Meiji Holdings Co., Ltd.: $693.3 Million CapEx Deployment and Pipeline Commercialization Across Asia as 8.0% ROE Target Signals Strategic Pivot from Commoditized Dairy

Date : 2026-06-26

Reading : 192

HDIN Executive Takeaways

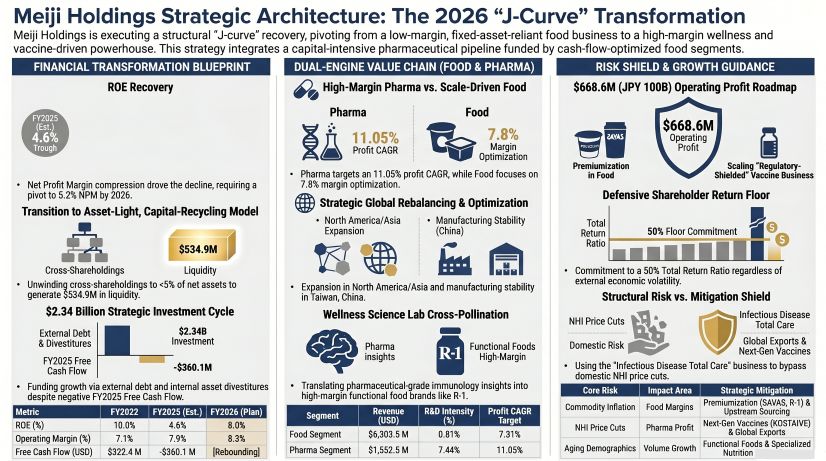

* Meiji Holdings Co., Ltd. offsets a mature, demographically constrained Japanese market by allocating $115.6 million (7.44% intensity) to pharmaceutical R&D, leveraging high-margin vaccine commercialization to shield against domestic National Health Insurance pricing cuts.

* A $693.3 million FY2025 fixed-asset CapEx program domesticates penicillin active pharmaceutical ingredient (API) production in Japan while scaling localized manufacturing in Southeast Asia via CP-Meiji Co., Ltd. and Meiji Food Vietnam Co., Ltd.

* Unwinding corporate cross-shareholdings to below 5% of consolidated net assets is structurally mandated to generate $534.9 million, directly funding a $2.34 billion, three-year investment cycle engineered to recover a 4.6% FY2025 ROE to an 8.0% FY2026 target.

Figure Meiji Holdings Strategic Architecture: The 2026 "J-Curve" Transformation

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Meiji Holdings Co., Ltd. [TYO: 2269] operates a highly bifurcated business model, utilizing cash flows from a low-R&D intensity Food Segment to subsidize a capital-heavy Pharmaceutical pipeline. Consolidated Return on Equity (ROE) deteriorated from 10.0% in FY2022 to 4.6% in FY2025, driven exclusively by Net Profit Margin (NPM) collapsing from 6.5% to 3.0%. During this period, Asset Turnover remained within a 0.90x–0.97x band, while Financial Leverage expanded from 1.60x to 1.63x, lowering the Equity Ratio from 62.7% to 60.1%. Management models a recovery to a 5.2% NPM and 1.70x Financial Leverage to hit an 8.0% ROE in FY2026.

The corporate R&D bifurcation is extreme: in FY2025, the Food Segment consumed $51.2 million (7.66 billion JPY) yielding a 0.81% R&D intensity, while the Pharmaceutical Segment required $115.6 million (17.28 billion JPY), representing a 7.44% R&D intensity. Total consolidated R&D spend contracted from $201.8 million (30.17 billion JPY; 2.73% intensity) in FY2024 to $195.2 million (29.19 billion JPY; 2.53% intensity) in FY2025.

Table Consolidated and Segment Financial Realities (FY2022–FY2026)

Note: Converted at 1 USD = 149.5686 JPY. FY2026 Consolidated Sales target is 1.21 trillion JPY; Consolidated OP target is 100 billion JPY.

To defend the Food Segment’s FY2025 7.3% operating margin (targeting 7.8% in FY2026) against soft commodity inflation, Meiji executes a strict premiumization strategy. Relying on the centralized Wellness Science Laboratories, the firm monetizes biopharma insights via mass-market functional foods. Key margin-defense assets include Meiji Bulgaria Yogurt, Meiji Probio Yogurt R-1, Chocolate Kouka, SAVAS, Meiji Milk Chocolate, Meiji Oishii Gyunyu, Meiji 0-1 year old INFANT FORMULA Premium, and Meiji 1-3 years old GROWING UP FORMULA. Innovations such as "Label-less R-1" yogurt bottles bypass plastic procurement costs, while the "Low Glycemic Index Concept" and research into OLL1073R-1 Exopolysaccharides (EPS) command specialized retail premiums.

Infrastructure Layout and Regional Moats

Geographic revenue concentration remains heavily skewed toward the domestic market. In FY2025, Japan generated 86.8% ($6,699.3 million) of the $7,716.0 million regional net sales base. The FY2026 plan maintains this dependency, projecting an 86.3% concentration ($6,776.4 million out of $7,847.1 million).

Despite this, Meiji operates a decentralized, physical supply chain moat targeting emerging markets, overseen by a formal Chief Digital Officer (CDO) managing the Group DX Strategy and Promotion Departments:

* North America: Localized food production via D.F. Stauffer Biscuit Co., Inc. and Laguna Cookie Co., Inc., controlled by Meiji America Inc.

* Southeast & South Asia: CP-Meiji Co., Ltd. (Thailand) and Meiji Food Vietnam Co., Ltd. operate as food manufacturing anchors. Medreich Limited (India) and PT. Meiji Indonesian Pharmaceutical Industries serve as pharmaceutical supply nodes.

* Greater China Region: Taiwan operations include Taiwan Meiji Food Co., Ltd. and Taiwan Meiji Pharmaceutical Co., Ltd. Mainland production is executed by Meiji Ice Cream (Guangzhou) Co., Ltd. and Meiji Confectionery & Food (Shanghai) Co., Ltd.

* Europe: Meiji Pharma Spain, S.A. anchors regional distribution.

To execute structural cost reforms, management ring-fenced $334.3 million (50 billion JPY) specifically for ESG-linked fixed-asset CapEx. This capital is deployed to domesticate penicillin API production, install CFC-free turbo chillers, deploy lightweight PET bottle manufacturing lines, and construct closed-loop rinse water recycling systems.

To bypass agricultural spot market volatility, Meiji utilizes direct supply chain interventions. The Meiji Dairy Advisory program integrated 72 farms in FY2025 (targeting 100 by FY2026), and the Meiji Cocoa Support initiative achieved a 68.9% sustainable sourcing ratio in FY2025 (mandating 100% by FY2026). The firm achieved 100% deforestation-free palm oil procurement in FY2025. Long-term raw material resilience includes a direct R&D partnership with California Cultured Inc. to develop cell-cultured cocoa and novel proteins.

Operational Environmental Metrics & Trajectories

* Scope 1 & 2 GHG Emissions: Reduced 30.1% in FY2025 against a 2019 baseline of 590,000 t-CO2. FY2026 target is a 32% reduction; FY2030 target is a 50% reduction (295,000 t-CO2).

* Renewable Energy: Reached 28.6% of total mix in FY2025. FY2026 target is 30%; 2050 target is 100%.

* Scope 3 Emissions (Categories 1 & 12): Reduced 10.2% in FY2025, tracking toward a 15% reduction target by FY2026, aided by transitioning from secondary IDEA estimates to primary supplier data.

* Resource Optimization: Water consumption decreased 23.6% in FY2025 versus 2017 (targeting 25% by FY2026). Plastic volume decreased 24.0% in FY2025 (targeting 25% by FY2026).

HDIN Institutional Verdict

Meiji Holdings is navigating a classic capital-intensive "J-curve" restructuring, intentionally absorbing a negative Free Cash Flow position of -$360.1 million in FY2025. Operating Cash Flow of $377.9 million (56.5 billion JPY) was eclipsed by an Investing Cash Flow deficit of -$737.9 million (110.3 billion JPY), of which exactly $693.3 million (103.7 billion JPY) was allocated to fixed facility CapEx. This deficit was financed by securing $421.2 million (63.0 billion JPY) in external interest-bearing debt and executing a $114.3 million (17.1 billion JPY) drawdown of internal cash reserves.

Across the full three-year Medium-Term Business Plan (MTBP), Meiji models $2.34 billion (350 billion JPY) in Operating CF, directly funding $2.34 billion in recurring investments ($1.6 billion allocated to Food, including $267.4 million / 40 billion JPY ring-fenced for overseas growth; $0.73 billion allocated to Pharma).

To defend equity valuation during this transition, management instituted a "Meiji ROESG" KPI (calculating 3-year average ROE multiplied by an ESG coefficient from 0.8 to 1.2), achieving 6.1 points in FY2025 with a target of 9.8 points in FY2026. Concurrently, the firm legally mandates a Total Return Ratio floor of 50%, guaranteeing a minimum distribution of $802.3 million (120 billion JPY). The FY2025 absolute dividend was maintained at JPY 105 per share ($0.70), artificially inflating the payout ratio to 81.1%, with plans to maintain the JPY 105 dividend in FY2026.

Institutional value extraction relies on successful commercialization of the Pharmaceutical pipeline, categorized as the "Infectious Disease Total Care Business," structurally insulated from Japanese regulatory drug price revisions. Active clinical assets include:

* KOSTAIVE: COVID-19 mRNA/replicon vaccine in commercial scale-up.

* OP0595 (Nacubactam): Phase-progressing antibacterial β-lactamase inhibitor.

* KD-414 / KD-382: Domestic COVID-19/Infectious disease vaccines advancing in Phase trials under SCARDA.

* ME3241: Clinical-stage PD-1 immunology/oncology asset.

* Pre-clinical / Pipeline Assets: KD2-396, KD-380, KD-416, ME4305, Dengue Vaccine, Mpox Vaccine, alongside specialized treatments targeting Cervical Intraepithelial Neoplasia and Rho-associated coiled-coil containing protein kinases.

Execution of this dual-track global strategy is constrained by human capital availability. Meiji's Board maintains a 44.4% independence ratio (4 of 9 members), while the Audit Board sits at 50% independence (2 of 4 members). Operational KPIs aggressively track workforce agility: the "Global Business Talent Fill Rate" registered 28.8% in FY2025 (targeting 35.0% in FY2026), and the mid-career management ratio reached 11.8%. Management achieved a 6.5% female executive ratio and an 8.0% female management ratio in FY2025, operating a rigorous productivity baseline recording 0.4% absenteeism, 22.0% presenteeism, a 96.0% male paternity leave rate, 0 product recalls, and 0 major occupational accidents. The 2050 vision mandates achieving 50% female representation, >30% mid-career hires, and >30% overseas talent across executive ranks.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Meiji Holdings Co., Ltd. offsets a mature, demographically constrained Japanese market by allocating $115.6 million (7.44% intensity) to pharmaceutical R&D, leveraging high-margin vaccine commercialization to shield against domestic National Health Insurance pricing cuts.

* A $693.3 million FY2025 fixed-asset CapEx program domesticates penicillin active pharmaceutical ingredient (API) production in Japan while scaling localized manufacturing in Southeast Asia via CP-Meiji Co., Ltd. and Meiji Food Vietnam Co., Ltd.

* Unwinding corporate cross-shareholdings to below 5% of consolidated net assets is structurally mandated to generate $534.9 million, directly funding a $2.34 billion, three-year investment cycle engineered to recover a 4.6% FY2025 ROE to an 8.0% FY2026 target.

Figure Meiji Holdings Strategic Architecture: The 2026 "J-Curve" Transformation

Segmental Realities and Margin CompressionMeiji Holdings Co., Ltd. [TYO: 2269] operates a highly bifurcated business model, utilizing cash flows from a low-R&D intensity Food Segment to subsidize a capital-heavy Pharmaceutical pipeline. Consolidated Return on Equity (ROE) deteriorated from 10.0% in FY2022 to 4.6% in FY2025, driven exclusively by Net Profit Margin (NPM) collapsing from 6.5% to 3.0%. During this period, Asset Turnover remained within a 0.90x–0.97x band, while Financial Leverage expanded from 1.60x to 1.63x, lowering the Equity Ratio from 62.7% to 60.1%. Management models a recovery to a 5.2% NPM and 1.70x Financial Leverage to hit an 8.0% ROE in FY2026.

The corporate R&D bifurcation is extreme: in FY2025, the Food Segment consumed $51.2 million (7.66 billion JPY) yielding a 0.81% R&D intensity, while the Pharmaceutical Segment required $115.6 million (17.28 billion JPY), representing a 7.44% R&D intensity. Total consolidated R&D spend contracted from $201.8 million (30.17 billion JPY; 2.73% intensity) in FY2024 to $195.2 million (29.19 billion JPY; 2.53% intensity) in FY2025.

Table Consolidated and Segment Financial Realities (FY2022–FY2026)

| Financial Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 | 4-Year CAGR |

| Consolidated Net Sales | $7,101.1 M | $7,390.6 M | $7,715.5 M | $7,846.5 M | $8,103.3 M | +3.36% |

| Consolidated OP | $504.1 M | $563.6 M | $566.3 M | $623.8 M | $668.6 M | +7.32% |

| Consolidated OP Margin | 7.1% | 7.6% | 7.3% | 7.9% | 8.3% | -- |

| Consolidated Net Profit | $464.0 M | $338.3 M | $339.6 M | $234.0 M | $417.9 M | -2.58% |

| Food Segment Net Sales | $5,787.3 M | $6,018.0 M | $6,187.8 M | $6,303.5 M | $6,377.7 M | +2.46% |

| Food Segment OP | $373.1 M | $429.9 M | $431.9 M | $459.3 M | $494.8 M | +7.31% |

| Pharma Segment Net Sales | $1,318.5 M | $1,378.0 M | $1,535.1 M | $1,552.5 M | $1,733.7 M | +7.08% |

| Pharma Segment OP | $145.1 M | $151.8 M | $165.1 M | $203.3 M | $220.6 M | +11.05% |

To defend the Food Segment’s FY2025 7.3% operating margin (targeting 7.8% in FY2026) against soft commodity inflation, Meiji executes a strict premiumization strategy. Relying on the centralized Wellness Science Laboratories, the firm monetizes biopharma insights via mass-market functional foods. Key margin-defense assets include Meiji Bulgaria Yogurt, Meiji Probio Yogurt R-1, Chocolate Kouka, SAVAS, Meiji Milk Chocolate, Meiji Oishii Gyunyu, Meiji 0-1 year old INFANT FORMULA Premium, and Meiji 1-3 years old GROWING UP FORMULA. Innovations such as "Label-less R-1" yogurt bottles bypass plastic procurement costs, while the "Low Glycemic Index Concept" and research into OLL1073R-1 Exopolysaccharides (EPS) command specialized retail premiums.

Infrastructure Layout and Regional Moats

Geographic revenue concentration remains heavily skewed toward the domestic market. In FY2025, Japan generated 86.8% ($6,699.3 million) of the $7,716.0 million regional net sales base. The FY2026 plan maintains this dependency, projecting an 86.3% concentration ($6,776.4 million out of $7,847.1 million).

Despite this, Meiji operates a decentralized, physical supply chain moat targeting emerging markets, overseen by a formal Chief Digital Officer (CDO) managing the Group DX Strategy and Promotion Departments:

* North America: Localized food production via D.F. Stauffer Biscuit Co., Inc. and Laguna Cookie Co., Inc., controlled by Meiji America Inc.

* Southeast & South Asia: CP-Meiji Co., Ltd. (Thailand) and Meiji Food Vietnam Co., Ltd. operate as food manufacturing anchors. Medreich Limited (India) and PT. Meiji Indonesian Pharmaceutical Industries serve as pharmaceutical supply nodes.

* Greater China Region: Taiwan operations include Taiwan Meiji Food Co., Ltd. and Taiwan Meiji Pharmaceutical Co., Ltd. Mainland production is executed by Meiji Ice Cream (Guangzhou) Co., Ltd. and Meiji Confectionery & Food (Shanghai) Co., Ltd.

* Europe: Meiji Pharma Spain, S.A. anchors regional distribution.

To execute structural cost reforms, management ring-fenced $334.3 million (50 billion JPY) specifically for ESG-linked fixed-asset CapEx. This capital is deployed to domesticate penicillin API production, install CFC-free turbo chillers, deploy lightweight PET bottle manufacturing lines, and construct closed-loop rinse water recycling systems.

To bypass agricultural spot market volatility, Meiji utilizes direct supply chain interventions. The Meiji Dairy Advisory program integrated 72 farms in FY2025 (targeting 100 by FY2026), and the Meiji Cocoa Support initiative achieved a 68.9% sustainable sourcing ratio in FY2025 (mandating 100% by FY2026). The firm achieved 100% deforestation-free palm oil procurement in FY2025. Long-term raw material resilience includes a direct R&D partnership with California Cultured Inc. to develop cell-cultured cocoa and novel proteins.

Operational Environmental Metrics & Trajectories

* Scope 1 & 2 GHG Emissions: Reduced 30.1% in FY2025 against a 2019 baseline of 590,000 t-CO2. FY2026 target is a 32% reduction; FY2030 target is a 50% reduction (295,000 t-CO2).

* Renewable Energy: Reached 28.6% of total mix in FY2025. FY2026 target is 30%; 2050 target is 100%.

* Scope 3 Emissions (Categories 1 & 12): Reduced 10.2% in FY2025, tracking toward a 15% reduction target by FY2026, aided by transitioning from secondary IDEA estimates to primary supplier data.

* Resource Optimization: Water consumption decreased 23.6% in FY2025 versus 2017 (targeting 25% by FY2026). Plastic volume decreased 24.0% in FY2025 (targeting 25% by FY2026).

HDIN Institutional Verdict

Meiji Holdings is navigating a classic capital-intensive "J-curve" restructuring, intentionally absorbing a negative Free Cash Flow position of -$360.1 million in FY2025. Operating Cash Flow of $377.9 million (56.5 billion JPY) was eclipsed by an Investing Cash Flow deficit of -$737.9 million (110.3 billion JPY), of which exactly $693.3 million (103.7 billion JPY) was allocated to fixed facility CapEx. This deficit was financed by securing $421.2 million (63.0 billion JPY) in external interest-bearing debt and executing a $114.3 million (17.1 billion JPY) drawdown of internal cash reserves.

Across the full three-year Medium-Term Business Plan (MTBP), Meiji models $2.34 billion (350 billion JPY) in Operating CF, directly funding $2.34 billion in recurring investments ($1.6 billion allocated to Food, including $267.4 million / 40 billion JPY ring-fenced for overseas growth; $0.73 billion allocated to Pharma).

To defend equity valuation during this transition, management instituted a "Meiji ROESG" KPI (calculating 3-year average ROE multiplied by an ESG coefficient from 0.8 to 1.2), achieving 6.1 points in FY2025 with a target of 9.8 points in FY2026. Concurrently, the firm legally mandates a Total Return Ratio floor of 50%, guaranteeing a minimum distribution of $802.3 million (120 billion JPY). The FY2025 absolute dividend was maintained at JPY 105 per share ($0.70), artificially inflating the payout ratio to 81.1%, with plans to maintain the JPY 105 dividend in FY2026.

Institutional value extraction relies on successful commercialization of the Pharmaceutical pipeline, categorized as the "Infectious Disease Total Care Business," structurally insulated from Japanese regulatory drug price revisions. Active clinical assets include:

* KOSTAIVE: COVID-19 mRNA/replicon vaccine in commercial scale-up.

* OP0595 (Nacubactam): Phase-progressing antibacterial β-lactamase inhibitor.

* KD-414 / KD-382: Domestic COVID-19/Infectious disease vaccines advancing in Phase trials under SCARDA.

* ME3241: Clinical-stage PD-1 immunology/oncology asset.

* Pre-clinical / Pipeline Assets: KD2-396, KD-380, KD-416, ME4305, Dengue Vaccine, Mpox Vaccine, alongside specialized treatments targeting Cervical Intraepithelial Neoplasia and Rho-associated coiled-coil containing protein kinases.

Execution of this dual-track global strategy is constrained by human capital availability. Meiji's Board maintains a 44.4% independence ratio (4 of 9 members), while the Audit Board sits at 50% independence (2 of 4 members). Operational KPIs aggressively track workforce agility: the "Global Business Talent Fill Rate" registered 28.8% in FY2025 (targeting 35.0% in FY2026), and the mid-career management ratio reached 11.8%. Management achieved a 6.5% female executive ratio and an 8.0% female management ratio in FY2025, operating a rigorous productivity baseline recording 0.4% absenteeism, 22.0% presenteeism, a 96.0% male paternity leave rate, 0 product recalls, and 0 major occupational accidents. The 2050 vision mandates achieving 50% female representation, >30% mid-career hires, and >30% overseas talent across executive ranks.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."