Tongchuang Purun: $208.70M Capex Realignment Near Harbin and Lishui as 82.67% Aluminum Utilization Signals Immediate Production Capacity Pivot

Date : 2026-07-06

Reading : 114

HDIN Executive Takeaways

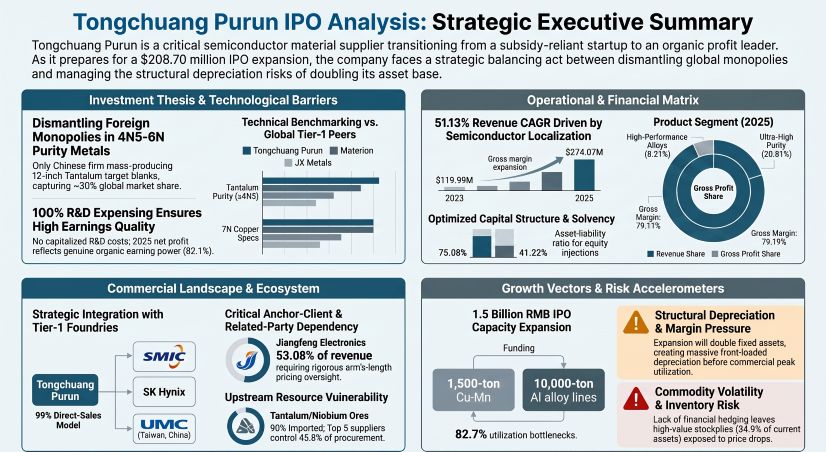

* Operating revenue expanded at a 51.13% compound annual growth rate (CAGR) to $274.07 million in 2025, driven by ultra-high purity Tantalum capturing 30% of the global market share and reducing reliance on state subsidies from 33.0% of net profits in 2024 to 17.9% in 2025.

* The $208.70 million (1.5 billion RMB) capital expenditure schedule across Harbin, Lishui, and Yiyang introduces severe near-term margin pressure, utilizing a 36-month timeline that will double the fixed asset base and accelerate straight-line depreciation.

* Institutional risk remains concentrated as related-party transactions with anchor client Jiangfeng Electronics accounted for 53.08% of 2025 revenue, alongside ongoing intellectual property litigation with Orient Tantalum involving 39 million RMB in frozen assets.

Figure Tongchuang Purun lPO Analysis: Strategic Executive Summary

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Tongchuang Purun [TCPR] executed a structural turnaround, pivoting from a net loss of -$5.79 million in 2023 to a net profit of $24.86 million in 2025. Consolidated gross margins expanded by 787 basis points across the reporting period, driven by the optimization of its product mix toward semiconductor-grade materials. The company's organic earning power (Core Net Profit) reached 82.1% of total net profits in 2025.

Government subsidies totaled $2.76 million in 2023, $2.41 million in 2024, and $4.42 million in 2025. Capital occupation fees generated $3.08 million in 2023. Multiple subsidiaries benefit from a 15% High-Tech Enterprise (HNTE) tax rate and a 5% VAT deduction. An HDIN stress test simulating a 50% subsidy cut indicates a net margin deterioration of 1.15 percentage points in 2023 (to -5.98%), 0.57 percentage points in 2024 (to 4.74%), and 0.81 percentage points in 2025 (to 8.26%).

Table 1: Financial & Profitability Matrix (2023–2025)

The company's revenue architecture relies on two distinct product pipelines. Ultra-High Purity Metal Materials (4N5-6N Ta, 7N Cu, 6N Al, 5N Mn) scaled from $36.77 million (31.61% of total) in 2023 to $121.52 million (46.65%) in 2025. Tantalum alone generated $99.62 million in 2025. This segment generated $43.39 million in gross profit in 2025 (79.19% of total), commanding a 35.71% margin. The High-Performance Metal Materials segment (Al & Ta/Nb alloys) grew from $79.55 million (68.39%) to $138.98 million (53.35%), with Aluminum contributing $79.73 million in 2025. Gross margins in this volume segment improved from 1.28% to 8.21%, generating $11.41 million in 2025 profit.

Geographical revenue distribution reflects aggressive domestic localization. Domestic revenue scaled from $56.30 million (48.40%) to $181.55 million (69.69%), while international revenue grew in absolute terms from $60.02 million to $78.96 million, though its relative share contracted from 51.60% to 30.31%.

Table 2: Inventory & Working Capital Architecture (2023–2025)

Inventory balances reached $123.42 million (34.94% of total current assets) in 2025. Dispatched goods accounted for $5.02 million (4.06%) at the end of 2025. The company's inventory provision rate of 1.44% tracks below the 2.26% industry average but aligns with normalized Tier-1 peers such as Sirui New Materials (0.65%-1.54%) and Xinjiang Joinworld (0.73%-0.90%), differing from structurally inefficient peers like Orient Tantalum (3.02%-6.40%) and GRIAM (1.72%-8.21%). Accounts Receivable (AR) aging remains below one year for 96.84% of balances in 2025 (96.54% in 2023; 97.29% in 2024), while AR turnover improved from 3.36x to 4.56x.

Infrastructure Layout and Regional Moats

The corporate balance sheet completed a massive asset conversion cycle. Construction in Progress (CIP) plummeted 83% from $28.24 million (202.97 million RMB) in 2024 to $4.74 million (34.09 million RMB) in 2025. This directly corresponded to the commissioning of the Harbin Longjiang Scholar Pioneer Park / Electronic Material Industrialization Project (Phase I), which drove Fixed Assets to $158.73 million (114,084.00 million RMB) by year-end 2025, up from $96.81 million in 2023. Cash liquidity reached $118.96 million. Consequently, the Current Ratio improved from 1.21x to 2.81x, the Quick Ratio from 0.77x to 1.83x, and the gearing ratio contracted from 75.08% to 41.22%.

The company operates a strict "make-to-order + reasonable stocking" model. Production is distributed across Shanghai Jidian and Shanghai Tecai (Huancheng North Road), Lishui Tongchuang (Lisha Road), Hunan Tongchuang (Henglong New Area Industrial Park), Harbin Tongchuang (Zhigu 2nd Street), Ningbo Chuangzhi, Ningbo Weitai, and Ningbo Tongchuang (Yuyao), alongside the MKN Aluminum subsidiary in Joetsu, Niigata, Japan (acquired from Mitsubishi Chemical).

Table 3: 2025 Capacity & Output Utilization Ledger

To address capacity constraints (notably the 82.67% Aluminum utilization), the proposed $208.70 million (1.5 billion RMB) IPO expansion utilizes a 36-month ramp cycle (Months 1-12 engineering; 13-24 installation; 25-30 trial; 31-36 commercialization). Machinery will depreciate straight-line over 3-10 years with a 5% salvage value, requiring a >70% utilization rate to offset margin drags.

Capital Expenditure Pipeline Matrix:

* Project 1: High-Purity Tantalum R&D/Industrialization: $61.68 million (443.33 million RMB) total. Includes Sub-project A ($13.37 million) at Hunan Tongchuang in Yiyang for Ta powder/Nb-Ta alloy (EIA: Xiang Huan Xu Jue No. 190; NDRC: 2508-430903-04-01-461565). Sub-project B ($48.31 million / also reported as $49.82 million in initial filings) at Lishui Tongchuang (EIA: Li Huan Jian Kai No. 17; NDRC: 2511-331151-04-01-883526).

* Project 2: Advanced Metal Material Industrialization: $91.82 million (659.99 million RMB) total, though initially filed jointly at $108.09 million. Includes Sub-project A ($67.81 million) for 1,500-ton Cu-Mn alloy and Sub-project B ($24.01 million) for 10,000-ton Al alloy at Harbin Tongchuang via Harbin New Area New Material Industrial Park (EIA: Ha Xin Shen Huan Shen Biao No. 8; NDRC: 2603-230109-04-03-499715).

* Project 3: R&D Center Upgrade: $16.17 million (116.24 million RMB) targeting 5N Chromium (Cr) powder.

* Project 4: Supplemental Working Capital: $39.02 million (280.43 million RMB).

HDIN Institutional Verdict

Tongchuang Purun [TCPR] operates a highly concentrated direct-sales (99.21% in 2025) and upstream procurement model. Its top five clients accounted for 71.06% ($85.27 million) of revenue in 2023, 84.15% ($180.62 million) in 2024, and 81.90% ($224.47 million) in 2025. Related-party transactions with Jiangfeng Electronics represent the primary governance vulnerability, accounting for 36.84% ($44.21 million), 53.58% ($82.68 million), and 53.08% ($145.47 million) of sales across the three-year period. Other top clients include Yanling Jincheng (12.47%) and Japan BBS (9.77%), ultimately supplying wafer fabs such as SMIC [SHA: 688981], UMC [NYSE: UMC / TWSE: 2303], SK Hynix, and Micron. Upstream, the top five suppliers accounted for 45.84% ($106.75 million) of 2025 procurement, led by Ximei Resources (13.89%) and Itochu Corporation (11.03%).

The technical moat is validated by raw material benchmarks matching or beating global competitors like JX Metals, Materion, Sumitomo Chemical, and Norsk Hydro. The company's Tantalum achieves ≥4N5 purity (vs. Materion's ≥4N), with Tungsten impurities <15ppm (vs. <50ppm), grain sizes ≤80μm (vs. ≤100μm), and ingot diameters ≥240mm (vs. ≤200mm). Aluminum Iron impurities hit ≤0.5ppm (vs. Norsk Hydro ≤1ppm) with alkali metals ≤0.5ppm. Copper achieves Silver impurities of 0.02-0.2ppm and Sulfur <0.01ppm. Consequently, the company holds a 30% global market share in Tantalum, alongside a 24% domestic share in Copper and 27% in Aluminum, competing with domestic peers like GRI Composites and Youyan Yijin.

Research and Development accounting is 100% expensed. Expenditures scaled from $6.36 million to $12.83 million, totaling $27.80 million (19,981.79 万元) at a 41.98% CAGR. 2025 R&D allocations include Material Costs at $9.17 million (71.51%), Personnel at $2.10 million (16.36%), D&A at $0.62 million (4.84%), Fuel at $0.60 million (4.69%), and Testing at $0.33 million (2.59%). The company holds 83 authorized patents (28 invention, 55 utility) and 11 software copyrights. A forensic flag remains on 5 invention patents and 11 software copyrights transferred in 2021-2022 to meet HNTE certification thresholds.

Corporate control rests with Chairman Dr. Yao Lijun (14.72% direct, 19.12% via 12 concerted entities including employee platforms Ningbo Hongxin and Ningbo Xinju, plus executives Mao Jian and Li Guipeng, totaling 33.84%). Technical leadership relies heavily on Dr. WUWEN YI. Institutional backers include CNBM Fund (5.40%), ICBC Investment (3.60%), and Shenzhen Capital Group (0.36%). Alignment is enforced by share-based compensation totaling $20.11 million, $19.86 million, and $14.44 million over three years. Near-term risks remain anchored to pending litigation with Orient Tantalum, involving 39 million RMB in frozen assets at Lishui Tongchuang, counterbalanced by a 50 million RMB defamation claim and two 3 million RMB malicious litigation suits.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Operating revenue expanded at a 51.13% compound annual growth rate (CAGR) to $274.07 million in 2025, driven by ultra-high purity Tantalum capturing 30% of the global market share and reducing reliance on state subsidies from 33.0% of net profits in 2024 to 17.9% in 2025.

* The $208.70 million (1.5 billion RMB) capital expenditure schedule across Harbin, Lishui, and Yiyang introduces severe near-term margin pressure, utilizing a 36-month timeline that will double the fixed asset base and accelerate straight-line depreciation.

* Institutional risk remains concentrated as related-party transactions with anchor client Jiangfeng Electronics accounted for 53.08% of 2025 revenue, alongside ongoing intellectual property litigation with Orient Tantalum involving 39 million RMB in frozen assets.

Figure Tongchuang Purun lPO Analysis: Strategic Executive Summary

Segmental Realities and Margin CompressionTongchuang Purun [TCPR] executed a structural turnaround, pivoting from a net loss of -$5.79 million in 2023 to a net profit of $24.86 million in 2025. Consolidated gross margins expanded by 787 basis points across the reporting period, driven by the optimization of its product mix toward semiconductor-grade materials. The company's organic earning power (Core Net Profit) reached 82.1% of total net profits in 2025.

Government subsidies totaled $2.76 million in 2023, $2.41 million in 2024, and $4.42 million in 2025. Capital occupation fees generated $3.08 million in 2023. Multiple subsidiaries benefit from a 15% High-Tech Enterprise (HNTE) tax rate and a 5% VAT deduction. An HDIN stress test simulating a 50% subsidy cut indicates a net margin deterioration of 1.15 percentage points in 2023 (to -5.98%), 0.57 percentage points in 2024 (to 4.74%), and 0.81 percentage points in 2025 (to 8.26%).

Table 1: Financial & Profitability Matrix (2023–2025)

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Operating Revenue | $119.99M | $214.65M | $274.07M |

| Gross Margin | 13.44% | 20.19% | 21.31% |

| Total Net Profit | $(5.79M) | $11.39M | $24.86M |

| Core Net Profit | $(10.33M) | $7.63M | $20.40M |

| Return on Equity (ROE) | -5.10% | N/A | 10.87% |

| Operating Cash Flow (OCF) | N/A | N/A | $(7.11M) |

The company's revenue architecture relies on two distinct product pipelines. Ultra-High Purity Metal Materials (4N5-6N Ta, 7N Cu, 6N Al, 5N Mn) scaled from $36.77 million (31.61% of total) in 2023 to $121.52 million (46.65%) in 2025. Tantalum alone generated $99.62 million in 2025. This segment generated $43.39 million in gross profit in 2025 (79.19% of total), commanding a 35.71% margin. The High-Performance Metal Materials segment (Al & Ta/Nb alloys) grew from $79.55 million (68.39%) to $138.98 million (53.35%), with Aluminum contributing $79.73 million in 2025. Gross margins in this volume segment improved from 1.28% to 8.21%, generating $11.41 million in 2025 profit.

Geographical revenue distribution reflects aggressive domestic localization. Domestic revenue scaled from $56.30 million (48.40%) to $181.55 million (69.69%), while international revenue grew in absolute terms from $60.02 million to $78.96 million, though its relative share contracted from 51.60% to 30.31%.

Table 2: Inventory & Working Capital Architecture (2023–2025)

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Total Inventory Book Value | $92.80M | $94.11M | $123.42M |

| Raw Materials (Value / % of Total) | $14.51M / 15.63% | $19.99M / 21.24% | $29.71M / 24.07% |

| Work-in-Progress (Value / % of Total) | $65.22M / 70.29% | $57.97M / 61.60% | $67.25M / 54.49% |

| Finished Goods (Value / % of Total) | $11.37M / 12.26% | $15.56M / 16.54% | $19.11M / 15.48% |

| Inventory Provisions (Value / Provision Rate) | $2.12M / 2.23% | $1.40M / 1.46% | $1.81M / 1.44% |

| Inventory Turnover Rate | 1.09× | N/A | 1.95× |

Inventory balances reached $123.42 million (34.94% of total current assets) in 2025. Dispatched goods accounted for $5.02 million (4.06%) at the end of 2025. The company's inventory provision rate of 1.44% tracks below the 2.26% industry average but aligns with normalized Tier-1 peers such as Sirui New Materials (0.65%-1.54%) and Xinjiang Joinworld (0.73%-0.90%), differing from structurally inefficient peers like Orient Tantalum (3.02%-6.40%) and GRIAM (1.72%-8.21%). Accounts Receivable (AR) aging remains below one year for 96.84% of balances in 2025 (96.54% in 2023; 97.29% in 2024), while AR turnover improved from 3.36x to 4.56x.

Infrastructure Layout and Regional Moats

The corporate balance sheet completed a massive asset conversion cycle. Construction in Progress (CIP) plummeted 83% from $28.24 million (202.97 million RMB) in 2024 to $4.74 million (34.09 million RMB) in 2025. This directly corresponded to the commissioning of the Harbin Longjiang Scholar Pioneer Park / Electronic Material Industrialization Project (Phase I), which drove Fixed Assets to $158.73 million (114,084.00 million RMB) by year-end 2025, up from $96.81 million in 2023. Cash liquidity reached $118.96 million. Consequently, the Current Ratio improved from 1.21x to 2.81x, the Quick Ratio from 0.77x to 1.83x, and the gearing ratio contracted from 75.08% to 41.22%.

The company operates a strict "make-to-order + reasonable stocking" model. Production is distributed across Shanghai Jidian and Shanghai Tecai (Huancheng North Road), Lishui Tongchuang (Lisha Road), Hunan Tongchuang (Henglong New Area Industrial Park), Harbin Tongchuang (Zhigu 2nd Street), Ningbo Chuangzhi, Ningbo Weitai, and Ningbo Tongchuang (Yuyao), alongside the MKN Aluminum subsidiary in Joetsu, Niigata, Japan (acquired from Mitsubishi Chemical).

Table 3: 2025 Capacity & Output Utilization Ledger

2025 Capacity & Output Utilization Ledger

| Product | Nameplate Capacity | Actual Output | Utilization Rate |

|---|---|---|---|

| Ultra-High Purity Tantalum (Ta) | 12,000 PCS | 8,831 PCS | 73.59% |

| Ultra-High Purity Aluminum (Al) | 405.00 Tons | 334.82 Tons | 82.67% |

| Ultra-High Purity Copper (Cu) | 972.80 Tons | 609.85 Tons | 62.69% |

| High-Performance Aluminum Alloys | 33,051.30 Tons | 23,414.30 Tons | 70.84% |

To address capacity constraints (notably the 82.67% Aluminum utilization), the proposed $208.70 million (1.5 billion RMB) IPO expansion utilizes a 36-month ramp cycle (Months 1-12 engineering; 13-24 installation; 25-30 trial; 31-36 commercialization). Machinery will depreciate straight-line over 3-10 years with a 5% salvage value, requiring a >70% utilization rate to offset margin drags.

Capital Expenditure Pipeline Matrix:

* Project 1: High-Purity Tantalum R&D/Industrialization: $61.68 million (443.33 million RMB) total. Includes Sub-project A ($13.37 million) at Hunan Tongchuang in Yiyang for Ta powder/Nb-Ta alloy (EIA: Xiang Huan Xu Jue No. 190; NDRC: 2508-430903-04-01-461565). Sub-project B ($48.31 million / also reported as $49.82 million in initial filings) at Lishui Tongchuang (EIA: Li Huan Jian Kai No. 17; NDRC: 2511-331151-04-01-883526).

* Project 2: Advanced Metal Material Industrialization: $91.82 million (659.99 million RMB) total, though initially filed jointly at $108.09 million. Includes Sub-project A ($67.81 million) for 1,500-ton Cu-Mn alloy and Sub-project B ($24.01 million) for 10,000-ton Al alloy at Harbin Tongchuang via Harbin New Area New Material Industrial Park (EIA: Ha Xin Shen Huan Shen Biao No. 8; NDRC: 2603-230109-04-03-499715).

* Project 3: R&D Center Upgrade: $16.17 million (116.24 million RMB) targeting 5N Chromium (Cr) powder.

* Project 4: Supplemental Working Capital: $39.02 million (280.43 million RMB).

HDIN Institutional Verdict

Tongchuang Purun [TCPR] operates a highly concentrated direct-sales (99.21% in 2025) and upstream procurement model. Its top five clients accounted for 71.06% ($85.27 million) of revenue in 2023, 84.15% ($180.62 million) in 2024, and 81.90% ($224.47 million) in 2025. Related-party transactions with Jiangfeng Electronics represent the primary governance vulnerability, accounting for 36.84% ($44.21 million), 53.58% ($82.68 million), and 53.08% ($145.47 million) of sales across the three-year period. Other top clients include Yanling Jincheng (12.47%) and Japan BBS (9.77%), ultimately supplying wafer fabs such as SMIC [SHA: 688981], UMC [NYSE: UMC / TWSE: 2303], SK Hynix, and Micron. Upstream, the top five suppliers accounted for 45.84% ($106.75 million) of 2025 procurement, led by Ximei Resources (13.89%) and Itochu Corporation (11.03%).

The technical moat is validated by raw material benchmarks matching or beating global competitors like JX Metals, Materion, Sumitomo Chemical, and Norsk Hydro. The company's Tantalum achieves ≥4N5 purity (vs. Materion's ≥4N), with Tungsten impurities <15ppm (vs. <50ppm), grain sizes ≤80μm (vs. ≤100μm), and ingot diameters ≥240mm (vs. ≤200mm). Aluminum Iron impurities hit ≤0.5ppm (vs. Norsk Hydro ≤1ppm) with alkali metals ≤0.5ppm. Copper achieves Silver impurities of 0.02-0.2ppm and Sulfur <0.01ppm. Consequently, the company holds a 30% global market share in Tantalum, alongside a 24% domestic share in Copper and 27% in Aluminum, competing with domestic peers like GRI Composites and Youyan Yijin.

Research and Development accounting is 100% expensed. Expenditures scaled from $6.36 million to $12.83 million, totaling $27.80 million (19,981.79 万元) at a 41.98% CAGR. 2025 R&D allocations include Material Costs at $9.17 million (71.51%), Personnel at $2.10 million (16.36%), D&A at $0.62 million (4.84%), Fuel at $0.60 million (4.69%), and Testing at $0.33 million (2.59%). The company holds 83 authorized patents (28 invention, 55 utility) and 11 software copyrights. A forensic flag remains on 5 invention patents and 11 software copyrights transferred in 2021-2022 to meet HNTE certification thresholds.

Corporate control rests with Chairman Dr. Yao Lijun (14.72% direct, 19.12% via 12 concerted entities including employee platforms Ningbo Hongxin and Ningbo Xinju, plus executives Mao Jian and Li Guipeng, totaling 33.84%). Technical leadership relies heavily on Dr. WUWEN YI. Institutional backers include CNBM Fund (5.40%), ICBC Investment (3.60%), and Shenzhen Capital Group (0.36%). Alignment is enforced by share-based compensation totaling $20.11 million, $19.86 million, and $14.44 million over three years. Near-term risks remain anchored to pending litigation with Orient Tantalum, involving 39 million RMB in frozen assets at Lishui Tongchuang, counterbalanced by a 50 million RMB defamation claim and two 3 million RMB malicious litigation suits.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."