Factorial Energy Inc.: Asset-Light Strategy Faces Dilutive Resale Dynamics as 83.5% Trust Redemptions Restructure Capital Runway

Date : 2026-07-06

Reading : 418

HDIN Executive Takeaways

* Cartesian Growth Corporation III [NASDAQ: CGC] merger net cash yields of $92.0 million secure Factorial Energy Inc.'s operational runway to Q1 2028, absorbing an 83.5% redemption rate that drained $240.10 million from the trust account.

* Q1 2026 operational R&D burn declined 71.2% year-over-year to $1.94 million, actively subsidized by $3.4 million in expense reimbursements from Tier-1 automotive joint development partners.

* Management's 80% capital expenditure reduction strategy hinges on a 200 MWh operational baseline in Cheonan, South Korea, establishing a defensive moat against the elimination of U.S. electric vehicle tax credits scheduled for September 2025.

Figure Factorial Energy: Strategic Framework for Solid-State Commercialization

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

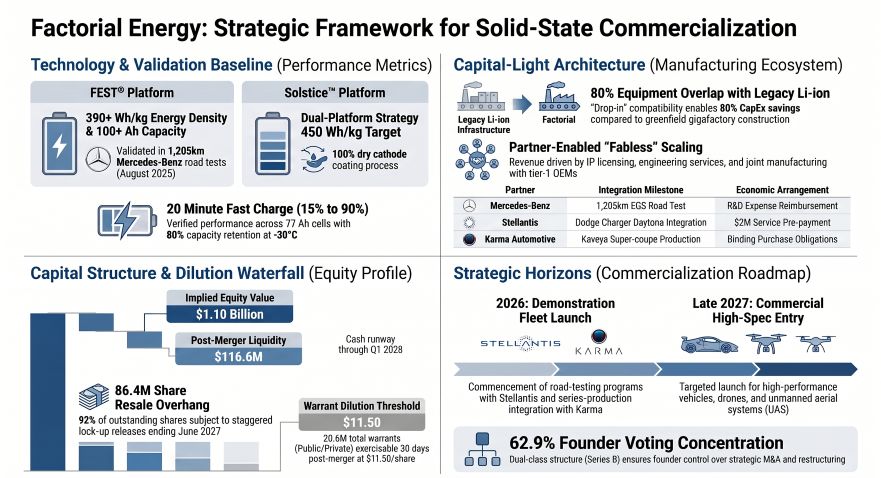

Factorial Energy Inc. executes a pre-revenue, partnership-subsidized balance sheet model resulting in highly compressed optical burn rates. The company closed Q1 2026 with a $2.04 million average monthly cash burn from operating activities (totaling $6.12 million), contracting from an average $2.51 million monthly burn (totaling $30.16 million) in FY 2025. Pre-merger cash equivalents of $25.45 million on March 31, 2026, escalated to $116.6 million in total liquidity by June 10, 2026, following the de-SPAC transaction. This capitalization is modeled to fund planned operations and $7.5 million in projected H2 2026 fabrication line capital expenditures into the first quarter of 2028. The company reported an accumulated deficit of $264.15 million as of March 31, 2026.

Administrative overhead now technically exceeds research and development (R&D) outlays. While gross R&D outpaced selling, general, and administrative (SG&A) expenses in FY 2024 ($31.81 million versus $24.71 million) and FY 2025 ($24.32 million versus $22.20 million), Q1 2026 reported R&D plummeted to $1.94 million against $4.55 million in SG&A. This is entirely a function of $3.4 million in direct Q1 2026 reimbursements from Joint Development Agreement (JDA) partners offsetting gross R&D spend. Mercedes-Benz provided $2.6 million in 2024 and $110,000 in 2025 in expense reimbursements, while Stellantis Europe S.p.A remitted $776,000 in 2024 and $1.185 million in 2025. Mercedes-Benz Corporate Investments LLC and Stellantis Ventures B.V. each additionally hold $2.0 million senior secured convertible promissory notes bearing 15% interest. Conversely, Factorial Energy Inc. prepaid $2.0 million to Stellantis for demonstration fleet testing services.

The baseline transaction economics underwent severe restructuring due to public market withdrawals. The $1.10 billion implied Equity Value merger faced a maximum theoretical gross proceed projection of $385.8 million, comprising $285.87 million in the trust account and $100.0 million in Private Investment in Public Equity (PIPE) financing. Actual gross proceeds totaled $112.06 million ($47.38 million from trust; $64.68 million direct PIPE cash) after 23,051,313 of the 27,600,000 Cartesian Growth Corporation III shares were redeemed. PIPE investors absorbed 3,470,764 public shares in the open market, shifting $36.2 million of their commitment to prevent further trust drain.

Transaction expenses totaled $22.06 million, yielding a final net cash injection of exactly $92.0 million.

De-SPAC Transaction Expense Matrix

* Investment Banking & Underwriting ($9.31 Million Total)

* Cartesian Underwriting Fee: $4.31 million (Paid to Cantor Fitzgerald & Co. via a Fee Modification Agreement, reduced from the original $13.14 million deferred IPO discount).

* Factorial Merger Underwriting Fee: $5.00 million ($2.50 million fixed cash, $1.85 million dynamic cash, $647,000 non-cash Series A Common Stock).

* Legal & Advisory ($12.75 Million Total)

* Factorial Non-Underwriting Costs: $5.26 million ($3.47 million incurred through Q1 2026; $1.79 million incurred at close).

* Cartesian Non-Underwriting Costs: $3.74 million.

* PIPE Financing Costs: $3.75 million.

The company accounts for its physical footprint strictly through operating leases. Factorial Energy Inc. explicitly expenses all R&D costs as incurred, refusing to capitalize its 150+ patent portfolio as intangible assets. Equipment depreciation is straight-lined over 7 to 10 years for machinery, 7 years for building fixtures, 5 years for furniture, 3 years for computing software, and 20 years for buildings (leaseholds amortized over the lesser of the lease term or useful life).

Amortization of Future Undiscounted Operating Lease Obligations

* 2026: $1,994,000

* 2027: $2,053,000

* 2028: $1,546,000

* 2029: $1,308,000

* 2030: $1,348,000

* Thereafter: $2,577,000

* Gross Obligation: $10,826,000

* Imputed Interest: ($2,289,000) at an 8.05% weighted-average discount rate.

* Net Lease Liability Recognized: $8,537,000 ($1,357,000 current; $7,180,000 long-term).

Infrastructure Layout and Regional Moats

Factorial Energy Inc.'s industrial thesis revolves around a "capital-light" fabless drop-in manufacturing capability designed to repurpose underutilized global lithium-ion (Li-ion) capacity. Management asserts the FEST® (Factorial Electrolyte System Technology) platform is engineered to utilize 80% of the equipment found in conventional Li-ion assembly lines, yielding an 80% reduction in upfront capital expenditures versus greenfield construction.

The geographic footprint is anchored by corporate headquarters and R&D within a Billerica, Massachusetts facility operating under a 10-year sublease expiring in October 2032 (with one five-year direct extension option). Prototyping operations occupy a noncancelable Woburn, Massachusetts lease at 19 Presidential Way, amended through April 30, 2028 (a separate two-year Woburn office lease expired in July 2024). Factorial Energy Inc. previously operated a manufacturing site in Methuen, Massachusetts, but recorded a $17.06 million impairment and lease termination loss upon exiting the site in October 2025, a figure inclusive of a $2.0 million cash termination fee. A Tallahassee, Florida R&D site initiated in February 2022 expired at the end of its term in February 2025 without the execution of a three-year extension option. Scale operations are centralized in Cheonan, South Korea, where a 28,000-square-foot facility accommodates up to 200 megawatt-hours (MWh) of production.

The technology portfolio is bifurcated. The FEST® platform utilizes a quasi-solid-state polymer-based electrolyte with a small liquid component, achieving cell energy densities greater than 390 Wh/kg. The Solstice™ platform deploys an all-solid, sulfide-based electrolyte using a dry cathode coating process designed to eliminate solvent-based mixing steps, targeting a 450 Wh/kg limit and thermal stability at 90°C (surpassing the 60°C limit of liquid electrolytes). Export controls classify batteries exceeding 350 Wh/kg as restricted, requiring strict government licensing for export to markets such as China and Singapore. Intellectual property protection spans 9 jurisdictions including the European Patent Office, United Kingdom, Germany, France, Italy, Japan, South Korea, Taiwan, and China.

Third-party validation operates via JDAs with Mercedes-Benz, Stellantis Europe S.p.A, Hyundai/Kia, and PowerCo SE (Volkswagen Group), entities collectively commanding 26% of the 2024 U.S. and European EV market. In August 2025, Mercedes-Benz deployed a lightly modified EQS vehicle utilizing 100+ Ah B-sample solid-state lithium-metal cells for a 1,205 km (748 miles) real-world route from Stuttgart, Germany, to Malmö, Sweden, arriving with 137 km (85 miles) of remaining range. Stellantis testing verified FEST® cells delivering 375 Wh/kg, completing a 15% to 90% fast charge in less than 20 minutes, demonstrating a 4C discharge rate across a -30°C to 45°C window (retaining over 80% capacity at -30°C), and achieving 10C transient loads. Stellantis integrated 77 Ah cells into a Dodge Charger Daytona (STLA Large platform) for a June 2026 road demonstration program.

Commercial volume is governed by February 2026 agreements with Karma Automotive and PowerCo SE. Karma Automotive established binding production purchase obligations contingent on specific key performance indicators for its 1,000+ horsepower Kaveya super-coupe, while PowerCo relies on milestone-based payments tied to technical deliverables. Asian localized supply chains are secured via joint development with POSCO Future M, Philenergy, and SungEel HiTech. Subsidiary entities include Factorial Germany GmbH and Netherlands-based Tulip Tech B.V., alongside unmanned aerial systems (UAS) integration partnerships with KULR Technology Group, Avidrone Aerospace, and JRES.

HDIN Institutional Verdict

Factorial Energy Inc.'s corporate governance mathematically isolates its founders from the incoming dilution wave inherent in its complex equity derivatives structure. Co-founders Dr. Siyu Huang and Dr. Alex Yu hold 100% of the 15,512,744 shares of Series B Common Stock (a 10-to-1 super-voting instrument). Despite holding only 19.1% of the aggregate outstanding shares, the founders wield 62.9% of the total voting power, establishing Nasdaq "controlled company" status.

To execute the 80% equipment overlap strategy and negotiate contract manufacturing against Tier-1 incumbents like QuantumScape, Panasonic, Samsung SDI, CATL, BYD, LG Energy Solution, Tesla, and Toyota, the board deploys 160+ years of legacy experience. Executive Chairman Joseph M. Taylor leverages 34 years at Panasonic Corporation of North America (1983-2017) and historical structuring of the Tesla-Panasonic gigafactory alliance. Director Dieter Zetsche, former CEO of Daimler AG (2006-2019) and Chrysler Group (2000-2005), provides the institutional authority required to enforce JDAs without the benefit of preferential capacity allocation or right-of-first-refusal clauses governing material output.

The equity architecture features an 86,441,489-share registered resale pool. The components break down into 32,812,316 legacy non-founder shares (38.0%), 17,924,907 employee equity awards (20.7%), 15,512,744 legacy founder shares via Series B conversion (17.9%), 7,519,404 PIPE shares (8.7%), 6,800,000 Private Warrants (7.9%), 5,810,000 SPAC Sponsor shares (6.7%), and 62,118 advisory shares allocated to Cantor Fitzgerald & Co. (0.1%).

The company faces a highly structured lock-up restricting 121,936,243 shares (approximately 92% of Series A Common Stock post-merger) on a baseline release schedule: 25% at 180 days, 25% at 270 days, and 50% at the one-year anniversary. However, the schedule integrates volume-weighted average price (VWAP) acceleration triggers based on a 20-day metric: one-third releases at a $12.00 VWAP, one-third at $14.00, and the final one-third at $16.00. The 7,519,404 PIPE investor shares are entirely exempt from this lock-up and achieve liquidity 30 days post-merger upon the filing of the mandated Resale Registration Statement.

Simultaneously, fully exercising outstanding derivative instruments could yield $172.16 million in liquidity, mitigating operating cash needs but aggressively diluting the float. The 13,800,000 Series A Public Warrants ($11.50 exercise) provide $158.70 million and carry a $0.01 forced redemption trigger if the stock trades at or above $18.00 for 20 of 30 days. The 6,800,000 Private Warrants ($11.50 exercise, 30-day transfer lock-up) offer up to $78.2 million. The company reported 19,639,374 outstanding employee options holding a weighted average exercise price of just $1.09 per share (yielding $13.46 million upon full cash exercise) and an additional 5,116,217 outstanding Restricted Stock Units (RSUs) representing pure equity dilution (the resale pool accounts for 13,293,953 of the options and 4,630,954 of the RSUs).

Macroeconomic constraints pose the greatest threat to Factorial Energy Inc.'s late-2027 commercialization timeline. The company operates without locked-in vendor pricing or minimum take-or-pay clauses, rendering its input costs exposed to the U.S. government’s February 2025 and April 2025 import tariffs on Chinese supply chains. Domestically, the July 2025 enactment of the One Big Beautiful Bill Act (OBBBA) eliminated EV tax credits previously authorized by the Inflation Reduction Act. The formal phase-outs—effective September 2025 for passenger EVs and June 2026 for infrastructure—severely threaten OEM end-market demand models exactly as Factorial scales its capacity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Cartesian Growth Corporation III [NASDAQ: CGC] merger net cash yields of $92.0 million secure Factorial Energy Inc.'s operational runway to Q1 2028, absorbing an 83.5% redemption rate that drained $240.10 million from the trust account.

* Q1 2026 operational R&D burn declined 71.2% year-over-year to $1.94 million, actively subsidized by $3.4 million in expense reimbursements from Tier-1 automotive joint development partners.

* Management's 80% capital expenditure reduction strategy hinges on a 200 MWh operational baseline in Cheonan, South Korea, establishing a defensive moat against the elimination of U.S. electric vehicle tax credits scheduled for September 2025.

Figure Factorial Energy: Strategic Framework for Solid-State Commercialization

Segmental Realities and Margin CompressionFactorial Energy Inc. executes a pre-revenue, partnership-subsidized balance sheet model resulting in highly compressed optical burn rates. The company closed Q1 2026 with a $2.04 million average monthly cash burn from operating activities (totaling $6.12 million), contracting from an average $2.51 million monthly burn (totaling $30.16 million) in FY 2025. Pre-merger cash equivalents of $25.45 million on March 31, 2026, escalated to $116.6 million in total liquidity by June 10, 2026, following the de-SPAC transaction. This capitalization is modeled to fund planned operations and $7.5 million in projected H2 2026 fabrication line capital expenditures into the first quarter of 2028. The company reported an accumulated deficit of $264.15 million as of March 31, 2026.

Administrative overhead now technically exceeds research and development (R&D) outlays. While gross R&D outpaced selling, general, and administrative (SG&A) expenses in FY 2024 ($31.81 million versus $24.71 million) and FY 2025 ($24.32 million versus $22.20 million), Q1 2026 reported R&D plummeted to $1.94 million against $4.55 million in SG&A. This is entirely a function of $3.4 million in direct Q1 2026 reimbursements from Joint Development Agreement (JDA) partners offsetting gross R&D spend. Mercedes-Benz provided $2.6 million in 2024 and $110,000 in 2025 in expense reimbursements, while Stellantis Europe S.p.A remitted $776,000 in 2024 and $1.185 million in 2025. Mercedes-Benz Corporate Investments LLC and Stellantis Ventures B.V. each additionally hold $2.0 million senior secured convertible promissory notes bearing 15% interest. Conversely, Factorial Energy Inc. prepaid $2.0 million to Stellantis for demonstration fleet testing services.

The baseline transaction economics underwent severe restructuring due to public market withdrawals. The $1.10 billion implied Equity Value merger faced a maximum theoretical gross proceed projection of $385.8 million, comprising $285.87 million in the trust account and $100.0 million in Private Investment in Public Equity (PIPE) financing. Actual gross proceeds totaled $112.06 million ($47.38 million from trust; $64.68 million direct PIPE cash) after 23,051,313 of the 27,600,000 Cartesian Growth Corporation III shares were redeemed. PIPE investors absorbed 3,470,764 public shares in the open market, shifting $36.2 million of their commitment to prevent further trust drain.

Transaction expenses totaled $22.06 million, yielding a final net cash injection of exactly $92.0 million.

De-SPAC Transaction Expense Matrix

* Investment Banking & Underwriting ($9.31 Million Total)

* Cartesian Underwriting Fee: $4.31 million (Paid to Cantor Fitzgerald & Co. via a Fee Modification Agreement, reduced from the original $13.14 million deferred IPO discount).

* Factorial Merger Underwriting Fee: $5.00 million ($2.50 million fixed cash, $1.85 million dynamic cash, $647,000 non-cash Series A Common Stock).

* Legal & Advisory ($12.75 Million Total)

* Factorial Non-Underwriting Costs: $5.26 million ($3.47 million incurred through Q1 2026; $1.79 million incurred at close).

* Cartesian Non-Underwriting Costs: $3.74 million.

* PIPE Financing Costs: $3.75 million.

The company accounts for its physical footprint strictly through operating leases. Factorial Energy Inc. explicitly expenses all R&D costs as incurred, refusing to capitalize its 150+ patent portfolio as intangible assets. Equipment depreciation is straight-lined over 7 to 10 years for machinery, 7 years for building fixtures, 5 years for furniture, 3 years for computing software, and 20 years for buildings (leaseholds amortized over the lesser of the lease term or useful life).

Amortization of Future Undiscounted Operating Lease Obligations

* 2026: $1,994,000

* 2027: $2,053,000

* 2028: $1,546,000

* 2029: $1,308,000

* 2030: $1,348,000

* Thereafter: $2,577,000

* Gross Obligation: $10,826,000

* Imputed Interest: ($2,289,000) at an 8.05% weighted-average discount rate.

* Net Lease Liability Recognized: $8,537,000 ($1,357,000 current; $7,180,000 long-term).

Infrastructure Layout and Regional Moats

Factorial Energy Inc.'s industrial thesis revolves around a "capital-light" fabless drop-in manufacturing capability designed to repurpose underutilized global lithium-ion (Li-ion) capacity. Management asserts the FEST® (Factorial Electrolyte System Technology) platform is engineered to utilize 80% of the equipment found in conventional Li-ion assembly lines, yielding an 80% reduction in upfront capital expenditures versus greenfield construction.

The geographic footprint is anchored by corporate headquarters and R&D within a Billerica, Massachusetts facility operating under a 10-year sublease expiring in October 2032 (with one five-year direct extension option). Prototyping operations occupy a noncancelable Woburn, Massachusetts lease at 19 Presidential Way, amended through April 30, 2028 (a separate two-year Woburn office lease expired in July 2024). Factorial Energy Inc. previously operated a manufacturing site in Methuen, Massachusetts, but recorded a $17.06 million impairment and lease termination loss upon exiting the site in October 2025, a figure inclusive of a $2.0 million cash termination fee. A Tallahassee, Florida R&D site initiated in February 2022 expired at the end of its term in February 2025 without the execution of a three-year extension option. Scale operations are centralized in Cheonan, South Korea, where a 28,000-square-foot facility accommodates up to 200 megawatt-hours (MWh) of production.

The technology portfolio is bifurcated. The FEST® platform utilizes a quasi-solid-state polymer-based electrolyte with a small liquid component, achieving cell energy densities greater than 390 Wh/kg. The Solstice™ platform deploys an all-solid, sulfide-based electrolyte using a dry cathode coating process designed to eliminate solvent-based mixing steps, targeting a 450 Wh/kg limit and thermal stability at 90°C (surpassing the 60°C limit of liquid electrolytes). Export controls classify batteries exceeding 350 Wh/kg as restricted, requiring strict government licensing for export to markets such as China and Singapore. Intellectual property protection spans 9 jurisdictions including the European Patent Office, United Kingdom, Germany, France, Italy, Japan, South Korea, Taiwan, and China.

Third-party validation operates via JDAs with Mercedes-Benz, Stellantis Europe S.p.A, Hyundai/Kia, and PowerCo SE (Volkswagen Group), entities collectively commanding 26% of the 2024 U.S. and European EV market. In August 2025, Mercedes-Benz deployed a lightly modified EQS vehicle utilizing 100+ Ah B-sample solid-state lithium-metal cells for a 1,205 km (748 miles) real-world route from Stuttgart, Germany, to Malmö, Sweden, arriving with 137 km (85 miles) of remaining range. Stellantis testing verified FEST® cells delivering 375 Wh/kg, completing a 15% to 90% fast charge in less than 20 minutes, demonstrating a 4C discharge rate across a -30°C to 45°C window (retaining over 80% capacity at -30°C), and achieving 10C transient loads. Stellantis integrated 77 Ah cells into a Dodge Charger Daytona (STLA Large platform) for a June 2026 road demonstration program.

Commercial volume is governed by February 2026 agreements with Karma Automotive and PowerCo SE. Karma Automotive established binding production purchase obligations contingent on specific key performance indicators for its 1,000+ horsepower Kaveya super-coupe, while PowerCo relies on milestone-based payments tied to technical deliverables. Asian localized supply chains are secured via joint development with POSCO Future M, Philenergy, and SungEel HiTech. Subsidiary entities include Factorial Germany GmbH and Netherlands-based Tulip Tech B.V., alongside unmanned aerial systems (UAS) integration partnerships with KULR Technology Group, Avidrone Aerospace, and JRES.

HDIN Institutional Verdict

Factorial Energy Inc.'s corporate governance mathematically isolates its founders from the incoming dilution wave inherent in its complex equity derivatives structure. Co-founders Dr. Siyu Huang and Dr. Alex Yu hold 100% of the 15,512,744 shares of Series B Common Stock (a 10-to-1 super-voting instrument). Despite holding only 19.1% of the aggregate outstanding shares, the founders wield 62.9% of the total voting power, establishing Nasdaq "controlled company" status.

To execute the 80% equipment overlap strategy and negotiate contract manufacturing against Tier-1 incumbents like QuantumScape, Panasonic, Samsung SDI, CATL, BYD, LG Energy Solution, Tesla, and Toyota, the board deploys 160+ years of legacy experience. Executive Chairman Joseph M. Taylor leverages 34 years at Panasonic Corporation of North America (1983-2017) and historical structuring of the Tesla-Panasonic gigafactory alliance. Director Dieter Zetsche, former CEO of Daimler AG (2006-2019) and Chrysler Group (2000-2005), provides the institutional authority required to enforce JDAs without the benefit of preferential capacity allocation or right-of-first-refusal clauses governing material output.

The equity architecture features an 86,441,489-share registered resale pool. The components break down into 32,812,316 legacy non-founder shares (38.0%), 17,924,907 employee equity awards (20.7%), 15,512,744 legacy founder shares via Series B conversion (17.9%), 7,519,404 PIPE shares (8.7%), 6,800,000 Private Warrants (7.9%), 5,810,000 SPAC Sponsor shares (6.7%), and 62,118 advisory shares allocated to Cantor Fitzgerald & Co. (0.1%).

The company faces a highly structured lock-up restricting 121,936,243 shares (approximately 92% of Series A Common Stock post-merger) on a baseline release schedule: 25% at 180 days, 25% at 270 days, and 50% at the one-year anniversary. However, the schedule integrates volume-weighted average price (VWAP) acceleration triggers based on a 20-day metric: one-third releases at a $12.00 VWAP, one-third at $14.00, and the final one-third at $16.00. The 7,519,404 PIPE investor shares are entirely exempt from this lock-up and achieve liquidity 30 days post-merger upon the filing of the mandated Resale Registration Statement.

Simultaneously, fully exercising outstanding derivative instruments could yield $172.16 million in liquidity, mitigating operating cash needs but aggressively diluting the float. The 13,800,000 Series A Public Warrants ($11.50 exercise) provide $158.70 million and carry a $0.01 forced redemption trigger if the stock trades at or above $18.00 for 20 of 30 days. The 6,800,000 Private Warrants ($11.50 exercise, 30-day transfer lock-up) offer up to $78.2 million. The company reported 19,639,374 outstanding employee options holding a weighted average exercise price of just $1.09 per share (yielding $13.46 million upon full cash exercise) and an additional 5,116,217 outstanding Restricted Stock Units (RSUs) representing pure equity dilution (the resale pool accounts for 13,293,953 of the options and 4,630,954 of the RSUs).

Macroeconomic constraints pose the greatest threat to Factorial Energy Inc.'s late-2027 commercialization timeline. The company operates without locked-in vendor pricing or minimum take-or-pay clauses, rendering its input costs exposed to the U.S. government’s February 2025 and April 2025 import tariffs on Chinese supply chains. Domestically, the July 2025 enactment of the One Big Beautiful Bill Act (OBBBA) eliminated EV tax credits previously authorized by the Inflation Reduction Act. The formal phase-outs—effective September 2025 for passenger EVs and June 2026 for infrastructure—severely threaten OEM end-market demand models exactly as Factorial scales its capacity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*