ispace inc.: Strategic Hardware Pivot Near Denver Subsidiary Triggers $63.58 Million Capital Lock-Up as Advance Payments Signal Severe Liquidity Compression

Date : 2026-06-27

Reading : 181

HDIN Executive Takeaways

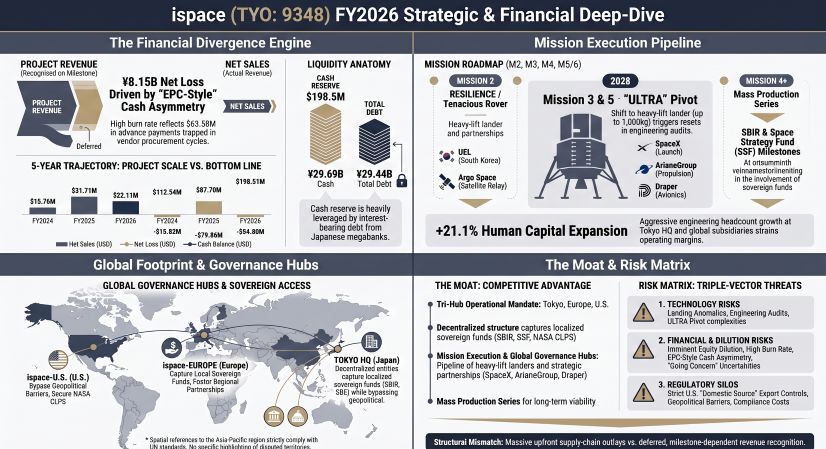

* ispace, inc.'s cash burn accelerated to negative $90.72 million in FY2026, offsetting a $198.51 million liquidity position heavily subsidized by a $100.29 million debt facility.

* A structural pivot to the 1,000kg-capacity ULTRA lander at the Denver-based subsidiary forced a $24.66 million non-consolidated write-down and trapped $63.58 million in non-refundable vendor advances.

* Institutional viability relies strictly on bridging a 24-month working capital deficit before the March 2027 going-concern projection window expires, necessitating continued equity dilution.

Figure ispace FY2026 Strategic & Financial Deep-Dive

Segmental Realities and Capital Allocation Mechanics

ispace, inc. [TSE: 9348] is currently operating in a pre-profitability phase defined by a structural mismatch between immediate supply chain cash outflows and highly deferred, milestone-dependent revenue recognition. Financial figures, evaluated at a fixed conversion rate of 1 USD = 149.5686 JPY, expose an Engineering, Procurement, and Construction (EPC) infrastructure profile rather than a traditional software or logistics business model.

The consolidated financial trajectory demonstrates exponential top-line scaling fully offset by compounding operational costs. In FY2026, ispace, inc. generated $22.11 million in Net Sales but recorded $41.19 million in Cost of Sales (escalated from $24.48 million in FY2025), resulting in a Gross Loss of $19.08 million. Selling, General, and Administrative (SG&A) expenses absorbed $58.35 million in FY2026. Within this overhead, Research and Development (R&D) expenses rose from $10.34 million in FY2025 to $13.52 million in FY2026, while fixed personnel costs for salaries and allowances expanded 21.1% from $10.18 million to $12.33 million year-over-year.

To bridge this operational deficit, the company relies heavily on capital markets. Total cash flow from financing activities for FY2026 reached $210.25 million, anchored by a $100.29 million bank borrowing initiated in May 2025 titled "SMBC x HAKUTO-R VENTURE MOON" via Sumitomo Mitsui Banking Corporation (SMBC). This was supplemented by a $122.08 million capital stock issuance and equity raise, executing dilution programs with institutional entities including Heights Capital Management, Inc. and CVI Investments, Inc. The IF GROWTH OPPORTUNITY FUND, L.P. SMBC remains integrated as a major stakeholder.

Table ispace, inc. 5-Year Financial Trend Analysis (FY2022–FY2026)

Payload Service Agreement (PSA) revenue is governed by a rigid 10-step "Success Milestone" accounting policy. Cash inflows are secured upfront as deposits, but Net Sales are strictly deferred until engineering verification. Milestones scale from "Success 1" (Launch Readiness Completed) through "Success 3" (Establishment of Stable Navigation), reaching "Success 9" (Lunar Landing Completed) and "Success 10" (Steady State Operations). During Mission 1, telemetry was lost prior to touchdown, preventing the achievement of Success 9 and 10 and voiding the P&L realization of the final contracted revenue.

Infrastructure Layout and Monopolistic Supply Chain Dependencies

ispace, inc. operates a decentralized, tri-hub corporate structure to circumvent geopolitical export controls and capture localized sovereign capital. Corporate governance is executed by a seven-member Board of Directors (five Outside Directors) and a three-member Audit & Supervisory Committee (two Outside Members).

The Tokyo, Japan headquarters (comprising ispace, inc. and subsidiary ispace Ops Japan) centralizes software platform development and secures domestic base-load subsidies, specifically the Japanese government's Small Business Innovation Research (JP SBIR) and Space Strategy Fund (SSF1 and SSF2) initiatives. The Asian pipeline is further supported by international PSAs, notably a payload contract with the space agency of Taiwan, Province of China, which recognized $3.01 million in net sales during FY2025, alongside commercial partnerships such as South Korea's Unmanned Exploration Laboratory (UEL).

In Luxembourg, ispace-EUROPE S.A. functions as the precision engineering hub, developing the TENACIOUS micro-rover for the January 2025 Mission 2 (RESILIENCE lander) execution. The European arm successfully acts as the conduit for European Space Agency (ESA) contracts, recognizing $3.51 million in FY2025.

In Denver, Colorado, ispace technologies U.S., inc. is siloed to comply with U.S. domestic sourcing requirements for Department of Defense and NASA funding, specifically targeting the Commercial Lunar Payload Services (CLPS CP-12) contract for Mission 5 in 2030. The U.S. entity is executing a structural transition from the 200kg-class APEX 1.0 lander to the "ULTRA" model, designed to accommodate payloads between 300kg and 1,000kg. This pivot necessitated the repetition of Preliminary Design Reviews (PDR), Critical Design Reviews (CDR), and Pre-Shipment Reviews (PSR) ahead of the planned Mission 3 (2028) launch, mechanically triggering a $24.66 million valuation loss adjustment on the parent company’s non-consolidated balance sheet.

Supply chain mechanics reveal absolute reliance on Tier-1 aerospace monopolies, quantified by $63.58 million in advance payments sitting on the balance sheet. ispace, inc. maintains a Launch Service Agreement executed August 29, 2018, with Space Exploration Technologies Corp. (SpaceX) for Falcon 9 transport, a manufacturing consignment agreement with ArianeGroup for propulsion systems, and master agreements with The Charles Stark Draper Laboratory, Inc. for guidance avionics (an initial 2018 HQ contract and a June 2023 US-specific contract). Furthermore, the firm aims to establish a commercial lunar satellite network relay via a partnership with Argo Space Corp., targeting Mission 2.5 around 2027 to transition into high-margin Cislunar Digital Twin data services.

HDIN Institutional Verdict

The FY2026 auditor's report explicitly features a section on significant uncertainties regarding the company's ability to continue as a going concern. While the current $198.51 million cash reserve appears robust, the structural burn rate of negative $90.72 million in annual operating cash flow limits the theoretical linear runway to exactly 2.18 years.

Management's defense against this going concern qualification relies entirely on internal mathematical liquidity modeling extending only to March 31, 2027. Because ispace, inc. functions as a system integrator rather than a vertically integrated manufacturer, the multi-year lead times demanded by SpaceX and ArianeGroup force continuous cash outflows 24 to 36 months before mission execution. The absence of predefined emergency credit lines indicates a rigid balance sheet highly dependent on the SMBC network. Should external vendor delays freeze the CDR or PDR integration phases for the ULTRA lander, the timeline mismatch between the $63.58 million in executed vendor prepayments and the delayed 10-step customer milestone revenue will compress this 24-month window, mechanically forcing the firm into aggressive equity dilution prior to its target mass production phase in 2030.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* ispace, inc.'s cash burn accelerated to negative $90.72 million in FY2026, offsetting a $198.51 million liquidity position heavily subsidized by a $100.29 million debt facility.

* A structural pivot to the 1,000kg-capacity ULTRA lander at the Denver-based subsidiary forced a $24.66 million non-consolidated write-down and trapped $63.58 million in non-refundable vendor advances.

* Institutional viability relies strictly on bridging a 24-month working capital deficit before the March 2027 going-concern projection window expires, necessitating continued equity dilution.

Figure ispace FY2026 Strategic & Financial Deep-Dive

Segmental Realities and Capital Allocation Mechanics

ispace, inc. [TSE: 9348] is currently operating in a pre-profitability phase defined by a structural mismatch between immediate supply chain cash outflows and highly deferred, milestone-dependent revenue recognition. Financial figures, evaluated at a fixed conversion rate of 1 USD = 149.5686 JPY, expose an Engineering, Procurement, and Construction (EPC) infrastructure profile rather than a traditional software or logistics business model.

The consolidated financial trajectory demonstrates exponential top-line scaling fully offset by compounding operational costs. In FY2026, ispace, inc. generated $22.11 million in Net Sales but recorded $41.19 million in Cost of Sales (escalated from $24.48 million in FY2025), resulting in a Gross Loss of $19.08 million. Selling, General, and Administrative (SG&A) expenses absorbed $58.35 million in FY2026. Within this overhead, Research and Development (R&D) expenses rose from $10.34 million in FY2025 to $13.52 million in FY2026, while fixed personnel costs for salaries and allowances expanded 21.1% from $10.18 million to $12.33 million year-over-year.

To bridge this operational deficit, the company relies heavily on capital markets. Total cash flow from financing activities for FY2026 reached $210.25 million, anchored by a $100.29 million bank borrowing initiated in May 2025 titled "SMBC x HAKUTO-R VENTURE MOON" via Sumitomo Mitsui Banking Corporation (SMBC). This was supplemented by a $122.08 million capital stock issuance and equity raise, executing dilution programs with institutional entities including Heights Capital Management, Inc. and CVI Investments, Inc. The IF GROWTH OPPORTUNITY FUND, L.P. SMBC remains integrated as a major stakeholder.

Table ispace, inc. 5-Year Financial Trend Analysis (FY2022–FY2026)

| Fiscal Year | Net Sales | Net Loss | Operating Cash Flow | Cash Balance |

|---|---|---|---|---|

| FY2022 | $4.51 million | $(27.14) million | $(36.14) million | $42.34 million |

| FY2023 | $6.61 million | $(76.21) million | $(48.96) million | $22.61 million |

| FY2024 | $15.76 million | $(15.82) million | $(33.59) million | $112.54 million |

| FY2025 | $31.71 million | $(79.86) million | $(80.56) million | $87.70 million |

| FY2026 | $22.11 million | $(54.50) million | $(90.72) million | $198.51 million |

Payload Service Agreement (PSA) revenue is governed by a rigid 10-step "Success Milestone" accounting policy. Cash inflows are secured upfront as deposits, but Net Sales are strictly deferred until engineering verification. Milestones scale from "Success 1" (Launch Readiness Completed) through "Success 3" (Establishment of Stable Navigation), reaching "Success 9" (Lunar Landing Completed) and "Success 10" (Steady State Operations). During Mission 1, telemetry was lost prior to touchdown, preventing the achievement of Success 9 and 10 and voiding the P&L realization of the final contracted revenue.

Infrastructure Layout and Monopolistic Supply Chain Dependencies

ispace, inc. operates a decentralized, tri-hub corporate structure to circumvent geopolitical export controls and capture localized sovereign capital. Corporate governance is executed by a seven-member Board of Directors (five Outside Directors) and a three-member Audit & Supervisory Committee (two Outside Members).

The Tokyo, Japan headquarters (comprising ispace, inc. and subsidiary ispace Ops Japan) centralizes software platform development and secures domestic base-load subsidies, specifically the Japanese government's Small Business Innovation Research (JP SBIR) and Space Strategy Fund (SSF1 and SSF2) initiatives. The Asian pipeline is further supported by international PSAs, notably a payload contract with the space agency of Taiwan, Province of China, which recognized $3.01 million in net sales during FY2025, alongside commercial partnerships such as South Korea's Unmanned Exploration Laboratory (UEL).

In Luxembourg, ispace-EUROPE S.A. functions as the precision engineering hub, developing the TENACIOUS micro-rover for the January 2025 Mission 2 (RESILIENCE lander) execution. The European arm successfully acts as the conduit for European Space Agency (ESA) contracts, recognizing $3.51 million in FY2025.

In Denver, Colorado, ispace technologies U.S., inc. is siloed to comply with U.S. domestic sourcing requirements for Department of Defense and NASA funding, specifically targeting the Commercial Lunar Payload Services (CLPS CP-12) contract for Mission 5 in 2030. The U.S. entity is executing a structural transition from the 200kg-class APEX 1.0 lander to the "ULTRA" model, designed to accommodate payloads between 300kg and 1,000kg. This pivot necessitated the repetition of Preliminary Design Reviews (PDR), Critical Design Reviews (CDR), and Pre-Shipment Reviews (PSR) ahead of the planned Mission 3 (2028) launch, mechanically triggering a $24.66 million valuation loss adjustment on the parent company’s non-consolidated balance sheet.

Supply chain mechanics reveal absolute reliance on Tier-1 aerospace monopolies, quantified by $63.58 million in advance payments sitting on the balance sheet. ispace, inc. maintains a Launch Service Agreement executed August 29, 2018, with Space Exploration Technologies Corp. (SpaceX) for Falcon 9 transport, a manufacturing consignment agreement with ArianeGroup for propulsion systems, and master agreements with The Charles Stark Draper Laboratory, Inc. for guidance avionics (an initial 2018 HQ contract and a June 2023 US-specific contract). Furthermore, the firm aims to establish a commercial lunar satellite network relay via a partnership with Argo Space Corp., targeting Mission 2.5 around 2027 to transition into high-margin Cislunar Digital Twin data services.

HDIN Institutional Verdict

The FY2026 auditor's report explicitly features a section on significant uncertainties regarding the company's ability to continue as a going concern. While the current $198.51 million cash reserve appears robust, the structural burn rate of negative $90.72 million in annual operating cash flow limits the theoretical linear runway to exactly 2.18 years.

Management's defense against this going concern qualification relies entirely on internal mathematical liquidity modeling extending only to March 31, 2027. Because ispace, inc. functions as a system integrator rather than a vertically integrated manufacturer, the multi-year lead times demanded by SpaceX and ArianeGroup force continuous cash outflows 24 to 36 months before mission execution. The absence of predefined emergency credit lines indicates a rigid balance sheet highly dependent on the SMBC network. Should external vendor delays freeze the CDR or PDR integration phases for the ULTRA lander, the timeline mismatch between the $63.58 million in executed vendor prepayments and the delayed 10-step customer milestone revenue will compress this 24-month window, mechanically forcing the firm into aggressive equity dilution prior to its target mass production phase in 2030.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."