Beijing Surgerii Robotics Co., Ltd.: 2026 European Direct-Sale Pivot Near Amsterdam as 47.83% Sales-to-Production Ratio Signals Global Single-Port Expansion

Date : 2026-07-04

Reading : 65

HDIN Executive Takeaways

* Operating Scale: FY2025 revenue hit $11.30 million (78.03% hardware) via 11 commercial installations. Gross margins normalized to 59.52% amid a 47.83% sales-to-production ratio.

* Global Footprint: EU direct-sales initiated via a $2.74 million Spanish public tender and German pay-per-use models, supported by Amsterdam and Hong Kong regional hubs.

* Capital Strategy: Founder Dr. Xu Kai leverages a 43.61% voting bloc to target $97.39 million in IPO proceeds, prioritizing dual-continent distribution to navigate domestic 819-unit Class B equipment quotas.

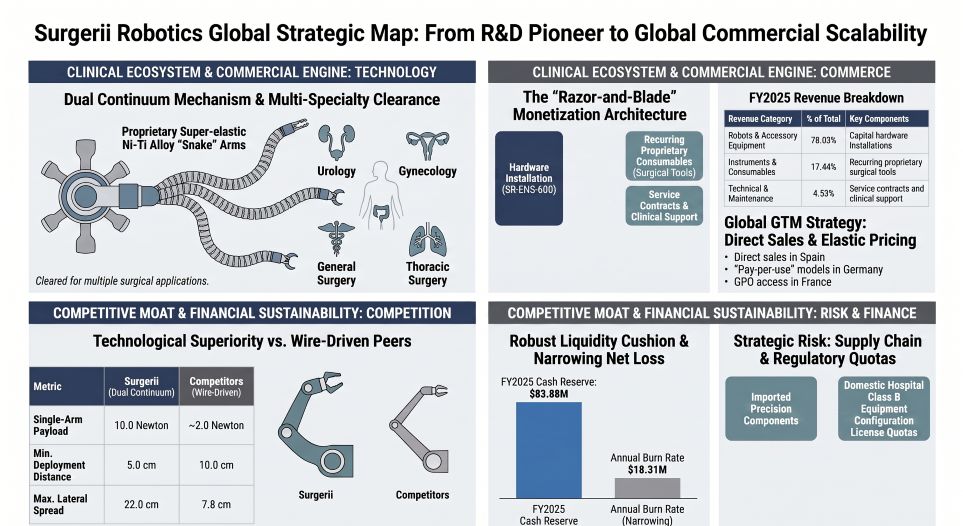

Figure Surgeri Robotics Global Strategic Map: From R&D Pioneer to Global Commercial Scalability

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Beijing Surgerii Robotics Co., Ltd. (Surgerii Robotics) is transitioning from R&D capitalization to early commercial scaling. FY2025 operating cash burn contracted to -$14.74 million (from -$27.11 million in FY2024 and -$29.80 million in FY2023) as cash inflows from goods sold accelerated from $6.66 million in FY2024 to $13.17 million in FY2025. Consolidated asset-liability ratio stands at 6.40%, with strict short-term solvency indicated by a Current Ratio of 20.13x, a Quick Ratio of 18.27x, and total liabilities capped at $11.01 million.

Total FY2025 recognized revenue registered at $11.30 million (CNY 81.23 million), driven 100% by the domestic market. The commercial architecture relies heavily on distribution (71.32%) versus direct sales (28.68%). Total inventory turnover accelerated from 0.01 in FY2023 to 0.10 in FY2024, reaching 0.49 in FY2025, with final inventory value stabilizing at $8.79 million.

Revenue and Volume Distribution (FY2025)

* Production & Sales: 23 units manufactured, 11 units sold (47.83% sales-to-production ratio).

* Single-Port Robots & Accessory Equipment: $8.82 million (CNY 63.38 million), representing 78.03% of core revenue. Hardware gross margins sustained at 68.38%.

* Instruments & Consumables: $1.97 million (CNY 14.17 million), representing 17.44% of revenue (up from 7.54% in FY2024). Consumable margins sit at 21.45%.

* Technical & Maintenance Services: $0.51 million (CNY 3.68 million), representing 4.53% of revenue.

Cost Structure and Profitability

Overall gross margin contracted from 67.39% in FY2024 to 59.52% in FY2025 due to revenue mix normalization. Total Cost of Goods Sold (COGS) reached $4.57 million, exhibiting high material intensity: raw materials (79.82% / $3.65 million), direct labor (5.55%), and manufacturing overhead (14.64%). Historical R&D commitments yielded a net loss of -$26.56 million in FY2023, peaking at -$27.19 million in FY2024, and narrowing to -$18.31 million in FY2025, driven by $12.27 million in FY2025 R&D expenditures. Accumulated unrecovered deficit stands at -$73.78 million.

Accounts Receivable (AR) management is highly disciplined, with an AR balance of $3.09 million at the end of FY2025 (100% aged under one year). Post-balance-sheet data confirms $3.03 million (93.09%) was collected by May 2026, generating an AR turnover ratio of 7.32.

Infrastructure Layout and Regional Moats

The operational architecture of Surgerii Robotics utilizes decentralized domestic manufacturing hubs and dedicated regional corporate entities. Production and assembly of the Class B large medical equipment are executed at the Daxing Biomedical Industry Base within the Zhongguancun Science Park in Beijing, with corporate registration anchored in the Haidian District. Core R&D—focusing on hardware, software algorithms, and multi-articulating snake-like surgical instruments—is consolidated at the Caohejing Zhuanqiao Technology Oasis in Minhang District, Shanghai.

International Corporate Footprint & Commercial Milestones

To bypass domestic configuration license quotas (capped nationally at 819 units), the company initiated an aggressive European and Asia-Pacific direct-sales strategy:

* European Hub: Surgerii Robotics (Netherlands) B.V. operates out of Amsterdam with a registered capital of $113,060 (EUR 100,000) to manage EU warehousing, marketing, and clinical support.

* APAC Hub: Surgerii Robotics (Hong Kong) Limited manages Southeast Asian operations and cross-border settlements with a registered capital of $500,000.

* H1 2026 Commercial Execution: The firm secured a direct-sale public tender at Vall d'Hebron University Hospital (Spain) for $2.74 million (EUR 2.42 million). Simultaneously, it implemented an elastic "pay-per-use" revenue model at München Klinik Bogenhausen (Germany) and achieved central procurement qualification from UniHA in France.

Supply Chain Architecture

The material-heavy COGS profile relies on top 5 supplier concentration ratios of 34.46% (FY2023), 31.07% (FY2024), and 34.00% (FY2025). The company holds no single-source reliance exceeding 50%. Critical FY2025 hardware vendor distributions include:

* Suzhou Junhe Servo Technology Co., Ltd. (High-precision motors): 11.32%

* Shanghai Yilian Precision Machinery Manufacturing Co., Ltd. (Modules): 8.39%

* Xiamen Baoqi Medical Technology Co., Ltd. (Modules): 5.29%

* Shanghai Qianran Technology Development Co., Ltd. (Mechanical parts): 4.61%

HDIN Institutional Verdict

Surgerii Robotics commands highly defensive engineering parameters. The firm’s proprietary "Dual Continuum Mechanism" utilizes super-elastic Nickel-Titanium (Ni-Ti) alloy to achieve a 10N single-arm payload, a 22cm lateral spread, and a 5cm minimum deployment distance. This directly outperforms incumbent wire-driven systems like the da Vinci SP, which yields a 2N payload, a 7.8cm lateral spread, and a 10cm minimum deployment requirement.

To commercialize this technological advantage, the company leverages an entrenched clinical network across 19 domestic Grade A tertiary hospitals, completing over 3,500 global surgeries. However, the regulatory pipeline requires strict monitoring:

* SR-ENS-600 Series: NMPA approved for urology (June 2023), gynecology (February 2024), and general/thoracic surgery (May 2025). Maxillofacial indications are targeted for H1 2027. CE Mark secured in August 2025 (world's first CE-certified pediatric single-port system).

* SR-ENS-660 Series: NMPA approved in March 2026 for multi-port integration.

* SR-ENS-700 Series: Currently integrating 8mm and 6mm instruments, targeting NMPA/CE by H2 2027 and FDA clearance by H1 2029.

Clinical Integrity and Institutional Backing

Rigorous clinical validations utilized 135 subjects in urology (4 centers, plus 32 pre-trial cases), 63 in gynecology (6 centers), 31 in general surgery (4 centers), 35 in thoracic surgery (Guangzhou Medical University First Affiliated Hospital), and 63 in maxillofacial trials. Documented Severe Adverse Events (SAEs)—including 1 gastrointestinal anastomotic leakage, 1 vaginal stump bleeding, 1 Type I respiratory failure, and 6 maxillofacial SAEs—were universally assessed as unrelated to the device, with zero fatal adverse events recorded.

The cap table reflects heavy institutional validation. Dr. Xu Kai controls 43.61% of voting rights (17.99% direct; 25.62% via employee platforms Beijing Shucheng, Shanghai Shurui, and Hainan Shurui) and nominates 5 of 8 non-independent directors. Strategic capital includes Medtronic [NYSE: MDT] via Covidien Healthcare International Trading (Shanghai) Co., Ltd. at 2.96%. Institutional VC support is led by Loyal Valley Capital (LVC) and its affiliates at 17.29% (11.56% direct LVC), Astrend III (Hong Kong) Limited at 8.30%, Shanghai Biomedical Fund at 5.21%, SDIC Fund Management at 6.73%, and Tianfeng Healthcare/Yangfan at 5.47%.

Armed with $83.88 million in cash equivalents and $127.80 million in total monetary funds (including $43.71 million in FX cleared in January 2026), the firm targets $97.39 million (CNY 700.00 million) in net IPO proceeds against a $134.59 million (CNY 967.38 million) total project pool. Capital deployment will prioritize $38.96 million for R&D ($58.31 million total), $29.22 million for global marketing networks ($47.06 million total), and $29.22 million for working capital. Intellectual property risk is tightly managed, featuring 732 applied and 471 granted patents (319 core patents: 148 domestic, 171 overseas), the acquisition of 5 foundational patents from Shanghai Jiao Tong University for $487,000 (CNY 3.50 million), and 26 shared clinical patents requiring zero future royalty disbursements.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating Scale: FY2025 revenue hit $11.30 million (78.03% hardware) via 11 commercial installations. Gross margins normalized to 59.52% amid a 47.83% sales-to-production ratio.

* Global Footprint: EU direct-sales initiated via a $2.74 million Spanish public tender and German pay-per-use models, supported by Amsterdam and Hong Kong regional hubs.

* Capital Strategy: Founder Dr. Xu Kai leverages a 43.61% voting bloc to target $97.39 million in IPO proceeds, prioritizing dual-continent distribution to navigate domestic 819-unit Class B equipment quotas.

Figure Surgeri Robotics Global Strategic Map: From R&D Pioneer to Global Commercial Scalability

Segmental Realities and Margin CompressionBeijing Surgerii Robotics Co., Ltd. (Surgerii Robotics) is transitioning from R&D capitalization to early commercial scaling. FY2025 operating cash burn contracted to -$14.74 million (from -$27.11 million in FY2024 and -$29.80 million in FY2023) as cash inflows from goods sold accelerated from $6.66 million in FY2024 to $13.17 million in FY2025. Consolidated asset-liability ratio stands at 6.40%, with strict short-term solvency indicated by a Current Ratio of 20.13x, a Quick Ratio of 18.27x, and total liabilities capped at $11.01 million.

Total FY2025 recognized revenue registered at $11.30 million (CNY 81.23 million), driven 100% by the domestic market. The commercial architecture relies heavily on distribution (71.32%) versus direct sales (28.68%). Total inventory turnover accelerated from 0.01 in FY2023 to 0.10 in FY2024, reaching 0.49 in FY2025, with final inventory value stabilizing at $8.79 million.

Revenue and Volume Distribution (FY2025)

* Production & Sales: 23 units manufactured, 11 units sold (47.83% sales-to-production ratio).

* Single-Port Robots & Accessory Equipment: $8.82 million (CNY 63.38 million), representing 78.03% of core revenue. Hardware gross margins sustained at 68.38%.

* Instruments & Consumables: $1.97 million (CNY 14.17 million), representing 17.44% of revenue (up from 7.54% in FY2024). Consumable margins sit at 21.45%.

* Technical & Maintenance Services: $0.51 million (CNY 3.68 million), representing 4.53% of revenue.

Cost Structure and Profitability

Overall gross margin contracted from 67.39% in FY2024 to 59.52% in FY2025 due to revenue mix normalization. Total Cost of Goods Sold (COGS) reached $4.57 million, exhibiting high material intensity: raw materials (79.82% / $3.65 million), direct labor (5.55%), and manufacturing overhead (14.64%). Historical R&D commitments yielded a net loss of -$26.56 million in FY2023, peaking at -$27.19 million in FY2024, and narrowing to -$18.31 million in FY2025, driven by $12.27 million in FY2025 R&D expenditures. Accumulated unrecovered deficit stands at -$73.78 million.

Accounts Receivable (AR) management is highly disciplined, with an AR balance of $3.09 million at the end of FY2025 (100% aged under one year). Post-balance-sheet data confirms $3.03 million (93.09%) was collected by May 2026, generating an AR turnover ratio of 7.32.

Infrastructure Layout and Regional Moats

The operational architecture of Surgerii Robotics utilizes decentralized domestic manufacturing hubs and dedicated regional corporate entities. Production and assembly of the Class B large medical equipment are executed at the Daxing Biomedical Industry Base within the Zhongguancun Science Park in Beijing, with corporate registration anchored in the Haidian District. Core R&D—focusing on hardware, software algorithms, and multi-articulating snake-like surgical instruments—is consolidated at the Caohejing Zhuanqiao Technology Oasis in Minhang District, Shanghai.

International Corporate Footprint & Commercial Milestones

To bypass domestic configuration license quotas (capped nationally at 819 units), the company initiated an aggressive European and Asia-Pacific direct-sales strategy:

* European Hub: Surgerii Robotics (Netherlands) B.V. operates out of Amsterdam with a registered capital of $113,060 (EUR 100,000) to manage EU warehousing, marketing, and clinical support.

* APAC Hub: Surgerii Robotics (Hong Kong) Limited manages Southeast Asian operations and cross-border settlements with a registered capital of $500,000.

* H1 2026 Commercial Execution: The firm secured a direct-sale public tender at Vall d'Hebron University Hospital (Spain) for $2.74 million (EUR 2.42 million). Simultaneously, it implemented an elastic "pay-per-use" revenue model at München Klinik Bogenhausen (Germany) and achieved central procurement qualification from UniHA in France.

Supply Chain Architecture

The material-heavy COGS profile relies on top 5 supplier concentration ratios of 34.46% (FY2023), 31.07% (FY2024), and 34.00% (FY2025). The company holds no single-source reliance exceeding 50%. Critical FY2025 hardware vendor distributions include:

* Suzhou Junhe Servo Technology Co., Ltd. (High-precision motors): 11.32%

* Shanghai Yilian Precision Machinery Manufacturing Co., Ltd. (Modules): 8.39%

* Xiamen Baoqi Medical Technology Co., Ltd. (Modules): 5.29%

* Shanghai Qianran Technology Development Co., Ltd. (Mechanical parts): 4.61%

HDIN Institutional Verdict

Surgerii Robotics commands highly defensive engineering parameters. The firm’s proprietary "Dual Continuum Mechanism" utilizes super-elastic Nickel-Titanium (Ni-Ti) alloy to achieve a 10N single-arm payload, a 22cm lateral spread, and a 5cm minimum deployment distance. This directly outperforms incumbent wire-driven systems like the da Vinci SP, which yields a 2N payload, a 7.8cm lateral spread, and a 10cm minimum deployment requirement.

To commercialize this technological advantage, the company leverages an entrenched clinical network across 19 domestic Grade A tertiary hospitals, completing over 3,500 global surgeries. However, the regulatory pipeline requires strict monitoring:

* SR-ENS-600 Series: NMPA approved for urology (June 2023), gynecology (February 2024), and general/thoracic surgery (May 2025). Maxillofacial indications are targeted for H1 2027. CE Mark secured in August 2025 (world's first CE-certified pediatric single-port system).

* SR-ENS-660 Series: NMPA approved in March 2026 for multi-port integration.

* SR-ENS-700 Series: Currently integrating 8mm and 6mm instruments, targeting NMPA/CE by H2 2027 and FDA clearance by H1 2029.

Clinical Integrity and Institutional Backing

Rigorous clinical validations utilized 135 subjects in urology (4 centers, plus 32 pre-trial cases), 63 in gynecology (6 centers), 31 in general surgery (4 centers), 35 in thoracic surgery (Guangzhou Medical University First Affiliated Hospital), and 63 in maxillofacial trials. Documented Severe Adverse Events (SAEs)—including 1 gastrointestinal anastomotic leakage, 1 vaginal stump bleeding, 1 Type I respiratory failure, and 6 maxillofacial SAEs—were universally assessed as unrelated to the device, with zero fatal adverse events recorded.

The cap table reflects heavy institutional validation. Dr. Xu Kai controls 43.61% of voting rights (17.99% direct; 25.62% via employee platforms Beijing Shucheng, Shanghai Shurui, and Hainan Shurui) and nominates 5 of 8 non-independent directors. Strategic capital includes Medtronic [NYSE: MDT] via Covidien Healthcare International Trading (Shanghai) Co., Ltd. at 2.96%. Institutional VC support is led by Loyal Valley Capital (LVC) and its affiliates at 17.29% (11.56% direct LVC), Astrend III (Hong Kong) Limited at 8.30%, Shanghai Biomedical Fund at 5.21%, SDIC Fund Management at 6.73%, and Tianfeng Healthcare/Yangfan at 5.47%.

Armed with $83.88 million in cash equivalents and $127.80 million in total monetary funds (including $43.71 million in FX cleared in January 2026), the firm targets $97.39 million (CNY 700.00 million) in net IPO proceeds against a $134.59 million (CNY 967.38 million) total project pool. Capital deployment will prioritize $38.96 million for R&D ($58.31 million total), $29.22 million for global marketing networks ($47.06 million total), and $29.22 million for working capital. Intellectual property risk is tightly managed, featuring 732 applied and 471 granted patents (319 core patents: 148 domestic, 171 overseas), the acquisition of 5 foundational patents from Shanghai Jiao Tong University for $487,000 (CNY 3.50 million), and 26 shared clinical patents requiring zero future royalty disbursements.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."