Dexerials Corporation: 2026 Capex Realignment Near East Asian Fabrication Nodes as 37.5% Segment Margin Signals Sustained Pricing Leverage

Date : 2026-07-03

Reading : 244

HDIN Executive Takeaways

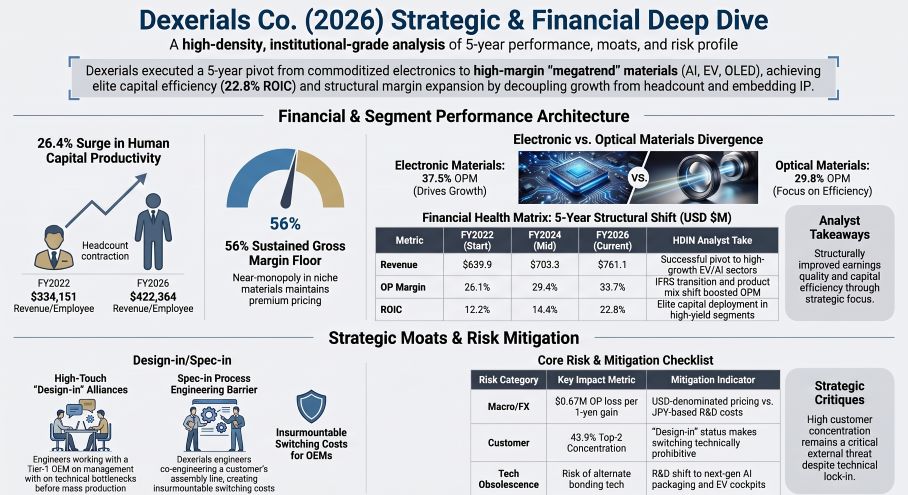

* Electronic Materials Operating Profit margin of 37.5% drove a $256.7M corporate operating profit, outperforming 2029 EBITDA targets by $12.65M amid a $168.7M CapEx outlay.

* Customer concentration reached 43.9% across two OEMs, amplifying FX vulnerability where a 1-Yen/USD swing erodes $2.27M in revenue across Suzhou and Taiwan, China operations.

* A 70% jump in underfunded pension liabilities to $68.75M strains equity targets, forcing $90.5M in FY2026 buybacks to bridge the gap toward a 31% ROE mandate.

Figure Dexerials Strategic & Financial Deep Dive

Segmental Realities and Financial Architecture

Segmental Realities and Financial Architecture

Dexerials Corporation [TYO: 4980] executes a dual-engine production model heavily consolidated around Anisotropic Conductive Films (ACF), Anti-Reflection Films (ARF), and Smart View Receptors (SVR). The transition to International Financial Reporting Standards (IFRS) from JGAAP has fundamentally altered balance sheet mechanics, ceasing goodwill amortization in favor of annual impairment testing. Applying a constant exchange rate of 1 USD = 149.5686 JPY, corporate top-line growth masks distinct segmental divergences.

Table Corporate 5-Year Financial Trajectory

FY2025 to FY2026 Segmental Dynamics:

* Optical Materials: Revenue contracted 5.3% to $320.7M (from $338.6M). Operating profit fell 1.6% to $95.7M (from $97.3M), yet operating margins expanded 110 basis points to 29.8%. FY2026 production value equaled $325.7M (99.2% of FY2025) against sales value of $315.3M.

* Electronic Materials: Revenue expanded 10.4% to $446.1M (from $404.1M). Operating profit rose 6.5% to $167.4M (from $157.2M), with margins contracting 140 basis points to 37.5%. FY2026 production value hit $451.9M (113.0% of FY2025) against sales value of $445.7M.

Revenue generation relies on a 43.9% top-two customer concentration. Customer A represents $246.9M (32.5% of total revenue) and Customer B accounts for $86.6M (11.4%). Pricing leverage is verified by a corporate Gross Margin maintaining parity at 56.0% in FY2026 (against 56.3% in FY2025), achieved despite a 35.9% contraction in R&D expenditure from $30.15M (4,510 million JPY, 4.1% of sales) to $19.32M (2,890 million JPY, 2.5% of sales).

Asset efficiency metrics reveal a radical shortening of Days Sales Outstanding (DSO) from 115.6 days ($233.9M in trade receivables) to 53.4 days ($111.4M in receivables). Conversely, Days Inventory Outstanding (DIO) lengthened by 18.3 days, moving from 136.0 days ($120.2M inventory on $322.6M COGS) to 154.3 days ($141.6M inventory on $334.8M COGS). Write-downs of inventory recognized as expense simultaneously dropped 17%, falling from $2.79M (418 million JPY) to $2.31M (346 million JPY). Free Cash Flow (FCF) compressed from $121.1M to $16.6M as Operating Cash Flow of $184.2M funded aggressive fixed-asset allocations.

Infrastructure Layout and Supply Chain Architecture

Dexerials Corporation anchors its production via Dexerials Photonics Solutions Corporation in Japan and Dexerials (Suzhou) Co., Ltd. in mainland China. Distribution and localized engineering are executed through subsidiaries including Dexerials Korea Corporation, Dexerials Marketing Taiwan Corporation, RESTAR DEXERIALS TAIWAN CORPORATION, and RESTAR DEXERIALS HONG KONG LIMITED, supplemented by operating hubs in the USA, Germany, the Netherlands, Singapore, and Shanghai.

The firm captures market share through "Design-in" and "Spec-in" business models, substituting traditional commoditized sales for embedded process engineering at Tier-1 Organic EL (OLED), Integrated Circuit (IC), and Electric Vehicle (EV) assembly lines. Technical milestones for next-generation photonics and AI components are benchmarked at the Optical Fiber Communication Conference (OFC) and the China International Optoelectronic Expo (CIOE). The Dexerials Innovation Group (DIG) manages applied materials engineering, while internal network integrity is maintained by a dedicated Computer Security Incident Response Team (CSIRT). ISO9001 and IATF16949 certifications gatekeep the company's access to global automotive supply chains.

The global headcount stands at 1,802 permanent employees and 495 temporary/contract workers. Over five years, total permanent headcount decreased 5.9% from 1,915 in FY2022, driving a 26.4% gain in revenue per employee (from $334,151 to $422,364).

* Electronic Materials Segment: 551 employees (278 temporary).

* Optical Materials Segment: 427 employees (109 temporary).

* Corporate Functions: 824 employees (108 temporary).

The parent entity commands 1,344 personnel with an average age of 44.0 years, an average tenure of 15.4 years, and an average annual salary of $51,438 (7,693,479 JPY). Executive development is channeled through the Dexerials Business Leadership Program (D-BLP). The ratio of female employees in management progressed from 2.7% (FY2019) to 5.1% (FY2022), reaching 8.6% (FY2025) and 8.8% (FY2026), targeting 10.0% by FY2028.

Environmental disclosures model a 4°C climate warming scenario by 2028 inducing a $17.65M (2.64 billion JPY) operating profit impairment via raw material inflation and a $4.34M (650 million JPY) penalty from carbon taxation. A 2°C transition models an $8.29M (1.24 billion JPY) business opportunity. Scope 3 emissions measure 247.6 thousand t-CO2 (FY2024 data), with purchased goods generating 196.6 thousand t-CO2 (79% of the Scope 3 footprint). The firm targets a 46% reduction in Scope 1 and 2 emissions by 2030. Foreign exchange risks are hyper-leveraged to the USD/JPY pair; every 1-yen appreciation triggers a $2.27M (340 million JPY) top-line decay and a $0.67M (100 million JPY) operating profit loss, reflecting a 29.4% margin flow-through penalty.

HDIN Institutional Verdict

Management's execution of the "Empower Evolution" mid-term business plan demonstrates immediate operational outperformance offset by structural balance sheet friction. The FY2029 operational targets require EBITDA of $300.86M (45 billion JPY), a 19% ROIC, 31% ROE, and an EPS of 263 JPY ($1.76). By FY2026, Dexerials Corporation generated $313.51M (46.89 billion JPY) in EBITDA and a 22.8% ROIC, eclipsing its 2029 yield mandates three years prematurely.

Despite elite asset efficiency, the FY2026 ROE of 27.3% trails the 31% target. A forensic audit of non-current liabilities identifies a 70% expansion in the underfunded net Retirement Benefit Liability, surging from $40.25M (6,020 million JPY) to $68.75M (10,283 million JPY) over 12 months. This hidden drag forces management into an aggressive barbell capital allocation framework. In FY2026, the company deployed $168.7M (25,238 million JPY) in CapEx while simultaneously funding $159.9M in shareholder returns ($69.4M in dividends, $90.5M in buybacks). This matched the FY2025 output of $105.3M (15,745 million JPY) in CapEx against $136.2M in returns ($77.7M dividends, $58.5M buybacks), supporting strict >40% dividend and >60% total return payout ratios to shrink the equity denominator.

Corporate governance operates under a "Company with an Audit and Supervisory Committee" model, enforcing a 30% fixed, 30% short-term bonus, and 40% long-term equity (Performance Share Units and Restricted Stock) executive compensation mix tied directly to TSR, EBITDA, ROE, and CO2 targets. Keiretsu-style cross-shareholding risks are neutralized, isolating just $2.01M (300 million JPY) in unlisted equity and $20,000 (3 million JPY) in other holdings.

PwC Japan identifies goodwill impairment as a Key Audit Matter (KAM). Total intangible assets measure $192.45M (28,785 million JPY). This includes an unamortized goodwill base of $142.33M (21,288 million JPY) representing 7.7% of total consolidated assets. FY2026 impairment tests yielded zero write-downs on goodwill, while PP&E impairments contracted from $2.57M (385 million JPY) to $0.27M (41 million JPY). Remaining finite-life intangibles demand aggressive continuous yield: Technology-Related IP carries a $15.66M (2,343 million JPY) net balance against $5.21M (779 million JPY) in annual amortization, Customer-Related assets hold a $19.68M (2,944 million JPY) balance against $1.20M (180 million JPY) in amortization, and Software/Other intangibles measure $14.75M (2,207 million JPY) against $1.21M (181 million JPY) in amortization.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Electronic Materials Operating Profit margin of 37.5% drove a $256.7M corporate operating profit, outperforming 2029 EBITDA targets by $12.65M amid a $168.7M CapEx outlay.

* Customer concentration reached 43.9% across two OEMs, amplifying FX vulnerability where a 1-Yen/USD swing erodes $2.27M in revenue across Suzhou and Taiwan, China operations.

* A 70% jump in underfunded pension liabilities to $68.75M strains equity targets, forcing $90.5M in FY2026 buybacks to bridge the gap toward a 31% ROE mandate.

Figure Dexerials Strategic & Financial Deep Dive

Segmental Realities and Financial ArchitectureDexerials Corporation [TYO: 4980] executes a dual-engine production model heavily consolidated around Anisotropic Conductive Films (ACF), Anti-Reflection Films (ARF), and Smart View Receptors (SVR). The transition to International Financial Reporting Standards (IFRS) from JGAAP has fundamentally altered balance sheet mechanics, ceasing goodwill amortization in favor of annual impairment testing. Applying a constant exchange rate of 1 USD = 149.5686 JPY, corporate top-line growth masks distinct segmental divergences.

Table Corporate 5-Year Financial Trajectory

| Fiscal Year | Revenue | Operating Profit (OP) | Operating Margin | ROE | ROIC |

|---|---|---|---|---|---|

| FY2022 | $639.9M | $167.3M | 26.1% | 28.5% | 12.2% |

| FY2023 | $709.8M | $201.7M | 28.4% | 30.3% | 7.7% |

| FY2024 | $703.3M | $206.5M | 29.4% | 29.5% | 14.4% |

| FY2025 | $738.1M | $263.1M | 35.7% | 30.6% | 22.1% |

| FY2026 | $761.1M | $256.7M | 33.7% | 27.3% | 22.8% |

FY2025 to FY2026 Segmental Dynamics:

* Optical Materials: Revenue contracted 5.3% to $320.7M (from $338.6M). Operating profit fell 1.6% to $95.7M (from $97.3M), yet operating margins expanded 110 basis points to 29.8%. FY2026 production value equaled $325.7M (99.2% of FY2025) against sales value of $315.3M.

* Electronic Materials: Revenue expanded 10.4% to $446.1M (from $404.1M). Operating profit rose 6.5% to $167.4M (from $157.2M), with margins contracting 140 basis points to 37.5%. FY2026 production value hit $451.9M (113.0% of FY2025) against sales value of $445.7M.

Revenue generation relies on a 43.9% top-two customer concentration. Customer A represents $246.9M (32.5% of total revenue) and Customer B accounts for $86.6M (11.4%). Pricing leverage is verified by a corporate Gross Margin maintaining parity at 56.0% in FY2026 (against 56.3% in FY2025), achieved despite a 35.9% contraction in R&D expenditure from $30.15M (4,510 million JPY, 4.1% of sales) to $19.32M (2,890 million JPY, 2.5% of sales).

Asset efficiency metrics reveal a radical shortening of Days Sales Outstanding (DSO) from 115.6 days ($233.9M in trade receivables) to 53.4 days ($111.4M in receivables). Conversely, Days Inventory Outstanding (DIO) lengthened by 18.3 days, moving from 136.0 days ($120.2M inventory on $322.6M COGS) to 154.3 days ($141.6M inventory on $334.8M COGS). Write-downs of inventory recognized as expense simultaneously dropped 17%, falling from $2.79M (418 million JPY) to $2.31M (346 million JPY). Free Cash Flow (FCF) compressed from $121.1M to $16.6M as Operating Cash Flow of $184.2M funded aggressive fixed-asset allocations.

Infrastructure Layout and Supply Chain Architecture

Dexerials Corporation anchors its production via Dexerials Photonics Solutions Corporation in Japan and Dexerials (Suzhou) Co., Ltd. in mainland China. Distribution and localized engineering are executed through subsidiaries including Dexerials Korea Corporation, Dexerials Marketing Taiwan Corporation, RESTAR DEXERIALS TAIWAN CORPORATION, and RESTAR DEXERIALS HONG KONG LIMITED, supplemented by operating hubs in the USA, Germany, the Netherlands, Singapore, and Shanghai.

The firm captures market share through "Design-in" and "Spec-in" business models, substituting traditional commoditized sales for embedded process engineering at Tier-1 Organic EL (OLED), Integrated Circuit (IC), and Electric Vehicle (EV) assembly lines. Technical milestones for next-generation photonics and AI components are benchmarked at the Optical Fiber Communication Conference (OFC) and the China International Optoelectronic Expo (CIOE). The Dexerials Innovation Group (DIG) manages applied materials engineering, while internal network integrity is maintained by a dedicated Computer Security Incident Response Team (CSIRT). ISO9001 and IATF16949 certifications gatekeep the company's access to global automotive supply chains.

The global headcount stands at 1,802 permanent employees and 495 temporary/contract workers. Over five years, total permanent headcount decreased 5.9% from 1,915 in FY2022, driving a 26.4% gain in revenue per employee (from $334,151 to $422,364).

* Electronic Materials Segment: 551 employees (278 temporary).

* Optical Materials Segment: 427 employees (109 temporary).

* Corporate Functions: 824 employees (108 temporary).

The parent entity commands 1,344 personnel with an average age of 44.0 years, an average tenure of 15.4 years, and an average annual salary of $51,438 (7,693,479 JPY). Executive development is channeled through the Dexerials Business Leadership Program (D-BLP). The ratio of female employees in management progressed from 2.7% (FY2019) to 5.1% (FY2022), reaching 8.6% (FY2025) and 8.8% (FY2026), targeting 10.0% by FY2028.

Environmental disclosures model a 4°C climate warming scenario by 2028 inducing a $17.65M (2.64 billion JPY) operating profit impairment via raw material inflation and a $4.34M (650 million JPY) penalty from carbon taxation. A 2°C transition models an $8.29M (1.24 billion JPY) business opportunity. Scope 3 emissions measure 247.6 thousand t-CO2 (FY2024 data), with purchased goods generating 196.6 thousand t-CO2 (79% of the Scope 3 footprint). The firm targets a 46% reduction in Scope 1 and 2 emissions by 2030. Foreign exchange risks are hyper-leveraged to the USD/JPY pair; every 1-yen appreciation triggers a $2.27M (340 million JPY) top-line decay and a $0.67M (100 million JPY) operating profit loss, reflecting a 29.4% margin flow-through penalty.

HDIN Institutional Verdict

Management's execution of the "Empower Evolution" mid-term business plan demonstrates immediate operational outperformance offset by structural balance sheet friction. The FY2029 operational targets require EBITDA of $300.86M (45 billion JPY), a 19% ROIC, 31% ROE, and an EPS of 263 JPY ($1.76). By FY2026, Dexerials Corporation generated $313.51M (46.89 billion JPY) in EBITDA and a 22.8% ROIC, eclipsing its 2029 yield mandates three years prematurely.

Despite elite asset efficiency, the FY2026 ROE of 27.3% trails the 31% target. A forensic audit of non-current liabilities identifies a 70% expansion in the underfunded net Retirement Benefit Liability, surging from $40.25M (6,020 million JPY) to $68.75M (10,283 million JPY) over 12 months. This hidden drag forces management into an aggressive barbell capital allocation framework. In FY2026, the company deployed $168.7M (25,238 million JPY) in CapEx while simultaneously funding $159.9M in shareholder returns ($69.4M in dividends, $90.5M in buybacks). This matched the FY2025 output of $105.3M (15,745 million JPY) in CapEx against $136.2M in returns ($77.7M dividends, $58.5M buybacks), supporting strict >40% dividend and >60% total return payout ratios to shrink the equity denominator.

Corporate governance operates under a "Company with an Audit and Supervisory Committee" model, enforcing a 30% fixed, 30% short-term bonus, and 40% long-term equity (Performance Share Units and Restricted Stock) executive compensation mix tied directly to TSR, EBITDA, ROE, and CO2 targets. Keiretsu-style cross-shareholding risks are neutralized, isolating just $2.01M (300 million JPY) in unlisted equity and $20,000 (3 million JPY) in other holdings.

PwC Japan identifies goodwill impairment as a Key Audit Matter (KAM). Total intangible assets measure $192.45M (28,785 million JPY). This includes an unamortized goodwill base of $142.33M (21,288 million JPY) representing 7.7% of total consolidated assets. FY2026 impairment tests yielded zero write-downs on goodwill, while PP&E impairments contracted from $2.57M (385 million JPY) to $0.27M (41 million JPY). Remaining finite-life intangibles demand aggressive continuous yield: Technology-Related IP carries a $15.66M (2,343 million JPY) net balance against $5.21M (779 million JPY) in annual amortization, Customer-Related assets hold a $19.68M (2,944 million JPY) balance against $1.20M (180 million JPY) in amortization, and Software/Other intangibles measure $14.75M (2,207 million JPY) against $1.21M (181 million JPY) in amortization.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."