Mitsubishi Gas Chemical: Functional Chemicals Pivot Near MGC Specialty Chemicals Netherlands B.V. as 3.20% ROIC Signals Severe Asset Impairment Execution Drag

Date : 2026-07-08

Reading : 198

HDIN Executive Takeaways

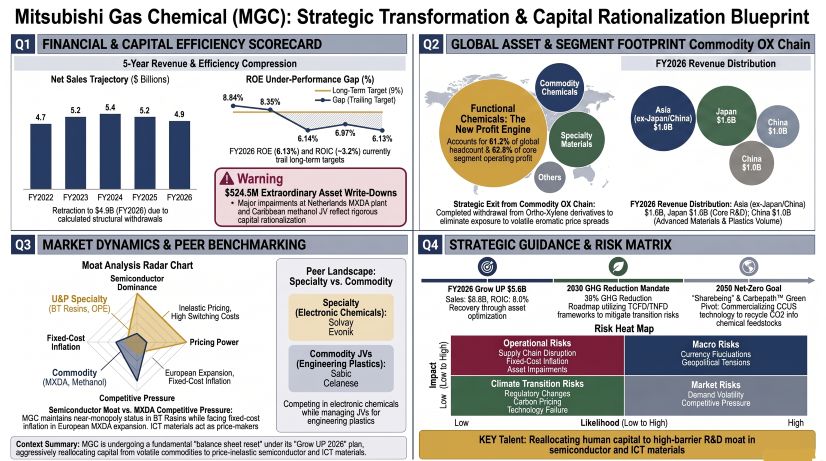

* FY2025 Return on Invested Capital (ROIC) compressed to 3.20% and FY2026 Return on Equity (ROE) fell to 6.13%, missing the 8.0% and 9.0% targets, driven by a 2.4x CapEx-to-Depreciation ratio and a 10-day Cash Conversion Cycle expansion.

* A $370.6 million construction-in-progress write-down at MGC Specialty Chemicals Netherlands B.V. and a $524.5 million asset impairment at Caribbean Gas Chemical Limited exposed structural vulnerabilities in overseas MXDA and methanol fixed costs.

* Management's "Uniqueness & Presence" portfolio realignment artificially deflates the invested capital denominator, utilizing $105.3 million in legacy Polycarbonate write-offs to engineer future net operating profit after tax (NOPAT) recovery.

Figure Mitsubishi Gas Chemical (MGC): Strategic Transformation & Capital Rationalization Blueprint

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Mitsubishi Gas Chemical [TYO: 4182] is executing an aggressive, highly capital-intensive structural transition. Baseline internal modeling for the "Grow UP 2026" Mid-Term Management Plan assumes a foreign exchange rate of 135 JPY/USD and Dubai crude oil pricing at $80/BBL. Conversion of all disclosed metrics relies on a fixed exchange rate of 1 USD = 149.5686 JPY.

Table 1: 5-Year Consolidated Financial Timeline

*Disclosed reporting variations note alternative Operating Profit statements at $340.0 million for FY2025 and $302.8 million for FY2026 within management KPI extracts. Additional consolidated non-operating variance tables record FY2025 Operating Profit at $403.3 million [¥60,316 million] against Ordinary Profit of $322.5 million [¥48,229 million], and FY2026 Operating Profit at $347.3 million [¥51,947 million] against Ordinary Profit of $269.6 million [¥40,318 million].

Top-line execution severely trails the "Grow UP 2026" target of $5,683.0 million (¥850 billion) in Net Sales, $568.3 million (¥85 billion) in Operating Profit, $635.2 million (¥95 billion) in Ordinary Profit, and $1,002.9 million (¥150 billion) in EBITDA.

Working capital efficiency is deteriorating. The Cash Conversion Cycle (CCC) expanded by 10 days, shifting from 137 days to 147 days. While Accounts Receivable days flatlined at approximately 74 days and Accounts Payable days accelerated from 62 days to 58 days, capital remains locked in stagnant inventory. Despite Cost of Goods Sold (COGS) dropping 5.3% year-over-year from $4,073.7 million to $3,857.0 million, total inventory value stagnated at $1,384 million, forcing Inventory Days from 124 days in FY2025 to 131 days in FY2026.

Capital deployment outpaced asset maturation across the FY2025/FY2026 cycles. Consolidated capital expenditures reached $570.7 million (¥85.37 billion) in FY2025 against $231.8 million (¥34.67 billion) in depreciation, producing a 2.4x investment ratio. This metric adjusted to $513.0 million (¥76.73 billion) in FY2026 CapEx against $255.7 million (¥38.24 billion) in depreciation (2.0x ratio).

FY2026 Segmental Profitability & Human Capital Matrix

* Green Energy & Chemicals (Methanol, Ammonia, MXDA, LNG):

* Net Sales: $1,858.0 million. Core Operating Profit: $88.4 million (4.76% margin).

* CapEx Intensity: FY2025 CapEx of $233.8 million (¥34.96 billion) vs. Depreciation of $91.9 million (¥13.75 billion) [2.5x ratio]. FY2026 CapEx of $164.8 million (¥24.64 billion) vs. Depreciation of $88.4 million (¥13.22 billion) [1.9x ratio].

* Labor Economics: 2,632 employees (31.6% of total). Revenue per capita: $705,900. Profit per capita: $33,500.

* Functional Chemicals (BT materials, PC, POM, Ultra-pure chemicals):

* Net Sales: $2,995.3 million (60.7% of total). Core Operating Profit: $150.6 million (62.8% of total). Margin: 5.03%.

* CapEx Intensity: FY2025 CapEx of $334.5 million (¥50.03 billion) vs. Depreciation of $123.8 million (¥18.52 billion) [2.7x ratio]. FY2026 CapEx of $284.6 million (¥42.56 billion) vs. Depreciation of $150.6 million (¥22.52 billion) [1.9x ratio].

* Labor Economics: 5,090 employees (61.2% of total). Revenue per capita: $588,400. Profit per capita: $29,500.

* Other Businesses (Trading, Real Estate):

* Net Sales: $82.5 million. Core Operating Profit: $0.9 million (1.09% margin). Employees: 597.

*(Consolidated totals sum to $4,935.8 million in sales and $239.9 million in profit at a 4.86% margin after corporate eliminations).*

Supply Chain Architecture and Regional Moats

Mitsubishi Gas Chemical’s geographic revenue distribution relies heavily on Asian and domestic demand: Japan generated $1,570.2 million (31.8%), Asia (excluding Japan/China) provided $1,562.6 million (31.7%), China accounted for $979.8 million (19.9%), Europe delivered $500.2 million (10.1%), and North America contributed $323.1 million (6.5%).

Physical asset allocation via Property, Plant, and Equipment (PP&E) reflects a structural shift away from Europe and toward North America. European PP&E contracted from $357.5 million (¥53.47 billion) in FY2025 to $251.5 million (¥37.61 billion) in FY2026. Conversely, North American PP&E expanded from $362.4 million (¥54.20 billion) to $499.6 million (¥74.72 billion), driven by capacity scaling at MGC Pure Chemicals America, Inc. to service domestic semiconductor fabrication.

The European asset contraction stems entirely from a $370.6 million (¥55.44 billion) impairment on construction-in-progress assets at MGC Specialty Chemicals Netherlands B.V. (MSCN), a facility intended for specialty amine (MXDA) production. Total recognized asset impairment losses tied to MSCN scaled from $94.1 million (¥14.08 billion) in FY2025 to $112.8 million (¥16.88 billion) in FY2026.

Equity-method affiliate performance injected massive non-operating volatility. Caribbean Gas Chemical Limited (CGCL) in Trinidad and Tobago absorbed a gross impairment loss of $524.5 million (¥78,448 million), comprising $375.4 million (¥56,145 million) in buildings/structures and $149.1 million (¥22,302 million) in machinery/equipment. This write-down flowed directly to Mitsubishi Gas Chemical, generating a severe equity method loss of $93.4 million (¥13,963 million) in FY2025. This $80.8 million negative gap between Operating Profit and Ordinary Profit stabilized in FY2026, pivoting to an equity method income of $31.2 million (¥4,664 million). *(Alternative disclosed non-operating line items report equity losses of $73.2 million [¥10.96 billion] for FY2025 and $10.3 million [¥1.55 billion] for FY2026).*

Foreign exchange exposures remain unhedged across operations. Segmental filings cite structural FX gains of $12.75 million (¥1,907 million) in FY2025 and $16.87 million (¥2,523 million) in FY2026, while adjacent non-operating ledgers report concurrent FX losses of $12.8 million (¥1.91 billion) in FY2025 and $16.9 million (¥2.52 billion) in FY2026.

Global production continuity requires integration across joint ventures and subsidiaries, including:

MGC Pure Chemicals Taiwan and TAI HONG CIRCUIT INDUSTRIAL CO., LTD. (Taiwan, China).

* Thai Polyacetal, Thai Polycarbonate, Korea Polyacetal, and Samyoung Pure Chemicals.

* Metanol de Oriente, METOR, S.A. (Venezuela - 25.0% voting interest).

* Brunei Methanol Company Sdn. Bhd. (Brunei - 50.0% stake).

* Korea Engineering Plastics Co., Ltd. (South Korea - 50.0% consolidated voting interest; 10.0% direct).

* Samyang Kasei Co., Ltd. (South Korea - 25.0% stake).

Total global headcount expanded from 8,146 to 8,319 employees. Materiality and ESG mandates target a reduction in Scope 1 and 2 Greenhouse Gas (GHG) emissions by 39% by 2030 against a FY2013 baseline, alongside a 2050 Net-Zero timeline. The firm’s human capital architecture targets a female management appointment rate of 6.0% for FY2026 (up from 4.3% in FY2025), scaling to 9.0% by FY2030. Next-Generation Management Candidate (KEY Talent) training pipelines track 81 candidates in FY2025, with internal KPI quotas set at 70 for FY2026 and 75 by FY2030.

HDIN Institutional Verdict

Mitsubishi Gas Chemical is engineering a balance sheet reset, permanently writing down $524.5 million in legacy and non-viable assets to artificially deflate its invested capital base. By halting the MSCN facility in the CIP phase, management eliminates approximately $24 million in annualized straight-line depreciation expenses over a 15-year horizon.

The firm executed an additional $105.3 million (¥15.75 billion) impairment loss on legacy general-purpose Polycarbonate (PC) lines, absorbing $7.0 million (¥1.04 billion) in business withdrawal provisions and incurring $3.5 million (¥519 million) out of a broader $12.1 million (¥1.81 billion) total in restructuring expenses. This strategic exit from the highly elastic, commoditized Ortho-Xylene (OX) and general PC chains protects the firm from Bisphenol-A feedstock cyclicality.

Operational elasticity now relies entirely on the firm's $164.8 million (¥24.64 billion) R&D budget and its "Uniqueness & Presence" (U&P) strategy. Value capture is shifting toward price-inelastic advanced materials, such as Bismaleimide Triazine (BT) resins, Oligo-phenylene ether (OPE), LEXTER polyamides, ENDUREDGE, and Fiber Reinforced Plastics (FRP). To mitigate macroeconomic transition risks, management is commercializing Carbopath™ for CO2 utilization and expanding its Life Sciences IP, which includes Microphysiological Systems (MPS), PQQ, SPD, and SAMe. The success of the "Grow UP 2026" margin recovery relies mathematically on the enforcement of strict ROI thresholds on future basic chemicals CapEx and maintaining absolute pricing power in the electronic materials segment.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

* FY2025 Return on Invested Capital (ROIC) compressed to 3.20% and FY2026 Return on Equity (ROE) fell to 6.13%, missing the 8.0% and 9.0% targets, driven by a 2.4x CapEx-to-Depreciation ratio and a 10-day Cash Conversion Cycle expansion.

* A $370.6 million construction-in-progress write-down at MGC Specialty Chemicals Netherlands B.V. and a $524.5 million asset impairment at Caribbean Gas Chemical Limited exposed structural vulnerabilities in overseas MXDA and methanol fixed costs.

* Management's "Uniqueness & Presence" portfolio realignment artificially deflates the invested capital denominator, utilizing $105.3 million in legacy Polycarbonate write-offs to engineer future net operating profit after tax (NOPAT) recovery.

Figure Mitsubishi Gas Chemical (MGC): Strategic Transformation & Capital Rationalization Blueprint

Segmental Realities and Margin CompressionMitsubishi Gas Chemical [TYO: 4182] is executing an aggressive, highly capital-intensive structural transition. Baseline internal modeling for the "Grow UP 2026" Mid-Term Management Plan assumes a foreign exchange rate of 135 JPY/USD and Dubai crude oil pricing at $80/BBL. Conversion of all disclosed metrics relies on a fixed exchange rate of 1 USD = 149.5686 JPY.

Table 1: 5-Year Consolidated Financial Timeline

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 |

|---|---|---|---|---|---|

| Net Sales ($M) | $4,717.9M | $5,223.1M | $5,438.4M | $5,172.1M | $4,935.8M |

| Ordinary Profit ($M) | $495.8M | $466.4M | $307.8M | $403.3M | $347.3M |

| Net Income ($M) | $322.9M | $328.2M | $259.5M | $304.5M | $269.6M |

| Return on Equity (ROE) | 8.84% | 8.35% | 6.14% | 6.87% | 6.13% |

| Return on Invested Capital (ROIC) | N/A | N/A | 6.40% | 3.20% | N/A |

Top-line execution severely trails the "Grow UP 2026" target of $5,683.0 million (¥850 billion) in Net Sales, $568.3 million (¥85 billion) in Operating Profit, $635.2 million (¥95 billion) in Ordinary Profit, and $1,002.9 million (¥150 billion) in EBITDA.

Working capital efficiency is deteriorating. The Cash Conversion Cycle (CCC) expanded by 10 days, shifting from 137 days to 147 days. While Accounts Receivable days flatlined at approximately 74 days and Accounts Payable days accelerated from 62 days to 58 days, capital remains locked in stagnant inventory. Despite Cost of Goods Sold (COGS) dropping 5.3% year-over-year from $4,073.7 million to $3,857.0 million, total inventory value stagnated at $1,384 million, forcing Inventory Days from 124 days in FY2025 to 131 days in FY2026.

Capital deployment outpaced asset maturation across the FY2025/FY2026 cycles. Consolidated capital expenditures reached $570.7 million (¥85.37 billion) in FY2025 against $231.8 million (¥34.67 billion) in depreciation, producing a 2.4x investment ratio. This metric adjusted to $513.0 million (¥76.73 billion) in FY2026 CapEx against $255.7 million (¥38.24 billion) in depreciation (2.0x ratio).

FY2026 Segmental Profitability & Human Capital Matrix

* Green Energy & Chemicals (Methanol, Ammonia, MXDA, LNG):

* Net Sales: $1,858.0 million. Core Operating Profit: $88.4 million (4.76% margin).

* CapEx Intensity: FY2025 CapEx of $233.8 million (¥34.96 billion) vs. Depreciation of $91.9 million (¥13.75 billion) [2.5x ratio]. FY2026 CapEx of $164.8 million (¥24.64 billion) vs. Depreciation of $88.4 million (¥13.22 billion) [1.9x ratio].

* Labor Economics: 2,632 employees (31.6% of total). Revenue per capita: $705,900. Profit per capita: $33,500.

* Functional Chemicals (BT materials, PC, POM, Ultra-pure chemicals):

* Net Sales: $2,995.3 million (60.7% of total). Core Operating Profit: $150.6 million (62.8% of total). Margin: 5.03%.

* CapEx Intensity: FY2025 CapEx of $334.5 million (¥50.03 billion) vs. Depreciation of $123.8 million (¥18.52 billion) [2.7x ratio]. FY2026 CapEx of $284.6 million (¥42.56 billion) vs. Depreciation of $150.6 million (¥22.52 billion) [1.9x ratio].

* Labor Economics: 5,090 employees (61.2% of total). Revenue per capita: $588,400. Profit per capita: $29,500.

* Other Businesses (Trading, Real Estate):

* Net Sales: $82.5 million. Core Operating Profit: $0.9 million (1.09% margin). Employees: 597.

*(Consolidated totals sum to $4,935.8 million in sales and $239.9 million in profit at a 4.86% margin after corporate eliminations).*

Supply Chain Architecture and Regional Moats

Mitsubishi Gas Chemical’s geographic revenue distribution relies heavily on Asian and domestic demand: Japan generated $1,570.2 million (31.8%), Asia (excluding Japan/China) provided $1,562.6 million (31.7%), China accounted for $979.8 million (19.9%), Europe delivered $500.2 million (10.1%), and North America contributed $323.1 million (6.5%).

Physical asset allocation via Property, Plant, and Equipment (PP&E) reflects a structural shift away from Europe and toward North America. European PP&E contracted from $357.5 million (¥53.47 billion) in FY2025 to $251.5 million (¥37.61 billion) in FY2026. Conversely, North American PP&E expanded from $362.4 million (¥54.20 billion) to $499.6 million (¥74.72 billion), driven by capacity scaling at MGC Pure Chemicals America, Inc. to service domestic semiconductor fabrication.

The European asset contraction stems entirely from a $370.6 million (¥55.44 billion) impairment on construction-in-progress assets at MGC Specialty Chemicals Netherlands B.V. (MSCN), a facility intended for specialty amine (MXDA) production. Total recognized asset impairment losses tied to MSCN scaled from $94.1 million (¥14.08 billion) in FY2025 to $112.8 million (¥16.88 billion) in FY2026.

Equity-method affiliate performance injected massive non-operating volatility. Caribbean Gas Chemical Limited (CGCL) in Trinidad and Tobago absorbed a gross impairment loss of $524.5 million (¥78,448 million), comprising $375.4 million (¥56,145 million) in buildings/structures and $149.1 million (¥22,302 million) in machinery/equipment. This write-down flowed directly to Mitsubishi Gas Chemical, generating a severe equity method loss of $93.4 million (¥13,963 million) in FY2025. This $80.8 million negative gap between Operating Profit and Ordinary Profit stabilized in FY2026, pivoting to an equity method income of $31.2 million (¥4,664 million). *(Alternative disclosed non-operating line items report equity losses of $73.2 million [¥10.96 billion] for FY2025 and $10.3 million [¥1.55 billion] for FY2026).*

Foreign exchange exposures remain unhedged across operations. Segmental filings cite structural FX gains of $12.75 million (¥1,907 million) in FY2025 and $16.87 million (¥2,523 million) in FY2026, while adjacent non-operating ledgers report concurrent FX losses of $12.8 million (¥1.91 billion) in FY2025 and $16.9 million (¥2.52 billion) in FY2026.

Global production continuity requires integration across joint ventures and subsidiaries, including:

MGC Pure Chemicals Taiwan and TAI HONG CIRCUIT INDUSTRIAL CO., LTD. (Taiwan, China).

* Thai Polyacetal, Thai Polycarbonate, Korea Polyacetal, and Samyoung Pure Chemicals.

* Metanol de Oriente, METOR, S.A. (Venezuela - 25.0% voting interest).

* Brunei Methanol Company Sdn. Bhd. (Brunei - 50.0% stake).

* Korea Engineering Plastics Co., Ltd. (South Korea - 50.0% consolidated voting interest; 10.0% direct).

* Samyang Kasei Co., Ltd. (South Korea - 25.0% stake).

Total global headcount expanded from 8,146 to 8,319 employees. Materiality and ESG mandates target a reduction in Scope 1 and 2 Greenhouse Gas (GHG) emissions by 39% by 2030 against a FY2013 baseline, alongside a 2050 Net-Zero timeline. The firm’s human capital architecture targets a female management appointment rate of 6.0% for FY2026 (up from 4.3% in FY2025), scaling to 9.0% by FY2030. Next-Generation Management Candidate (KEY Talent) training pipelines track 81 candidates in FY2025, with internal KPI quotas set at 70 for FY2026 and 75 by FY2030.

HDIN Institutional Verdict

Mitsubishi Gas Chemical is engineering a balance sheet reset, permanently writing down $524.5 million in legacy and non-viable assets to artificially deflate its invested capital base. By halting the MSCN facility in the CIP phase, management eliminates approximately $24 million in annualized straight-line depreciation expenses over a 15-year horizon.

The firm executed an additional $105.3 million (¥15.75 billion) impairment loss on legacy general-purpose Polycarbonate (PC) lines, absorbing $7.0 million (¥1.04 billion) in business withdrawal provisions and incurring $3.5 million (¥519 million) out of a broader $12.1 million (¥1.81 billion) total in restructuring expenses. This strategic exit from the highly elastic, commoditized Ortho-Xylene (OX) and general PC chains protects the firm from Bisphenol-A feedstock cyclicality.

Operational elasticity now relies entirely on the firm's $164.8 million (¥24.64 billion) R&D budget and its "Uniqueness & Presence" (U&P) strategy. Value capture is shifting toward price-inelastic advanced materials, such as Bismaleimide Triazine (BT) resins, Oligo-phenylene ether (OPE), LEXTER polyamides, ENDUREDGE, and Fiber Reinforced Plastics (FRP). To mitigate macroeconomic transition risks, management is commercializing Carbopath™ for CO2 utilization and expanding its Life Sciences IP, which includes Microphysiological Systems (MPS), PQQ, SPD, and SAMe. The success of the "Grow UP 2026" margin recovery relies mathematically on the enforcement of strict ROI thresholds on future basic chemicals CapEx and maintaining absolute pricing power in the electronic materials segment.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer:*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."