Academic Publishing 2026 Outlook: Why John Wiley & Sons, Inc. and Springer Nature AG & Co. KGaA Diverge on Open Access Scale Amid Surging AI Compliance Costs

Date : 2026-06-27

Reading : 622

HDIN Executive Takeaways

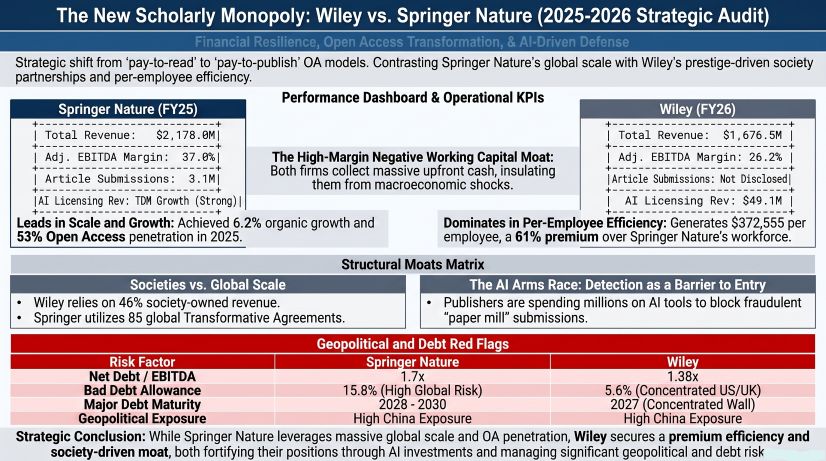

* John Wiley & Sons, Inc. [NYSE: WLY] reported flat FY2026 revenue of $1,676.5 million (-1.0% constant currency), dragged by a 7% contraction in Learning, while Springer Nature AG & Co. KGaA [FSE: SPG] achieved $2,178.0 million (€1,926.4 million), driven by 20% growth in Open Access (OA) article volumes.

* Geopolitical risk bifurcates the sector: Wiley relies on China-based authors for 31% of its published articles amid US-China trade tensions, whereas Springer Nature mitigates regional risk through a globally balanced footprint yielding $636.9 million across APAC markets, including Taiwan, China, and a 20-university consortium in Malaysia.

* Platform capitalization is redefining the industry cost structure; both firms are leveraging multi-year Transformative Agreements (TAs) to bypass stagnant library budgets, utilizing artificial intelligence screening to automate workflow, defend brand impact factors, and secure highly predictable, negative working capital profiles.

Figure The New Scholarly Monopoly: Wiley vs Springer Nature (2025-2026 Strategic Audit)

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

A forensic analysis of FY2025/2026 disclosures reveals diverging trajectories in top-line growth, operating leverage, and capital structures. (Note: Springer Nature financial conversions are calculated at a 2025 average rate of 1 EUR = 1.1306 USD).

Springer Nature AG & Co. KGaA: Top-Line Expansion

Total revenue reached $2,178.0 million (€1,926.4 million), driven by comprehensive segment growth:

* Research: Generated $1,715.3 million (€1,517.2 million), achieving 7.4% underlying growth. Transactional revenue hit $692.7 million (€612.7 million), primarily fueled by OA Article Processing Charges (APCs).

* Health: Contributed $216.0 million (€191.0 million), posting a 2.7% underlying growth rate, supported by scientific writing services despite advertising restraint in the German pharmaceutical sector.

* Education: Generated $248.5 million (€219.8 million) with a 0.8% underlying growth rate. Government stimulus in Argentina (adjusted for IAS 29 hyperinflation) and India offset foreign exchange volatility from the Mexican peso, Indian rupee, and K-12 curriculum funding delays in South Africa.

John Wiley & Sons, Inc.: Bifurcated Portfolio

Total revenue registered at $1,676.5 million (-1.0% constant currency), reflecting structural divergence:

* Research (67% of total): Generated $1,129.9 million (+4% constant currency). The Research Publishing division contributed $965.8 million (+3% constant currency), while Research Solutions reached $164.2 million (+6% constant currency), capturing $49.1 million in AI licensing revenue (up from $40.0 million in the prior year).

* Learning (33% of total): Generated $546.6 million (-7% constant currency). The Academic division fell 5% to $318.8 million, and the Professional division plummeted 10% to $227.8 million due to retail channel weakness across franchises like For Dummies and Everything DiSC.

Cash Flow, Profitability, and Capital Structure Matrix

* Earnings Quality: Springer Nature reported Adjusted EBITDA of $806.3 million (€713.2M) and Adjusted Operating Profit of $614.6 million. Operating Cash Flow (OCF) reached $620.9 million (€549.2M), converting to Free Cash Flow (FCF) of $336.7 million (€297.8M) for a 41.7% conversion rate. Wiley recorded Adjusted EBITDA of $439.6 million, Adjusted Operating Income of $296.2 million, OCF of $260.5 million, and FCF of $195.3 million, yielding a 44.4% conversion rate.

* Leverage & Maturities: Springer Nature executed a $565.3 million (€500M) promissory note refinancing, operating at a 1.7x Net Debt to EBITDA ratio with 31.4% of its debt hedged. Maturities are staged in Nov/Dec 2028 (Term Loans B & C, plus €210M in notes) and Nov 2030 (€290M in notes). Wiley operates with leaner leverage at 1.38x Net Debt to Adj. EBITDA, carrying $608.1 million in net debt ($683.7 million total variable-rate debt offset by $75.6 million cash). Wiley faces a concentrated $671.2 million maturity wall in November 2027 (Term Loan A and Revolver).

Infrastructure Layout and Regional Moats

Geographic revenue distribution and digital infrastructure explicitly define the competitive moats for both publishers, functioning simultaneously as distribution channels and defensive mechanisms against AI-generated paper mills.

Geographic Concentration vs. Diversification

Wiley’s footprint is intensely concentrated, deriving 80% of total revenue from the United States ($854.5 million; 51.0%) and the United Kingdom ($490.4 million; 29.3%). Germany contributed $192.3 million (11.5%), with the remainder of the globe generating $139.3 million (8.3%). Conversely, Springer Nature operates a balanced matrix: the Americas generated $686.8 million (€607.5M), heavily weighted by $505.4 million (€447.0M) from the US. The APAC region delivered $636.9 million (€563.3M), and EMEA contributed $600.1 million (€530.8M), with Germany accounting for $254.2 million (€224.8M).

Technological Capital Expenditures and B2B Platforms

Both firms are actively migrating capital toward fixed digital infrastructure to facilitate zero-marginal-cost volume scaling.

* Springer Nature Ecosystem: Total cumulative technology spend reached $212.6 million (€188M) since 2021. In FY2025, cash paid for intangibles was $24.0 million (€21.2M) alongside $8.8 million (€7.8M) for property, plant, and equipment. The firm capitalized $44.7 million (€39.5M) in internal software and content creation costs. The proprietary Snapp (Springer Nature Article Processing Platform) has processed 3.7 million submissions to date. Content distribution relies on Springer Nature Link (18 million active monthly users), while corporate operations utilize Text and Data Mining (TDM) tools, AskAdis for pharmaceuticals, and Medbee (serving 43,000 doctors among the company's 324,000 global healthcare professional users). The Nature Research Assistant is currently in beta with over 20,000 users.

* Wiley Ecosystem: Wiley deployed $51.2 million in technology and PPE, plus $14.0 million in product development, totaling $65.2 million. Gross capitalized software reached $687.4 million, registering a $61.7 million amortization expense based on a rapid 3-year useful life cycle. Infrastructure centers on Research Exchange (ReX) for AI-enabled manuscript screening and the Atypon platform, which hosts B2B content for approximately 2,000 competitor publishers and societies. Wiley also monetizes R&D through the Cochrane Library for Evidence-Based Medicine (EBM) and Spectral databases for microscopy and bioanalysis.

Throughput Dynamics, Quality Filters, and Consortia Lock-ins

In 2025, Springer Nature received 3.1 million submissions across its 3,000+ journals (770 Gold OA, 2,200 Springer hybrid, 66 Nature hybrid). It published 539,000 primary articles, enforcing an 82.6% implied rejection rate (17.4% acceptance rate). Of the published output, 288,419 were OA articles (+20% year-over-year), pushing OA penetration above 53%. The firm secured 85 Transformative Agreements (19 new, 17 renewed) covering 4,000 institutions (including DEAL, LYRASIS, and the Big Ten Academic Alliance), resulting in over 63,000 OA articles funded via TAs (+12%). To support global parity, Springer Nature waived $24.87 million (€22M) in APCs.

Wiley commands 8% of global titles and articles, generating 10% of global citations across its 1,900+ journals. The publisher grew OA output by 25%. A critical operational dependency exists through prestigious society partnerships, which secure 46% of Wiley's Journal Subscriptions revenue.

HDIN Institutional Verdict

The institutional evaluation of these academic publishing entities hinges on their divergent approaches to working capital optimization and algorithmic defense mechanisms against industry fraud.

Working Capital Optimization and Deferred Revenue Moats

The legacy subscription model allows both firms to function with structurally negative working capital by collecting upfront cash. Wiley operates with superior balance sheet efficiency, recording negative net working capital of -$359.3 million. The firm holds $468.6 million in contract liabilities ($451.4 million short-term), representing 28.0% of total revenue, which drives its lean Days Sales Outstanding (DSO) of 53 days. Wiley secures 48% of its total revenue via contractually obligated recurring streams, embedding explicit fixed price escalators into its 2-to-5-year Atypon hosting contracts to guarantee compounding yield.

Springer Nature carries $353.1 million (€312.3M) in contract liabilities, representing 16.2% of revenue. This lower deferred revenue ratio reflects its aggressive pivot toward transactional OA models. While its DSO sits higher at 61 days, Springer Nature utilizes volume metrics to defend pricing during institutional negotiations, registering 5.6 billion downloads (+50% year-over-year) to orchestrate a 54% drop in the average cost per download since 2019. This protects its estimated ~$2,400 per-unit APC proxy and secures high author (87%) and reviewer (88%) satisfaction rates.

Intangible Assets and Credit Risk Exposures

The capitalization of intellectual property dictates balance sheet risk. Springer Nature carries $1,065.3 million (€942.2M) in Publishing Rights and $1,079.6 million (€954.9M) in Trademarks, utilizing 10-to-40-year amortization schedules. Its net self-developed software stands at $87.3 million (€77.2M). Wiley’s definite-lived Content and Publishing Rights hold a net value of $414.2 million (26-year weighted average life), alongside customer relationships (16 years), brands (17 years), and $127.2 million in indefinite-lived assets. Notably, Wiley executed a $108.4 million non-cash impairment in 2024 to clear defunct internal segments, demonstrating the risk of software capitalization.

The transition to OA shifts credit risk from secure institutional libraries to fragmented research grants. Wiley mitigates this via geographical concentration, holding only a $13.77 million allowance on $244.1 million in net accounts receivable. Springer Nature’s broader exposure requires an allowance of €60.9 million ($68.8M) against gross AR of €384.3 million ($434.5M)—a 15.8% bad debt allowance rate—though tightened credit controls reduced its annual write-off provision to $35.84 million (€31.7M) from $54.38 million (€48.1M) in the prior period.

The Integrity CapEx Imperative

Ultimately, AI-generated "paper mills" threaten the core monetization engine of these entities. Wiley explicitly states that integrity failures force the company to pause, retract, or halt journals entirely, directly severing APC pipelines. To defend the ecosystem, Wiley integrates AI directly into ReX for automated, upstream metadata extraction prior to peer review. Springer Nature attacks the threat via human capital and open-source deterrence, employing 75 dedicated integrity specialists equipped with proprietary non-standard-phrases detectors and irrelevant-reference checkers. By donating its nonsense-text detector to the STM Integrity Hub, Springer Nature is cementing a multi-publisher deterrence grid. For institutional investors, this defensive CapEx is non-negotiable; entities that fail to automate fraud detection will face margin collapse as manual editorial costs outstrip volume-driven OA revenue.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* John Wiley & Sons, Inc. [NYSE: WLY] reported flat FY2026 revenue of $1,676.5 million (-1.0% constant currency), dragged by a 7% contraction in Learning, while Springer Nature AG & Co. KGaA [FSE: SPG] achieved $2,178.0 million (€1,926.4 million), driven by 20% growth in Open Access (OA) article volumes.

* Geopolitical risk bifurcates the sector: Wiley relies on China-based authors for 31% of its published articles amid US-China trade tensions, whereas Springer Nature mitigates regional risk through a globally balanced footprint yielding $636.9 million across APAC markets, including Taiwan, China, and a 20-university consortium in Malaysia.

* Platform capitalization is redefining the industry cost structure; both firms are leveraging multi-year Transformative Agreements (TAs) to bypass stagnant library budgets, utilizing artificial intelligence screening to automate workflow, defend brand impact factors, and secure highly predictable, negative working capital profiles.

Figure The New Scholarly Monopoly: Wiley vs Springer Nature (2025-2026 Strategic Audit)

Segmental Realities and Margin CompressionA forensic analysis of FY2025/2026 disclosures reveals diverging trajectories in top-line growth, operating leverage, and capital structures. (Note: Springer Nature financial conversions are calculated at a 2025 average rate of 1 EUR = 1.1306 USD).

Springer Nature AG & Co. KGaA: Top-Line Expansion

Total revenue reached $2,178.0 million (€1,926.4 million), driven by comprehensive segment growth:

* Research: Generated $1,715.3 million (€1,517.2 million), achieving 7.4% underlying growth. Transactional revenue hit $692.7 million (€612.7 million), primarily fueled by OA Article Processing Charges (APCs).

* Health: Contributed $216.0 million (€191.0 million), posting a 2.7% underlying growth rate, supported by scientific writing services despite advertising restraint in the German pharmaceutical sector.

* Education: Generated $248.5 million (€219.8 million) with a 0.8% underlying growth rate. Government stimulus in Argentina (adjusted for IAS 29 hyperinflation) and India offset foreign exchange volatility from the Mexican peso, Indian rupee, and K-12 curriculum funding delays in South Africa.

John Wiley & Sons, Inc.: Bifurcated Portfolio

Total revenue registered at $1,676.5 million (-1.0% constant currency), reflecting structural divergence:

* Research (67% of total): Generated $1,129.9 million (+4% constant currency). The Research Publishing division contributed $965.8 million (+3% constant currency), while Research Solutions reached $164.2 million (+6% constant currency), capturing $49.1 million in AI licensing revenue (up from $40.0 million in the prior year).

* Learning (33% of total): Generated $546.6 million (-7% constant currency). The Academic division fell 5% to $318.8 million, and the Professional division plummeted 10% to $227.8 million due to retail channel weakness across franchises like For Dummies and Everything DiSC.

Cash Flow, Profitability, and Capital Structure Matrix

* Earnings Quality: Springer Nature reported Adjusted EBITDA of $806.3 million (€713.2M) and Adjusted Operating Profit of $614.6 million. Operating Cash Flow (OCF) reached $620.9 million (€549.2M), converting to Free Cash Flow (FCF) of $336.7 million (€297.8M) for a 41.7% conversion rate. Wiley recorded Adjusted EBITDA of $439.6 million, Adjusted Operating Income of $296.2 million, OCF of $260.5 million, and FCF of $195.3 million, yielding a 44.4% conversion rate.

* Leverage & Maturities: Springer Nature executed a $565.3 million (€500M) promissory note refinancing, operating at a 1.7x Net Debt to EBITDA ratio with 31.4% of its debt hedged. Maturities are staged in Nov/Dec 2028 (Term Loans B & C, plus €210M in notes) and Nov 2030 (€290M in notes). Wiley operates with leaner leverage at 1.38x Net Debt to Adj. EBITDA, carrying $608.1 million in net debt ($683.7 million total variable-rate debt offset by $75.6 million cash). Wiley faces a concentrated $671.2 million maturity wall in November 2027 (Term Loan A and Revolver).

Infrastructure Layout and Regional Moats

Geographic revenue distribution and digital infrastructure explicitly define the competitive moats for both publishers, functioning simultaneously as distribution channels and defensive mechanisms against AI-generated paper mills.

Geographic Concentration vs. Diversification

Wiley’s footprint is intensely concentrated, deriving 80% of total revenue from the United States ($854.5 million; 51.0%) and the United Kingdom ($490.4 million; 29.3%). Germany contributed $192.3 million (11.5%), with the remainder of the globe generating $139.3 million (8.3%). Conversely, Springer Nature operates a balanced matrix: the Americas generated $686.8 million (€607.5M), heavily weighted by $505.4 million (€447.0M) from the US. The APAC region delivered $636.9 million (€563.3M), and EMEA contributed $600.1 million (€530.8M), with Germany accounting for $254.2 million (€224.8M).

Technological Capital Expenditures and B2B Platforms

Both firms are actively migrating capital toward fixed digital infrastructure to facilitate zero-marginal-cost volume scaling.

* Springer Nature Ecosystem: Total cumulative technology spend reached $212.6 million (€188M) since 2021. In FY2025, cash paid for intangibles was $24.0 million (€21.2M) alongside $8.8 million (€7.8M) for property, plant, and equipment. The firm capitalized $44.7 million (€39.5M) in internal software and content creation costs. The proprietary Snapp (Springer Nature Article Processing Platform) has processed 3.7 million submissions to date. Content distribution relies on Springer Nature Link (18 million active monthly users), while corporate operations utilize Text and Data Mining (TDM) tools, AskAdis for pharmaceuticals, and Medbee (serving 43,000 doctors among the company's 324,000 global healthcare professional users). The Nature Research Assistant is currently in beta with over 20,000 users.

* Wiley Ecosystem: Wiley deployed $51.2 million in technology and PPE, plus $14.0 million in product development, totaling $65.2 million. Gross capitalized software reached $687.4 million, registering a $61.7 million amortization expense based on a rapid 3-year useful life cycle. Infrastructure centers on Research Exchange (ReX) for AI-enabled manuscript screening and the Atypon platform, which hosts B2B content for approximately 2,000 competitor publishers and societies. Wiley also monetizes R&D through the Cochrane Library for Evidence-Based Medicine (EBM) and Spectral databases for microscopy and bioanalysis.

Throughput Dynamics, Quality Filters, and Consortia Lock-ins

In 2025, Springer Nature received 3.1 million submissions across its 3,000+ journals (770 Gold OA, 2,200 Springer hybrid, 66 Nature hybrid). It published 539,000 primary articles, enforcing an 82.6% implied rejection rate (17.4% acceptance rate). Of the published output, 288,419 were OA articles (+20% year-over-year), pushing OA penetration above 53%. The firm secured 85 Transformative Agreements (19 new, 17 renewed) covering 4,000 institutions (including DEAL, LYRASIS, and the Big Ten Academic Alliance), resulting in over 63,000 OA articles funded via TAs (+12%). To support global parity, Springer Nature waived $24.87 million (€22M) in APCs.

Wiley commands 8% of global titles and articles, generating 10% of global citations across its 1,900+ journals. The publisher grew OA output by 25%. A critical operational dependency exists through prestigious society partnerships, which secure 46% of Wiley's Journal Subscriptions revenue.

HDIN Institutional Verdict

The institutional evaluation of these academic publishing entities hinges on their divergent approaches to working capital optimization and algorithmic defense mechanisms against industry fraud.

Working Capital Optimization and Deferred Revenue Moats

The legacy subscription model allows both firms to function with structurally negative working capital by collecting upfront cash. Wiley operates with superior balance sheet efficiency, recording negative net working capital of -$359.3 million. The firm holds $468.6 million in contract liabilities ($451.4 million short-term), representing 28.0% of total revenue, which drives its lean Days Sales Outstanding (DSO) of 53 days. Wiley secures 48% of its total revenue via contractually obligated recurring streams, embedding explicit fixed price escalators into its 2-to-5-year Atypon hosting contracts to guarantee compounding yield.

Springer Nature carries $353.1 million (€312.3M) in contract liabilities, representing 16.2% of revenue. This lower deferred revenue ratio reflects its aggressive pivot toward transactional OA models. While its DSO sits higher at 61 days, Springer Nature utilizes volume metrics to defend pricing during institutional negotiations, registering 5.6 billion downloads (+50% year-over-year) to orchestrate a 54% drop in the average cost per download since 2019. This protects its estimated ~$2,400 per-unit APC proxy and secures high author (87%) and reviewer (88%) satisfaction rates.

Intangible Assets and Credit Risk Exposures

The capitalization of intellectual property dictates balance sheet risk. Springer Nature carries $1,065.3 million (€942.2M) in Publishing Rights and $1,079.6 million (€954.9M) in Trademarks, utilizing 10-to-40-year amortization schedules. Its net self-developed software stands at $87.3 million (€77.2M). Wiley’s definite-lived Content and Publishing Rights hold a net value of $414.2 million (26-year weighted average life), alongside customer relationships (16 years), brands (17 years), and $127.2 million in indefinite-lived assets. Notably, Wiley executed a $108.4 million non-cash impairment in 2024 to clear defunct internal segments, demonstrating the risk of software capitalization.

The transition to OA shifts credit risk from secure institutional libraries to fragmented research grants. Wiley mitigates this via geographical concentration, holding only a $13.77 million allowance on $244.1 million in net accounts receivable. Springer Nature’s broader exposure requires an allowance of €60.9 million ($68.8M) against gross AR of €384.3 million ($434.5M)—a 15.8% bad debt allowance rate—though tightened credit controls reduced its annual write-off provision to $35.84 million (€31.7M) from $54.38 million (€48.1M) in the prior period.

The Integrity CapEx Imperative

Ultimately, AI-generated "paper mills" threaten the core monetization engine of these entities. Wiley explicitly states that integrity failures force the company to pause, retract, or halt journals entirely, directly severing APC pipelines. To defend the ecosystem, Wiley integrates AI directly into ReX for automated, upstream metadata extraction prior to peer review. Springer Nature attacks the threat via human capital and open-source deterrence, employing 75 dedicated integrity specialists equipped with proprietary non-standard-phrases detectors and irrelevant-reference checkers. By donating its nonsense-text detector to the STM Integrity Hub, Springer Nature is cementing a multi-publisher deterrence grid. For institutional investors, this defensive CapEx is non-negotiable; entities that fail to automate fraud detection will face margin collapse as manual editorial costs outstrip volume-driven OA revenue.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."