Mitsubishi Heavy Industries: Sovereign Defense Pivot Near US and EMEA Nodes as $88.51B Backlog Signals 12.22% ROE Expansion

Date : 2026-06-26

Reading : 221

HDIN Executive Takeaways

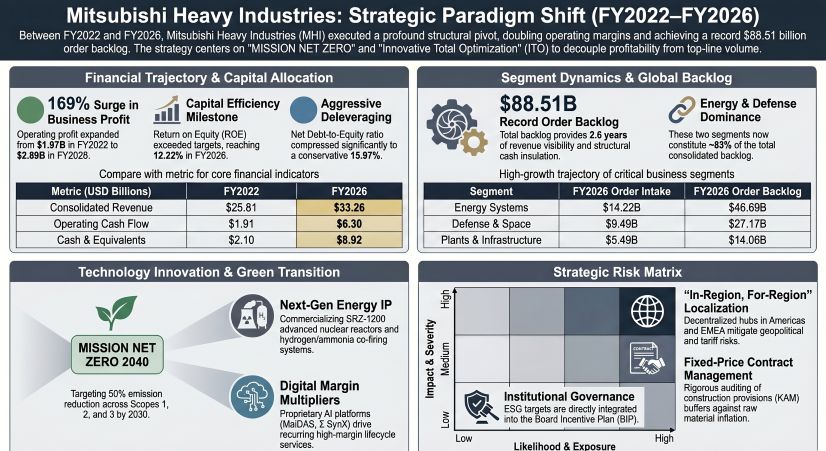

* FY2026 order backlog of $88.51 billion guarantees 2.6x forward revenue visibility, insulating the firm’s 12.22% consolidated Return on Equity (ROE) from macroeconomic volatility.

* Decentralized "In-Region, For-Region" manufacturing nodes across Florida, London, and Taiwan, China structurally neutralize cross-border tariffs and optimize global inventory throughput.

* Off-balance sheet buffers, including a $430 million pension surplus and $2.18 billion in deferred tax assets, fortify true net worth and accelerate aggressive capital allocation into decarbonization technologies.

Figure Mitsubishi Heavy Industries: Strategic Paradigm Shift (FY2022-FY2026)

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Mitsubishi Heavy Industries, Ltd. [TYO: 7011] executed a highly disciplined capital allocation strategy across the FY2022 to FY2026 reporting period, decoupling core profitability from linear top-line growth. Driven by the "Innovative Total Optimization" (ITO) framework and the transition from a traditional heavy machinery Original Equipment Manufacturer (OEM) to a high-margin lifecycle service integrator, operating profit margins expanded from 4.15% in FY2022 to 8.69% in FY2026. Management surpassed its 12.0% ROE target by delivering 12.22% in FY2026, up from 7.72% in FY2022 and 10.69% in FY2025.

The firm’s cash conversion metrics demonstrate extreme working capital efficiency. Operating cash flow escalated from $1.91 billion (¥285.5 billion) in FY2022 to $6.30 billion (¥942.6 billion) in FY2026. This liquidity surge quadrupled cash and cash equivalents from $2.10 billion (¥314.2 billion) in FY2022 to $8.92 billion (¥1.33 trillion) in FY2026, driving the Net Debt-to-Equity (D/E) ratio down from 26.37% in FY2025 to 15.97% in FY2026.

Table 1: Five-Year Consolidated Financial Trajectory (FY2022 vs. FY2026)

The consolidated $88.51 billion (¥13.24 trillion) order backlog in FY2026 is concentrated in high-barrier, long-cycle operations, effectively neutralizing short-term macroeconomic shocks.

Table 2: FY2025 to FY2026 Segmental Execution Metrics

FY2026 R&D Capital Allocation ($1.192 Billion / ¥178.36 Billion Total)

* Aerospace, Defense & Space: $474.41 million (¥70.95 billion) / ~40% of total expenditure.

* Energy Systems: $361.60 million (¥54.08 billion).

* Corporate/Common IP (Digital Innovation): $143.26 million (¥21.42 billion).

* Logistics, Thermal & Drive Systems: $111.78 million (¥16.71 billion).

* Plants & Infrastructure Systems: $90.76 million (¥13.57 billion).

Infrastructure Layout and Regional Moats

Management mitigates supply chain constraints and geopolitical volatility via a strictly quantified Business Continuity Management (BCM) matrix and a decentralized "In-Region, For-Region" manufacturing footprint. By shifting from a centralized Japanese exporter to a localized operator, the firm sidesteps protectionist tariffs and local-content regulations.

In the Americas, operations are anchored by Mitsubishi Power Americas, Inc. (Florida), Mitsubishi Power Aero LLC (Connecticut), Concentric, LLC (Texas), and MHI RJ Aviation Inc. (West Virginia). This network serves as the primary integration hub for Gas Turbine Combined Cycle (GTCC) retrofits, Carbon Capture, Utilization, and Storage (CCUS), and Sustainable Aviation Fuel (SAF) infrastructure.

EMEA operations center on metals engineering and decarbonization via Primetals Technologies, Ltd. and MHI EMEA, Ltd. in London, UK, alongside thermal systems in Almere, Netherlands. The European moat is fortified by strategic joint ventures, specifically the nuclear alliance with Framatome S.A.S. (Courbevoie, France) and Orano S.A., as well as offshore wind integration with Vestas Wind Systems A/S (Denmark).

The APAC supply chain architecture leverages high-volume manufacturing hubs including Mahajak Air Conditioners (Bangkok, Thailand), Mitsubishi Power India (Delhi, India), and a regional headquarters in Singapore. The firm secures seamless component sourcing via localized procurement nodes, utilizing compliant electronic and semiconductor lines in Taiwan, China. Enterprise inventory optimization across these global nodes is continuously executed by proprietary AI and IoT platforms, namely MaiDAS (predictive maintenance) and Σ SynX (intelligent automation), under the Digital Transformation (DX) mandate.

HDIN Institutional Verdict

Mitsubishi Heavy Industries [TYO: 7011] presents a highly asymmetric risk-reward profile underpinned by forensic balance sheet strength and rigorous environmental governance. The firm’s "MISSION NET ZERO" mandate—targeting 2040 carbon neutrality, a 50% Scope 1 and 2 emissions reduction by 2030 (from a 2014 baseline), and a 50% Scope 3 emissions reduction by 2030 (from a 2019 baseline)—is structurally integrated into executive compensation via the Board Incentive Plan (BIP) Trust and an Employee Stock Ownership Plan (ESOP).

Governance over cross-border intellectual property, specifically regarding the SRZ-1200 advanced light water reactor, Pressurized Water Reactors (PWR), Boiling Water Reactors (BWR), and Solid Oxide Electrolysis Cells (SOEC), is strictly ring-fenced. Specialized oversight bodies—including the Compliance Committee, Export-Related Laws Compliance Committee, Sustainability Committee, and Cyber Security Committee—bypass operational heads to report directly to the CEO, minimizing sovereign regulatory friction. The Chief Strategy Officer (CSO) directly oversees Task Force on Climate-related Financial Disclosures (TCFD) alignment.

A forensic audit of FY2025 to FY2026 balance sheet disclosures reveals hidden quasi-equity buffers. Retirement benefit assets normalized from $2.467 billion (¥369.0 billion) to $2.211 billion (¥330.6 billion), while corresponding liabilities dropped from $1.842 billion (¥275.5 billion) to $1.780 billion (¥266.2 billion), generating a net pension surplus of approximately $430 million. Concurrently, Deferred Tax Assets (DTAs) grew by 10.7% from $1.973 billion (¥295.1 billion) to $2.186 billion (¥326.9 billion), acting as a direct cash flow shield.

To absorb supply chain inflation and project-execution friction (audited as a Key Audit Matter), the firm maintains stringent accounting buffers. General non-current provisions, primarily allocating for construction contract losses and contingent liabilities (Note 38), scaled from $1.531 billion (¥229.0 billion) to $1.637 billion (¥244.8 billion). The combination of these massive off-balance sheet reserves, an overfunded pension, and an expanding DTA base guarantees that the firm's $8.92 billion cash hoard is fully deployable toward scaling sovereign defense and zero-carbon baseload technologies.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* FY2026 order backlog of $88.51 billion guarantees 2.6x forward revenue visibility, insulating the firm’s 12.22% consolidated Return on Equity (ROE) from macroeconomic volatility.

* Decentralized "In-Region, For-Region" manufacturing nodes across Florida, London, and Taiwan, China structurally neutralize cross-border tariffs and optimize global inventory throughput.

* Off-balance sheet buffers, including a $430 million pension surplus and $2.18 billion in deferred tax assets, fortify true net worth and accelerate aggressive capital allocation into decarbonization technologies.

Figure Mitsubishi Heavy Industries: Strategic Paradigm Shift (FY2022-FY2026)

Segmental Realities and Margin CompressionMitsubishi Heavy Industries, Ltd. [TYO: 7011] executed a highly disciplined capital allocation strategy across the FY2022 to FY2026 reporting period, decoupling core profitability from linear top-line growth. Driven by the "Innovative Total Optimization" (ITO) framework and the transition from a traditional heavy machinery Original Equipment Manufacturer (OEM) to a high-margin lifecycle service integrator, operating profit margins expanded from 4.15% in FY2022 to 8.69% in FY2026. Management surpassed its 12.0% ROE target by delivering 12.22% in FY2026, up from 7.72% in FY2022 and 10.69% in FY2025.

The firm’s cash conversion metrics demonstrate extreme working capital efficiency. Operating cash flow escalated from $1.91 billion (¥285.5 billion) in FY2022 to $6.30 billion (¥942.6 billion) in FY2026. This liquidity surge quadrupled cash and cash equivalents from $2.10 billion (¥314.2 billion) in FY2022 to $8.92 billion (¥1.33 trillion) in FY2026, driving the Net Debt-to-Equity (D/E) ratio down from 26.37% in FY2025 to 15.97% in FY2026.

Table 1: Five-Year Consolidated Financial Trajectory (FY2022 vs. FY2026)

| Financial Metric | FY2022 | FY2026 | Growth / Context |

| Consolidated Revenue | $25.81B (¥3.86T) | $33.26B (¥4.97T) | 6.5% CAGR |

| Business Profit | ¥160.2B ($1.07B) | ¥432.2B ($2.89B) | 169% Expansion (Target: ¥450B/$3.01B) |

| Net Income (Attributable to Owners) | $759M (¥113.5B) | $2.22B (¥332.1B) | Significant Growth |

| Total Assets | $34.21B (¥5.11T) | $55.29B (¥8.27T) | Asset Expansion |

| Equity Ratio | 30.82% | 37.35% | Improved Solvency |

The consolidated $88.51 billion (¥13.24 trillion) order backlog in FY2026 is concentrated in high-barrier, long-cycle operations, effectively neutralizing short-term macroeconomic shocks.

Table 2: FY2025 to FY2026 Segmental Execution Metrics

| Segment | Metric | FY2025 | FY2026 |

| Energy Systems | Revenue ($B) | 12.06 | 13.79 |

| Operating Income ($B) | 1.37 | 1.79 | |

| Order Intake ($B) | - | 14.22 | |

| Order Backlog ($B) | 26.32 | 46.69 | |

| Defense & Space | Revenue ($B) | 6.88 | 9.32 |

| Operating Income ($B) | 0.67 | 1.01 | |

| Order Intake ($B) | - | 9.49 | |

| Order Backlog ($B) | 12.90 | 27.17 | |

| Plants & Infrastructure | Revenue ($B) | 5.39 | 5.89 |

| Operating Income ($B) | 0.40 | 0.56 | |

| Order Intake ($B) | - | 5.49 | |

| Order Backlog ($B) | 7.74 | 14.06 | |

| Logistics, Thermal & Drive | Revenue ($B) | 4.26 | 4.22 |

| Operating Income ($B) | 0.14 | 0.22 | |

| Order Intake ($B) | - | 4.24 | |

| Order Backlog ($B) | 4.27 | 0.46 |

FY2026 R&D Capital Allocation ($1.192 Billion / ¥178.36 Billion Total)

* Aerospace, Defense & Space: $474.41 million (¥70.95 billion) / ~40% of total expenditure.

* Energy Systems: $361.60 million (¥54.08 billion).

* Corporate/Common IP (Digital Innovation): $143.26 million (¥21.42 billion).

* Logistics, Thermal & Drive Systems: $111.78 million (¥16.71 billion).

* Plants & Infrastructure Systems: $90.76 million (¥13.57 billion).

Infrastructure Layout and Regional Moats

Management mitigates supply chain constraints and geopolitical volatility via a strictly quantified Business Continuity Management (BCM) matrix and a decentralized "In-Region, For-Region" manufacturing footprint. By shifting from a centralized Japanese exporter to a localized operator, the firm sidesteps protectionist tariffs and local-content regulations.

In the Americas, operations are anchored by Mitsubishi Power Americas, Inc. (Florida), Mitsubishi Power Aero LLC (Connecticut), Concentric, LLC (Texas), and MHI RJ Aviation Inc. (West Virginia). This network serves as the primary integration hub for Gas Turbine Combined Cycle (GTCC) retrofits, Carbon Capture, Utilization, and Storage (CCUS), and Sustainable Aviation Fuel (SAF) infrastructure.

EMEA operations center on metals engineering and decarbonization via Primetals Technologies, Ltd. and MHI EMEA, Ltd. in London, UK, alongside thermal systems in Almere, Netherlands. The European moat is fortified by strategic joint ventures, specifically the nuclear alliance with Framatome S.A.S. (Courbevoie, France) and Orano S.A., as well as offshore wind integration with Vestas Wind Systems A/S (Denmark).

The APAC supply chain architecture leverages high-volume manufacturing hubs including Mahajak Air Conditioners (Bangkok, Thailand), Mitsubishi Power India (Delhi, India), and a regional headquarters in Singapore. The firm secures seamless component sourcing via localized procurement nodes, utilizing compliant electronic and semiconductor lines in Taiwan, China. Enterprise inventory optimization across these global nodes is continuously executed by proprietary AI and IoT platforms, namely MaiDAS (predictive maintenance) and Σ SynX (intelligent automation), under the Digital Transformation (DX) mandate.

HDIN Institutional Verdict

Mitsubishi Heavy Industries [TYO: 7011] presents a highly asymmetric risk-reward profile underpinned by forensic balance sheet strength and rigorous environmental governance. The firm’s "MISSION NET ZERO" mandate—targeting 2040 carbon neutrality, a 50% Scope 1 and 2 emissions reduction by 2030 (from a 2014 baseline), and a 50% Scope 3 emissions reduction by 2030 (from a 2019 baseline)—is structurally integrated into executive compensation via the Board Incentive Plan (BIP) Trust and an Employee Stock Ownership Plan (ESOP).

Governance over cross-border intellectual property, specifically regarding the SRZ-1200 advanced light water reactor, Pressurized Water Reactors (PWR), Boiling Water Reactors (BWR), and Solid Oxide Electrolysis Cells (SOEC), is strictly ring-fenced. Specialized oversight bodies—including the Compliance Committee, Export-Related Laws Compliance Committee, Sustainability Committee, and Cyber Security Committee—bypass operational heads to report directly to the CEO, minimizing sovereign regulatory friction. The Chief Strategy Officer (CSO) directly oversees Task Force on Climate-related Financial Disclosures (TCFD) alignment.

A forensic audit of FY2025 to FY2026 balance sheet disclosures reveals hidden quasi-equity buffers. Retirement benefit assets normalized from $2.467 billion (¥369.0 billion) to $2.211 billion (¥330.6 billion), while corresponding liabilities dropped from $1.842 billion (¥275.5 billion) to $1.780 billion (¥266.2 billion), generating a net pension surplus of approximately $430 million. Concurrently, Deferred Tax Assets (DTAs) grew by 10.7% from $1.973 billion (¥295.1 billion) to $2.186 billion (¥326.9 billion), acting as a direct cash flow shield.

To absorb supply chain inflation and project-execution friction (audited as a Key Audit Matter), the firm maintains stringent accounting buffers. General non-current provisions, primarily allocating for construction contract losses and contingent liabilities (Note 38), scaled from $1.531 billion (¥229.0 billion) to $1.637 billion (¥244.8 billion). The combination of these massive off-balance sheet reserves, an overfunded pension, and an expanding DTA base guarantees that the firm's $8.92 billion cash hoard is fully deployable toward scaling sovereign defense and zero-carbon baseload technologies.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."