Cyber Enviro-Tech Inc.: 2026 Capital Restructuring Near Dubai and Istanbul Hubs as Zero-Revenue Commercialization Signals Deep Solvency Crisis

Date : 2026-07-09

Reading : 185

HDIN Executive Takeaways

1. Cyber Enviro-Tech, Inc. recorded $0 in Q1 2026 revenue against an escalating $22.81 million accumulated deficit, functioning entirely via 7 external consultants while managing a $(2.33) million working capital shortfall.

2. Management’s strategic shift to the Middle Eastern distributed energy market involves a $2.5 million related-party distribution pact, directly exposing its Turkish and UAE outposts to acute operational execution barriers and severe geopolitical sanctions.

3. The corporate balance sheet faces imminent insolvency driven by $1.96 million in short-term convertible notes and a $30 million variable-rate equity line, legally mandating infinite dilution while compounding a $2.98 million marked-to-market derivative liability.

Figure Cyber Enviro-Tech Inc. (CETl): S-1 Institutional Diagnostic & Capital Structure Analysis

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

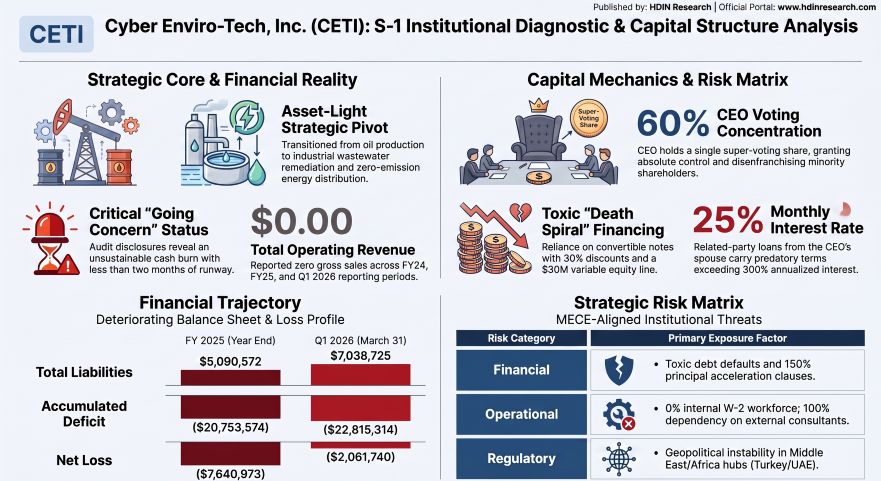

Cyber Enviro-Tech, Inc. [OTCQB: CETI] operates as a strictly pre-revenue entity following the October 14, 2025, spin-off of its legacy 479-acre, 33-well Alvey Oil Field in Callahan County, Texas. The divestiture to Texas Coastal Energy, Corp. and subsequent reverse merger into West Texas Resources, Inc. successfully removed a $343,500 note payable to the Estate of Danny Hyde from the balance sheet. However, the transaction crystallized severe value destruction, forcing a $(1,225,399) loss from discontinued operations (recognized as a $1,241,110 cash flow loss) and writing off $3.4 million in historical well development costs. The 8.6 million retained shares of West Texas Resources, Inc. carry a Level 3 fair value of $203,368, driving a further $(147,435) unrealized loss.

The core financial profile reflects an enterprise reliant on volatile external financing to sustain a cash burn rate of approximately $143,000 per month. Operational continuity remains threatened, resulting in an active "Going Concern" qualification from independent auditors.

Table Income Statement & Balance Sheet Trajectory (Reported in USD)

The Q1 2026 net loss includes massive non-cash distortions governed by U.S. GAAP (ASC 815). Despite reducing operating expenses to $413,290, Cyber Enviro-Tech, Inc. reported a net loss of $(2,061,740), driven almost entirely by a $(1,086,158) non-cash loss on the issuance of derivatives and a $(366,009) mark-to-market fair value reduction on existing derivative liabilities.

Asset Liquidations, R&D Contraction, and Legacy Impairments

* KAM Biotechnology Ltd IP Complete Impairment: Initially valued at $758,501 for a 10-year US license, the agreement was expanded globally via the issuance of 1,000,000 shares of common stock valued at $370,000, pushing the net capitalized intangible asset to $1,070,226 in 2023. Following the insolvency of KAM Biotechnology Ltd in 2024, Cyber Enviro-Tech, Inc. executed a 100% write-off of the remaining $957,377 asset.

* Axenic Subsidiary Dissolution: The 51%-owned commercial laundry remediation unit ceased operations on December 31, 2025, generating an $(18,451) loss. It left $14,482 in accrued "orphan" expenses on the balance sheet, accruing interest at an 8% annual rate.

* R&D Expense Contraction: Capital deployment for proprietary electrochemical and catalytic AI-integrated water filtration R&D contracted from $1.5 million in FY 2024 to $396,000 in FY 2025, reaching $0 for the three months ended March 31, 2026.

* Physical Asset Impairments: The company recognized a $579,957 impairment loss on legacy physical machinery in FY 2025 to reflect depreciated market valuations. Legacy asset retirement obligations attached to the Texas Railroad Commission ($62,537 bond for $160,000 in capping costs at $5,000 across 32 wells) were completely transferred off-book during the 2025 spin-off.

Infrastructure Layout and Regional Moats

Cyber Enviro-Tech, Inc. executes a highly decentralized operational footprint, managing the enterprise entirely through 7 part-time and full-time consultants with zero W-2 employees. The principal executive office is situated in Scottsdale, Arizona, with statutory domicile in Sheridan, Wyoming. To target a projected global industrial water treatment total addressable market (TAM) forecasted by Grand View Research to expand from $46.1 billion in 2024 to $71.6 billion by 2033, the company relies heavily on third-party validation networks, notably utilizing Texas Tech University for testing filtration metrics within the domestic meat-packing vertical.

International Expansion and CapEx Mandates

International commercial deployment strategy is anchored by wholly-owned subsidiaries and satellite outposts in Istanbul, Turkey, and Dubai, United Arab Emirates. Physical asset deployments currently consist solely of a $916,512 water filtration demonstration machine located in Mardin, Turkey, alongside a $115,000 ClO2 plant.

The geographic focus officially pivoted in February 2026 following an exclusive $2.5 million manufacturing and distribution agreement with related-party AirPower USA, targeting off-grid and military clean energy applications across the Middle East and Africa.

* Transaction Obligations: Cyber Enviro-Tech, Inc. provided a $600,000 initial deposit via Series A preferred stock, with subsequent cash obligations of $300,000 due in July 2026 and $1.6 million by December 2026.

* Collateralization: The company issued 5.5 million shares of common stock and 40,000 shares of Series A Preferred Stock as collateral.

* Manufacturing CapEx Requirements: Transitioning from an asset-light R&D unit to a scaled distributor mandates an immediate capital injection structured at $120,000 for a manufacturing facility, $100,000 for machinery, $200,000 for direct labor, and $400,000 for raw material procurement.

* Geopolitical Vulnerabilities: Management specifically notes that ongoing military and diplomatic conflicts between the United States and Iran place Middle Eastern deployment projections at immediate risk, potentially forcing the redirection of international deployment capital back to domestic operations.

HDIN Institutional Verdict

An audit of the Cyber Enviro-Tech, Inc. capital structure and corporate governance architecture reveals structural toxicity that mechanically guarantees infinite equity dilution while enriching related parties at the direct expense of common stockholders. The company operates under absolute autocratic control; CEO Kim D. Southworth (65) holds a single Special 2025 Series A Preferred Share that guarantees 60% voting control, nullifying minority shareholder influence and acting as a concrete anti-takeover barrier. The Board lacks Nasdaq-defined independence, counting AirPower USA CEO Brianna Stoecklein (38) and Don Gritten (43) among its members, following extreme financial leadership instability highlighted by the departure and subsequent reinstatement of CFO Dan Leboffe (68) to the advisory board, alongside the one-month tenure of former CFO Deborah Casper-Stone.

Death Spiral Financing and Predatory Debt Architecture

The company funds its $143,000 monthly burn rate through complex convertible mechanisms and high-interest related-party bridge loans that are systemically triggering covenant breaches. As of Q1 2026, Current Liabilities register at $3,252,435 against $922,296 in Current Assets. Net short-term convertible debt sits at $1,880,351, supplemented by $84,600 in related-party notes and $167,763 in standard short-term notes.

* Monroe Capital $30 Million Equity Purchase Agreement: Executed in March 2026, Monroe Street Capital Partners controls a 24-month Put option calculated at a 15% discount (85% of the lowest traded price over a five-day Valuation Period), constrained only by a $0.0005 floor and a 4.99% beneficial ownership limit. The agreement extracted an upfront fee of 3,000,000 Initial Commitment Shares, with 9,000,000 Fulfillment Commitment Shares due at $2.5 million, $5.0 million, and $7.5 million capital draw milestones.

* Lambda Ventures & Monroe Capital Convertibles: March and April 2026 issuances feature $275,000 in principal derived from $250,000 in cash (9.1% OID). These 12-month notes bear a guaranteed 7% interest rate. The debt converts at the lesser of $0.10 per share or 70% of the lowest traded price during the preceding 20 trading days. The transaction stripped 1,833,333 common stock warrants at $0.15 and 500,000 Note Commitment Shares. An additional April commercial note for $55,000 (7% interest) mirrors the 70% discount conversion terms and includes 366,667 warrants at $0.15.

* Institutional 2024/2025 Vintages: 2024 operations netted $2,582,650 across 47 notes (primarily 8% interest, fixed $0.10-$0.25 conversion), excluding a $150,000 10% note ($0.35 conversion) and $600,000 in 9-10% notes maturing in 2025/2026. 2025 activity netted $3,632,744 across 45 notes (8% interest, $0.08-$0.25 conversion), with seven specific notes totaling $714,744 structured at 12% interest maturing January 2027.

* Active Defaults and Acceleration Risk: Default events automatically accelerate repayment to 150% of outstanding principal on the 2026 convertibles. Active defaults include a legacy 2020 related-party note for $22,000 (convertible at $0.001) and a $153,989 loan issued by former President TJ Agardy at 12.5% interest. A May 6, 2026, loan for $25,000 defaulted within 20 days and accrues a $300 daily penalty.

* Predatory Related-Party Extractions: In early 2026, the company borrowed $65,600 from CEO spouse Kim N. Southworth, collateralized by $45,000 in equipment. This includes a $28,000 note carrying a 25% *monthly* interest rate for the initial 60 days, and two notes ($17,600 and $20,000) mandating $2,000 upfront fees and $1,000 monthly interest. These terms utterly invalidate management’s claims of standard arm's-length related-party transactions. External consulting fees paid to related parties registered $409,850 in FY 2024 and $421,510 in FY 2025, against broader general consulting expenditures of $1.66 million and $1.78 million, respectively.

* Additional Commercial Distress Facilities: A December 2023 $100,000 loan ($62,000 outstanding) requires a $7,500 cash fee and $250 daily interest ($50 cash, $200 in stock at $0.15). Four December 2025 revenue-share loans totaling $60,000 demand 10% of specific project net revenue until a 200% principal return is achieved, stripping 280,000 stock kickers. A February 2026 Payments Rights Agreement ($35,000) mandates $2,226 weekly payments over 25 weeks ($20,650 in interest). The company maintains a $55,000 line of credit at 8.5% and a $25,000 QuickBooks/WebBank LOC at 28.99%, both personally guaranteed by the CEO. An Essentia Funding $30,000 future receipts agreement (netting $18,000) breached prior covenants.

Legal and regulatory contingencies continue to accumulate. Cyber Enviro-Tech, Inc. received a formal notice of default on June 17, 2026, for failing to file its Form 10-Q. The company has failed to file its 2024 federal corporate tax return, threatening the viability of $19.7 million in Net Operating Loss carryforwards (currently fully offset by a valuation allowance). Furthermore, the company faces unaccrued West Fox SWD, LLC litigation risks involving an $80,000 settlement offer, and maintains two "zombie" consulting agreements that absorbed $100,000 in retainers with 5% future success fees attached to hypothetical £50 million and $25 million capital raises. A historical stock price guarantee generated a $190,000 liability in 2025, which was cleared in Q1 2026 via the issuance of 250,000 penalty shares.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. Cyber Enviro-Tech, Inc. recorded $0 in Q1 2026 revenue against an escalating $22.81 million accumulated deficit, functioning entirely via 7 external consultants while managing a $(2.33) million working capital shortfall.

2. Management’s strategic shift to the Middle Eastern distributed energy market involves a $2.5 million related-party distribution pact, directly exposing its Turkish and UAE outposts to acute operational execution barriers and severe geopolitical sanctions.

3. The corporate balance sheet faces imminent insolvency driven by $1.96 million in short-term convertible notes and a $30 million variable-rate equity line, legally mandating infinite dilution while compounding a $2.98 million marked-to-market derivative liability.

Figure Cyber Enviro-Tech Inc. (CETl): S-1 Institutional Diagnostic & Capital Structure Analysis

Segmental Realities and Margin CompressionCyber Enviro-Tech, Inc. [OTCQB: CETI] operates as a strictly pre-revenue entity following the October 14, 2025, spin-off of its legacy 479-acre, 33-well Alvey Oil Field in Callahan County, Texas. The divestiture to Texas Coastal Energy, Corp. and subsequent reverse merger into West Texas Resources, Inc. successfully removed a $343,500 note payable to the Estate of Danny Hyde from the balance sheet. However, the transaction crystallized severe value destruction, forcing a $(1,225,399) loss from discontinued operations (recognized as a $1,241,110 cash flow loss) and writing off $3.4 million in historical well development costs. The 8.6 million retained shares of West Texas Resources, Inc. carry a Level 3 fair value of $203,368, driving a further $(147,435) unrealized loss.

The core financial profile reflects an enterprise reliant on volatile external financing to sustain a cash burn rate of approximately $143,000 per month. Operational continuity remains threatened, resulting in an active "Going Concern" qualification from independent auditors.

Table Income Statement & Balance Sheet Trajectory (Reported in USD)

| Metric | FY2024 | FY2025 | Q1 2025 | Q1 2026 |

|---|---|---|---|---|

| Revenue | $0 | $0 | $0 | $0 |

| Operating Expenses | $2.85M | $3.12M (+9.4% YoY) | $0.88M | $0.41M (-53.3% YoY) |

| Net Loss | $(6.37M) | $(7.64M) | $(1.15M) | $(2.06M) |

| Cash & Cash Equivalents | $59.4K | $50.2K | N/A | $263.3K |

| Total Assets | $3.57M | $1.99M | N/A | $2.77M |

| Total Liabilities | $4.07M | $5.09M | N/A | $7.04M |

| Accumulated Deficit | $(13.13M) | $(20.75M) | N/A | $(22.82M) |

| Derivative Liability | $387.2K | $1.07M | N/A | $2.98M |

The Q1 2026 net loss includes massive non-cash distortions governed by U.S. GAAP (ASC 815). Despite reducing operating expenses to $413,290, Cyber Enviro-Tech, Inc. reported a net loss of $(2,061,740), driven almost entirely by a $(1,086,158) non-cash loss on the issuance of derivatives and a $(366,009) mark-to-market fair value reduction on existing derivative liabilities.

Asset Liquidations, R&D Contraction, and Legacy Impairments

* KAM Biotechnology Ltd IP Complete Impairment: Initially valued at $758,501 for a 10-year US license, the agreement was expanded globally via the issuance of 1,000,000 shares of common stock valued at $370,000, pushing the net capitalized intangible asset to $1,070,226 in 2023. Following the insolvency of KAM Biotechnology Ltd in 2024, Cyber Enviro-Tech, Inc. executed a 100% write-off of the remaining $957,377 asset.

* Axenic Subsidiary Dissolution: The 51%-owned commercial laundry remediation unit ceased operations on December 31, 2025, generating an $(18,451) loss. It left $14,482 in accrued "orphan" expenses on the balance sheet, accruing interest at an 8% annual rate.

* R&D Expense Contraction: Capital deployment for proprietary electrochemical and catalytic AI-integrated water filtration R&D contracted from $1.5 million in FY 2024 to $396,000 in FY 2025, reaching $0 for the three months ended March 31, 2026.

* Physical Asset Impairments: The company recognized a $579,957 impairment loss on legacy physical machinery in FY 2025 to reflect depreciated market valuations. Legacy asset retirement obligations attached to the Texas Railroad Commission ($62,537 bond for $160,000 in capping costs at $5,000 across 32 wells) were completely transferred off-book during the 2025 spin-off.

Infrastructure Layout and Regional Moats

Cyber Enviro-Tech, Inc. executes a highly decentralized operational footprint, managing the enterprise entirely through 7 part-time and full-time consultants with zero W-2 employees. The principal executive office is situated in Scottsdale, Arizona, with statutory domicile in Sheridan, Wyoming. To target a projected global industrial water treatment total addressable market (TAM) forecasted by Grand View Research to expand from $46.1 billion in 2024 to $71.6 billion by 2033, the company relies heavily on third-party validation networks, notably utilizing Texas Tech University for testing filtration metrics within the domestic meat-packing vertical.

International Expansion and CapEx Mandates

International commercial deployment strategy is anchored by wholly-owned subsidiaries and satellite outposts in Istanbul, Turkey, and Dubai, United Arab Emirates. Physical asset deployments currently consist solely of a $916,512 water filtration demonstration machine located in Mardin, Turkey, alongside a $115,000 ClO2 plant.

The geographic focus officially pivoted in February 2026 following an exclusive $2.5 million manufacturing and distribution agreement with related-party AirPower USA, targeting off-grid and military clean energy applications across the Middle East and Africa.

* Transaction Obligations: Cyber Enviro-Tech, Inc. provided a $600,000 initial deposit via Series A preferred stock, with subsequent cash obligations of $300,000 due in July 2026 and $1.6 million by December 2026.

* Collateralization: The company issued 5.5 million shares of common stock and 40,000 shares of Series A Preferred Stock as collateral.

* Manufacturing CapEx Requirements: Transitioning from an asset-light R&D unit to a scaled distributor mandates an immediate capital injection structured at $120,000 for a manufacturing facility, $100,000 for machinery, $200,000 for direct labor, and $400,000 for raw material procurement.

* Geopolitical Vulnerabilities: Management specifically notes that ongoing military and diplomatic conflicts between the United States and Iran place Middle Eastern deployment projections at immediate risk, potentially forcing the redirection of international deployment capital back to domestic operations.

HDIN Institutional Verdict

An audit of the Cyber Enviro-Tech, Inc. capital structure and corporate governance architecture reveals structural toxicity that mechanically guarantees infinite equity dilution while enriching related parties at the direct expense of common stockholders. The company operates under absolute autocratic control; CEO Kim D. Southworth (65) holds a single Special 2025 Series A Preferred Share that guarantees 60% voting control, nullifying minority shareholder influence and acting as a concrete anti-takeover barrier. The Board lacks Nasdaq-defined independence, counting AirPower USA CEO Brianna Stoecklein (38) and Don Gritten (43) among its members, following extreme financial leadership instability highlighted by the departure and subsequent reinstatement of CFO Dan Leboffe (68) to the advisory board, alongside the one-month tenure of former CFO Deborah Casper-Stone.

Death Spiral Financing and Predatory Debt Architecture

The company funds its $143,000 monthly burn rate through complex convertible mechanisms and high-interest related-party bridge loans that are systemically triggering covenant breaches. As of Q1 2026, Current Liabilities register at $3,252,435 against $922,296 in Current Assets. Net short-term convertible debt sits at $1,880,351, supplemented by $84,600 in related-party notes and $167,763 in standard short-term notes.

* Monroe Capital $30 Million Equity Purchase Agreement: Executed in March 2026, Monroe Street Capital Partners controls a 24-month Put option calculated at a 15% discount (85% of the lowest traded price over a five-day Valuation Period), constrained only by a $0.0005 floor and a 4.99% beneficial ownership limit. The agreement extracted an upfront fee of 3,000,000 Initial Commitment Shares, with 9,000,000 Fulfillment Commitment Shares due at $2.5 million, $5.0 million, and $7.5 million capital draw milestones.

* Lambda Ventures & Monroe Capital Convertibles: March and April 2026 issuances feature $275,000 in principal derived from $250,000 in cash (9.1% OID). These 12-month notes bear a guaranteed 7% interest rate. The debt converts at the lesser of $0.10 per share or 70% of the lowest traded price during the preceding 20 trading days. The transaction stripped 1,833,333 common stock warrants at $0.15 and 500,000 Note Commitment Shares. An additional April commercial note for $55,000 (7% interest) mirrors the 70% discount conversion terms and includes 366,667 warrants at $0.15.

* Institutional 2024/2025 Vintages: 2024 operations netted $2,582,650 across 47 notes (primarily 8% interest, fixed $0.10-$0.25 conversion), excluding a $150,000 10% note ($0.35 conversion) and $600,000 in 9-10% notes maturing in 2025/2026. 2025 activity netted $3,632,744 across 45 notes (8% interest, $0.08-$0.25 conversion), with seven specific notes totaling $714,744 structured at 12% interest maturing January 2027.

* Active Defaults and Acceleration Risk: Default events automatically accelerate repayment to 150% of outstanding principal on the 2026 convertibles. Active defaults include a legacy 2020 related-party note for $22,000 (convertible at $0.001) and a $153,989 loan issued by former President TJ Agardy at 12.5% interest. A May 6, 2026, loan for $25,000 defaulted within 20 days and accrues a $300 daily penalty.

* Predatory Related-Party Extractions: In early 2026, the company borrowed $65,600 from CEO spouse Kim N. Southworth, collateralized by $45,000 in equipment. This includes a $28,000 note carrying a 25% *monthly* interest rate for the initial 60 days, and two notes ($17,600 and $20,000) mandating $2,000 upfront fees and $1,000 monthly interest. These terms utterly invalidate management’s claims of standard arm's-length related-party transactions. External consulting fees paid to related parties registered $409,850 in FY 2024 and $421,510 in FY 2025, against broader general consulting expenditures of $1.66 million and $1.78 million, respectively.

* Additional Commercial Distress Facilities: A December 2023 $100,000 loan ($62,000 outstanding) requires a $7,500 cash fee and $250 daily interest ($50 cash, $200 in stock at $0.15). Four December 2025 revenue-share loans totaling $60,000 demand 10% of specific project net revenue until a 200% principal return is achieved, stripping 280,000 stock kickers. A February 2026 Payments Rights Agreement ($35,000) mandates $2,226 weekly payments over 25 weeks ($20,650 in interest). The company maintains a $55,000 line of credit at 8.5% and a $25,000 QuickBooks/WebBank LOC at 28.99%, both personally guaranteed by the CEO. An Essentia Funding $30,000 future receipts agreement (netting $18,000) breached prior covenants.

Legal and regulatory contingencies continue to accumulate. Cyber Enviro-Tech, Inc. received a formal notice of default on June 17, 2026, for failing to file its Form 10-Q. The company has failed to file its 2024 federal corporate tax return, threatening the viability of $19.7 million in Net Operating Loss carryforwards (currently fully offset by a valuation allowance). Furthermore, the company faces unaccrued West Fox SWD, LLC litigation risks involving an $80,000 settlement offer, and maintains two "zombie" consulting agreements that absorbed $100,000 in retainers with 5% future success fees attached to hypothetical £50 million and $25 million capital raises. A historical stock price guarantee generated a $190,000 liability in 2025, which was cleared in Q1 2026 via the issuance of 250,000 penalty shares.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."