AeroVironment: $3.48 Billion Defense Prime Pivot Near Alabama and Utah as 1,350-bps Margin Contraction Signals M&A Friction

Date : 2026-07-02

Reading : 284

HDIN Executive Takeaways

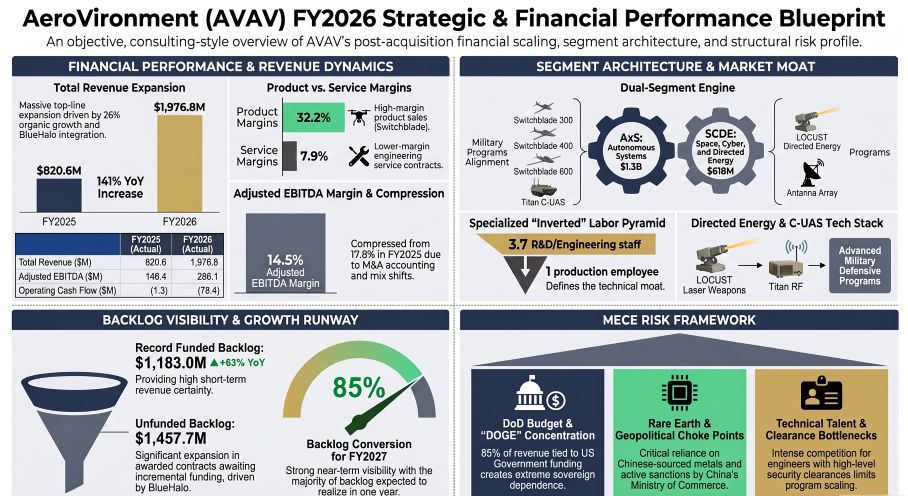

* FY2026 consolidated revenue reached $1,976.8 million (up 141% YoY) backed by a $1,183.0 million funded backlog, though GAAP gross margins collapsed 1,350 basis points to 25.3% amidst aggressive M&A integration.

* Capital deployment targets physical supply chain bottlenecks via a $16.3 million facility acquisition in Huntsville, Alabama, and a new West Valley City, Utah footprint, navigating Chinese rare-earth export sanctions.

* A $240.7 million Space segment goodwill impairment—triggered by a U.S. Space Force stop-work order—exposes acute vulnerabilities to sovereign funding cycles and un-definitized contracting risks.

Figure AeroVironment (AVAV) FY2026 Strategic & Financial Performance Blueprint

Segmental Realities and Financial Diagnostics

Segmental Realities and Financial Diagnostics

AeroVironment, Inc. [NASDAQ: AVAV] fundamentally restructured its P&L in FY2026, transitioning from a tactical hardware manufacturer into a dual-segment defense prime following the $3.48 billion acquisition of BlueHalo (effective May 1, 2025) and the $177.9 million acquisition of ESAero (effective March 2026). While consolidated top-line growth accelerated to 141%, operating leverage deteriorated due to integration friction, structural shifts in services revenue, and acute margin compression.

Of the $1,156.2 million top-line expansion, $939.2 million was inorganic ($526.0 million in products and $413.2 million in services). Stripping out M&A contributions, legacy organic revenue expanded 26.4%, adding $217.0 million ($196.6 million in products, $20.4 million in services) to the FY2025 $820.6 million baseline.

Consolidated Income & Margin Compression Matrix

* Total Revenue: $1,976.8 million in FY2026 vs. $820.6 million in FY2025.

* GAAP Net Income / Loss: Net loss of $(265.1) million vs. Net income of $43.6 million.

* GAAP Gross Margin: 25.3% ($500.6 million) vs. 38.8% ($318.6 million).

* Product Margin: 32.2% ($456.1 million GM on $1,415.3 million revenue) vs. 41.6%.

* Services Margin: 7.9% ($44.5 million GM on $561.5 million revenue) vs. 23.7%.

* Non-GAAP Adjusted EBITDA Margin: 14.5% ($286.1 million) vs. 17.8% ($146.4 million).

* Research & Development (R&D): $127.7 million (6% of revenue) vs. $100.7 million (12% of revenue). Customer-funded R&D generated $240.9 million in revenue against $209.7 million in costs.

* SG&A Expenses: 22% of revenue ($443.2 million).

* M&A & Intangible Amortization: Acquisition expenses totaled $48.1 million. Cost of sales absorbed $92.7 million in non-cash purchase accounting and intangible amortization vs. $19.4 million.

Table Reporting Segment Realities

Working Capital and Balance Sheet Architecture

Cash Flow from Operations (CFO) contracted to $(78.4) million from $(1.3) million, driven by the operational absorption of $399.3 million in working capital.

* Liquidity & Capital Raise: Following a July 2025 $1.70 billion capital raise (common stock and 0% convertible senior notes), the company allocated $965.3 million to eradicate existing Term Loan and Revolver debt. Total available liquidity sits at $969.1 million ($377.3 million cash and cash equivalents, $255.0 million short-term investments, $336.8 million available revolver capacity).

* Receivables: Accounts receivable consumed $128.7 million, with ending billed AR at $316.2 million. Unbilled receivables and retentions grew 96.7% to $570.4 million from $290.0 million (BlueHalo added $96.4 million, ESAero added $25.0 million, resulting in 54.8% organic growth).

* Inventory Turns: Inventory levels surged to $312.9 million from $144.1 million, triggering a $111.6 million cash outflow. Against $1,476.2 million in Cost of Sales and $228.5 million in average inventory, turns stand at 6.46x (or 4.7x measured against ending inventory).

* Liabilities & Deferred Costs: Deferred revenue (customer advances) expanded to $79.6 million from $16.0 million. Deferred costs to fulfill dropped to $0 from $1.9 million.

Contract Typology & Forward Visibility

The total funded backlog reached $1,183.0 million (up 63% from $726.6 million), with management projecting an 85% conversion rate in FY2027. Unfunded backlog expanded to $1,457.7 million from $774.6 million.

* Firm-Fixed-Price (FFP): $1,384.3 million (70.0% of revenue) vs. $746.2 million (90.9%). A $3.9 million forward loss reserve was recorded on an Integrated Air and Missile Defense (IAMD) contract.

* Cost-Plus-Fee (CPFF, CPIF, CPAF): $454.1 million (23.0% of revenue) vs. $68.0 million (8.3%), growing 567.8% YoY.

* Time-and-Materials (T&M): $138.4 million (7.0% of revenue) vs. $6.5 million (0.8%), growing 2,029.2% YoY.

Infrastructure Layout and Regional Moats

To execute against its backlog and integrate M&A targets, AeroVironment is executing a highly centralized capacity expansion utilizing ISO 9001:2015 and AS9100D certified facilities. Total segment capital expenditures reached $86.2 million ($50.7 million deployed in AxS, $29.3 million in SCDE, $6.0 million in Corporate). Cash used strictly for purchasing property and equipment was $62.5 million, up from $22.8 million.

Geographic Facility Map

* California Core: Simi Valley contains 280,000 square feet of leased space expiring between 2027 and 2030; Moorpark adds 150,000 square feet.

* SCDE & Tech Hubs: Albuquerque, New Mexico operates 200,000 square feet (leases expiring 2028-2034).

* Capital Expansion Execution: Huntsville, Alabama operates a 150,000-square-foot node. In May 2026, the company notified the lessor of its intent to purchase the 100 Quality Circle building in Huntsville for $16.3 million. In December 2025, a new lease was executed for 4387 West 2100 South in West Valley City, Utah.

* Global & Auxiliary Footprint: Stuttgart, Germany (Telerob/UGV) and Hampton Bishop, United Kingdom. Domestic operations span Arlington, Virginia (Corporate HQ), Maryland, Florida, Pennsylvania, Kansas, Colorado, Minnesota, Oklahoma, Texas, and Ohio.

Labor Demographics and Component Vulnerabilities

The enterprise relies on 3,991 full-time and 100 part-time employees. The labor pyramid is heavily skewed toward technical design, featuring 2,366 R&D/Engineering staff (including 208 PhDs) against 637 Operations/Manufacturing personnel (a 3.7 to 1 ratio). G&A encompasses 907 employees, while Sales/Marketing holds 181. A June 11, 2025 agreement in principle settled a 2024 PAGA labor/wage class action (accrued in FY2025).

Supply chain architecture is actively threatened by geopolitical choke points. Sourcing for advanced UAS components, motors, and batteries relies on rare earth metals predominantly refined in China. Following U.S. military sales to Taiwan, China, the Chinese Ministry of Commerce placed AeroVironment on its export control list and imposed direct sanctions in early 2024 and March 2025. Concurrently, the Telerob subsidiary in Germany must navigate the phased 2025 rollout of the EU Artificial Intelligence Act, which classifies critical infrastructure biometric systems as high-risk.

Customer Concentration

The U.S. Government dictates 85% of total revenue. Direct Department of Defense (DoD) contracts constitute 63%, with the U.S. Army comprising 25% and other U.S. agencies comprising 47%. International/Foreign customers (including Foreign Military Sales) generated $556.4 million (28% of revenue), proportionally diluted from 52% strictly due to BlueHalo's domestic concentration.

Competitor Matrix and Intellectual Property

AeroVironment deploys 407 U.S. patents and proprietary AI software (AVACORE and SPOTR-EDGE) to operate within Modular Open Systems Architecture (MOSA) and Sensor Open System Architecture (SOSA) standards. The physical product portfolio spans Switchblade 300, 400, and 600, Blackwing, Red Dragon, Mayhem, the Titan family (Titan 4, Titan SV MPV3, Titan-MS), Freedom Eagle (FE-1), WildCat (DARPA), LOCUST (20-35+ kilowatt laser), BADGER antennas, and AV_Halo/Kinesis software.

Management explicitly identifies the following entities as direct market competitors across its operating vectors:

* UAS: Elbit Systems Ltd., Quantum-Systems, Inc., Redwire Corporation, Teledyne Technologies, Inc., Sierra Nevada Corporation, Lockheed Martin Corporation, The Boeing Company, Textron, Inc., Shield AI, Inc., Northrop Grumman Corporation, Griffon Aerospace, Inc., L3Harris Technologies, Inc., Anduril Industries, Inc., Airbus SE, and Israeli Aircraft Industries.

* Precision Strike: Textron Inc., RTX Corporation, Lockheed Martin Corporation, Anduril Industries, Inc., Aevex Corp., SpektreWorks, Inc., Dragoon Technology LLC, Cummings Aerospace, Inc., Elbit Systems Ltd., and UVision Air Ltd.

* C-UAS & EW: Anduril Industries, Inc., The Boeing Company, Lockheed Martin Corporation, RTX Corporation, DroneShield Limited, SRC Inc., Polaris, Inc., CACI International Inc., Northrop Grumman Corporation, and L3Harris Technologies, Inc.

* SCDE: The Boeing Company, Lockheed Martin Corporation, L3Harris Technologies, Inc., BAE Systems, Inc., nLIGHT, Inc., Epirus, Inc., EO Solutions Corporation, Huntington Ingalls Industries, Inc., RTX Corporation, Thales Group, Anduril Industries, Inc., Sierra Nevada Corporation, Booz Allen Hamilton Inc., and Leidos Holdings, Inc.

HDIN Institutional Verdict and Legal Liabilities

The aggressive transition from hardware assembly to AI-driven prime contracting has fundamentally expanded AeroVironment’s balance sheet risk. Gross goodwill exploded to $2,493.7 million from $256.8 million (BlueHalo added $2,367.4 million; ESAero added $110.2 million). Net intangible assets surged to $929.8 million from $48.7 million, with BlueHalo contributing $1,029.8 million in gross intangibles ($499.5 million in Customer Relationships, $480.4 million in Developed Technology) and ESAero adding $55.3 million.

The Space Segment Anomaly & Due Diligence Exposure

The most severe forensic anomaly is the $240.7 million goodwill impairment recognized in the Space reporting unit. Triggered by a January 2026 U.S. Space Force stop-work order and the March 2026 termination for convenience of the SCAR (Satellite Communication Augmentation Resource) program, the impairment indicates that management paid a heavy M&A premium for un-definitized, high-risk contracts.

This programmatic failure triggered immediate legal contingencies. On May 26, 2026, a securities class action (*Norrell v. AeroVironment, Inc.*) was filed in the U.S. District Court for the Eastern District of Virginia against CEO Wahid Nawabi, former CFO Kevin McDonnell, and Space Segment President Mary Clum, alleging false and materially misleading statements regarding the SCAR program.

Governance and Structural Alignments

Executive compensation strictly tethers management to growth execution. Under the FY2023 Long-Term Incentive Plan (LTIP), 61,605 fully-vested Performance-Based Restricted Stock Units (PRSUs) were issued on August 2, 2025, explicitly linking CEO Wahid Nawabi and CFO Sean T. Woodward’s payouts to specific Revenue and Non-GAAP Adjusted EBITDA thresholds. The Board of Directors—which includes former U.S. DoD executive William J. Lynn III—experienced recent instability when Arlington Capital Partners acquired a 26.3% equity stake via the BlueHalo transaction; the two directors nominated by Arlington subsequently resigned on June 17, 2026.

From a compliance vector, incurred cost claims for Legacy operations are DCAA-audited through FY2024, while BlueHalo is audited through FY2021, holding $0 in active reserves. However, the company is actively executing an internal investigation (initiated February 2026 via external counsel) regarding legacy compliance with DoD cybersecurity mandates (CMMC and SPRS), presenting binary debarment risks if material control failures are validated.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* FY2026 consolidated revenue reached $1,976.8 million (up 141% YoY) backed by a $1,183.0 million funded backlog, though GAAP gross margins collapsed 1,350 basis points to 25.3% amidst aggressive M&A integration.

* Capital deployment targets physical supply chain bottlenecks via a $16.3 million facility acquisition in Huntsville, Alabama, and a new West Valley City, Utah footprint, navigating Chinese rare-earth export sanctions.

* A $240.7 million Space segment goodwill impairment—triggered by a U.S. Space Force stop-work order—exposes acute vulnerabilities to sovereign funding cycles and un-definitized contracting risks.

Figure AeroVironment (AVAV) FY2026 Strategic & Financial Performance Blueprint

Segmental Realities and Financial DiagnosticsAeroVironment, Inc. [NASDAQ: AVAV] fundamentally restructured its P&L in FY2026, transitioning from a tactical hardware manufacturer into a dual-segment defense prime following the $3.48 billion acquisition of BlueHalo (effective May 1, 2025) and the $177.9 million acquisition of ESAero (effective March 2026). While consolidated top-line growth accelerated to 141%, operating leverage deteriorated due to integration friction, structural shifts in services revenue, and acute margin compression.

Of the $1,156.2 million top-line expansion, $939.2 million was inorganic ($526.0 million in products and $413.2 million in services). Stripping out M&A contributions, legacy organic revenue expanded 26.4%, adding $217.0 million ($196.6 million in products, $20.4 million in services) to the FY2025 $820.6 million baseline.

Consolidated Income & Margin Compression Matrix

* Total Revenue: $1,976.8 million in FY2026 vs. $820.6 million in FY2025.

* GAAP Net Income / Loss: Net loss of $(265.1) million vs. Net income of $43.6 million.

* GAAP Gross Margin: 25.3% ($500.6 million) vs. 38.8% ($318.6 million).

* Product Margin: 32.2% ($456.1 million GM on $1,415.3 million revenue) vs. 41.6%.

* Services Margin: 7.9% ($44.5 million GM on $561.5 million revenue) vs. 23.7%.

* Non-GAAP Adjusted EBITDA Margin: 14.5% ($286.1 million) vs. 17.8% ($146.4 million).

* Research & Development (R&D): $127.7 million (6% of revenue) vs. $100.7 million (12% of revenue). Customer-funded R&D generated $240.9 million in revenue against $209.7 million in costs.

* SG&A Expenses: 22% of revenue ($443.2 million).

* M&A & Intangible Amortization: Acquisition expenses totaled $48.1 million. Cost of sales absorbed $92.7 million in non-cash purchase accounting and intangible amortization vs. $19.4 million.

Table Reporting Segment Realities

| Segment | Revenue | YoY Growth | Sub-Segment Breakdown | Profitability |

|---|---|---|---|---|

| Autonomous Systems (AxS) | $1,358.1M | +65% (from $820.6M) | — | — |

| Precision Strike & Defense Systems (PSDS) | $848.3M | +136% (from $359.4M) | Largest growth driver within AxS | — |

| Uncrewed Aircraft Systems (UAS) | $363.9M | +3.4% (from $352.0M) | Stable UAV demand | — |

| Other (MacCready Works, UGV, UUV) | $145.9M | ↑ from $109.2M | Robotics & unmanned diversification | — |

| Space, Cyber & Directed Energy (SCDE) | $618.8M | N/A | Cyber + Space/DE split | $(2.6)M Adj. EBITDA |

| Cyber & Mission Solutions | $345.4M | N/A | Core cyber operations | — |

| Space & Directed Energy | $273.4M | N/A | Space systems + directed energy | — |

Working Capital and Balance Sheet Architecture

Cash Flow from Operations (CFO) contracted to $(78.4) million from $(1.3) million, driven by the operational absorption of $399.3 million in working capital.

* Liquidity & Capital Raise: Following a July 2025 $1.70 billion capital raise (common stock and 0% convertible senior notes), the company allocated $965.3 million to eradicate existing Term Loan and Revolver debt. Total available liquidity sits at $969.1 million ($377.3 million cash and cash equivalents, $255.0 million short-term investments, $336.8 million available revolver capacity).

* Receivables: Accounts receivable consumed $128.7 million, with ending billed AR at $316.2 million. Unbilled receivables and retentions grew 96.7% to $570.4 million from $290.0 million (BlueHalo added $96.4 million, ESAero added $25.0 million, resulting in 54.8% organic growth).

* Inventory Turns: Inventory levels surged to $312.9 million from $144.1 million, triggering a $111.6 million cash outflow. Against $1,476.2 million in Cost of Sales and $228.5 million in average inventory, turns stand at 6.46x (or 4.7x measured against ending inventory).

* Liabilities & Deferred Costs: Deferred revenue (customer advances) expanded to $79.6 million from $16.0 million. Deferred costs to fulfill dropped to $0 from $1.9 million.

Contract Typology & Forward Visibility

The total funded backlog reached $1,183.0 million (up 63% from $726.6 million), with management projecting an 85% conversion rate in FY2027. Unfunded backlog expanded to $1,457.7 million from $774.6 million.

* Firm-Fixed-Price (FFP): $1,384.3 million (70.0% of revenue) vs. $746.2 million (90.9%). A $3.9 million forward loss reserve was recorded on an Integrated Air and Missile Defense (IAMD) contract.

* Cost-Plus-Fee (CPFF, CPIF, CPAF): $454.1 million (23.0% of revenue) vs. $68.0 million (8.3%), growing 567.8% YoY.

* Time-and-Materials (T&M): $138.4 million (7.0% of revenue) vs. $6.5 million (0.8%), growing 2,029.2% YoY.

Infrastructure Layout and Regional Moats

To execute against its backlog and integrate M&A targets, AeroVironment is executing a highly centralized capacity expansion utilizing ISO 9001:2015 and AS9100D certified facilities. Total segment capital expenditures reached $86.2 million ($50.7 million deployed in AxS, $29.3 million in SCDE, $6.0 million in Corporate). Cash used strictly for purchasing property and equipment was $62.5 million, up from $22.8 million.

Geographic Facility Map

* California Core: Simi Valley contains 280,000 square feet of leased space expiring between 2027 and 2030; Moorpark adds 150,000 square feet.

* SCDE & Tech Hubs: Albuquerque, New Mexico operates 200,000 square feet (leases expiring 2028-2034).

* Capital Expansion Execution: Huntsville, Alabama operates a 150,000-square-foot node. In May 2026, the company notified the lessor of its intent to purchase the 100 Quality Circle building in Huntsville for $16.3 million. In December 2025, a new lease was executed for 4387 West 2100 South in West Valley City, Utah.

* Global & Auxiliary Footprint: Stuttgart, Germany (Telerob/UGV) and Hampton Bishop, United Kingdom. Domestic operations span Arlington, Virginia (Corporate HQ), Maryland, Florida, Pennsylvania, Kansas, Colorado, Minnesota, Oklahoma, Texas, and Ohio.

Labor Demographics and Component Vulnerabilities

The enterprise relies on 3,991 full-time and 100 part-time employees. The labor pyramid is heavily skewed toward technical design, featuring 2,366 R&D/Engineering staff (including 208 PhDs) against 637 Operations/Manufacturing personnel (a 3.7 to 1 ratio). G&A encompasses 907 employees, while Sales/Marketing holds 181. A June 11, 2025 agreement in principle settled a 2024 PAGA labor/wage class action (accrued in FY2025).

Supply chain architecture is actively threatened by geopolitical choke points. Sourcing for advanced UAS components, motors, and batteries relies on rare earth metals predominantly refined in China. Following U.S. military sales to Taiwan, China, the Chinese Ministry of Commerce placed AeroVironment on its export control list and imposed direct sanctions in early 2024 and March 2025. Concurrently, the Telerob subsidiary in Germany must navigate the phased 2025 rollout of the EU Artificial Intelligence Act, which classifies critical infrastructure biometric systems as high-risk.

Customer Concentration

The U.S. Government dictates 85% of total revenue. Direct Department of Defense (DoD) contracts constitute 63%, with the U.S. Army comprising 25% and other U.S. agencies comprising 47%. International/Foreign customers (including Foreign Military Sales) generated $556.4 million (28% of revenue), proportionally diluted from 52% strictly due to BlueHalo's domestic concentration.

Competitor Matrix and Intellectual Property

AeroVironment deploys 407 U.S. patents and proprietary AI software (AVACORE and SPOTR-EDGE) to operate within Modular Open Systems Architecture (MOSA) and Sensor Open System Architecture (SOSA) standards. The physical product portfolio spans Switchblade 300, 400, and 600, Blackwing, Red Dragon, Mayhem, the Titan family (Titan 4, Titan SV MPV3, Titan-MS), Freedom Eagle (FE-1), WildCat (DARPA), LOCUST (20-35+ kilowatt laser), BADGER antennas, and AV_Halo/Kinesis software.

Management explicitly identifies the following entities as direct market competitors across its operating vectors:

* UAS: Elbit Systems Ltd., Quantum-Systems, Inc., Redwire Corporation, Teledyne Technologies, Inc., Sierra Nevada Corporation, Lockheed Martin Corporation, The Boeing Company, Textron, Inc., Shield AI, Inc., Northrop Grumman Corporation, Griffon Aerospace, Inc., L3Harris Technologies, Inc., Anduril Industries, Inc., Airbus SE, and Israeli Aircraft Industries.

* Precision Strike: Textron Inc., RTX Corporation, Lockheed Martin Corporation, Anduril Industries, Inc., Aevex Corp., SpektreWorks, Inc., Dragoon Technology LLC, Cummings Aerospace, Inc., Elbit Systems Ltd., and UVision Air Ltd.

* C-UAS & EW: Anduril Industries, Inc., The Boeing Company, Lockheed Martin Corporation, RTX Corporation, DroneShield Limited, SRC Inc., Polaris, Inc., CACI International Inc., Northrop Grumman Corporation, and L3Harris Technologies, Inc.

* SCDE: The Boeing Company, Lockheed Martin Corporation, L3Harris Technologies, Inc., BAE Systems, Inc., nLIGHT, Inc., Epirus, Inc., EO Solutions Corporation, Huntington Ingalls Industries, Inc., RTX Corporation, Thales Group, Anduril Industries, Inc., Sierra Nevada Corporation, Booz Allen Hamilton Inc., and Leidos Holdings, Inc.

HDIN Institutional Verdict and Legal Liabilities

The aggressive transition from hardware assembly to AI-driven prime contracting has fundamentally expanded AeroVironment’s balance sheet risk. Gross goodwill exploded to $2,493.7 million from $256.8 million (BlueHalo added $2,367.4 million; ESAero added $110.2 million). Net intangible assets surged to $929.8 million from $48.7 million, with BlueHalo contributing $1,029.8 million in gross intangibles ($499.5 million in Customer Relationships, $480.4 million in Developed Technology) and ESAero adding $55.3 million.

The Space Segment Anomaly & Due Diligence Exposure

The most severe forensic anomaly is the $240.7 million goodwill impairment recognized in the Space reporting unit. Triggered by a January 2026 U.S. Space Force stop-work order and the March 2026 termination for convenience of the SCAR (Satellite Communication Augmentation Resource) program, the impairment indicates that management paid a heavy M&A premium for un-definitized, high-risk contracts.

This programmatic failure triggered immediate legal contingencies. On May 26, 2026, a securities class action (*Norrell v. AeroVironment, Inc.*) was filed in the U.S. District Court for the Eastern District of Virginia against CEO Wahid Nawabi, former CFO Kevin McDonnell, and Space Segment President Mary Clum, alleging false and materially misleading statements regarding the SCAR program.

Governance and Structural Alignments

Executive compensation strictly tethers management to growth execution. Under the FY2023 Long-Term Incentive Plan (LTIP), 61,605 fully-vested Performance-Based Restricted Stock Units (PRSUs) were issued on August 2, 2025, explicitly linking CEO Wahid Nawabi and CFO Sean T. Woodward’s payouts to specific Revenue and Non-GAAP Adjusted EBITDA thresholds. The Board of Directors—which includes former U.S. DoD executive William J. Lynn III—experienced recent instability when Arlington Capital Partners acquired a 26.3% equity stake via the BlueHalo transaction; the two directors nominated by Arlington subsequently resigned on June 17, 2026.

From a compliance vector, incurred cost claims for Legacy operations are DCAA-audited through FY2024, while BlueHalo is audited through FY2021, holding $0 in active reserves. However, the company is actively executing an internal investigation (initiated February 2026 via external counsel) regarding legacy compliance with DoD cybersecurity mandates (CMMC and SPRS), presenting binary debarment risks if material control failures are validated.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."