Mahindra & Mahindra Limited: Aggressive EV Capitalization Near Nagpur as 20.1% ROE Signals Unprecedented ICE-to-Electric Operating Leverage

Date : 2026-07-08

Reading : 229

HDIN Executive Takeaways

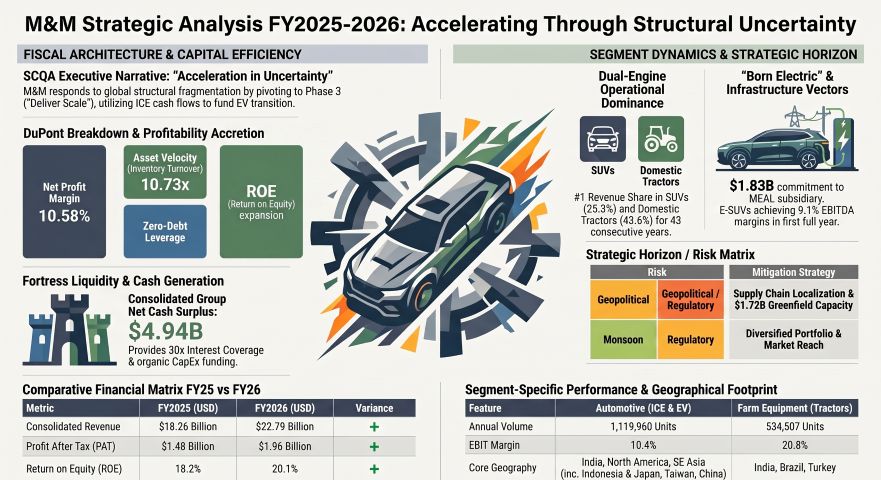

* Mahindra & Mahindra Limited absorbed a 28.9% material cost spike by restricting fixed cost growth to 14.4%, driving Profit After Tax up 32% to $1.96 billion while yielding a 20.1% consolidated Return on Equity.

* Mitigating geopolitical risks, the firm deployed $1.72 billion for a Nagpur greenfield plant yielding 500,000-vehicle capacity, simultaneously exiting Finland and Japan to capture Latin American and Turkish market share.

* Capitalizing 82.4% of its $653.08 million R&D outlay shields near-term margins. However, first-year electric SUV EBITDA of 9.1% confirms tangible unit economics despite a $1.33 billion off-balance-sheet contingent tax overhang.

Figure M&M Strategic Analysis FY2025-2026 Accelerating Through Structural Uncertainty

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Mahindra & Mahindra Limited [NSE: M&M] executed Phase 3 of its "Deliver Scale" strategy in FY2025-2026, recording consolidated revenues of $22.79 billion (₹1,98,639 crore), representing a 24.8% year-over-year expansion. Consolidated Profit After Tax (PAT) reached $1.96 billion (₹1,7099 crore), a 32% increase. This margin accretion was achieved despite the consolidated Cost of Goods Sold (COGS) surging 28.9% to $13.03 billion (₹1,13,553.14 crore). On a standalone basis, material costs as a percentage of operations income expanded by 220 basis points (bps) to 75.0%.

The firm defended its bottom line via aggressive fixed-cost dilution. Standalone employee costs contracted by 50 bps to 3.6% of revenue, as consolidated employee benefits grew only 14.4% to $1.46 billion (₹12,730.62 crore), comprising $1.25 billion (₹10,941.99 crore) in salaries and $39.7 million (₹346.19 crore) in ESOPs. SG&A expanded 16.7% to $2.92 billion (₹25,424.14 crore), pushing standalone operating costs down from 6.9% to 5.8%.

Segmental Financial & Operational Matrix:

* Automotive Segment: Revenue reached $12.53 billion (₹1,09,199 crore) with an EBIT of $1.19 billion (₹10,383 crore). Core EBIT margins expanded 70 bps to 10.4%. Global sales hit 1,119,960 vehicles (+19.1%), including 660,276 domestic passenger vehicles (+19.7%). E-SUV penetration reached 9.6% by Q4 FY26, yielding a first-year end-to-end EBITDA of 9.1% and EBIT of 2.0%.

* Farm Equipment Segment: Revenue stood at $4.17 billion (₹36,376 crore) with an EBIT of $0.63 billion (₹5,516 crore). Core tractor EBIT margins expanded 110 bps to 20.8%. Global volumes reached 534,507 units (+23.3%) against total production of 521,945 units. Domestic volumes hit 505,930 units (+24.3%). Non-tractor machinery revenue grew 32% to $155.37 million (₹1,354 crore).

* Financial Services (Mahindra Finance / MMFSL): Revenue reached $2.39 billion (₹20,817 crore) with an EBIT of $0.43 billion (₹3,778 crore). Assets Under Management (AUM) expanded 12% to $15.39 billion (₹1,34,096 crore), aided by a 49% surge in tractor disbursements. Gross Stage 3 (GS3) assets fell to 3.4%. Total loans stand at $16.45 billion (₹1,43,403 crore) against an Expected Credit Loss (ECL) provision of $475.06 million (₹4,140 crore).

* Tech Mahindra (IT Services): Revenue reached $6.52 billion (₹56,815 crore). EBIT margins expanded 290 bps to 12.6% on $3.79 billion in large deal wins. The unit generated $616 million in Free Cash Flow (a 115% FCF-to-PAT conversion rate). Management targets a 15% margin by FY27, >30% ROCE, and >85% FCF return to shareholders.

* Mahindra Accelo (Tier 0.5/1 Supplier): Revenue scaled to $688.5 million (₹6,000 crore) via localized production of EV motor cores and aluminum battery casings.

Domestic & International Market Share Dynamics:

* India Dominance: Ranked #1 in ICE SUVs with 25.3% revenue share (+260 bps); #1 in E-SUVs at 37.4%; #1 in Tractors at 43.6% (+30 bps, marking 43 consecutive years of leadership); #1 in LCVs (<3.5T) at 52.3% (+60 bps); #1 in E-3Ws at 40.0%. ILCV combined share reached 6.0% following a 58.97% stake acquisition in SML Isuzu, capturing 22.9% of the bus segment.

* Global Footprint: Exports totaled 41,030 automotive units and 20,473 tractors, anchored by a 35,000 Scorpio Pikup order to Indonesia. Market share reached 6.3% in US <110 HP tractors, 6.6% in Brazil <120 HP tractors, and 5.8% in Turkey via Erkunt Traktor.

Capital Efficiency & Leverage Ratios:

* Return Metrics: Standalone Net Profit Margin expanded 59 bps to 10.58%. Standalone EBIT margin reached 19.8% (+140 bps). Standalone Return on Equity (ROE) expanded 219 bps to 23.01%. Standalone Return on Capital Employed (ROCE) expanded 296 bps to 30.23%.

* Asset Velocity & Debt: Inventory turnover accelerated from 8.61x to 10.73x; Receivables turnover improved from 22.17x to 23.42x; Payables turnover stood at 4.51x. Net capital turnover decelerated slightly from 9.26x to 8.44x. Standalone Debt-to-Equity contracted from 0.02x to 0.01x, while consolidated D/E sits at 0.04x. Interest coverage fortified from 62.0x to 77.8x, with a Debt Service Coverage Ratio (DSCR) of 30.05x. Standalone net cash surplus equals $4.06 billion (₹35,431.94 crore), while consolidated net cash (excluding financial services) sits at $4.94 billion (₹43,093.82 crore). Standalone gross borrowings dropped from $130.24 million (₹1,135 crore) to $121.17 million (₹1,056 crore).

Infrastructure Layout and Regional Moats

Mahindra & Mahindra Limited operates 49 manufacturing plants in India and 24 international facilities across 100 countries. Total net CapEx for FY26 reached $1.04 billion (₹9,112 crore). The firm is restructuring its physical architecture, committing $1.72 billion (₹15,000 crore) toward a Nagpur greenfield plant expected to yield 500,000 vehicles and 100,000 tractors annually by 2028. Concurrently, it exited structurally weak operations at Sampo Rosenlew in Finland and Mitsubishi Mahindra Agricultural Machinery in Japan.

Supply Chain, Subsidies & EV Infrastructure:

* EV Architecture & Subsidies: Backed by the $1.25 billion (₹10,900 crore) PM E-DRIVE scheme and $83.54 million (₹7,280 crore) REPM scheme, the firm's INGLO electric platform utilizes Lithium Iron Phosphate (LFP) prismatic cells configured at 59 kWh, 70 kWh, and 79 kWh, yielding 500 km ranges. The firm recorded 999 units sold in 135 seconds for its BE 6 model. Operating exit capacity scaled to 64.5k units/month (774k annual run-rate).

* Infrastructure & Logistics: The Charge_iN network will scale from 120 current points to 1,000 fast-charging points across 250 stations by 2027. Last Mile Mobility (LMM) deployed 3.4 lakh commercial EVs, targeting 1 million by 2031. Mahindra Logistics (MLL), utilizing the LogiOne AI platform, broke even after 11 quarters, aiming to double revenue by FY31. The Cero recycling venture recovered materials from 40,000 end-of-life vehicles.

* R&D Ecosystem: The Mahindra Research Valley (MRV) in Detroit and India houses 5,000 engineers with 1,440+ granted patents. Future product pipelines (FY27-2031) include 26 auto launches (10 ICE, 6 E-SUV, 10 Veero LCVs) and 19 farm launches (7 new OJA/Target tractors, 12 upgrades) by FY27. Management forecasts 20-30% EV penetration by 2027 and a 3X revenue scale in Farm Equipment.

Contingent Liabilities, RPTs, and Hedging Exposures:

* Off-Balance Sheet Risk: Contingent liabilities total $1.33 billion (₹11,600.31 crore), encompassing indirect tax disputes of $495.53 million (₹4,318.35 crore), direct tax appeals of $357.44 million (₹3,114.99 crore) and $96.16 million (₹837.99 crore), JV liabilities of $288.10 million (₹2,510.71 crore), and legal matters of $93.90 million (₹818.27 crore). Furthermore, battery waste provisions total $6.52 million (₹56.84 crore).

* Capital Commitments: Material purchase agreements total $1.21 billion (₹10,527.89 crore) and CapEx commitments sit at $807.29 million (₹7,035.26 crore). Corporate guarantees stand at $113.14 million (₹986.02 crore), primarily covering Mahindra Aerostructures ($96.93 million / ₹844.73 crore) and Mahindra USA Inc. ($16.21 million / ₹141.29 crore).

* Related-Party Transactions (RPTs): Mahindra Electric Automobile Limited (MEAL) received $1.42 billion (₹12,413.01 crore) in sales and $171.66 million (₹1,496.00 crore) in equity in FY26. The Board seeks omnibus approval for up to $4.02 billion (₹35,000 crore) in MEAL transactions. Total MEAL EV investment approval is $1.83 billion (₹15,925 crore), with $797.56 million (₹6,950 crore) deployed. Mahindra USA (MUSA) and Mahindra Finance USA (MFUSA) executed total financing of $354.98 million (₹3,093.49 crore) ($349.5 million / ₹3,093.49 crore invoice discounting; $47.46 million / ₹420.05 crore retail) with pending approvals to scale to $688.49 million (₹6,000 crore).

* Valuation & Impairment: $3.16 billion (₹27,547.10 crore) in long-term investments face impairment models using discount rates between 12.80% and 19.60%. An impairment provision of $7.67 million (₹668.37 crore) was recorded. Commodity hedging programs generated $6.76 million (₹589.47 crore) in gains. Freight outward costs expanded 16.2% to $766.31 million (₹6,678.17 crore). Marketing expenditures hit $189.67 million (₹1,652.87 crore) (Advertising: $115.79 million / ₹1,009.07 crore; Promotions: $73.88 million / ₹643.80 crore). Depreciation and amortization increased by 20.5%.

ESG, Emissions, and Human Capital Metrics:

* Emissions Profile (SBTi Targets: -47% S1/S2, -30% S3 by 2033): Scope 1 emissions rose to 80,319 tCO2e, while Scope 2 dropped to 2,41,210 tCO2e. Total S1+S2 emissions equal 3,21,529 tCO2e. Automotive carbon intensity dropped 57%. However, Scope 3 emissions spiked to 123,705,567 tCO2e following the inclusion of truck and bus operations. Internal carbon pricing is set at $10/ton.

* Resource Efficiency: Total water withdrawal reached 3,050,611 kl, achieving 100.001% water positivity. Nashik plant evaporators cut fresh water usage by 50% and energy by 60%. Mahindra Susten provided 37% renewable electricity to operations, targeting a portfolio scale from 2.1 GWp to 7.0 GWp. India Meteorological Department (IMD) projects 90-92% of the Long Period Average (LPA) monsoon, prompting 40 kg (2-3%) weight reductions per tractor to hedge variable costs.

* Human Capital & Safety: The 11-member Board features 6 independent directors (55%) and 4 women (36.36%). Women comprise 67% (4 out of 6) of independent directors. Total employees equal 16,642, with 2,166 women (13.02%). Female compensation share reached 8.46%. CEO remuneration stands at $2.06 million (₹17.99 crore), a 514x median pay ratio. LTIFR for employees is 0 (0 fatalities), while contractor LTIFR stands at 0.07.

* Supply Chain Audits: 95% of suppliers signed the code of conduct. ESG due diligence covered 68.1% of the supply base (11.9% in FY26); 42% report renewable energy use, and 51% use recycled water. Independent safety audits covered 67% of suppliers (13% in FY26).

* Growth Gems: Mahindra Lifespaces achieved a Gross Development Value (GDV) of $2.07 billion (₹18,060 crore) with FY30 pre-sales targets of $1.15 billion (₹10,000 crore). Mahindra Holidays targets 12,000 keys by FY30.

HDIN Institutional Verdict

Mahindra & Mahindra Limited’s FY26 financial architecture demonstrates masterclass operational leverage, but relies heavily on sophisticated accounting treatments to shield near-term profitability during its EV transition. By capitalizing 82.4% ($537.88 million / ₹4,687.45 crore) of its $653.08 million (₹5,691.40 crore) total R&D outlay—expensing only $115.20 million (₹1,003.95 crore)—the firm artificially suppresses COGS, inflating intangible assets under development to $616.38 million (₹5,371.51 crore). This capitalization matrix directly enables the elite 23.01% standalone ROE and 30.23% ROCE.

However, the underlying unit economics confirm the strategy's operational viability. Achieving a 9.1% end-to-end EBITDA on the E-SUV portfolio in its first full year invalidates the traditional cash-burn narrative associated with legacy OEM electrification. The firm is successfully extracting peak cash flow from its ICE dominance (25.3% SUV share, 43.6% tractor share) to subsidize the Born Electric ecosystem, AI matrix (Experience.AI, Efficiency.AI, Enterprise.AI), and its NU_IQ/DAVINCI ICE/SDV platforms. While the $1.33 billion off-balance-sheet contingent tax liability and $4.02 billion in internal EV RPTs require stringent auditor oversight, the core balance sheet's negligible 0.01x standalone D/E ratio provides a highly fortified moat against impending macroeconomic fragmentation.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

* Mahindra & Mahindra Limited absorbed a 28.9% material cost spike by restricting fixed cost growth to 14.4%, driving Profit After Tax up 32% to $1.96 billion while yielding a 20.1% consolidated Return on Equity.

* Mitigating geopolitical risks, the firm deployed $1.72 billion for a Nagpur greenfield plant yielding 500,000-vehicle capacity, simultaneously exiting Finland and Japan to capture Latin American and Turkish market share.

* Capitalizing 82.4% of its $653.08 million R&D outlay shields near-term margins. However, first-year electric SUV EBITDA of 9.1% confirms tangible unit economics despite a $1.33 billion off-balance-sheet contingent tax overhang.

Figure M&M Strategic Analysis FY2025-2026 Accelerating Through Structural Uncertainty

Segmental Realities and Margin CompressionMahindra & Mahindra Limited [NSE: M&M] executed Phase 3 of its "Deliver Scale" strategy in FY2025-2026, recording consolidated revenues of $22.79 billion (₹1,98,639 crore), representing a 24.8% year-over-year expansion. Consolidated Profit After Tax (PAT) reached $1.96 billion (₹1,7099 crore), a 32% increase. This margin accretion was achieved despite the consolidated Cost of Goods Sold (COGS) surging 28.9% to $13.03 billion (₹1,13,553.14 crore). On a standalone basis, material costs as a percentage of operations income expanded by 220 basis points (bps) to 75.0%.

The firm defended its bottom line via aggressive fixed-cost dilution. Standalone employee costs contracted by 50 bps to 3.6% of revenue, as consolidated employee benefits grew only 14.4% to $1.46 billion (₹12,730.62 crore), comprising $1.25 billion (₹10,941.99 crore) in salaries and $39.7 million (₹346.19 crore) in ESOPs. SG&A expanded 16.7% to $2.92 billion (₹25,424.14 crore), pushing standalone operating costs down from 6.9% to 5.8%.

Segmental Financial & Operational Matrix:

* Automotive Segment: Revenue reached $12.53 billion (₹1,09,199 crore) with an EBIT of $1.19 billion (₹10,383 crore). Core EBIT margins expanded 70 bps to 10.4%. Global sales hit 1,119,960 vehicles (+19.1%), including 660,276 domestic passenger vehicles (+19.7%). E-SUV penetration reached 9.6% by Q4 FY26, yielding a first-year end-to-end EBITDA of 9.1% and EBIT of 2.0%.

* Farm Equipment Segment: Revenue stood at $4.17 billion (₹36,376 crore) with an EBIT of $0.63 billion (₹5,516 crore). Core tractor EBIT margins expanded 110 bps to 20.8%. Global volumes reached 534,507 units (+23.3%) against total production of 521,945 units. Domestic volumes hit 505,930 units (+24.3%). Non-tractor machinery revenue grew 32% to $155.37 million (₹1,354 crore).

* Financial Services (Mahindra Finance / MMFSL): Revenue reached $2.39 billion (₹20,817 crore) with an EBIT of $0.43 billion (₹3,778 crore). Assets Under Management (AUM) expanded 12% to $15.39 billion (₹1,34,096 crore), aided by a 49% surge in tractor disbursements. Gross Stage 3 (GS3) assets fell to 3.4%. Total loans stand at $16.45 billion (₹1,43,403 crore) against an Expected Credit Loss (ECL) provision of $475.06 million (₹4,140 crore).

* Tech Mahindra (IT Services): Revenue reached $6.52 billion (₹56,815 crore). EBIT margins expanded 290 bps to 12.6% on $3.79 billion in large deal wins. The unit generated $616 million in Free Cash Flow (a 115% FCF-to-PAT conversion rate). Management targets a 15% margin by FY27, >30% ROCE, and >85% FCF return to shareholders.

* Mahindra Accelo (Tier 0.5/1 Supplier): Revenue scaled to $688.5 million (₹6,000 crore) via localized production of EV motor cores and aluminum battery casings.

Domestic & International Market Share Dynamics:

* India Dominance: Ranked #1 in ICE SUVs with 25.3% revenue share (+260 bps); #1 in E-SUVs at 37.4%; #1 in Tractors at 43.6% (+30 bps, marking 43 consecutive years of leadership); #1 in LCVs (<3.5T) at 52.3% (+60 bps); #1 in E-3Ws at 40.0%. ILCV combined share reached 6.0% following a 58.97% stake acquisition in SML Isuzu, capturing 22.9% of the bus segment.

* Global Footprint: Exports totaled 41,030 automotive units and 20,473 tractors, anchored by a 35,000 Scorpio Pikup order to Indonesia. Market share reached 6.3% in US <110 HP tractors, 6.6% in Brazil <120 HP tractors, and 5.8% in Turkey via Erkunt Traktor.

Capital Efficiency & Leverage Ratios:

* Return Metrics: Standalone Net Profit Margin expanded 59 bps to 10.58%. Standalone EBIT margin reached 19.8% (+140 bps). Standalone Return on Equity (ROE) expanded 219 bps to 23.01%. Standalone Return on Capital Employed (ROCE) expanded 296 bps to 30.23%.

* Asset Velocity & Debt: Inventory turnover accelerated from 8.61x to 10.73x; Receivables turnover improved from 22.17x to 23.42x; Payables turnover stood at 4.51x. Net capital turnover decelerated slightly from 9.26x to 8.44x. Standalone Debt-to-Equity contracted from 0.02x to 0.01x, while consolidated D/E sits at 0.04x. Interest coverage fortified from 62.0x to 77.8x, with a Debt Service Coverage Ratio (DSCR) of 30.05x. Standalone net cash surplus equals $4.06 billion (₹35,431.94 crore), while consolidated net cash (excluding financial services) sits at $4.94 billion (₹43,093.82 crore). Standalone gross borrowings dropped from $130.24 million (₹1,135 crore) to $121.17 million (₹1,056 crore).

Infrastructure Layout and Regional Moats

Mahindra & Mahindra Limited operates 49 manufacturing plants in India and 24 international facilities across 100 countries. Total net CapEx for FY26 reached $1.04 billion (₹9,112 crore). The firm is restructuring its physical architecture, committing $1.72 billion (₹15,000 crore) toward a Nagpur greenfield plant expected to yield 500,000 vehicles and 100,000 tractors annually by 2028. Concurrently, it exited structurally weak operations at Sampo Rosenlew in Finland and Mitsubishi Mahindra Agricultural Machinery in Japan.

Supply Chain, Subsidies & EV Infrastructure:

* EV Architecture & Subsidies: Backed by the $1.25 billion (₹10,900 crore) PM E-DRIVE scheme and $83.54 million (₹7,280 crore) REPM scheme, the firm's INGLO electric platform utilizes Lithium Iron Phosphate (LFP) prismatic cells configured at 59 kWh, 70 kWh, and 79 kWh, yielding 500 km ranges. The firm recorded 999 units sold in 135 seconds for its BE 6 model. Operating exit capacity scaled to 64.5k units/month (774k annual run-rate).

* Infrastructure & Logistics: The Charge_iN network will scale from 120 current points to 1,000 fast-charging points across 250 stations by 2027. Last Mile Mobility (LMM) deployed 3.4 lakh commercial EVs, targeting 1 million by 2031. Mahindra Logistics (MLL), utilizing the LogiOne AI platform, broke even after 11 quarters, aiming to double revenue by FY31. The Cero recycling venture recovered materials from 40,000 end-of-life vehicles.

* R&D Ecosystem: The Mahindra Research Valley (MRV) in Detroit and India houses 5,000 engineers with 1,440+ granted patents. Future product pipelines (FY27-2031) include 26 auto launches (10 ICE, 6 E-SUV, 10 Veero LCVs) and 19 farm launches (7 new OJA/Target tractors, 12 upgrades) by FY27. Management forecasts 20-30% EV penetration by 2027 and a 3X revenue scale in Farm Equipment.

Contingent Liabilities, RPTs, and Hedging Exposures:

* Off-Balance Sheet Risk: Contingent liabilities total $1.33 billion (₹11,600.31 crore), encompassing indirect tax disputes of $495.53 million (₹4,318.35 crore), direct tax appeals of $357.44 million (₹3,114.99 crore) and $96.16 million (₹837.99 crore), JV liabilities of $288.10 million (₹2,510.71 crore), and legal matters of $93.90 million (₹818.27 crore). Furthermore, battery waste provisions total $6.52 million (₹56.84 crore).

* Capital Commitments: Material purchase agreements total $1.21 billion (₹10,527.89 crore) and CapEx commitments sit at $807.29 million (₹7,035.26 crore). Corporate guarantees stand at $113.14 million (₹986.02 crore), primarily covering Mahindra Aerostructures ($96.93 million / ₹844.73 crore) and Mahindra USA Inc. ($16.21 million / ₹141.29 crore).

* Related-Party Transactions (RPTs): Mahindra Electric Automobile Limited (MEAL) received $1.42 billion (₹12,413.01 crore) in sales and $171.66 million (₹1,496.00 crore) in equity in FY26. The Board seeks omnibus approval for up to $4.02 billion (₹35,000 crore) in MEAL transactions. Total MEAL EV investment approval is $1.83 billion (₹15,925 crore), with $797.56 million (₹6,950 crore) deployed. Mahindra USA (MUSA) and Mahindra Finance USA (MFUSA) executed total financing of $354.98 million (₹3,093.49 crore) ($349.5 million / ₹3,093.49 crore invoice discounting; $47.46 million / ₹420.05 crore retail) with pending approvals to scale to $688.49 million (₹6,000 crore).

* Valuation & Impairment: $3.16 billion (₹27,547.10 crore) in long-term investments face impairment models using discount rates between 12.80% and 19.60%. An impairment provision of $7.67 million (₹668.37 crore) was recorded. Commodity hedging programs generated $6.76 million (₹589.47 crore) in gains. Freight outward costs expanded 16.2% to $766.31 million (₹6,678.17 crore). Marketing expenditures hit $189.67 million (₹1,652.87 crore) (Advertising: $115.79 million / ₹1,009.07 crore; Promotions: $73.88 million / ₹643.80 crore). Depreciation and amortization increased by 20.5%.

ESG, Emissions, and Human Capital Metrics:

* Emissions Profile (SBTi Targets: -47% S1/S2, -30% S3 by 2033): Scope 1 emissions rose to 80,319 tCO2e, while Scope 2 dropped to 2,41,210 tCO2e. Total S1+S2 emissions equal 3,21,529 tCO2e. Automotive carbon intensity dropped 57%. However, Scope 3 emissions spiked to 123,705,567 tCO2e following the inclusion of truck and bus operations. Internal carbon pricing is set at $10/ton.

* Resource Efficiency: Total water withdrawal reached 3,050,611 kl, achieving 100.001% water positivity. Nashik plant evaporators cut fresh water usage by 50% and energy by 60%. Mahindra Susten provided 37% renewable electricity to operations, targeting a portfolio scale from 2.1 GWp to 7.0 GWp. India Meteorological Department (IMD) projects 90-92% of the Long Period Average (LPA) monsoon, prompting 40 kg (2-3%) weight reductions per tractor to hedge variable costs.

* Human Capital & Safety: The 11-member Board features 6 independent directors (55%) and 4 women (36.36%). Women comprise 67% (4 out of 6) of independent directors. Total employees equal 16,642, with 2,166 women (13.02%). Female compensation share reached 8.46%. CEO remuneration stands at $2.06 million (₹17.99 crore), a 514x median pay ratio. LTIFR for employees is 0 (0 fatalities), while contractor LTIFR stands at 0.07.

* Supply Chain Audits: 95% of suppliers signed the code of conduct. ESG due diligence covered 68.1% of the supply base (11.9% in FY26); 42% report renewable energy use, and 51% use recycled water. Independent safety audits covered 67% of suppliers (13% in FY26).

* Growth Gems: Mahindra Lifespaces achieved a Gross Development Value (GDV) of $2.07 billion (₹18,060 crore) with FY30 pre-sales targets of $1.15 billion (₹10,000 crore). Mahindra Holidays targets 12,000 keys by FY30.

HDIN Institutional Verdict

Mahindra & Mahindra Limited’s FY26 financial architecture demonstrates masterclass operational leverage, but relies heavily on sophisticated accounting treatments to shield near-term profitability during its EV transition. By capitalizing 82.4% ($537.88 million / ₹4,687.45 crore) of its $653.08 million (₹5,691.40 crore) total R&D outlay—expensing only $115.20 million (₹1,003.95 crore)—the firm artificially suppresses COGS, inflating intangible assets under development to $616.38 million (₹5,371.51 crore). This capitalization matrix directly enables the elite 23.01% standalone ROE and 30.23% ROCE.

However, the underlying unit economics confirm the strategy's operational viability. Achieving a 9.1% end-to-end EBITDA on the E-SUV portfolio in its first full year invalidates the traditional cash-burn narrative associated with legacy OEM electrification. The firm is successfully extracting peak cash flow from its ICE dominance (25.3% SUV share, 43.6% tractor share) to subsidize the Born Electric ecosystem, AI matrix (Experience.AI, Efficiency.AI, Enterprise.AI), and its NU_IQ/DAVINCI ICE/SDV platforms. While the $1.33 billion off-balance-sheet contingent tax liability and $4.02 billion in internal EV RPTs require stringent auditor oversight, the core balance sheet's negligible 0.01x standalone D/E ratio provides a highly fortified moat against impending macroeconomic fragmentation.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*