Toray Industries: 2028 ROIC Mandate Accelerates Capital Shift Toward Mobility Chemistry and Aerospace Composites Amid $1.67B Strategic Portfolio Overhaul

Date : 2026-06-30

Reading : 218

HDIN Executive Takeaways

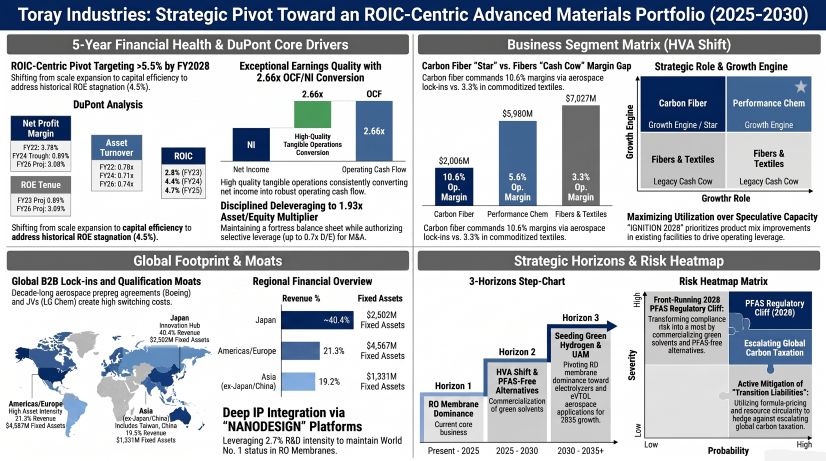

* Margin Bifurcation and ROIC Mandate: Toray's structural transition to the "IGNITION 2028" framework enforces a strict 5.5% ROIC floor, restricting low-yield CapEx to arrest a margin compression cycle that dragged net margins to 3.08% and ROE to 4.5% in FY2026.

* Geographic Asset Dislocation: While 40.4% of FY2026 revenue is generated in Japan, 70% of the firm's non-current assets are deployed globally, heavily concentrated in $4.56 billion worth of specialized localized infrastructure across the Americas and Europe.

* Regulatory Hedging via Innovation: Sustainability Innovation (SI) revenue expanded to $9.27 billion, representing 53.6% of consolidated sales, establishing a commercial moat against looming 2028 global PFAS restrictions and European carbon border tariffs.

Figure Toray Industries: Strategic Pivot Toward an ROlC-Centric Advanced Materials Portfolio (2025-2030)

Segmental Realities and Capital Structure Dynamics

Segmental Realities and Capital Structure Dynamics

Toray Industries operates a bifurcated portfolio, leveraging a high-volume, low-margin legacy cash cow to fund capital-intensive advanced materials. All internal modeling is pegged to a mandated 2025 average exchange rate of 1 USD = 149.5686 JPY. During the "AP-G 2025" execution cycle, management delivered FY2025 revenue of ¥2,585.1 billion ($17.28 billion) against a target of ¥2,800.0 billion ($18.72 billion), while Core Operating Income registered at ¥141.9 billion ($948.7 million) against a ¥180.0 billion ($1.20 billion) target, hampered by delayed semiconductor demand and unmitigated raw material inflation.

The portfolio deconstruction for FY2025 and FY2026 isolates the operating leverage across divisions:

DuPont analysis indicates severe historical profitability friction. Return on Equity (ROE) degraded from 6.4% in 2022 to a trough of 1.3% in 2024, stabilizing at 4.5% in both 2025 and 2026. Net margins fell from 3.78% (2022) to 0.89% (2024), recovering to 3.08% in 2026 (generating $531.7 million in Net Income on $17.28 billion in Revenue). Asset turnover remained constrained within a 0.71x to 0.78x bandwidth, resting at 0.74x in 2026. Historical Return on Invested Capital (ROIC) tracked at 2.8% (2023), 4.4% (2024), and 4.7% (2025).

Despite constrained GAAP profitability, earnings quality is exceptional. Net Income to Operating Cash Flow (OCF) conversion multiples hit 1.64x in 2022 ($0.92 billion OCF / $0.56 billion NI), an anomalous 8.48x in 2024 ($1.24 billion / $0.15 billion), and normalized to 2.66x in 2026 ($1.42 billion / $0.53 billion). Free Cash Flow (FCF) peaked at $1.28 billion in 2025 and printed at $0.97 billion in 2026. Consolidated CapEx reached ¥255.0 billion ($1.70 billion) in FY2025, adjusting to ¥211.8 billion ($1.42 billion) in FY2026. Segment-specific allocations for 2026 totaled $1.25 billion: Textiles consumed $506.8 million (40.5%), Performance Chemicals $431.7 million (34.5%), Environment & Engineering $173.8 million (13.9%), and Carbon Fiber Composite Materials absorbed just $45.2 million (3.6%).

The balance sheet maintains absolute short-term solvency with a 1.78x current ratio (Current Assets: $10.22 billion; Current Liabilities: $5.74 billion). Total interest-bearing debt rests at $5.78 billion, split 44% short-term ($2.55 billion) and 56% long-term ($3.23 billion). Financial leverage (Assets/Equity) systematically dropped from 2.17x in 2022 to 1.93x in 2026. The Debt-to-Equity (D/E) ratio is strictly anchored between 0.49x and 0.50x, though the "IGNITION 2028" strategy authorizes maximum leverage of 0.70x for tactical M&A. Working capital efficiency dictates a Cash Conversion Cycle (CCC) of 130 days based on 2026 metrics: Days Sales Outstanding (DSO) of 90.7 days (AR: $4.30 billion), Days Inventory Outstanding (DIO) stretched from 92.3 to 95.2 days (Inventory: $3.60 billion), and Days Payable Outstanding (DPO) of 56.1 days (AP: $2.12 billion).

Dividends per share grew systematically from ¥16.00 ($0.11) in FY2022 to ¥18.00 ($0.12) spanning FY2023–FY2025, culminating at ¥20.00 ($0.13) in FY2026. Executive compensation utilizes long-term stock acquisition rights covering the 3rd through 14th series, maturing up to 2054, enforcing alignment with the "IGNITION 2028" targets of ¥3,000.0 billion ($20.06 billion) in Revenue, ¥230.0 billion ($1.54 billion) in Core Operating Income, and a >5.5% ROIC.

Infrastructure Layout and Regional Manufacturing Moats

Toray's fixed asset deployment intentionally mismatches its revenue origination to construct localized B2B moats. FY2026 revenue distributions report Japan at $6,987 million (40.4%), China at $3,297 million (19.1%), Asia ex-Japan/China (strictly incorporating Taiwan, China) at $3,327 million (19.2%), and Others at $3,673 million (21.3%). Conversely, FY2026 non-current asset allocation registers Japan at $2,502 million, the Americas at $2,443 million, Europe/Others at $2,124 million, Asia ex-Japan/China at $1,331 million, and China at $1,309 million.

The R&D nexus is centralized at the Toray Research Center in Japan, operating on an FY2026 budget of $469.8 million (¥70.26 billion) for an intensity of 2.72%. This funds proprietary "NANODESIGN" (nano-level polymer structural control), "DEWEIGHT" xEV lightweighting applications, and next-generation Reverse Osmosis (RO) membranes where Toray holds the #1 global market position.

Manufacturing hubs function as specialized chokepoints. In the Americas, Toray Composite Materials America, Inc. (TCMA) localizes mission-critical carbon fiber prepreg production for Boeing Co., secured by supply agreements extending through 2028/2031 for the 787 and 777X airframes. Zoltek Companies, Inc. and Zoltek de Mexico manufacture large-tow carbon fiber for industrial wind turbines, while Toray Plastics (America) dominates advanced film production.

In Europe, Alcantara S.p.A. (Italy) captures luxury automotive interior margins, and Toray Carbon Fibers Europe S.A. (France) serves Airbus and regional industrials. EV battery ecosystem integration is locked via the LG Toray Hungary Battery Separator Kft. joint venture with LG Chem. Asian infrastructure prioritizes electronics and volume scaling: Toray Advanced Materials Korea Inc. drives PPS resins and separators, heavily reliant on partnerships with Samyang Corporation, Dow Silicones Corp., and Freudenberg SE. Facilities like Toray Polytech (Nantong) in China and Toray Textiles in Indonesia mass-produce commoditized lines.

Global trade architecture exposes the firm to rigorous U.S. EAR and Japanese METI dual-use technology export controls on carbon fibers. Supply chains rely heavily on upstream crude oil, naphtha, and acrylonitrile, managed defensively via formula pricing, USD/EUR/RMB/KRW foreign exchange forward contracts, and interest rate swaps guarding against TIBOR fluctuations.

Off-Balance Sheet Obligations and Sustainability Monetization

Toray possesses a $1.67 billion (¥250.37 billion) investment securities portfolio generating $355.2 million (¥53.13 billion) in FY2026 IFRS fair value gains. This portfolio hedges supply chains via cross-shareholdings in MS&AD Insurance Group, Shinkong Synthetic Fibers Corp., TSI Holdings, Bolt Biotherapeutics, and Bluejay Diagnostics. Further un-consolidated manufacturing scale is guaranteed via a 29.2% equity method stake in Pacific Textiles Holdings Limited and 33.0% in TMT Machinery.

Mid-term cash flow is encumbered by $1.09 billion in obscured obligations. As of FY2026, the net defined-benefit retirement liability sits at $507.0 million (¥75.84 billion), reduced marginally from $536.6 million (¥80.25 billion) in FY2025. IFRS 16 capitalized lease liabilities total $456.4 million, partitioned into $78.4 million (¥11.73 billion) current and $378.0 million (¥56.53 billion) non-current obligations. Off-balance-sheet capital commitments for PP&E claim an additional $125.8 million (¥18.82 billion). Environmental compliance provisions rose from $5.15 million (¥771 million) to $17.35 million (¥2,595 million) in FY2026, alongside $58.29 million (¥8,718 million) in absolute Asset Retirement Obligations (AROs).

Management successfully monetized its ESG transition. Sustainability Innovation (SI) revenue expanded from a FY2013 baseline of $3.76 billion (¥562.4 billion) to $9.27 billion (¥1,386.5 billion) in FY2025, constituting 53.6% of consolidated sales. Environmental efficiency metrics versus the 2013 baseline achieved a 45% reduction in absolute GHG emissions (surpassing the 40% target), a 31% reduction in water usage (surpassing the 20% target), and a 37% waste reduction (missing the 40% target). Downstream avoided emissions reached 1.22 billion tons (12.2 億トン), trailing the 1.50 billion ton target. By 2035, Toray mandates a 35% absolute GHG reduction and a 70% reduction per unit of revenue. Under 1.5°C, 2.0°C, and 4.0°C TCFD scenarios, the firm prioritizes its "Resource Circulation Project" (CE) to combat carbon taxes (e.g., EU CBAM) and expedites NMP (N-Methyl-2-pyrrolidone) solutions and PFAS-free chemistry ahead of anticipated 2028 regulatory bans and RoHS mandates. Enterprise risk is triangulated across the Risk Management Committee, Overseas Crisis Management Committee, and Security Trade Control Committee.

HDIN Institutional Verdict

Toray Industries operates a classic materials-science hourglass model, securing monopolistic pricing power by bottlenecking highly commoditized petrochemicals into irreplaceable downstream EV and aerospace components. However, the capital intensity required to maintain this moat actively punishes equity returns. Management's "TORAY Challenges 2035" objective of generating a 10% ROIC is mathematically improbable against a structural $15.5 billion+ global fixed-asset footprint, especially given the company's historical inability to push ROIC past 4.7% during peak CapEx cycles.

Conversely, the near-term "IGNITION 2028" strategy is fundamentally grounded. Imposing a 5.5% ROIC floor and reallocating only $45.2 million (3.6%) of 2026 CapEx to Carbon Fibers signals that management is finally forcing OEMs to absorb the costs of capacity utilization before authorizing new expansion. Toray’s intrinsic value remains disconnected from its balance sheet, hidden entirely in multi-decade Boeing airframe lock-ins, LG Chem JV agreements, and the impending 2028 PFAS transition, positioning the firm to cannibalize market share from slower competitors (Hexcel, Solvay, Teijin) while remaining safely insulated from Asian commodity overcapacity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Margin Bifurcation and ROIC Mandate: Toray's structural transition to the "IGNITION 2028" framework enforces a strict 5.5% ROIC floor, restricting low-yield CapEx to arrest a margin compression cycle that dragged net margins to 3.08% and ROE to 4.5% in FY2026.

* Geographic Asset Dislocation: While 40.4% of FY2026 revenue is generated in Japan, 70% of the firm's non-current assets are deployed globally, heavily concentrated in $4.56 billion worth of specialized localized infrastructure across the Americas and Europe.

* Regulatory Hedging via Innovation: Sustainability Innovation (SI) revenue expanded to $9.27 billion, representing 53.6% of consolidated sales, establishing a commercial moat against looming 2028 global PFAS restrictions and European carbon border tariffs.

Figure Toray Industries: Strategic Pivot Toward an ROlC-Centric Advanced Materials Portfolio (2025-2030)

Segmental Realities and Capital Structure DynamicsToray Industries operates a bifurcated portfolio, leveraging a high-volume, low-margin legacy cash cow to fund capital-intensive advanced materials. All internal modeling is pegged to a mandated 2025 average exchange rate of 1 USD = 149.5686 JPY. During the "AP-G 2025" execution cycle, management delivered FY2025 revenue of ¥2,585.1 billion ($17.28 billion) against a target of ¥2,800.0 billion ($18.72 billion), while Core Operating Income registered at ¥141.9 billion ($948.7 million) against a ¥180.0 billion ($1.20 billion) target, hampered by delayed semiconductor demand and unmitigated raw material inflation.

The portfolio deconstruction for FY2025 and FY2026 isolates the operating leverage across divisions:

| Business Segment | FY2025 Revenue | FY2026 Revenue | FY2025 Operating Profit | FY2026 Operating Profit | FY2026 Operating Margin | Strategic Classification |

|---|---|---|---|---|---|---|

| Fibers & Textiles | $6,760M | $7,027M | $230M | $231M | 3.3% | Cash Cow |

| Performance Chemicals | $6,317M | $5,980M | $325M | $336M | 5.6% | Growth Engine |

| Carbon Fiber Composites | $2,006M | $2,006M | $213M | $213M | 10.6% | Growth Engine / Star |

| Environment & Engineering | $1,581M | $1,784M | $54M | $59M | 3.3% | Strategic Hold |

| Life Science | $355M | $350M | $24M | $21M | 6.0% | Venture / Niche |

| Others / Adjustments | $135M | $135M | N/A | N/A | N/A | N/A |

| Consolidated Total | $17,143M | $17,284M | $965M | $795M (Core) | 4.6% | — |

DuPont analysis indicates severe historical profitability friction. Return on Equity (ROE) degraded from 6.4% in 2022 to a trough of 1.3% in 2024, stabilizing at 4.5% in both 2025 and 2026. Net margins fell from 3.78% (2022) to 0.89% (2024), recovering to 3.08% in 2026 (generating $531.7 million in Net Income on $17.28 billion in Revenue). Asset turnover remained constrained within a 0.71x to 0.78x bandwidth, resting at 0.74x in 2026. Historical Return on Invested Capital (ROIC) tracked at 2.8% (2023), 4.4% (2024), and 4.7% (2025).

Despite constrained GAAP profitability, earnings quality is exceptional. Net Income to Operating Cash Flow (OCF) conversion multiples hit 1.64x in 2022 ($0.92 billion OCF / $0.56 billion NI), an anomalous 8.48x in 2024 ($1.24 billion / $0.15 billion), and normalized to 2.66x in 2026 ($1.42 billion / $0.53 billion). Free Cash Flow (FCF) peaked at $1.28 billion in 2025 and printed at $0.97 billion in 2026. Consolidated CapEx reached ¥255.0 billion ($1.70 billion) in FY2025, adjusting to ¥211.8 billion ($1.42 billion) in FY2026. Segment-specific allocations for 2026 totaled $1.25 billion: Textiles consumed $506.8 million (40.5%), Performance Chemicals $431.7 million (34.5%), Environment & Engineering $173.8 million (13.9%), and Carbon Fiber Composite Materials absorbed just $45.2 million (3.6%).

The balance sheet maintains absolute short-term solvency with a 1.78x current ratio (Current Assets: $10.22 billion; Current Liabilities: $5.74 billion). Total interest-bearing debt rests at $5.78 billion, split 44% short-term ($2.55 billion) and 56% long-term ($3.23 billion). Financial leverage (Assets/Equity) systematically dropped from 2.17x in 2022 to 1.93x in 2026. The Debt-to-Equity (D/E) ratio is strictly anchored between 0.49x and 0.50x, though the "IGNITION 2028" strategy authorizes maximum leverage of 0.70x for tactical M&A. Working capital efficiency dictates a Cash Conversion Cycle (CCC) of 130 days based on 2026 metrics: Days Sales Outstanding (DSO) of 90.7 days (AR: $4.30 billion), Days Inventory Outstanding (DIO) stretched from 92.3 to 95.2 days (Inventory: $3.60 billion), and Days Payable Outstanding (DPO) of 56.1 days (AP: $2.12 billion).

Dividends per share grew systematically from ¥16.00 ($0.11) in FY2022 to ¥18.00 ($0.12) spanning FY2023–FY2025, culminating at ¥20.00 ($0.13) in FY2026. Executive compensation utilizes long-term stock acquisition rights covering the 3rd through 14th series, maturing up to 2054, enforcing alignment with the "IGNITION 2028" targets of ¥3,000.0 billion ($20.06 billion) in Revenue, ¥230.0 billion ($1.54 billion) in Core Operating Income, and a >5.5% ROIC.

Infrastructure Layout and Regional Manufacturing Moats

Toray's fixed asset deployment intentionally mismatches its revenue origination to construct localized B2B moats. FY2026 revenue distributions report Japan at $6,987 million (40.4%), China at $3,297 million (19.1%), Asia ex-Japan/China (strictly incorporating Taiwan, China) at $3,327 million (19.2%), and Others at $3,673 million (21.3%). Conversely, FY2026 non-current asset allocation registers Japan at $2,502 million, the Americas at $2,443 million, Europe/Others at $2,124 million, Asia ex-Japan/China at $1,331 million, and China at $1,309 million.

The R&D nexus is centralized at the Toray Research Center in Japan, operating on an FY2026 budget of $469.8 million (¥70.26 billion) for an intensity of 2.72%. This funds proprietary "NANODESIGN" (nano-level polymer structural control), "DEWEIGHT" xEV lightweighting applications, and next-generation Reverse Osmosis (RO) membranes where Toray holds the #1 global market position.

Manufacturing hubs function as specialized chokepoints. In the Americas, Toray Composite Materials America, Inc. (TCMA) localizes mission-critical carbon fiber prepreg production for Boeing Co., secured by supply agreements extending through 2028/2031 for the 787 and 777X airframes. Zoltek Companies, Inc. and Zoltek de Mexico manufacture large-tow carbon fiber for industrial wind turbines, while Toray Plastics (America) dominates advanced film production.

In Europe, Alcantara S.p.A. (Italy) captures luxury automotive interior margins, and Toray Carbon Fibers Europe S.A. (France) serves Airbus and regional industrials. EV battery ecosystem integration is locked via the LG Toray Hungary Battery Separator Kft. joint venture with LG Chem. Asian infrastructure prioritizes electronics and volume scaling: Toray Advanced Materials Korea Inc. drives PPS resins and separators, heavily reliant on partnerships with Samyang Corporation, Dow Silicones Corp., and Freudenberg SE. Facilities like Toray Polytech (Nantong) in China and Toray Textiles in Indonesia mass-produce commoditized lines.

Global trade architecture exposes the firm to rigorous U.S. EAR and Japanese METI dual-use technology export controls on carbon fibers. Supply chains rely heavily on upstream crude oil, naphtha, and acrylonitrile, managed defensively via formula pricing, USD/EUR/RMB/KRW foreign exchange forward contracts, and interest rate swaps guarding against TIBOR fluctuations.

Off-Balance Sheet Obligations and Sustainability Monetization

Toray possesses a $1.67 billion (¥250.37 billion) investment securities portfolio generating $355.2 million (¥53.13 billion) in FY2026 IFRS fair value gains. This portfolio hedges supply chains via cross-shareholdings in MS&AD Insurance Group, Shinkong Synthetic Fibers Corp., TSI Holdings, Bolt Biotherapeutics, and Bluejay Diagnostics. Further un-consolidated manufacturing scale is guaranteed via a 29.2% equity method stake in Pacific Textiles Holdings Limited and 33.0% in TMT Machinery.

Mid-term cash flow is encumbered by $1.09 billion in obscured obligations. As of FY2026, the net defined-benefit retirement liability sits at $507.0 million (¥75.84 billion), reduced marginally from $536.6 million (¥80.25 billion) in FY2025. IFRS 16 capitalized lease liabilities total $456.4 million, partitioned into $78.4 million (¥11.73 billion) current and $378.0 million (¥56.53 billion) non-current obligations. Off-balance-sheet capital commitments for PP&E claim an additional $125.8 million (¥18.82 billion). Environmental compliance provisions rose from $5.15 million (¥771 million) to $17.35 million (¥2,595 million) in FY2026, alongside $58.29 million (¥8,718 million) in absolute Asset Retirement Obligations (AROs).

Management successfully monetized its ESG transition. Sustainability Innovation (SI) revenue expanded from a FY2013 baseline of $3.76 billion (¥562.4 billion) to $9.27 billion (¥1,386.5 billion) in FY2025, constituting 53.6% of consolidated sales. Environmental efficiency metrics versus the 2013 baseline achieved a 45% reduction in absolute GHG emissions (surpassing the 40% target), a 31% reduction in water usage (surpassing the 20% target), and a 37% waste reduction (missing the 40% target). Downstream avoided emissions reached 1.22 billion tons (12.2 億トン), trailing the 1.50 billion ton target. By 2035, Toray mandates a 35% absolute GHG reduction and a 70% reduction per unit of revenue. Under 1.5°C, 2.0°C, and 4.0°C TCFD scenarios, the firm prioritizes its "Resource Circulation Project" (CE) to combat carbon taxes (e.g., EU CBAM) and expedites NMP (N-Methyl-2-pyrrolidone) solutions and PFAS-free chemistry ahead of anticipated 2028 regulatory bans and RoHS mandates. Enterprise risk is triangulated across the Risk Management Committee, Overseas Crisis Management Committee, and Security Trade Control Committee.

HDIN Institutional Verdict

Toray Industries operates a classic materials-science hourglass model, securing monopolistic pricing power by bottlenecking highly commoditized petrochemicals into irreplaceable downstream EV and aerospace components. However, the capital intensity required to maintain this moat actively punishes equity returns. Management's "TORAY Challenges 2035" objective of generating a 10% ROIC is mathematically improbable against a structural $15.5 billion+ global fixed-asset footprint, especially given the company's historical inability to push ROIC past 4.7% during peak CapEx cycles.

Conversely, the near-term "IGNITION 2028" strategy is fundamentally grounded. Imposing a 5.5% ROIC floor and reallocating only $45.2 million (3.6%) of 2026 CapEx to Carbon Fibers signals that management is finally forcing OEMs to absorb the costs of capacity utilization before authorizing new expansion. Toray’s intrinsic value remains disconnected from its balance sheet, hidden entirely in multi-decade Boeing airframe lock-ins, LG Chem JV agreements, and the impending 2028 PFAS transition, positioning the firm to cannibalize market share from slower competitors (Hexcel, Solvay, Teijin) while remaining safely insulated from Asian commodity overcapacity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."