Kureha Corporation: USD 244.04 Million Fixed Asset Impairment Forces B2B Pivot Amid Advanced Materials Margin Compression

Date : 2026-07-08

Reading : 128

HDIN Executive Takeaways

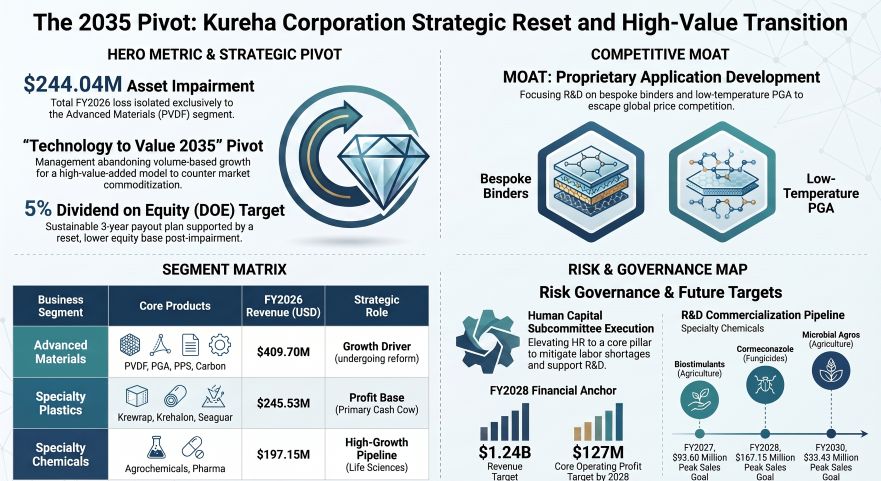

* Kureha Corporation recorded a USD 124.30 million operating loss in FY2026, driven exclusively by a USD 244.04 million impairment in its PVDF resin business, compressing total equity to USD 1,104.73 million as interest-bearing debt expanded to USD 830.56 million.

* Management is realigning its global supply chain—spanning the Iwaki Sanso Center to Kureha (Changshu) Fluoropolymers—navigating geopolitical friction and a 30% GHG reduction mandate via a 9.9% emission cut from idling one domestic coal-fired unit.

* The FY2026–2028 roadmap targets USD 568.30 million in operating cash flow, allocating USD 207.26 million in R&D to offset battery material commoditization while mechanically sustaining a 5% Dividend on Equity on a reduced asset base.

Figure The 2035 Pivot: Kureha Corporation Strategic Reset and High-Value Transition

Consolidated Financial Restructuring and Segment Margin Contraction

Consolidated Financial Restructuring and Segment Margin Contraction

Kureha Corporation [TYO: 4023] reported a consolidated operating loss of USD 124.30 million for the fiscal year ending March 2026, marking a severe contraction from the USD 63.03 million operating profit recorded in March 2025. This bottom-line deterioration stems directly from a USD 244.04 million (JPY 36.5 billion) impairment loss levied entirely against the fixed assets of the Polyvinylidene Fluoride (PVDF) resin business within the Advanced Materials segment. Unallocated corporate adjustments and impairments totaled USD -221.42 million.

The asset write-down structurally altered Kureha’s balance sheet. Total equity attributable to owners contracted from USD 1,399.84 million in March 2025 to USD 1,104.73 million in March 2026. Concurrently, interest-bearing debt expanded from USD 575.06 million to USD 830.56 million, shifting the capital structure toward higher leverage. Non-current assets declined from USD 1,195.20 million to USD 1,016.38 million. Long-term provisions surged 222%, rising from USD 13.31 million (JPY 1,991 million) in March 2025 to USD 42.98 million (JPY 6,428 million) in March 2026, signaling the recognition of long-term environmental remediation or Asset Retirement Obligations (ARO). Short-term provisions decreased marginally from USD 35.25 million (JPY 5,273 million) to USD 34.44 million (JPY 5,151 million).

Capital efficiency metrics turned negative, with Return on Equity (ROE) dropping to -5.7% and Return on Invested Capital (ROIC) falling to -4.2%.

Table 1: Five-Year Horizontal Revenue and Earnings Trajectory

Despite the consolidated operating loss, all core operational segments remained profitable at the gross level prior to structural reform costs. The Advanced Materials segment reported a 6.4% year-over-year expansion in production value to USD 354.83 million (JPY 53.07 billion), though overarching commoditization and market competition compressed margins.

Table 2: FY2026 Segmental Execution Metrics

Geographic Footprint and Supply Chain Realignment

Kureha's external revenue geographic matrix for FY2026 totals USD 1,081.03 million, stratified into five distinct, unlabeled tiers that align with its operational density: Tier 1 (USD 760.83M / JPY 113.80B), Tier 2 (USD 128.64M / JPY 19.24B), Tier 3 (USD 124.72M / JPY 18.65B), Tier 4 (USD 47.99M / JPY 7.18B), and Tier 5 (USD 18.83M / JPY 2.82B).

To execute manufacturing across these tiers, Kureha operates a deeply distributed physical architecture:

* Asia-Pacific: Anchored by the Iwaki Sanso Center in Japan. Operations in China operate under Kureha (Changshu) Fluoropolymers Co., Ltd. and Kureha (Shanghai) Carbon Fiber Materials Co., Ltd. Broader operations include Kureha Vietnam Co., Ltd. and Krehalon Australia Pty Ltd.

* Americas: U.S. penetration is governed by Kureha America Inc., Kureha PGA LLC, Kureha Energy Solutions LLC, and Fortron Industries LLC (a joint venture).

* Europe: Capacity is structured through Kureha GmbH in Germany, alongside Kureha Europe B.V. and Krehalon B.V. in the Netherlands.

Corporate governance frameworks classify both "Supply Chain Management (SCM)" (High Probability, Medium Impact) and "Procurement Risk" (Medium Probability, High Impact) as central operational vulnerabilities. To mitigate physical and transition risks tied to climate change regulations, Kureha initiated an absolute energy structural shift. In April 2024, the firm suspended operations of one of the two units at its in-house coal-fired power plant at the Iwaki Factory, executing a 9.9% reduction in total greenhouse gas (GHG) emissions measured against a FY2013 baseline. Management’s long-term environmental KPIs mandate a 30% GHG reduction by FY2030 and absolute Carbon Neutrality by 2050, allocating USD 8.69 million (JPY 1.3 billion) strictly for environmental capital investments over the next three years.

Research Pipeline and Capital Allocation Architecture

To counteract the acceleration of commoditization within the battery materials market, Kureha is executing its "Technology to Value 2035" mandate, systematically converting intellectual property into high-margin revenues. The Human Capital Subcommittee and the Sustainability Promotion Committee are tasked with securing the specialized labor necessary to maintain this R&D output amid demographic contractions.

In FY2026, Kureha recorded total consolidated R&D expenses of USD 47.94 million (JPY 7.17 billion), establishing an R&D-to-revenue ratio of 4.43%. Segment-specific R&D expenditures included USD 20.24 million (JPY 3.02 billion) in Advanced Materials, USD 17.24 million (JPY 2.57 billion) in Specialty Chemicals, and USD 10.44 million (JPY 1.56 billion) in Specialty Plastics.

Over the FY2026–2028 mid-term plan, management targets generating USD 568.30 million (JPY 85.0 billion) in operating cash flow to fund a recalibrated pipeline. Capital allocations include:

* USD 207.26 million (JPY 31.0 billion) for total R&D (USD 167.15 million in standard R&D and USD 40.12 million in R&D capital investments).

* USD 160.46 million for concrete equipment and environmental frameworks (including USD 143.75 million / JPY 21.5 billion earmarked for remaining PVDF capacity and maintenance investments).

* USD 180.52 million (JPY 27.0 billion) for strategic M&A and new grade developments.

The R&D pipeline targets bespoke applications, including engineering new PVDF binders and low-temperature sealing PGA. The Specialty Chemicals segment projects precise commercialization timelines and peak sales targets for its agricultural innovations: Biostimulants target a FY2027 launch (peak sales USD 93.60M / JPY 14.0B); Carmeconazole (ISO) targets a FY2028 launch (peak sales USD 167.15M / JPY 25.0B); and Microbial agrochemicals target a FY2030 launch (peak sales USD 33.43M / JPY 5.0B). Medical films target a US launch in FY2032 and a Japan launch in FY2035.

FY2028 Forward Guidance versus FY2035 Peak Targets

* FY2028 Consolidated Targets: Revenue USD 1,236.89M (JPY 185.0B); Core Operating Profit USD 127.03M (JPY 19.0B); EBITDA USD 220.63M (JPY 33.0B); ROE 8.0%; ROIC 4.8%.

* FY2028 Segment Revenue Targets: Advanced Materials USD 488.07M (JPY 73.0B) generating USD 40.12M in core operating profit; Specialty Plastics USD 280.81M (JPY 42.0B) generating USD 50.14M in core operating profit; Specialty Chemicals USD 207.26M (JPY 31.0B), encompassing Life Sciences (USD 73.55M) and Industrial Chemicals (USD 133.72M); Construction & Others USD 260.75M (JPY 39.0B).

* FY2035 Long-Term Revenue Targets: PVDF/PGA portfolio USD 267.44M (JPY 40.0B); Household goods USD 267.44M (JPY 40.0B).

HDIN Institutional Verdict

Kureha’s execution of a USD 244.04 million fixed asset impairment reflects a necessary capitulation to macroeconomic realities in the advanced fluoropolymers space. The aggressive write-down structurally resets the depreciation schedule for the PVDF business, stripping future fixed overhead costs from the income statement. This accounting mechanism artificially clears the runway for management to hit its FY2028 core operating profit target of USD 127.03 million (JPY 19.0 billion).

The 5% Dividend on Equity (DOE) policy—costing USD 167.15 million (JPY 25.0 billion) or roughly 29% of projected three-year OCF—is paradoxically fortified by the impairment. By contracting the equity denominator by 21%, Kureha minimizes the absolute cash outlay required to yield the 5% target. While the transition from B2B volume processing to the "Technology to Value 2035" framework is defensively sound, the concurrent expansion in interest-bearing debt to USD 830.56 million restricts balance sheet elasticity. Kureha must now flawlessly execute its USD 207.26 million R&D pipeline in agrochemicals and life sciences, as legacy battery material operations will no longer support long-term volume expansion models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* Kureha Corporation recorded a USD 124.30 million operating loss in FY2026, driven exclusively by a USD 244.04 million impairment in its PVDF resin business, compressing total equity to USD 1,104.73 million as interest-bearing debt expanded to USD 830.56 million.

* Management is realigning its global supply chain—spanning the Iwaki Sanso Center to Kureha (Changshu) Fluoropolymers—navigating geopolitical friction and a 30% GHG reduction mandate via a 9.9% emission cut from idling one domestic coal-fired unit.

* The FY2026–2028 roadmap targets USD 568.30 million in operating cash flow, allocating USD 207.26 million in R&D to offset battery material commoditization while mechanically sustaining a 5% Dividend on Equity on a reduced asset base.

Figure The 2035 Pivot: Kureha Corporation Strategic Reset and High-Value Transition

Consolidated Financial Restructuring and Segment Margin ContractionKureha Corporation [TYO: 4023] reported a consolidated operating loss of USD 124.30 million for the fiscal year ending March 2026, marking a severe contraction from the USD 63.03 million operating profit recorded in March 2025. This bottom-line deterioration stems directly from a USD 244.04 million (JPY 36.5 billion) impairment loss levied entirely against the fixed assets of the Polyvinylidene Fluoride (PVDF) resin business within the Advanced Materials segment. Unallocated corporate adjustments and impairments totaled USD -221.42 million.

The asset write-down structurally altered Kureha’s balance sheet. Total equity attributable to owners contracted from USD 1,399.84 million in March 2025 to USD 1,104.73 million in March 2026. Concurrently, interest-bearing debt expanded from USD 575.06 million to USD 830.56 million, shifting the capital structure toward higher leverage. Non-current assets declined from USD 1,195.20 million to USD 1,016.38 million. Long-term provisions surged 222%, rising from USD 13.31 million (JPY 1,991 million) in March 2025 to USD 42.98 million (JPY 6,428 million) in March 2026, signaling the recognition of long-term environmental remediation or Asset Retirement Obligations (ARO). Short-term provisions decreased marginally from USD 35.25 million (JPY 5,273 million) to USD 34.44 million (JPY 5,151 million).

Capital efficiency metrics turned negative, with Return on Equity (ROE) dropping to -5.7% and Return on Invested Capital (ROIC) falling to -4.2%.

Table 1: Five-Year Horizontal Revenue and Earnings Trajectory

| Fiscal Year (March Ending) | Revenue (USD M) | Net Income / Loss (USD M) | Operating Cash Flow (OCF) (USD M) |

|---|---|---|---|

| March 2022 | $1,125.51M | $94.70M | $191.09M |

| March 2023 (Peak) | $1,278.86M | $112.78M | $152.06M |

| March 2024 | $1,189.91M | $65.08M | $77.56M |

| March 2025 | $1,083.22M | $52.15M | $197.40M |

| March 2026 | $1,081.03M | $(71.49M) | $187.26M |

Despite the consolidated operating loss, all core operational segments remained profitable at the gross level prior to structural reform costs. The Advanced Materials segment reported a 6.4% year-over-year expansion in production value to USD 354.83 million (JPY 53.07 billion), though overarching commoditization and market competition compressed margins.

Table 2: FY2026 Segmental Execution Metrics

| Business Segment | Revenue (USD) | Revenue (JPY) | Revenue Share | Operating Profit (USD) | Operating Profit (JPY) | Strategic Classification / Trend |

|---|---|---|---|---|---|---|

| Advanced Materials (PVDF, PGA, PPS, Carbon) | $409.70M | ¥61.28B | 37.9% | $14.27M | ¥2.13B | Growth Driver Business (B2B) |

| Specialty Plastics (NEW Krewrap, Krehalon Film, Seaguar) | $245.53M | ¥36.72B | 22.7% | $46.22M | ¥6.91B | Profit Base Business (B2C cash generation) |

| Specialty Chemicals (Agrochemicals, Pharmaceuticals, Industrial) | $197.15M | ¥29.49B | 18.2% | $9.03M | ¥1.35B | Diversified specialty chemical platform |

| Construction | $107.06M | ¥16.01B | 9.9% | $10.25M | ¥1.53B | Revenue +7.9% YoY; Operating profit +10.1% YoY |

| Other Operations (Including Kureha Environment Co., Ltd.) | $121.57M | ¥18.18B | 11.2% | $17.33M | ¥2.59B | Revenue -2.2% YoY; Operating profit -11.0% YoY |

Geographic Footprint and Supply Chain Realignment

Kureha's external revenue geographic matrix for FY2026 totals USD 1,081.03 million, stratified into five distinct, unlabeled tiers that align with its operational density: Tier 1 (USD 760.83M / JPY 113.80B), Tier 2 (USD 128.64M / JPY 19.24B), Tier 3 (USD 124.72M / JPY 18.65B), Tier 4 (USD 47.99M / JPY 7.18B), and Tier 5 (USD 18.83M / JPY 2.82B).

To execute manufacturing across these tiers, Kureha operates a deeply distributed physical architecture:

* Asia-Pacific: Anchored by the Iwaki Sanso Center in Japan. Operations in China operate under Kureha (Changshu) Fluoropolymers Co., Ltd. and Kureha (Shanghai) Carbon Fiber Materials Co., Ltd. Broader operations include Kureha Vietnam Co., Ltd. and Krehalon Australia Pty Ltd.

* Americas: U.S. penetration is governed by Kureha America Inc., Kureha PGA LLC, Kureha Energy Solutions LLC, and Fortron Industries LLC (a joint venture).

* Europe: Capacity is structured through Kureha GmbH in Germany, alongside Kureha Europe B.V. and Krehalon B.V. in the Netherlands.

Corporate governance frameworks classify both "Supply Chain Management (SCM)" (High Probability, Medium Impact) and "Procurement Risk" (Medium Probability, High Impact) as central operational vulnerabilities. To mitigate physical and transition risks tied to climate change regulations, Kureha initiated an absolute energy structural shift. In April 2024, the firm suspended operations of one of the two units at its in-house coal-fired power plant at the Iwaki Factory, executing a 9.9% reduction in total greenhouse gas (GHG) emissions measured against a FY2013 baseline. Management’s long-term environmental KPIs mandate a 30% GHG reduction by FY2030 and absolute Carbon Neutrality by 2050, allocating USD 8.69 million (JPY 1.3 billion) strictly for environmental capital investments over the next three years.

Research Pipeline and Capital Allocation Architecture

To counteract the acceleration of commoditization within the battery materials market, Kureha is executing its "Technology to Value 2035" mandate, systematically converting intellectual property into high-margin revenues. The Human Capital Subcommittee and the Sustainability Promotion Committee are tasked with securing the specialized labor necessary to maintain this R&D output amid demographic contractions.

In FY2026, Kureha recorded total consolidated R&D expenses of USD 47.94 million (JPY 7.17 billion), establishing an R&D-to-revenue ratio of 4.43%. Segment-specific R&D expenditures included USD 20.24 million (JPY 3.02 billion) in Advanced Materials, USD 17.24 million (JPY 2.57 billion) in Specialty Chemicals, and USD 10.44 million (JPY 1.56 billion) in Specialty Plastics.

Over the FY2026–2028 mid-term plan, management targets generating USD 568.30 million (JPY 85.0 billion) in operating cash flow to fund a recalibrated pipeline. Capital allocations include:

* USD 207.26 million (JPY 31.0 billion) for total R&D (USD 167.15 million in standard R&D and USD 40.12 million in R&D capital investments).

* USD 160.46 million for concrete equipment and environmental frameworks (including USD 143.75 million / JPY 21.5 billion earmarked for remaining PVDF capacity and maintenance investments).

* USD 180.52 million (JPY 27.0 billion) for strategic M&A and new grade developments.

The R&D pipeline targets bespoke applications, including engineering new PVDF binders and low-temperature sealing PGA. The Specialty Chemicals segment projects precise commercialization timelines and peak sales targets for its agricultural innovations: Biostimulants target a FY2027 launch (peak sales USD 93.60M / JPY 14.0B); Carmeconazole (ISO) targets a FY2028 launch (peak sales USD 167.15M / JPY 25.0B); and Microbial agrochemicals target a FY2030 launch (peak sales USD 33.43M / JPY 5.0B). Medical films target a US launch in FY2032 and a Japan launch in FY2035.

FY2028 Forward Guidance versus FY2035 Peak Targets

* FY2028 Consolidated Targets: Revenue USD 1,236.89M (JPY 185.0B); Core Operating Profit USD 127.03M (JPY 19.0B); EBITDA USD 220.63M (JPY 33.0B); ROE 8.0%; ROIC 4.8%.

* FY2028 Segment Revenue Targets: Advanced Materials USD 488.07M (JPY 73.0B) generating USD 40.12M in core operating profit; Specialty Plastics USD 280.81M (JPY 42.0B) generating USD 50.14M in core operating profit; Specialty Chemicals USD 207.26M (JPY 31.0B), encompassing Life Sciences (USD 73.55M) and Industrial Chemicals (USD 133.72M); Construction & Others USD 260.75M (JPY 39.0B).

* FY2035 Long-Term Revenue Targets: PVDF/PGA portfolio USD 267.44M (JPY 40.0B); Household goods USD 267.44M (JPY 40.0B).

HDIN Institutional Verdict

Kureha’s execution of a USD 244.04 million fixed asset impairment reflects a necessary capitulation to macroeconomic realities in the advanced fluoropolymers space. The aggressive write-down structurally resets the depreciation schedule for the PVDF business, stripping future fixed overhead costs from the income statement. This accounting mechanism artificially clears the runway for management to hit its FY2028 core operating profit target of USD 127.03 million (JPY 19.0 billion).

The 5% Dividend on Equity (DOE) policy—costing USD 167.15 million (JPY 25.0 billion) or roughly 29% of projected three-year OCF—is paradoxically fortified by the impairment. By contracting the equity denominator by 21%, Kureha minimizes the absolute cash outlay required to yield the 5% target. While the transition from B2B volume processing to the "Technology to Value 2035" framework is defensively sound, the concurrent expansion in interest-bearing debt to USD 830.56 million restricts balance sheet elasticity. Kureha must now flawlessly execute its USD 207.26 million R&D pipeline in agrochemicals and life sciences, as legacy battery material operations will no longer support long-term volume expansion models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."