 and 2 GHG emissions contracted by 37% to 3.20 million tons in FY2024. The forward trajectory dictates an absolute ceiling of 3.60 million tons by 2030 (30% reduction) and 3.10 million tons by 2035 (40% reduction), while strict domestic mandates target 46% and 60% reductions over the identical timelines. FY2024 Carbon intensity tracked at 1,500 tons of CO2e per $668,589 (¥100 million) of operating profit.

HDIN Institutional Verdict

Asahi Kasei has successfully stabilized top-line volatility through inorganic Healthcare acquisitions and strict pricing controls, yet the core challenge remains the dilution of capital velocity. The Board's ability to drive a 32.4% EBITDA expansion while excising 4.9% of the global headcount confirms management's operational leverage capabilities. The strategic deployment of an "Offensive IP Strategy" to extend the Teribone exclusivity lifecycle—safeguarding $267.4 million (¥40 billion) in isolated annual sales—provides high-margin downside protection. Furthermore, the explicit target to execute 10 or more new strategic license agreements between FY2025 and FY2027 confirms a transition toward an asset-light royalty model.

However, the drag on ROIC (stalled at 5.9%) exposes the friction of absorbing massive intangible asset loads from entities like ZOLL Medical and Calliditas Therapeutics. Management's medium-term $8.02 billion capital deployment plan is highly credible due to its exact internal hurdle rates, specifically the $100.29/t-CO2 internal penalty. If the firm executes flawless post-merger integrations across its Western hubs and finalizes the 70% phase-out of low-yield legacy materials, the transition from a traditional Japanese chemical conglomerate into an IP-driven, specialized healthcare and deep-tech holding company will fulfill the FY2030 ROE targets.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."