Momenta Global Limited: Asset-Light Software Pivot Near Suzhou Headquarters as 82.1% Revenue Expansion Signals Viable L4 Operating Leverage

Date : 2026-07-01

Reading : 338

HDIN Executive Takeaways

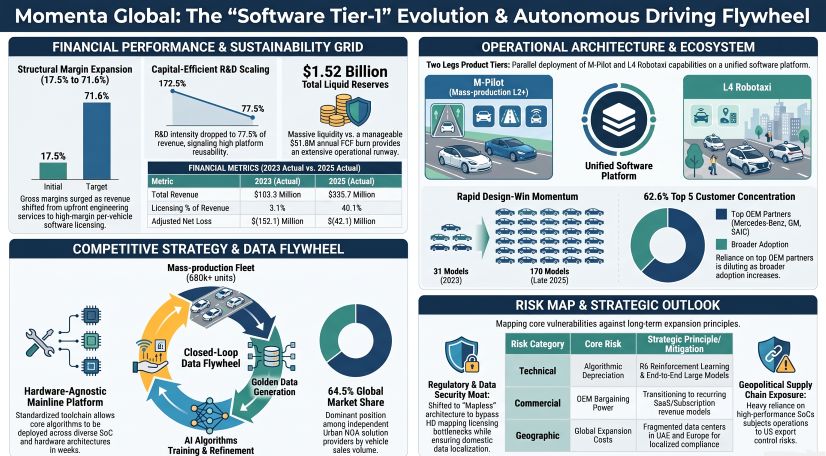

* Operating leverage compressed the R&D-to-revenue ratio from 172.5% to 77.5%, driving a structural gross margin expansion to 71.6% in 2025 as the company transitioned from upfront engineering to high-margin software licensing.

* Global supply chain architecture links 180 automotive design-wins across Suzhou and Stuttgart testing hubs to 4 primary SoC partners, mitigating hardware deployment bottlenecks amid escalating US export controls.

* Extreme institutional overhang looms with 76.6% of outstanding equity (180,548,872 shares) hitting a uniform 6-month lock-up expiration, generating an 84x gross multiple on invested capital off a $0.45 Series A cost basis.

Figure Momenta Global: The "Software Tier-1" Evolution & Autonomous Driving Flywheel

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Momenta Global Limited [HKEX: MOMENTA] is executing a textbook transition from a capital-intensive engineering service provider to a high-margin, pure-play software licensing entity. Top-line revenue advanced 78.4% year-over-year in 2024 and accelerated a further 82.1% in 2025. This scaling is directly correlated with an expanding base of active Standard Operating Procedure (SOP) vehicle deployments, driving the average selling price (ASP) per SOP model from $0.40 million in 2023 to $1.98 million in 2025.

The company employs a highly conservative R&D accounting methodology, recognizing an internal capitalization rate of 0.0%. All internally generated research is expensed immediately. Consequently, the intangible asset balance—comprising exclusively third-party purchased software—stood at a fractional $0 (2023), $0.64 million / RMB 4.6 million (2024), and $0.81 million / RMB 5.8 million (2025).

*(Exchange Rates Applied: 1 USD = 7.1875 CNY | 1 USD = 7.7956 HKD)*

Table Corporate Income & Operating Economics

The company's working capital cycle refutes typical Tier-1 automotive collection lag risks. Trade receivable turnover days compressed from 148 days in 2023 to 109 days in 2024, settling at 105 days in 2025. Simultaneously, trade payable turnover days extended from 55 days (2023) to 59 days (2024) and 61 days (2025).

Trade receivable aging schedules confirm excellent credit quality among OEM partners. Out of $132.6 million in net trade receivables, 99.88% ($132.4 million / RMB 951.9 million) were generated within the past 1 year. The 1-to-2-year aging bucket compressed from $1.4 million (2023) to $0.2 million (2024) and $0.15 million / RMB 1.1 million (2025). Accounts aged 2-to-3 years fell from $0.4 million in 2023 and 2024 to $0 in 2025. By April 30, 2026, $91.4 million (68.9%) of 2025 receivables were settled in cash. The total Expected Credit Loss (ECL) allowance stood at $2.9 million (RMB 20.8 million) against a gross balance of $135.5 million (RMB 973.8 million)—a 2.1% coverage ratio. Furthermore, the company recorded an impairment reversal of $0.46 million (RMB 3.3 million) in 2025.

Statutory balance sheet metrics are heavily distorted by IFRS treatment of Pre-IPO preferred shares. While the statutory current ratio and quick ratio sit at a distressed 0.38x (derived from $1,639.7 million in current assets against $4,277.7 million in current liabilities), $4,147.5 million (RMB 29,810.2 million) of those liabilities are redeemable preferred shares that will automatically convert to equity. Stripping this out, the adjusted current liabilities stand at $130.2 million, generating a robust adjusted current ratio of 12.59x. The statutory net deficit of $(2.49) billion (RMB 17,891.2 million) will clear upon listing. Bank borrowings were zero in 2023 and 2025, briefly touching $14.2 million in 2024. Contract liabilities (OEM prepayments) reached $37.5 million in 2025.

Operating cash outflows narrowed from $(148.7) million (2023) to $(116.3) million (2024) and $(39.1) million (2025). Capital expenditures tracked at $8.9 million, $18.1 million, and $12.7 million across the same period. With a 2025 Free Cash Flow (FCF) burn rate of $(51.8) million (approximately $4.3 million per month), the company maintains total liquid reserves of $1.52 billion (RMB 10,912.4 million). This comprises $181.8 million (RMB 1,306.8 million) in cash equivalents, $1,210.9 million in FVTPL wealth management products, and $101.4 million in term deposits. This yields a cash-only runway of 42 months, expanding to over 350 months when calculating total liquidity against short-term contractual commitments of roughly $75 million (composed of $42.6 million / RMB 306.1 million in cloud services, $30.0 million for a JV, and lease liabilities of $7.3 million / RMB 52.7 million staggered as $2.7 million <1 year, $2.7 million 1-2 years, and $1.9 million 2-5 years).

Infrastructure Layout and Regional Moats

Momenta Global Limited operates a decoupled "Software Tier-1" architecture, standardizing deployments through its "Momenta Mainline Platform" and associated modules (Momenta Adaptor, Framework, and Box). This agnostic approach bridges 24 global OEMs across 4 major System-on-Chip (SoC) partners (including NVIDIA and Qualcomm) and 10 Autonomous Driving Control Unit (ADCU) manufacturers. This infrastructure collapsed adaptation cycles for new SoC platforms to 2 to 3 months, while engineering efficiency improved from requiring 400 engineers over 2 years in 2022 to deploying with 10 to 50 engineers in under 3 months.

The technological moat is protected by a clean litigation record and 1,092 global patents, 473 trademarks, and 165 software copyrights. Registered proprietary architectures include the "R6 Reinforcement Learning Large Model", "Parking Planning Problem Solving Process Recovery System V1.0.0", "Perception Lane Processing Functional Software V1.0", and "Hands-off Warning Processing Functional Software V1.0".

Leveraging this IP, Momenta processes 630,000 daily data clips from consumer vehicles. Cumulative design-wins scaled from 31 models (2023) to 106 (2024), 170 (2025), and 180 by February 28, 2026. Cumulative shipped units expanded from 52,000 to 170,000, 680,000, and 733,000 across the identical timeline. SOP models climbed from 8 to 26, reaching 68 by 2025. This density yields a 64.5% global market share in independent Urban Navigate-on-Autopilot (NOA) solutions based on volume, and 27.4% within the combined Highway/Urban NOA segment. Its Urban NOA specifically boasts 650,000 installed vehicles, 155 design wins, and 57 SOPs. Overall L2 solutions rank Top 5 in China (5.4% share) and Top 10 globally (2.7% share).

Geographically, revenue remains highly concentrated in China (>99% across the track record period), with European operations contributing 0.2% in 2023, 0.1% in 2024, and 0% in 2025. Physical R&D infrastructure is rooted in Beijing, Shanghai, Shenzhen, and Suzhou. Testing and mobility operations span Suzhou, Shanghai, Wuxi, Stuttgart (Germany), Munich (Germany), Abu Dhabi (UAE), and Singapore. To circumvent domestic mapping compliance bottlenecks, subsidiary Beijing Chu Speed canceled its high-definition mapping licenses in January 2024, cementing a fully mapless algorithmic pivot.

Customer concentration is diluting but remains top-heavy. The top 5 customers contributed 86.7% ($89.6 million) of revenue in 2023, 78.3% ($144.3 million) in 2024, and 62.6% ($209.8 million) in 2025. The single largest customer represented 35.7% ($36.9 million), 19.3% ($35.6 million), and 21.6% ($72.7 million) respectively.

Strategic OEM and Connected Party Transactions Architecture

* Mercedes-Benz: Revenue scaled from $32.86M (RMB 236.2M) in 2023 to $33.38M (RMB 239.9M) in 2024, and $56.59M (RMB 406.8M) in 2025.

* General Motors (GM China): Revenue generated $36.94M (RMB 265.5M) in 2023, $23.41M (RMB 168.3M) in 2024, and $5.34M (RMB 38.4M) in 2025.

* SAIC Motor Ecosystem (IM Motors): Revenue provided advanced from $3.94M (RMB 28.3M) in 2023 to $32.78M (RMB 235.6M) in 2024, and $24.14M (RMB 173.5M) in 2025. Costs paid to IM Motors stood at $2.09M (RMB 15.0M) in 2024 and $4.76M (RMB 34.2M) in 2025.

* SAIC Direct Affiliates (2025 Revenue): SAIC-GM contributed $14.96M (RMB 107.5M), SAIC Volkswagen $8.40M (RMB 60.4M), and SAIC Motor direct $1.61M (RMB 11.6M).

* Xiangdao Chuxing (SAIC Mobility): Momenta paid operational service costs of $1.75M (RMB 12.6M) in 2023, $1.12M (RMB 8.1M) in 2024, and $0.46M (RMB 3.3M) in 2025.

* Minor JVs (2023/2024/2025): Dipai Zhixing yielded $9.47M (RMB 68.1M) in 2023 revenue. Lotus Robotics generated $1.54M (RMB 11.1M) in revenue and $0.62M (RMB 4.4M) in costs in 2023. Shanghai Chuangshi received payments of $0.06M (RMB 0.43M) in 2024 and $0.43M (RMB 3.1M) in 2025.

* Expanded Mobility Partners: The ecosystem extends to BMW, Audi, Toyota, Honda, BYD, Chery, Uber, Grab, and Lumo.

HDIN Institutional Verdict and Structural Equity Overhang

Momenta Global Limited's governance structure enforces a strict founder-led, strategically backed mandate. The executive suite—comprising Cao Xudong, Dr. Xia Yan, Dr. Sun Gang, Sun Huan, and An Ren—holds a minority economic stake of 14.85% post-IPO, yet controls 59.85% of the voting power via a Weighted Voting Rights (WVR) structure (Class A shares hold 1 vote; Class B shares hold 10 votes). The board integrates independent oversight from Feng Heping, Wei Yu, Li Dong, and Shao Yu, alongside direct strategic representation from major automotive clients: Zhang Jianjun (SAIC), Wang Xiao'ou (GM China), and Fabian Johannes THOMAS (Mercedes-Benz).

Despite this governance alignment, the company's hyper-scaling capitalization trajectory creates extreme post-IPO liquidity risks. Valuations expanded through over 20 pre-IPO tranches: from $27.5 million ($0.45 per share) in Series A (Jan 2017), passing $226.6 million to $345.0 million across B-1 to B-4, crossing the unicorn threshold at $1.02 billion ($9.82 per share) in Series B-12 (Sep 2018), and expanding from $1.315 billion in Series C to $3.607 billion in C-9. Final rounds (C-10 to C-13) pushed the valuation from $4.109 billion to $6.185 billion ($25.28 per share) by September 2025.

At the targeted listing price of HKD 295.60 per share, the implied IPO market capitalization is HKD 69.62 billion ($8.93 billion). The company plans to deploy roughly 60% of expected net proceeds ($432 million / HKD 3.37 billion) toward advanced GPU clusters (NVIDIA H100/H20) and infrastructure over five years.

However, all 180,548,872 Pre-IPO preferred shares will convert to Class A Ordinary Shares, equating to 76.6% of the 235,538,011 total outstanding shares post-IPO. Every Pre-IPO investor is bound by a uniform 6-month lock-up architecture lacking staggered releases. At the IPO price equivalent of $37.92, early backers possess extreme multiples on invested capital (MOIC): Series A holds an 84x gross multiple, Series B-1 holds a 14x multiple ($2.72 basis), and Series C-13 holds a 50% premium. Fiduciary obligations among venture funds guarantee severe supply-side dumping pressure exactly 180 days post-listing.

Furthermore, post-listing rights reveal a highly specific redemption anomaly. While standard pre-IPO rights permanently extinguish, Series C-1, C-8, and C-9 investors retain a strict redemption right yielding 8% annual simple interest if specified founders depart the firm within 36 months of the IPO.

Simultaneously, the capitalization table faces a 16.85% dilution overhang from aggressive talent retention pools. The 2016 Pre-IPO Share Incentive Plan granted 30,509,410 options (12.95% of post-IPO equity) to 1,711 grantees, while the 2025 RSU plan issued 17,207,372 units (7.31% of equity), with CEO Cao Xudong single-handedly receiving 9,980,285 units.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating leverage compressed the R&D-to-revenue ratio from 172.5% to 77.5%, driving a structural gross margin expansion to 71.6% in 2025 as the company transitioned from upfront engineering to high-margin software licensing.

* Global supply chain architecture links 180 automotive design-wins across Suzhou and Stuttgart testing hubs to 4 primary SoC partners, mitigating hardware deployment bottlenecks amid escalating US export controls.

* Extreme institutional overhang looms with 76.6% of outstanding equity (180,548,872 shares) hitting a uniform 6-month lock-up expiration, generating an 84x gross multiple on invested capital off a $0.45 Series A cost basis.

Figure Momenta Global: The "Software Tier-1" Evolution & Autonomous Driving Flywheel

Segmental Realities and Margin CompressionMomenta Global Limited [HKEX: MOMENTA] is executing a textbook transition from a capital-intensive engineering service provider to a high-margin, pure-play software licensing entity. Top-line revenue advanced 78.4% year-over-year in 2024 and accelerated a further 82.1% in 2025. This scaling is directly correlated with an expanding base of active Standard Operating Procedure (SOP) vehicle deployments, driving the average selling price (ASP) per SOP model from $0.40 million in 2023 to $1.98 million in 2025.

The company employs a highly conservative R&D accounting methodology, recognizing an internal capitalization rate of 0.0%. All internally generated research is expensed immediately. Consequently, the intangible asset balance—comprising exclusively third-party purchased software—stood at a fractional $0 (2023), $0.64 million / RMB 4.6 million (2024), and $0.81 million / RMB 5.8 million (2025).

*(Exchange Rates Applied: 1 USD = 7.1875 CNY | 1 USD = 7.7956 HKD)*

Table Corporate Income & Operating Economics

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Total Revenue | $103.3M / RMB 742.7M | $184.3M / RMB 1,324.7M | $335.7M / RMB 2,412.5M |

| Licensing Services Revenue | $3.2M (3.1%) | $40.7M (22.1%) | $134.7M (40.1%) |

| Technical Development (NRE) | $100.0M (96.8%) | $143.6M (77.9%) | $201.0M (59.9%) |

| Hardware / Other Revenue | $0.1M (0.1%) | $0 | $0 |

| Gross Profit | $18.1M | $90.4M | $240.2M |

| Gross Margin | 17.5% | 49.0% | 71.6% |

| Statutory Net Income / (Loss) | $(357.6)M / RMB 2,570.3M | N/A | $(481.1)M / RMB 3,457.9M |

| Adjusted Net Income / (Loss) (Non-IFRS) | $(152.1)M (147.2% of revenue) | N/A | $(42.1M) (12.6% of revenue) |

| R&D Expenses | $178.2M (172.5%) | $209.8M (113.9%) | $260.0M (77.5%) |

| G&A Expenses | $43.1M (41.7%) | N/A | $56.1M (16.7%) |

| S&M Expenses | $13.7M (13.2%) | N/A | $31.3M (9.3%) |

| Share-Based Compensation | $39.96M / RMB 287.2M | $38.82M / RMB 279.0M | $40.66M / RMB 292.2M |

The company's working capital cycle refutes typical Tier-1 automotive collection lag risks. Trade receivable turnover days compressed from 148 days in 2023 to 109 days in 2024, settling at 105 days in 2025. Simultaneously, trade payable turnover days extended from 55 days (2023) to 59 days (2024) and 61 days (2025).

Trade receivable aging schedules confirm excellent credit quality among OEM partners. Out of $132.6 million in net trade receivables, 99.88% ($132.4 million / RMB 951.9 million) were generated within the past 1 year. The 1-to-2-year aging bucket compressed from $1.4 million (2023) to $0.2 million (2024) and $0.15 million / RMB 1.1 million (2025). Accounts aged 2-to-3 years fell from $0.4 million in 2023 and 2024 to $0 in 2025. By April 30, 2026, $91.4 million (68.9%) of 2025 receivables were settled in cash. The total Expected Credit Loss (ECL) allowance stood at $2.9 million (RMB 20.8 million) against a gross balance of $135.5 million (RMB 973.8 million)—a 2.1% coverage ratio. Furthermore, the company recorded an impairment reversal of $0.46 million (RMB 3.3 million) in 2025.

Statutory balance sheet metrics are heavily distorted by IFRS treatment of Pre-IPO preferred shares. While the statutory current ratio and quick ratio sit at a distressed 0.38x (derived from $1,639.7 million in current assets against $4,277.7 million in current liabilities), $4,147.5 million (RMB 29,810.2 million) of those liabilities are redeemable preferred shares that will automatically convert to equity. Stripping this out, the adjusted current liabilities stand at $130.2 million, generating a robust adjusted current ratio of 12.59x. The statutory net deficit of $(2.49) billion (RMB 17,891.2 million) will clear upon listing. Bank borrowings were zero in 2023 and 2025, briefly touching $14.2 million in 2024. Contract liabilities (OEM prepayments) reached $37.5 million in 2025.

Operating cash outflows narrowed from $(148.7) million (2023) to $(116.3) million (2024) and $(39.1) million (2025). Capital expenditures tracked at $8.9 million, $18.1 million, and $12.7 million across the same period. With a 2025 Free Cash Flow (FCF) burn rate of $(51.8) million (approximately $4.3 million per month), the company maintains total liquid reserves of $1.52 billion (RMB 10,912.4 million). This comprises $181.8 million (RMB 1,306.8 million) in cash equivalents, $1,210.9 million in FVTPL wealth management products, and $101.4 million in term deposits. This yields a cash-only runway of 42 months, expanding to over 350 months when calculating total liquidity against short-term contractual commitments of roughly $75 million (composed of $42.6 million / RMB 306.1 million in cloud services, $30.0 million for a JV, and lease liabilities of $7.3 million / RMB 52.7 million staggered as $2.7 million <1 year, $2.7 million 1-2 years, and $1.9 million 2-5 years).

Infrastructure Layout and Regional Moats

Momenta Global Limited operates a decoupled "Software Tier-1" architecture, standardizing deployments through its "Momenta Mainline Platform" and associated modules (Momenta Adaptor, Framework, and Box). This agnostic approach bridges 24 global OEMs across 4 major System-on-Chip (SoC) partners (including NVIDIA and Qualcomm) and 10 Autonomous Driving Control Unit (ADCU) manufacturers. This infrastructure collapsed adaptation cycles for new SoC platforms to 2 to 3 months, while engineering efficiency improved from requiring 400 engineers over 2 years in 2022 to deploying with 10 to 50 engineers in under 3 months.

The technological moat is protected by a clean litigation record and 1,092 global patents, 473 trademarks, and 165 software copyrights. Registered proprietary architectures include the "R6 Reinforcement Learning Large Model", "Parking Planning Problem Solving Process Recovery System V1.0.0", "Perception Lane Processing Functional Software V1.0", and "Hands-off Warning Processing Functional Software V1.0".

Leveraging this IP, Momenta processes 630,000 daily data clips from consumer vehicles. Cumulative design-wins scaled from 31 models (2023) to 106 (2024), 170 (2025), and 180 by February 28, 2026. Cumulative shipped units expanded from 52,000 to 170,000, 680,000, and 733,000 across the identical timeline. SOP models climbed from 8 to 26, reaching 68 by 2025. This density yields a 64.5% global market share in independent Urban Navigate-on-Autopilot (NOA) solutions based on volume, and 27.4% within the combined Highway/Urban NOA segment. Its Urban NOA specifically boasts 650,000 installed vehicles, 155 design wins, and 57 SOPs. Overall L2 solutions rank Top 5 in China (5.4% share) and Top 10 globally (2.7% share).

Geographically, revenue remains highly concentrated in China (>99% across the track record period), with European operations contributing 0.2% in 2023, 0.1% in 2024, and 0% in 2025. Physical R&D infrastructure is rooted in Beijing, Shanghai, Shenzhen, and Suzhou. Testing and mobility operations span Suzhou, Shanghai, Wuxi, Stuttgart (Germany), Munich (Germany), Abu Dhabi (UAE), and Singapore. To circumvent domestic mapping compliance bottlenecks, subsidiary Beijing Chu Speed canceled its high-definition mapping licenses in January 2024, cementing a fully mapless algorithmic pivot.

Customer concentration is diluting but remains top-heavy. The top 5 customers contributed 86.7% ($89.6 million) of revenue in 2023, 78.3% ($144.3 million) in 2024, and 62.6% ($209.8 million) in 2025. The single largest customer represented 35.7% ($36.9 million), 19.3% ($35.6 million), and 21.6% ($72.7 million) respectively.

Strategic OEM and Connected Party Transactions Architecture

* Mercedes-Benz: Revenue scaled from $32.86M (RMB 236.2M) in 2023 to $33.38M (RMB 239.9M) in 2024, and $56.59M (RMB 406.8M) in 2025.

* General Motors (GM China): Revenue generated $36.94M (RMB 265.5M) in 2023, $23.41M (RMB 168.3M) in 2024, and $5.34M (RMB 38.4M) in 2025.

* SAIC Motor Ecosystem (IM Motors): Revenue provided advanced from $3.94M (RMB 28.3M) in 2023 to $32.78M (RMB 235.6M) in 2024, and $24.14M (RMB 173.5M) in 2025. Costs paid to IM Motors stood at $2.09M (RMB 15.0M) in 2024 and $4.76M (RMB 34.2M) in 2025.

* SAIC Direct Affiliates (2025 Revenue): SAIC-GM contributed $14.96M (RMB 107.5M), SAIC Volkswagen $8.40M (RMB 60.4M), and SAIC Motor direct $1.61M (RMB 11.6M).

* Xiangdao Chuxing (SAIC Mobility): Momenta paid operational service costs of $1.75M (RMB 12.6M) in 2023, $1.12M (RMB 8.1M) in 2024, and $0.46M (RMB 3.3M) in 2025.

* Minor JVs (2023/2024/2025): Dipai Zhixing yielded $9.47M (RMB 68.1M) in 2023 revenue. Lotus Robotics generated $1.54M (RMB 11.1M) in revenue and $0.62M (RMB 4.4M) in costs in 2023. Shanghai Chuangshi received payments of $0.06M (RMB 0.43M) in 2024 and $0.43M (RMB 3.1M) in 2025.

* Expanded Mobility Partners: The ecosystem extends to BMW, Audi, Toyota, Honda, BYD, Chery, Uber, Grab, and Lumo.

HDIN Institutional Verdict and Structural Equity Overhang

Momenta Global Limited's governance structure enforces a strict founder-led, strategically backed mandate. The executive suite—comprising Cao Xudong, Dr. Xia Yan, Dr. Sun Gang, Sun Huan, and An Ren—holds a minority economic stake of 14.85% post-IPO, yet controls 59.85% of the voting power via a Weighted Voting Rights (WVR) structure (Class A shares hold 1 vote; Class B shares hold 10 votes). The board integrates independent oversight from Feng Heping, Wei Yu, Li Dong, and Shao Yu, alongside direct strategic representation from major automotive clients: Zhang Jianjun (SAIC), Wang Xiao'ou (GM China), and Fabian Johannes THOMAS (Mercedes-Benz).

Despite this governance alignment, the company's hyper-scaling capitalization trajectory creates extreme post-IPO liquidity risks. Valuations expanded through over 20 pre-IPO tranches: from $27.5 million ($0.45 per share) in Series A (Jan 2017), passing $226.6 million to $345.0 million across B-1 to B-4, crossing the unicorn threshold at $1.02 billion ($9.82 per share) in Series B-12 (Sep 2018), and expanding from $1.315 billion in Series C to $3.607 billion in C-9. Final rounds (C-10 to C-13) pushed the valuation from $4.109 billion to $6.185 billion ($25.28 per share) by September 2025.

At the targeted listing price of HKD 295.60 per share, the implied IPO market capitalization is HKD 69.62 billion ($8.93 billion). The company plans to deploy roughly 60% of expected net proceeds ($432 million / HKD 3.37 billion) toward advanced GPU clusters (NVIDIA H100/H20) and infrastructure over five years.

However, all 180,548,872 Pre-IPO preferred shares will convert to Class A Ordinary Shares, equating to 76.6% of the 235,538,011 total outstanding shares post-IPO. Every Pre-IPO investor is bound by a uniform 6-month lock-up architecture lacking staggered releases. At the IPO price equivalent of $37.92, early backers possess extreme multiples on invested capital (MOIC): Series A holds an 84x gross multiple, Series B-1 holds a 14x multiple ($2.72 basis), and Series C-13 holds a 50% premium. Fiduciary obligations among venture funds guarantee severe supply-side dumping pressure exactly 180 days post-listing.

Furthermore, post-listing rights reveal a highly specific redemption anomaly. While standard pre-IPO rights permanently extinguish, Series C-1, C-8, and C-9 investors retain a strict redemption right yielding 8% annual simple interest if specified founders depart the firm within 36 months of the IPO.

Simultaneously, the capitalization table faces a 16.85% dilution overhang from aggressive talent retention pools. The 2016 Pre-IPO Share Incentive Plan granted 30,509,410 options (12.95% of post-IPO equity) to 1,711 grantees, while the 2025 RSU plan issued 17,207,372 units (7.31% of equity), with CEO Cao Xudong single-handedly receiving 9,980,285 units.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."