Nikon Corporation: M&A Premium Clearances Mask B2B Capital Reallocation as 292-Day Inventory Cycle Signals Working Capital Friction

Date : 2026-06-27

Reading : 350

HDIN Executive Takeaways

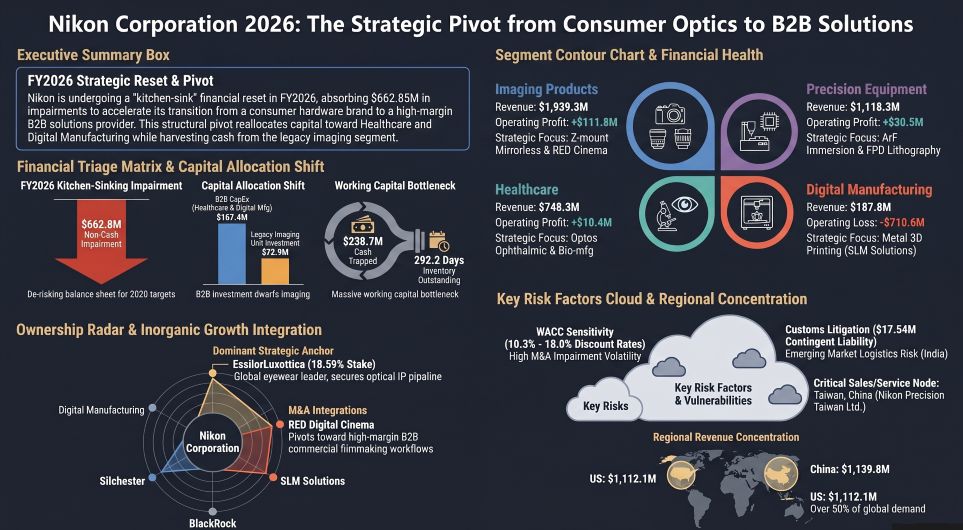

* Nikon Corporation [TYO: 7731] recorded a $751.8 million (JPY 112.4 billion) consolidated operating loss, driven by $662.85 million in non-financial impairments, artificially depressing FY2026 margins to clear legacy M&A premiums.

* Inventory bloated to 292.2 Days Outstanding ($2.22 billion), forcing a $33.74 million retirement trust liquidation to extract trapped liquidity amidst CapEx delays at Asian semiconductor foundries.

* Institutional restructuring shifts capital toward B2B nodes, aligning Performance Share Unit (PSU) executive compensation directly to a 7% ROIC and 10% ROE hurdle rate by FY2030.

Table Nikon Corporation 2026: The Strategic Pivot from Consumer Optics to B2B Solutions

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

For FY2026, Nikon Corporation generated a consolidated revenue of $4,527.4 million (JPY 677.16 billion) against a total operating loss of $751.8 million (JPY 112.4 billion). The top-line stability was negated by severe macroeconomic friction, an escalating cost of capital, and CapEx delays in semiconductor and Flat Panel Display (FPD) lithography, triggering massive non-financial asset impairments. Operations yielded an 11.4% R&D-to-revenue intensity, totaling $516.1 million (JPY 77.19 billion).

The regional revenue distribution exposes a heavy reliance on export markets, mapping as follows: China at 25.1% ($1,139.8 million / JPY 170.47 billion); the United States at $1,112.1 million (JPY 166.33 billion); Europe at $811.2 million (JPY 121.33 billion); Others at $793.6 million (JPY 118.70 billion); and Japan at 14.8% ($670.7 million / JPY 100.32 billion). Exchange calculations mandate a fixed average rate of 1 USD = 149.5686 JPY.

Table Consolidated Segmental Operations & Capital Deployment

Note: Precision Equipment operating profit fell 84.6% year-over-year. Imaging CapEx contracted 54.6% year-over-year. Healthcare CapEx expanded 52.5% year-over-year. Combined FY2026 CapEx for Healthcare, Digital Manufacturing, and Components reached $167.4 million, dwarfing the $72.97 million allocated to legacy Imaging.

Valuation Adjustments and Asset Impairments ($662.85M / JPY 99.14B Total)

Management executed severe write-downs of inorganic acquisition premiums, adjusting the Weighted Average Cost of Capital (WACC) to reflect tightening global liquidity:

* Nikon SLM Solutions AG: $404.95 million (JPY 60.57 billion) impairment. Determined via Fair Value Less Costs of Disposal, applying a post-tax discount rate of 10.3%.

* Optos Plc: $190.15 million (JPY 28.44 billion) impairment. Total Healthcare segment write-downs reached $191.77 million (JPY 28.68 billion). Determined via Value in Use, applying a post-tax discount rate of 10.7% (a 10-basis-point increase from 10.6%) and reducing the terminal growth rate to 2.1% (a 20-basis-point contraction from 2.3%).

* Mark Roberts Motion Control Limited: $5.68 million (JPY 850 million) impairment. Determined via Value in Use, applying a highly punitive pre-tax discount rate of 18.0%.

Working Capital Friction & Inventory Stratification

Total operating cash flow collapsed from $467.93 million (JPY 69.98 billion) in FY2025 to $84.26 million (JPY 12.60 billion) in FY2026, primarily starved by a massive inventory buildout of $2,225.55 million (JPY 332.87 billion). Average inventory stood at $2,140.84 million against a COGS of $2,673.71 million.

* Asset Quality: Merchandise and Finished Goods at $886.19 million (JPY 132.54 billion); Work in Progress (WIP) at $868.60 million (JPY 129.91 billion); Raw Materials at $470.76 million (JPY 70.41 billion).

* Metrics: Days Inventory Outstanding (DIO) reached 292.2 days, draining $238.70 million (JPY 35.70 billion) from operating cash flows. Days Sales Outstanding (DSO) stabilized at 68.2 days based on average trade receivables of $845.43 million.

* Write-Downs: Cyclical CapEx delays forced temporary inventory write-downs of $121.82 million (JPY 18.22 billion), scaling up from $86.05 million (JPY 12.87 billion) in FY2025.

Infrastructure Layout and Regional Moats

Nikon operates a highly decentralized physical value chain, acting as an inherent FX hedge against Japanese Yen (JPY) volatility by anchoring localized operating expenses and COGS to the Thai Baht (THB), Lao Kip (LAK), and Chinese Yuan (CNY).

Geographic Supply Chain Architecture:

* Japan (Core IP & Precision Manufacturing): Sendai Nikon and Tochigi Nikon retain strictly guarded manufacturing for ArF immersion and Flat Panel Display lithography systems. Hikari Glass Co., Ltd. serves as a vertically integrated subsidiary for proprietary chemical and optical glass formulation, insulating Nikon from external component monopolies.

* Southeast Asia (Imaging Assembly): Mass-market final assembly is offshored to Nikon Thailand Co., Ltd. and Nikon Lao Co., Ltd.

* Mainland China & Taiwan (Regional Nodes): Sales, installation, and biological manufacturing are executed via Nanjing Nikon Jiangnan Optical Instrument Co., Ltd., Nikon Precision Taiwan Ltd., Nikon Precision (Shanghai) Co., Ltd., Nikon Imaging China Sales Co., Ltd., and Nikon Hong Kong Ltd.

* Europe & United States (Digital & Cinema Expansion): Additive manufacturing is centralized at Nikon SLM Solutions AG (Germany). Specialized R&D and healthcare nodes are anchored by Mark Roberts Motion Control Limited (UK), Optos Plc (UK), and Nikon AM Synergy Inc. (California). The acquisition of RED Digital Cinema, Inc. (California) integrates RED ONE 4K, V-RAPTOR X, and RAW technology, accelerating US-based high-margin B2B cinema manufacturing alongside Nikon Inc. (US) and Nikon Europe B.V.

Governance, Contingencies, and IP Defense:

Procurement vulnerabilities are governed by a Supply Chain Subcommittee, Sustainable Procurement Promotion Meeting, and Green Procurement Promotion Meeting, utilizing Responsible Business Alliance (RBA) audits, TCFD climate modeling, Business Continuity Planning (BCP), and ISMS protocols overseen by a CISO.

Legal exposures are highly isolated. Nikon registered a specific contingent liability of $17.54 million (JPY 2,624 million / JPY 2.624 billion) regarding an ongoing customs and excise tax dispute with the CESTAT appellate tribunal in India. Intellectual property risks within the Precision Equipment segment are legally neutralized through 2029 via a cross-license agreement with ASML Holding N.V. and Carl Zeiss SMT AG.

HDIN Institutional Verdict

Nikon is structurally liquidating its reliance on consumer unit volumes. The product mix reflects this with aggressive prioritization of the Z9, Z8, NIKKOR Z 24-70mm f/2.8 S II, NIKKOR Z 70-200mm f/2.8 VR S II, Morf3D additive technologies, the NXG XII 600 platform, and NIS-Elements LE AI software.

The capitalization table highlights rigorous external oversight. EssilorLuxottica anchors the equity base with an 18.59% stake (62.03 million shares), structurally monetizing optical IP via the Nikon-Essilor Co., Ltd. joint venture without associated retail CapEx. Foreign and domestic institutional capital dictates board strategy, led by Silchester International Investors LLP holding 8.10% (27.01 million shares), Nomura Securities at 5.23% (17.45 million shares), BlackRock, Inc. at 5.10% (17.93 million shares), and The Master Trust Bank of Japan retaining 13.88% in primary custody.

Capital Allocation and Liquidity Engineering:

To bypass the 292-day inventory trap, management executed a partial termination of an overfunded retirement benefit trust, extracting $33.74 million (JPY 5.047 billion) in cash. The consolidated defined benefit profile remains structurally overfunded: present value of obligations is $801.29 million (JPY 119.84 billion) against plan assets of $877.41 million (JPY 131.23 billion). This yields a net asset of $172.60 million (JPY 25.81 billion) offsetting underfunded regional liabilities of $117.67 million (JPY 17.6 billion). Contractual commitments for property, plant, and equipment are contained at $26.86 million (JPY 4.017 billion).

2026–2030 Mid-Term Trajectory:

The board disbursed $1.96 million (JPY 293 million) in Director compensation while disposing of 638,537 treasury shares valued at $6.47 million (JPY 968 million) to fund the Long-Term Incentive (LTI) restructure. PSU vesting is now aggressively tied to a 30% ROIC weight, 20% ROE weight, 40% TSR/TOPIX ratio, and 10% DX/Sustainability metric.

Management's 2030 objective targets $6,685.9 million (JPY 1 trillion) in top-line revenue and $534.9 million (JPY 80 billion) in operating profit, achieving a 7% ROIC and 10% ROE. Baseline operating profit targets map from $66.9 million (JPY 10 billion) in FY2026 to $334.3 million (JPY 50 billion) by FY2028. This growth is funded by a projected $5,348.7 million (JPY 800 billion) operating cash flow pool—allocating >50% to high-growth ArF, EUV, and digital vectors, 45-50% to R&D, ~40% to CapEx, and ~10% to shareholder returns.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Nikon Corporation [TYO: 7731] recorded a $751.8 million (JPY 112.4 billion) consolidated operating loss, driven by $662.85 million in non-financial impairments, artificially depressing FY2026 margins to clear legacy M&A premiums.

* Inventory bloated to 292.2 Days Outstanding ($2.22 billion), forcing a $33.74 million retirement trust liquidation to extract trapped liquidity amidst CapEx delays at Asian semiconductor foundries.

* Institutional restructuring shifts capital toward B2B nodes, aligning Performance Share Unit (PSU) executive compensation directly to a 7% ROIC and 10% ROE hurdle rate by FY2030.

Table Nikon Corporation 2026: The Strategic Pivot from Consumer Optics to B2B Solutions

Segmental Realities and Margin CompressionFor FY2026, Nikon Corporation generated a consolidated revenue of $4,527.4 million (JPY 677.16 billion) against a total operating loss of $751.8 million (JPY 112.4 billion). The top-line stability was negated by severe macroeconomic friction, an escalating cost of capital, and CapEx delays in semiconductor and Flat Panel Display (FPD) lithography, triggering massive non-financial asset impairments. Operations yielded an 11.4% R&D-to-revenue intensity, totaling $516.1 million (JPY 77.19 billion).

The regional revenue distribution exposes a heavy reliance on export markets, mapping as follows: China at 25.1% ($1,139.8 million / JPY 170.47 billion); the United States at $1,112.1 million (JPY 166.33 billion); Europe at $811.2 million (JPY 121.33 billion); Others at $793.6 million (JPY 118.70 billion); and Japan at 14.8% ($670.7 million / JPY 100.32 billion). Exchange calculations mandate a fixed average rate of 1 USD = 149.5686 JPY.

Table Consolidated Segmental Operations & Capital Deployment

| Business Segment | Revenue (USD / JPY) | Operating Profit (Loss) | FY25 CapEx → FY26 CapEx | FY25 D&A → FY26 D&A | FY26 R&D Allocation |

|---|---|---|---|---|---|

| Imaging Products | $1,939.3M / ¥290.05B | $111.8M / ¥16.71B | $160.84M → $72.97M | $56.30M → $65.43M | $160.5M / ¥24.01B |

| Precision Equipment | $1,118.3M / ¥167.26B | $30.5M / ¥4.56B | $62.55M → $65.01M | $35.27M → $25.17M | $144.6M / ¥21.62B |

| Healthcare | $748.3M / ¥111.92B | $10.4M / ¥1.56B | $50.62M → $77.20M | $44.18M → $47.22M | $53.2M / ¥7.95B |

| Digital Manufacturing | $187.8M / ¥28.09B | $(710.6M) / (¥106.28B) | $43.42M → $52.85M | $42.30M → $44.59M | $50.8M / ¥7.60B |

| Components | $509.3M / ¥76.17B | $63.9M / ¥9.55B | $68.28M → $37.35M | $37.19M → $37.75M | $34.3M / ¥5.14B |

Valuation Adjustments and Asset Impairments ($662.85M / JPY 99.14B Total)

Management executed severe write-downs of inorganic acquisition premiums, adjusting the Weighted Average Cost of Capital (WACC) to reflect tightening global liquidity:

* Nikon SLM Solutions AG: $404.95 million (JPY 60.57 billion) impairment. Determined via Fair Value Less Costs of Disposal, applying a post-tax discount rate of 10.3%.

* Optos Plc: $190.15 million (JPY 28.44 billion) impairment. Total Healthcare segment write-downs reached $191.77 million (JPY 28.68 billion). Determined via Value in Use, applying a post-tax discount rate of 10.7% (a 10-basis-point increase from 10.6%) and reducing the terminal growth rate to 2.1% (a 20-basis-point contraction from 2.3%).

* Mark Roberts Motion Control Limited: $5.68 million (JPY 850 million) impairment. Determined via Value in Use, applying a highly punitive pre-tax discount rate of 18.0%.

Working Capital Friction & Inventory Stratification

Total operating cash flow collapsed from $467.93 million (JPY 69.98 billion) in FY2025 to $84.26 million (JPY 12.60 billion) in FY2026, primarily starved by a massive inventory buildout of $2,225.55 million (JPY 332.87 billion). Average inventory stood at $2,140.84 million against a COGS of $2,673.71 million.

* Asset Quality: Merchandise and Finished Goods at $886.19 million (JPY 132.54 billion); Work in Progress (WIP) at $868.60 million (JPY 129.91 billion); Raw Materials at $470.76 million (JPY 70.41 billion).

* Metrics: Days Inventory Outstanding (DIO) reached 292.2 days, draining $238.70 million (JPY 35.70 billion) from operating cash flows. Days Sales Outstanding (DSO) stabilized at 68.2 days based on average trade receivables of $845.43 million.

* Write-Downs: Cyclical CapEx delays forced temporary inventory write-downs of $121.82 million (JPY 18.22 billion), scaling up from $86.05 million (JPY 12.87 billion) in FY2025.

Infrastructure Layout and Regional Moats

Nikon operates a highly decentralized physical value chain, acting as an inherent FX hedge against Japanese Yen (JPY) volatility by anchoring localized operating expenses and COGS to the Thai Baht (THB), Lao Kip (LAK), and Chinese Yuan (CNY).

Geographic Supply Chain Architecture:

* Japan (Core IP & Precision Manufacturing): Sendai Nikon and Tochigi Nikon retain strictly guarded manufacturing for ArF immersion and Flat Panel Display lithography systems. Hikari Glass Co., Ltd. serves as a vertically integrated subsidiary for proprietary chemical and optical glass formulation, insulating Nikon from external component monopolies.

* Southeast Asia (Imaging Assembly): Mass-market final assembly is offshored to Nikon Thailand Co., Ltd. and Nikon Lao Co., Ltd.

* Mainland China & Taiwan (Regional Nodes): Sales, installation, and biological manufacturing are executed via Nanjing Nikon Jiangnan Optical Instrument Co., Ltd., Nikon Precision Taiwan Ltd., Nikon Precision (Shanghai) Co., Ltd., Nikon Imaging China Sales Co., Ltd., and Nikon Hong Kong Ltd.

* Europe & United States (Digital & Cinema Expansion): Additive manufacturing is centralized at Nikon SLM Solutions AG (Germany). Specialized R&D and healthcare nodes are anchored by Mark Roberts Motion Control Limited (UK), Optos Plc (UK), and Nikon AM Synergy Inc. (California). The acquisition of RED Digital Cinema, Inc. (California) integrates RED ONE 4K, V-RAPTOR X, and RAW technology, accelerating US-based high-margin B2B cinema manufacturing alongside Nikon Inc. (US) and Nikon Europe B.V.

Governance, Contingencies, and IP Defense:

Procurement vulnerabilities are governed by a Supply Chain Subcommittee, Sustainable Procurement Promotion Meeting, and Green Procurement Promotion Meeting, utilizing Responsible Business Alliance (RBA) audits, TCFD climate modeling, Business Continuity Planning (BCP), and ISMS protocols overseen by a CISO.

Legal exposures are highly isolated. Nikon registered a specific contingent liability of $17.54 million (JPY 2,624 million / JPY 2.624 billion) regarding an ongoing customs and excise tax dispute with the CESTAT appellate tribunal in India. Intellectual property risks within the Precision Equipment segment are legally neutralized through 2029 via a cross-license agreement with ASML Holding N.V. and Carl Zeiss SMT AG.

HDIN Institutional Verdict

Nikon is structurally liquidating its reliance on consumer unit volumes. The product mix reflects this with aggressive prioritization of the Z9, Z8, NIKKOR Z 24-70mm f/2.8 S II, NIKKOR Z 70-200mm f/2.8 VR S II, Morf3D additive technologies, the NXG XII 600 platform, and NIS-Elements LE AI software.

The capitalization table highlights rigorous external oversight. EssilorLuxottica anchors the equity base with an 18.59% stake (62.03 million shares), structurally monetizing optical IP via the Nikon-Essilor Co., Ltd. joint venture without associated retail CapEx. Foreign and domestic institutional capital dictates board strategy, led by Silchester International Investors LLP holding 8.10% (27.01 million shares), Nomura Securities at 5.23% (17.45 million shares), BlackRock, Inc. at 5.10% (17.93 million shares), and The Master Trust Bank of Japan retaining 13.88% in primary custody.

Capital Allocation and Liquidity Engineering:

To bypass the 292-day inventory trap, management executed a partial termination of an overfunded retirement benefit trust, extracting $33.74 million (JPY 5.047 billion) in cash. The consolidated defined benefit profile remains structurally overfunded: present value of obligations is $801.29 million (JPY 119.84 billion) against plan assets of $877.41 million (JPY 131.23 billion). This yields a net asset of $172.60 million (JPY 25.81 billion) offsetting underfunded regional liabilities of $117.67 million (JPY 17.6 billion). Contractual commitments for property, plant, and equipment are contained at $26.86 million (JPY 4.017 billion).

2026–2030 Mid-Term Trajectory:

The board disbursed $1.96 million (JPY 293 million) in Director compensation while disposing of 638,537 treasury shares valued at $6.47 million (JPY 968 million) to fund the Long-Term Incentive (LTI) restructure. PSU vesting is now aggressively tied to a 30% ROIC weight, 20% ROE weight, 40% TSR/TOPIX ratio, and 10% DX/Sustainability metric.

Management's 2030 objective targets $6,685.9 million (JPY 1 trillion) in top-line revenue and $534.9 million (JPY 80 billion) in operating profit, achieving a 7% ROIC and 10% ROE. Baseline operating profit targets map from $66.9 million (JPY 10 billion) in FY2026 to $334.3 million (JPY 50 billion) by FY2028. This growth is funded by a projected $5,348.7 million (JPY 800 billion) operating cash flow pool—allocating >50% to high-growth ArF, EUV, and digital vectors, 45-50% to R&D, ~40% to CapEx, and ~10% to shareholder returns.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*