Daikin Industries: 28.4% CapEx Rotation into Chemicals Amid Global Margin Divergence as 9.1% ROE Signals Capital Dilution

Date : 2026-07-03

Reading : 91

HDIN Executive Takeaways

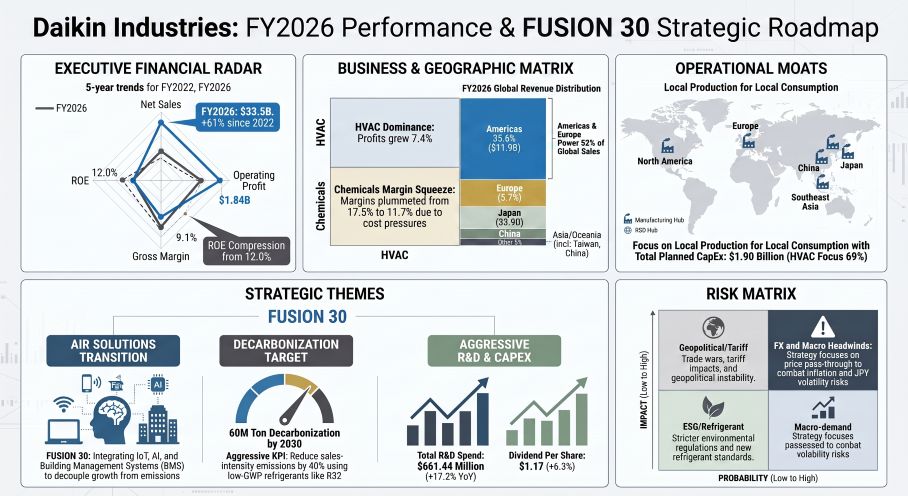

* Daikin Industries [OTC: DKILY] posted FY2026 consolidated sales of $33.53 billion (+5.5% YoY), driven by 9.2% expansion in the Americas and strategic price enforcement on "VRV 7" and R32 HVAC systems, lifting core hardware operating margins to 8.16%.

* Management authorized a $1.90 billion global capital expenditure program, disproportionately allocating $541.56 million (28.4%) to the chemicals segment, despite its operating profit plunging 28.3% amid acute supply chain margin compression.

* Asset efficiency structurally deteriorated, with ROE sliding 160 basis points to 9.1% from FY2024 levels, and ROA dropping to 4.74%; however, a $960.15 million free cash flow generation secures liquidity for "FUSION 30" decarbonization mandates.

Figure Daikin Industries: FY2026 Performance & FUSlON 30 Strategic Roadmap

Consolidated Financial Trajectory and Profitability Dilution

Consolidated Financial Trajectory and Profitability Dilution

Daikin Industries experienced divergent structural returns during the FY2022–FY2026 reporting period. While total assets expanded to $58.09 billion, marginal capital efficiency deteriorated. The consolidated balance sheet illustrates a deleveraging trend, with the debt ratio compressing from 47.50% in FY2022 to 42.91% in FY2026, and the equity ratio fortifying from 51.5% in FY2025 to 55.9% in FY2026. A favorable JPY exchange rate (1 USD = 149.5686 JPY) provided a conversion tailwind to top-line metrics.

Table Core Financial Evolution (FY2022 - FY2026)

Segmental Realities and Supply Chain Architecture

The total corporate framework operates via 324 consolidated subsidiaries (31 domestic in Japan, 293 overseas) and 16 equity-method affiliates. Segmental analysis exposes a severe profitability divergence. The core Air Conditioning & Refrigeration (HVAC) segment absorbed inflation through "Cost Down" measures and strategic pricing of premium product lines, including "FIVE STAR ZEAS" and "VRV7 machi." Conversely, the Chemicals division reported a 28.3% collapse in operating profit, dragging segment margins down to 11.76% from 17.53% in FY2025.

FY2026 Micro-Operational and Segment Analysis

* Air Conditioning & Refrigeration (HVAC)

* *Revenue Structure:* Sales reached $30,896.39 million (4,621,131 million JPY), commanding 92.1% of global revenue with a 5.4% YoY growth. Production value registered $21.28 billion (3,182,249 million JPY), increasing 5.3% YoY.

* *Profitability:* Operating profit hit $2,520.52 million (+7.4% YoY), driving margin expansion from 8.01% (FY25) to 8.16% (FY26).

* *Human & Physical Capital:* Employs 96,697 personnel supported by 11,658 temporary workers. CapEx allocation was $1.32 billion (198,000 million JPY), representing 69.4% of total planned CapEx.

* *Subsidiary Network:* Daikin Comfort Technologies North America, Inc., Daikin Applied Americas, Inc., American Air Filter Company, Inc. (AAF), Daikin Europe N.V., Daikin Applied Europe S.p.A., AHT Cooling Systems GmbH, Daikin (China) Investment Co., Ltd., Daikin Air-conditioning (Shanghai) Co., Ltd., Daikin Machinery and Electronics (Suzhou) Co., Ltd., Daikin HVAC Solution Tokyo, Daikin Applied Systems, and Daikin Airconditioning India Private Limited.

* Chemicals

* *Revenue Structure:* Sales generated $1,881.87 million (281,469 million JPY), accounting for 5.6% of revenue with 7.0% YoY growth. Production value flatlined at $1.72 billion (257,069 million JPY), returning 0.7% YoY growth.

* *Profitability:* Operating profit plummeted to $221.23 million (-28.3% YoY).

* *Human & Physical Capital:* Employs 4,341 personnel with 387 temporary workers. Absorbed a disproportionate CapEx allocation of $541.56 million (81,000 million JPY), equating to 28.4% of the corporate total.

* *Subsidiary Network:* Daikin Fluorochemicals (China) Co., Ltd., Daikin America, Inc., and Daikin Chemical Europe GmbH.

* Others & Corporate Administration

* *Others Segment:* Sales of $751.73 million (2.3% of total, +7.3% YoY); Operating profit of $32.93 million (+8.4% YoY) with margins at 4.38% (vs 4.33% in FY25); CapEx at $40.11 million (6,000 million JPY); Headcount of 1,930 personnel.

* *Corporate Metrics:* Total consolidated operating profit reached $2,774.59 million (+3.3% YoY) with an aggregate margin of 8.27% (down from 8.45% in FY25). Total headcount stood at 104,095, including 12,345 temporary/contract workers (10.6% of workforce). Corporate administration headcount totaled 1,127. Total CapEx forward planning is set at $1.90 billion (285,000 million JPY).

Geographic Footprint and Regional Moats

Daikin’s top-line growth is entirely dependent on established Western markets, offsetting observable weakness in the Asia-Pacific basin.

* The Americas: Reached $11,944.44 million (+9.2% YoY), securing a 35.6% global revenue proportion.

* Europe: Recorded $5,735.13 million (+10.0% YoY), constituting 17.1% of global sales.

* Japan (Domestic): Generated $5,413.14 million (+3.1% YoY), representing 16.1% of global operations.

* China (Including Taiwan, China): Contracted to $4,755.19 million (-1.7% YoY), capturing 14.2% of global volume.

* Asia / Oceania: Contracted to $3,155.19 million (-4.5% YoY), holding a 9.4% geographic share.

* Others: Expanded to $2,526.89 million (+13.3% YoY), taking 7.5% of total sales.

Free Cash Flow Yield, Asset Quality, and Capital Allocation

Despite escalating fixed costs, Daikin's core liquidity remains intact, enabling progressive shareholder returns and R&D acceleration.

* R&D Capital Expansion: Pure R&D expenditure expanded 17.2% YoY, rising from $564.25 million (84,394 million JPY) in FY2025 to $661.44 million (98,931 million JPY) in FY2026.

* Dividend Flow: Management increased the dividend per share from $1.10 (165 JPY) in FY2025 to $1.17 (175 JPY) in FY2026. Total capital outflow for dividends scaled from $323.04 million (48,317 million JPY) to $342.64 million (51,248 million JPY).

* Asset Impairment & Credit Risk: A specific $79.22 million (11,849 million JPY) fixed asset impairment loss was recognized and directly linked to AHT Cooling Systems GmbH in Europe. Bad debt provisions marginally increased from $149.7 million (22,395 million JPY) in FY2025 to $157.2 million (23,519 million JPY) in FY2026. Against a total receivables and contract asset baseline of $6.76 billion (1,011,104 million JPY), the bad debt ratio remains stabilized at 2.33%.

* Off-Balance Sheet Items & Pensions: Guarantee reservations increased to $109.8 million (16,424 million JPY) from $66.7 million (9,973 million JPY) in FY2025. The defined benefit obligations display no funding deficit; funded plan assets at fair value stand at $573.2 million (85,734 million JPY), entirely eclipsing the $379.2 million (56,724 million JPY) obligation. Unfunded pure liabilities are recognized at $246.6 million (36,878 million JPY).

Governance Integration and Decarbonization Architecture

Daikin evaluates top management through a strict "Skill Matrix" heavily indexing ESG and sustainability. Compensation structures are strictly performance-linked, utilizing Performance Share Units (PSU, 70% weight) and Restricted Stock Units (RSU, 30% weight). PSU payouts iterate from 0% to 200%, calculated via D-ROIC (Daikin Return on Invested Capital) targets and Relative Total Shareholder Return (TSR) against the TOPIX index. Execution readiness is monitored through "People-Centered Management (PCM) Behaviors," which tracked a 61% practical implementation rate in FY2025.

To satisfy the "Environment Vision 2050" and "FUSION 30" mandates, the executive board enforces scientifically validated (SBTi) greenhouse gas parameters:

* Carbon Intensity Reduction: Management locked a 40% reduction target in GHG emissions per unit of sales, decreasing from 0.08 kg-CO2/JPY in FY2022 to 0.05 kg-CO2/JPY by FY2030.

* Total Emission Reductions: Daikin dictates an expansion in its global emissions reduction contribution from 17.6 million tons of CO2 in FY2022 to 60 million tons by FY2030.

* Supply Chain Baselines: Scope 1 and Scope 2 emissions must drop 46.2% by 2030 (vs. 2019 baseline) leading to net zero by 2050, while Scope 3 upstream/downstream emissions carry a 55% reduction mandate by 2030.

* Solution Business Transition: To insulate against hardware cyclicality, Daikin integrates IoT and AI into Building Management Systems (BMS). Urban energy monetization is being tested through Virtual Power Plant (VPP) architecture and participation in the Toyota Woven City and Shizen Connect energy grid networks.

HDIN Institutional Verdict

An objective audit of the FY2026 data confirms Daikin is successfully executing aggressive cost pass-throughs in its HVAC division across the Americas and Europe, effectively weaponizing the weak Japanese Yen to shield operating profit against global inflation. However, the capital allocation ratio into the Chemicals segment (absorbing 28.4% of total CapEx despite generating only 5.6% of sales and suffering a 28.3% profit contraction) presents immediate D-ROIC drag risks. Furthermore, while rumor-driven market narratives point toward data center cooling acquisitions and structural exclusions involving Goodman, the FY2026 corporate filings provide zero financial confirmation of these specific consolidation shifts. Daikin’s structural ROE compression (12.3% to 9.1% over three years) proves that top-line revenue expansion is currently outpacing marginal capital efficiency, heavily relying on the success of its VPP and R32 solutions to restore unit economics in the 2030 cycle.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Daikin Industries [OTC: DKILY] posted FY2026 consolidated sales of $33.53 billion (+5.5% YoY), driven by 9.2% expansion in the Americas and strategic price enforcement on "VRV 7" and R32 HVAC systems, lifting core hardware operating margins to 8.16%.

* Management authorized a $1.90 billion global capital expenditure program, disproportionately allocating $541.56 million (28.4%) to the chemicals segment, despite its operating profit plunging 28.3% amid acute supply chain margin compression.

* Asset efficiency structurally deteriorated, with ROE sliding 160 basis points to 9.1% from FY2024 levels, and ROA dropping to 4.74%; however, a $960.15 million free cash flow generation secures liquidity for "FUSION 30" decarbonization mandates.

Figure Daikin Industries: FY2026 Performance & FUSlON 30 Strategic Roadmap

Consolidated Financial Trajectory and Profitability DilutionDaikin Industries experienced divergent structural returns during the FY2022–FY2026 reporting period. While total assets expanded to $58.09 billion, marginal capital efficiency deteriorated. The consolidated balance sheet illustrates a deleveraging trend, with the debt ratio compressing from 47.50% in FY2022 to 42.91% in FY2026, and the equity ratio fortifying from 51.5% in FY2025 to 55.9% in FY2026. A favorable JPY exchange rate (1 USD = 149.5686 JPY) provided a conversion tailwind to top-line metrics.

Table Core Financial Evolution (FY2022 - FY2026)

| Fiscal Year | Net Sales ($M) | Ordinary Profit ($M) | Net Profit ($M) | Gross Margin | ROE | ROA | Free Cash Flow ($M) | Debt Ratio |

|---|---|---|---|---|---|---|---|---|

| 2022 | 20,787.16 | 2,189.60 | 1,455.58 | N/A | 12.0% | 5.69% | 429.78 | 47.50% |

| 2023 | 26,620.41 | 2,448.68 | 1,723.32 | N/A | 12.3% | 5.99% | -474.01 | 47.04% |

| 2024 | 29,386.63 | 2,370.10 | 1,740.41 | N/A | 10.7% | 5.33% | 1,152.51 | 44.93% |

| 2025 | 31,773.61 | 2,450.02 | 1,770.14 | 34.23% | 9.7% | 5.16% | 1,183.70 | 44.16% |

| 2026 | 33,530.01 | 2,728.99 | 1,840.15 | 34.55% | 9.1% | 4.74% | 960.15 | 42.91% |

Segmental Realities and Supply Chain Architecture

The total corporate framework operates via 324 consolidated subsidiaries (31 domestic in Japan, 293 overseas) and 16 equity-method affiliates. Segmental analysis exposes a severe profitability divergence. The core Air Conditioning & Refrigeration (HVAC) segment absorbed inflation through "Cost Down" measures and strategic pricing of premium product lines, including "FIVE STAR ZEAS" and "VRV7 machi." Conversely, the Chemicals division reported a 28.3% collapse in operating profit, dragging segment margins down to 11.76% from 17.53% in FY2025.

FY2026 Micro-Operational and Segment Analysis

* Air Conditioning & Refrigeration (HVAC)

* *Revenue Structure:* Sales reached $30,896.39 million (4,621,131 million JPY), commanding 92.1% of global revenue with a 5.4% YoY growth. Production value registered $21.28 billion (3,182,249 million JPY), increasing 5.3% YoY.

* *Profitability:* Operating profit hit $2,520.52 million (+7.4% YoY), driving margin expansion from 8.01% (FY25) to 8.16% (FY26).

* *Human & Physical Capital:* Employs 96,697 personnel supported by 11,658 temporary workers. CapEx allocation was $1.32 billion (198,000 million JPY), representing 69.4% of total planned CapEx.

* *Subsidiary Network:* Daikin Comfort Technologies North America, Inc., Daikin Applied Americas, Inc., American Air Filter Company, Inc. (AAF), Daikin Europe N.V., Daikin Applied Europe S.p.A., AHT Cooling Systems GmbH, Daikin (China) Investment Co., Ltd., Daikin Air-conditioning (Shanghai) Co., Ltd., Daikin Machinery and Electronics (Suzhou) Co., Ltd., Daikin HVAC Solution Tokyo, Daikin Applied Systems, and Daikin Airconditioning India Private Limited.

* Chemicals

* *Revenue Structure:* Sales generated $1,881.87 million (281,469 million JPY), accounting for 5.6% of revenue with 7.0% YoY growth. Production value flatlined at $1.72 billion (257,069 million JPY), returning 0.7% YoY growth.

* *Profitability:* Operating profit plummeted to $221.23 million (-28.3% YoY).

* *Human & Physical Capital:* Employs 4,341 personnel with 387 temporary workers. Absorbed a disproportionate CapEx allocation of $541.56 million (81,000 million JPY), equating to 28.4% of the corporate total.

* *Subsidiary Network:* Daikin Fluorochemicals (China) Co., Ltd., Daikin America, Inc., and Daikin Chemical Europe GmbH.

* Others & Corporate Administration

* *Others Segment:* Sales of $751.73 million (2.3% of total, +7.3% YoY); Operating profit of $32.93 million (+8.4% YoY) with margins at 4.38% (vs 4.33% in FY25); CapEx at $40.11 million (6,000 million JPY); Headcount of 1,930 personnel.

* *Corporate Metrics:* Total consolidated operating profit reached $2,774.59 million (+3.3% YoY) with an aggregate margin of 8.27% (down from 8.45% in FY25). Total headcount stood at 104,095, including 12,345 temporary/contract workers (10.6% of workforce). Corporate administration headcount totaled 1,127. Total CapEx forward planning is set at $1.90 billion (285,000 million JPY).

Geographic Footprint and Regional Moats

Daikin’s top-line growth is entirely dependent on established Western markets, offsetting observable weakness in the Asia-Pacific basin.

* The Americas: Reached $11,944.44 million (+9.2% YoY), securing a 35.6% global revenue proportion.

* Europe: Recorded $5,735.13 million (+10.0% YoY), constituting 17.1% of global sales.

* Japan (Domestic): Generated $5,413.14 million (+3.1% YoY), representing 16.1% of global operations.

* China (Including Taiwan, China): Contracted to $4,755.19 million (-1.7% YoY), capturing 14.2% of global volume.

* Asia / Oceania: Contracted to $3,155.19 million (-4.5% YoY), holding a 9.4% geographic share.

* Others: Expanded to $2,526.89 million (+13.3% YoY), taking 7.5% of total sales.

Free Cash Flow Yield, Asset Quality, and Capital Allocation

Despite escalating fixed costs, Daikin's core liquidity remains intact, enabling progressive shareholder returns and R&D acceleration.

* R&D Capital Expansion: Pure R&D expenditure expanded 17.2% YoY, rising from $564.25 million (84,394 million JPY) in FY2025 to $661.44 million (98,931 million JPY) in FY2026.

* Dividend Flow: Management increased the dividend per share from $1.10 (165 JPY) in FY2025 to $1.17 (175 JPY) in FY2026. Total capital outflow for dividends scaled from $323.04 million (48,317 million JPY) to $342.64 million (51,248 million JPY).

* Asset Impairment & Credit Risk: A specific $79.22 million (11,849 million JPY) fixed asset impairment loss was recognized and directly linked to AHT Cooling Systems GmbH in Europe. Bad debt provisions marginally increased from $149.7 million (22,395 million JPY) in FY2025 to $157.2 million (23,519 million JPY) in FY2026. Against a total receivables and contract asset baseline of $6.76 billion (1,011,104 million JPY), the bad debt ratio remains stabilized at 2.33%.

* Off-Balance Sheet Items & Pensions: Guarantee reservations increased to $109.8 million (16,424 million JPY) from $66.7 million (9,973 million JPY) in FY2025. The defined benefit obligations display no funding deficit; funded plan assets at fair value stand at $573.2 million (85,734 million JPY), entirely eclipsing the $379.2 million (56,724 million JPY) obligation. Unfunded pure liabilities are recognized at $246.6 million (36,878 million JPY).

Governance Integration and Decarbonization Architecture

Daikin evaluates top management through a strict "Skill Matrix" heavily indexing ESG and sustainability. Compensation structures are strictly performance-linked, utilizing Performance Share Units (PSU, 70% weight) and Restricted Stock Units (RSU, 30% weight). PSU payouts iterate from 0% to 200%, calculated via D-ROIC (Daikin Return on Invested Capital) targets and Relative Total Shareholder Return (TSR) against the TOPIX index. Execution readiness is monitored through "People-Centered Management (PCM) Behaviors," which tracked a 61% practical implementation rate in FY2025.

To satisfy the "Environment Vision 2050" and "FUSION 30" mandates, the executive board enforces scientifically validated (SBTi) greenhouse gas parameters:

* Carbon Intensity Reduction: Management locked a 40% reduction target in GHG emissions per unit of sales, decreasing from 0.08 kg-CO2/JPY in FY2022 to 0.05 kg-CO2/JPY by FY2030.

* Total Emission Reductions: Daikin dictates an expansion in its global emissions reduction contribution from 17.6 million tons of CO2 in FY2022 to 60 million tons by FY2030.

* Supply Chain Baselines: Scope 1 and Scope 2 emissions must drop 46.2% by 2030 (vs. 2019 baseline) leading to net zero by 2050, while Scope 3 upstream/downstream emissions carry a 55% reduction mandate by 2030.

* Solution Business Transition: To insulate against hardware cyclicality, Daikin integrates IoT and AI into Building Management Systems (BMS). Urban energy monetization is being tested through Virtual Power Plant (VPP) architecture and participation in the Toyota Woven City and Shizen Connect energy grid networks.

HDIN Institutional Verdict

An objective audit of the FY2026 data confirms Daikin is successfully executing aggressive cost pass-throughs in its HVAC division across the Americas and Europe, effectively weaponizing the weak Japanese Yen to shield operating profit against global inflation. However, the capital allocation ratio into the Chemicals segment (absorbing 28.4% of total CapEx despite generating only 5.6% of sales and suffering a 28.3% profit contraction) presents immediate D-ROIC drag risks. Furthermore, while rumor-driven market narratives point toward data center cooling acquisitions and structural exclusions involving Goodman, the FY2026 corporate filings provide zero financial confirmation of these specific consolidation shifts. Daikin’s structural ROE compression (12.3% to 9.1% over three years) proves that top-line revenue expansion is currently outpacing marginal capital efficiency, heavily relying on the success of its VPP and R32 solutions to restore unit economics in the 2030 cycle.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."