Roadzen Inc.: 2026 Capex Realignment Near New Delhi as $20.3M Operating Cash Burn Signals Going Concern Warning

Date : 2026-07-02

Reading : 143

HDIN Executive Takeaways

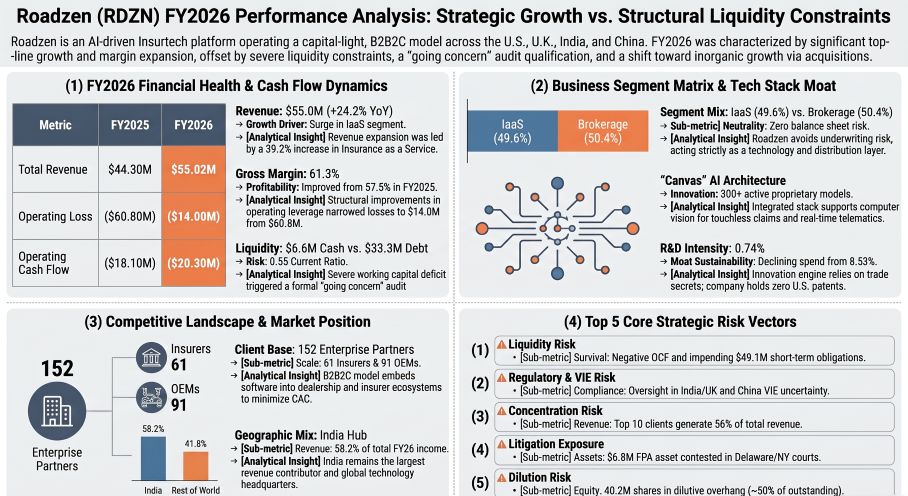

* Roadzen Inc. expanded FY2026 revenue by 24.2% to $55.0 million, achieving a 380-basis point gross margin improvement to 61.3%, counterbalanced by a $20.3 million negative operating cash flow.

* A retroactive consolidation of the Daokang Variable Interest Entity in Beijing and the VehicleCare integration in India masked severe structural liquidity deficits, prompting independent auditors to issue a formal going concern qualification.

* A 40.2 million share derivative overhang and the Meteora Capital Partners litigation concerning a $6.8 million Forward Purchase Agreement introduce catastrophic dilution and balance sheet impairment risks.

Figure Roadzen (RDZN) FY2026 Performance Analysis: Strategic Growth vs Structural Liquidity Constraints

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Roadzen Inc. [NASDAQ: RDZN] executed aggressive top-line expansion in FY2026, scaling total revenue by 24.2% to $55.0 million, up from $44.3 million in FY2025. This growth was structurally bifurcated into two distinct engines. The Insurance as a Service (IaaS) segment recorded a 39.2% expansion, reaching $29.0 million. Concurrently, the Brokerage Solutions and Commission segment posted a 10.9% advance, securing $26.0 million in revenue. This top-line momentum drove a material expansion in gross profitability; the consolidated corporate gross margin expanded by 380 basis points from 57.5% ($18.8 million cost of services) to 61.3% ($21.3 million cost of services).

Operating leverage demonstrated mathematical improvement, though absolute profitability remains deferred. The operating loss compressed from $60.8 million in FY2025 to $14.0 million in FY2026, pushing the operating margin from -137.3% to -25.4%. This shift was largely engineered through a $35.6 million reduction in general and administrative expenses, which settled at $16.0 million. Adjusted EBITDA losses narrowed from $8.4 million to $3.5 million. The net loss attributable to ordinary shareholders contracted 69.1%, from $72.9 million to $22.5 million, culminating in an earnings per share (EPS) of $(0.29). This bottom-line optical improvement was strictly tied to a collapse in recognized stock-based compensation (SBC), which fell from $47.21 million to $497,806. The Board avoided recognizing $139,617 in incremental SBC expense by extending the vesting schedules of 9.5 million unvested Restricted Stock Units (RSUs) to September 17, 2026.

Earnings quality remains heavily compromised by an accelerating cash burn. The $22.5 million net loss translated to a negative operating cash flow (OCF) of $20.3 million, a deterioration from the $18.1 million negative OCF in FY2025, heavily burdened by a $4.0 million working capital deficit. Capital expenditures on property, equipment, and intangible assets scaled from $0.4 million to $1.0 million, yielding a negative free cash flow (FCF) of $21.3 million, compared to a negative FCF of $18.5 million in the prior year. Financing activities injected $21.4 million into the balance sheet.

Balance sheet liquidity metrics indicate systemic distress. Roadzen Inc. holds merely $6.6 million in cash and cash equivalents against $32.3 million in current assets and $58.3 million in current liabilities, resulting in a fractured current ratio of 0.55. The independent auditor, ASA & Associates LLP, issued a formal going concern explanatory paragraph.

* Corporate Tax & Asset Impairment Profile:

* Tax Position: U.S. federal net operating loss (NOL) carryforwards total $42.53 million, driving $42.73 million in deferred tax assets. Management applied a 100% valuation allowance against this asset. Deferred tax liabilities (DTLs) stand at $1.02 million.

* Lease Commitments: Operating lease liabilities register at $1.02 million ($325,255 short-term; $699,817 long-term), aligned against $1.37 million in Right-of-Use (ROU) assets. These are discounted at an exceptionally high 14.80% rate over a weighted average remaining term of 4.42 years.

* Impairments: The company recognized a full impairment charge of $269,470 ($0.27 million), writing down its 6.68% non-marketable equity stake in Moonshot - Internet SAS to zero. In the prior year, $1.19 million in acquired customer contracts were completely written off.

Infrastructure Layout and Regional Moats

The company’s supply chain architecture and revenue distribution are highly fragmented across four international geographies, relying on a localized blend of software ecosystems, human capital, and corporate M&A. Operations target a B2B2C framework supporting 152 enterprise clients (61 insurers, 91 Original Equipment Manufacturers) alongside approximately 4,200 small-to-medium business fleets and agents. Customer concentration risk is acute; the top three clients account for 13.0%, 10.0%, and 8.0% of total revenue respectively (31.0% cumulatively), while the top 10 clients control 56.0% of the total top line. The human capital footprint totals 458 full-time employees, aggressively skewed toward go-to-market functions: 212 in Sales (46.3%), 91 in Operations (19.9%), 86 in Technology (18.8%), 50 in Corporate (10.9%), and 20 in Management (4.4%).

* Regional Market Distribution & M&A Infrastructure:

* India: The primary global hub, generating $32.0 million (58.2% of total revenue) via offices in New Delhi, Ahmedabad, and Chennai. The infrastructure features AutoSpace, managing 1,200 verified repair garages. Inorganic expansion included the $5.41 million acquisition of VehicleCare ($4.52 million equity, $0.89 million cash), which added $3.62 million in goodwill, $3.25 million in intangibles, $0.7 million in revenue, and $0.4 million in costs. The region also executed a $1.44 million asset purchase of an agency relationship with Viaansh, tied to $1.24 million in contingent consideration.

* United States: Generated $11.9 million (21.7% of total revenue) via headquarters in Burlingame and San Diego, maintaining a network of 75,000 service providers. The footprint was augmented by a 55% controlling stake acquisition in EliteCover, valued at $2.39 million ($1.0 million cash, $1.39 million contingent). This added $2.00 million in goodwill, $1.47 million in intangibles, and $1.0 million in revenue.

* United Kingdom & Europe: Generated $6.3 million (11.5% of total revenue), contracting from $9.3 million in FY2025 due to the Financial Conduct Authority (FCA) pausing Guaranteed Asset Protection (GAP) sales. The central hub is an MGA in Coventry.

* People's Republic of China (PRC): Generated $4.7 million (8.6% of total revenue) operating out of Beijing and Shanghai. This was driven by the April 1, 2025 retroactive consolidation of the Daokang VIE. Holding a 34.5% equity stake, Roadzen Inc. utilized a $1.0 million incremental investment to obtain control, triggering a $1.22 million remeasurement of previously held equity. This consolidation added $3.17 million in intangibles, captured a bargain purchase gain of $165,496, and contributed $3.0 million in IaaS revenue against $1.5 million in costs.

Technological defensibility rests on the proprietary Canvas AI platform, supporting over 300 active models. However, actual R&D cash intensity collapsed 89.2%, falling from $3.78 million (8.53% of revenue) in FY2025 to just $0.41 million (0.74% of revenue) in FY2026. This contraction was partially driven by the capitalization of $0.6 million in software development costs. Formal intellectual property is non-existent in the U.S. market (zero U.S. patents), relying instead on nine registered non-U.S. patents, one design patent, five pending applications, and seven registered trademarks.

HDIN Institutional Verdict

The capital structure of Roadzen Inc. is highly engineered, precariously over-leveraged, and characterized by continuous debt defaults and insider stopgap financing. The balance sheet carries aggregate contractual obligations of $65.7 million, demanding $49.1 million to be settled within one year. Total repayable debt obligations sit at $33.3 million. Management was forced to negotiate a definitive amendment with Mizuho to extend the maturity of $11.5 million in Senior Secured Notes to July 7, 2027, stipulating a mandatory refinancing negotiation by September 30, 2026.

To fund its burn rate, the company issued Junior Convertible Notes generating $10.0 million in gross proceeds ($11.11 million principal) at a 14% interest rate (escalating to 18% upon default), with conversion prices set at $2.25 and $3.50. Utilizing a 142.66% volatility assumption, these notes carry a Level 3 fair value of $12.2 million. Additionally, derivative warrant liabilities (including 1.53 million Mizuho shares at a $0.001 exercise price) are valued at $1.98 million. Due to the mathematically anti-dilutive effect of ongoing net losses, Roadzen Inc. excluded an alarming 40,255,123 potential common shares from its diluted EPS calculation—comprising 21,070,282 warrants, 11,071,966 RSUs, and 8,112,875 convertible instruments. Measured against the 79,695,672 ordinary shares currently outstanding, this represents a dormant dilution overhang exceeding 50%. The company recently closed a $7.99 million equity shelf registration in May 2026.

Related-party financial maneuvering remains a core liquidity tactic. CEO Rohan Malhotra's entity, Avacara PTE Ltd. (which holds a 20.8% ownership stake), swapped $0.13 million in debt for 104,000 shares. Insider debt issuance also extended to Director Supurna VedBrat ($500,000) and Krishnan-Shah Family Partners. The CEO's base salary registered at $105,465, adjusting to $120,000 annually as of November 2025.

The inorganic expansion strategy heavily inflated the intangible asset base, sending total goodwill from $2.06 million to $7.61 million, alongside $9.65 million in total intangible assets. This creates immense asset impairment risk if M&A synergies fail to materialize. Furthermore, a $6.8 million Level 3 Forward Purchase Agreement asset is currently facing severe write-down risk as Meteora Capital Partners actively litigates to limit its obligations to $0.9 million.

Regulatory exposure compounds the structural risk profile. Operations are governed by the California Department of Insurance (CDI), the FCA, the Insurance Regulatory and Development Authority of India (IRDAI), and the China Securities Regulatory Commission (CSRC), alongside hardware regulations from the FCC and FMCSA, and environmental directives WEEE and RoHS. Roadzen Inc. faces extreme penalty thresholds under the E.U. GDPR (€20 million or $22.61 million, or 4% of global turnover) and the U.K. equivalent (£17.5 million or $23.09 million), coupled with strict mandates under the CCPA, CPRA, GLBA, and BIPA. Corporate taxation risks in India remain critical; if "Place of Effective Management" rules are triggered by sales exceeding INR 20 million ($229,498), global income faces a 40% tax rate. The company must also navigate global anti-corruption standards under the FCPA and UKBA, alongside admitted historical reporting lapses under India's FEMA regulations.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Roadzen Inc. expanded FY2026 revenue by 24.2% to $55.0 million, achieving a 380-basis point gross margin improvement to 61.3%, counterbalanced by a $20.3 million negative operating cash flow.

* A retroactive consolidation of the Daokang Variable Interest Entity in Beijing and the VehicleCare integration in India masked severe structural liquidity deficits, prompting independent auditors to issue a formal going concern qualification.

* A 40.2 million share derivative overhang and the Meteora Capital Partners litigation concerning a $6.8 million Forward Purchase Agreement introduce catastrophic dilution and balance sheet impairment risks.

Figure Roadzen (RDZN) FY2026 Performance Analysis: Strategic Growth vs Structural Liquidity Constraints

Segmental Realities and Margin CompressionRoadzen Inc. [NASDAQ: RDZN] executed aggressive top-line expansion in FY2026, scaling total revenue by 24.2% to $55.0 million, up from $44.3 million in FY2025. This growth was structurally bifurcated into two distinct engines. The Insurance as a Service (IaaS) segment recorded a 39.2% expansion, reaching $29.0 million. Concurrently, the Brokerage Solutions and Commission segment posted a 10.9% advance, securing $26.0 million in revenue. This top-line momentum drove a material expansion in gross profitability; the consolidated corporate gross margin expanded by 380 basis points from 57.5% ($18.8 million cost of services) to 61.3% ($21.3 million cost of services).

Operating leverage demonstrated mathematical improvement, though absolute profitability remains deferred. The operating loss compressed from $60.8 million in FY2025 to $14.0 million in FY2026, pushing the operating margin from -137.3% to -25.4%. This shift was largely engineered through a $35.6 million reduction in general and administrative expenses, which settled at $16.0 million. Adjusted EBITDA losses narrowed from $8.4 million to $3.5 million. The net loss attributable to ordinary shareholders contracted 69.1%, from $72.9 million to $22.5 million, culminating in an earnings per share (EPS) of $(0.29). This bottom-line optical improvement was strictly tied to a collapse in recognized stock-based compensation (SBC), which fell from $47.21 million to $497,806. The Board avoided recognizing $139,617 in incremental SBC expense by extending the vesting schedules of 9.5 million unvested Restricted Stock Units (RSUs) to September 17, 2026.

Earnings quality remains heavily compromised by an accelerating cash burn. The $22.5 million net loss translated to a negative operating cash flow (OCF) of $20.3 million, a deterioration from the $18.1 million negative OCF in FY2025, heavily burdened by a $4.0 million working capital deficit. Capital expenditures on property, equipment, and intangible assets scaled from $0.4 million to $1.0 million, yielding a negative free cash flow (FCF) of $21.3 million, compared to a negative FCF of $18.5 million in the prior year. Financing activities injected $21.4 million into the balance sheet.

Balance sheet liquidity metrics indicate systemic distress. Roadzen Inc. holds merely $6.6 million in cash and cash equivalents against $32.3 million in current assets and $58.3 million in current liabilities, resulting in a fractured current ratio of 0.55. The independent auditor, ASA & Associates LLP, issued a formal going concern explanatory paragraph.

* Corporate Tax & Asset Impairment Profile:

* Tax Position: U.S. federal net operating loss (NOL) carryforwards total $42.53 million, driving $42.73 million in deferred tax assets. Management applied a 100% valuation allowance against this asset. Deferred tax liabilities (DTLs) stand at $1.02 million.

* Lease Commitments: Operating lease liabilities register at $1.02 million ($325,255 short-term; $699,817 long-term), aligned against $1.37 million in Right-of-Use (ROU) assets. These are discounted at an exceptionally high 14.80% rate over a weighted average remaining term of 4.42 years.

* Impairments: The company recognized a full impairment charge of $269,470 ($0.27 million), writing down its 6.68% non-marketable equity stake in Moonshot - Internet SAS to zero. In the prior year, $1.19 million in acquired customer contracts were completely written off.

Infrastructure Layout and Regional Moats

The company’s supply chain architecture and revenue distribution are highly fragmented across four international geographies, relying on a localized blend of software ecosystems, human capital, and corporate M&A. Operations target a B2B2C framework supporting 152 enterprise clients (61 insurers, 91 Original Equipment Manufacturers) alongside approximately 4,200 small-to-medium business fleets and agents. Customer concentration risk is acute; the top three clients account for 13.0%, 10.0%, and 8.0% of total revenue respectively (31.0% cumulatively), while the top 10 clients control 56.0% of the total top line. The human capital footprint totals 458 full-time employees, aggressively skewed toward go-to-market functions: 212 in Sales (46.3%), 91 in Operations (19.9%), 86 in Technology (18.8%), 50 in Corporate (10.9%), and 20 in Management (4.4%).

* Regional Market Distribution & M&A Infrastructure:

* India: The primary global hub, generating $32.0 million (58.2% of total revenue) via offices in New Delhi, Ahmedabad, and Chennai. The infrastructure features AutoSpace, managing 1,200 verified repair garages. Inorganic expansion included the $5.41 million acquisition of VehicleCare ($4.52 million equity, $0.89 million cash), which added $3.62 million in goodwill, $3.25 million in intangibles, $0.7 million in revenue, and $0.4 million in costs. The region also executed a $1.44 million asset purchase of an agency relationship with Viaansh, tied to $1.24 million in contingent consideration.

* United States: Generated $11.9 million (21.7% of total revenue) via headquarters in Burlingame and San Diego, maintaining a network of 75,000 service providers. The footprint was augmented by a 55% controlling stake acquisition in EliteCover, valued at $2.39 million ($1.0 million cash, $1.39 million contingent). This added $2.00 million in goodwill, $1.47 million in intangibles, and $1.0 million in revenue.

* United Kingdom & Europe: Generated $6.3 million (11.5% of total revenue), contracting from $9.3 million in FY2025 due to the Financial Conduct Authority (FCA) pausing Guaranteed Asset Protection (GAP) sales. The central hub is an MGA in Coventry.

* People's Republic of China (PRC): Generated $4.7 million (8.6% of total revenue) operating out of Beijing and Shanghai. This was driven by the April 1, 2025 retroactive consolidation of the Daokang VIE. Holding a 34.5% equity stake, Roadzen Inc. utilized a $1.0 million incremental investment to obtain control, triggering a $1.22 million remeasurement of previously held equity. This consolidation added $3.17 million in intangibles, captured a bargain purchase gain of $165,496, and contributed $3.0 million in IaaS revenue against $1.5 million in costs.

Technological defensibility rests on the proprietary Canvas AI platform, supporting over 300 active models. However, actual R&D cash intensity collapsed 89.2%, falling from $3.78 million (8.53% of revenue) in FY2025 to just $0.41 million (0.74% of revenue) in FY2026. This contraction was partially driven by the capitalization of $0.6 million in software development costs. Formal intellectual property is non-existent in the U.S. market (zero U.S. patents), relying instead on nine registered non-U.S. patents, one design patent, five pending applications, and seven registered trademarks.

HDIN Institutional Verdict

The capital structure of Roadzen Inc. is highly engineered, precariously over-leveraged, and characterized by continuous debt defaults and insider stopgap financing. The balance sheet carries aggregate contractual obligations of $65.7 million, demanding $49.1 million to be settled within one year. Total repayable debt obligations sit at $33.3 million. Management was forced to negotiate a definitive amendment with Mizuho to extend the maturity of $11.5 million in Senior Secured Notes to July 7, 2027, stipulating a mandatory refinancing negotiation by September 30, 2026.

To fund its burn rate, the company issued Junior Convertible Notes generating $10.0 million in gross proceeds ($11.11 million principal) at a 14% interest rate (escalating to 18% upon default), with conversion prices set at $2.25 and $3.50. Utilizing a 142.66% volatility assumption, these notes carry a Level 3 fair value of $12.2 million. Additionally, derivative warrant liabilities (including 1.53 million Mizuho shares at a $0.001 exercise price) are valued at $1.98 million. Due to the mathematically anti-dilutive effect of ongoing net losses, Roadzen Inc. excluded an alarming 40,255,123 potential common shares from its diluted EPS calculation—comprising 21,070,282 warrants, 11,071,966 RSUs, and 8,112,875 convertible instruments. Measured against the 79,695,672 ordinary shares currently outstanding, this represents a dormant dilution overhang exceeding 50%. The company recently closed a $7.99 million equity shelf registration in May 2026.

Related-party financial maneuvering remains a core liquidity tactic. CEO Rohan Malhotra's entity, Avacara PTE Ltd. (which holds a 20.8% ownership stake), swapped $0.13 million in debt for 104,000 shares. Insider debt issuance also extended to Director Supurna VedBrat ($500,000) and Krishnan-Shah Family Partners. The CEO's base salary registered at $105,465, adjusting to $120,000 annually as of November 2025.

The inorganic expansion strategy heavily inflated the intangible asset base, sending total goodwill from $2.06 million to $7.61 million, alongside $9.65 million in total intangible assets. This creates immense asset impairment risk if M&A synergies fail to materialize. Furthermore, a $6.8 million Level 3 Forward Purchase Agreement asset is currently facing severe write-down risk as Meteora Capital Partners actively litigates to limit its obligations to $0.9 million.

Regulatory exposure compounds the structural risk profile. Operations are governed by the California Department of Insurance (CDI), the FCA, the Insurance Regulatory and Development Authority of India (IRDAI), and the China Securities Regulatory Commission (CSRC), alongside hardware regulations from the FCC and FMCSA, and environmental directives WEEE and RoHS. Roadzen Inc. faces extreme penalty thresholds under the E.U. GDPR (€20 million or $22.61 million, or 4% of global turnover) and the U.K. equivalent (£17.5 million or $23.09 million), coupled with strict mandates under the CCPA, CPRA, GLBA, and BIPA. Corporate taxation risks in India remain critical; if "Place of Effective Management" rules are triggered by sales exceeding INR 20 million ($229,498), global income faces a 40% tax rate. The company must also navigate global anti-corruption standards under the FCPA and UKBA, alongside admitted historical reporting lapses under India's FEMA regulations.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."