iOThree Limited: Software-as-a-Service Pivot Near Kallang Way as 360-Basis-Point Gross Margin Expansion Signals Asset-Light Viability Amid Semiconductor Constraints

Date : 2026-07-10

Reading : 109

HDIN Executive Takeaways

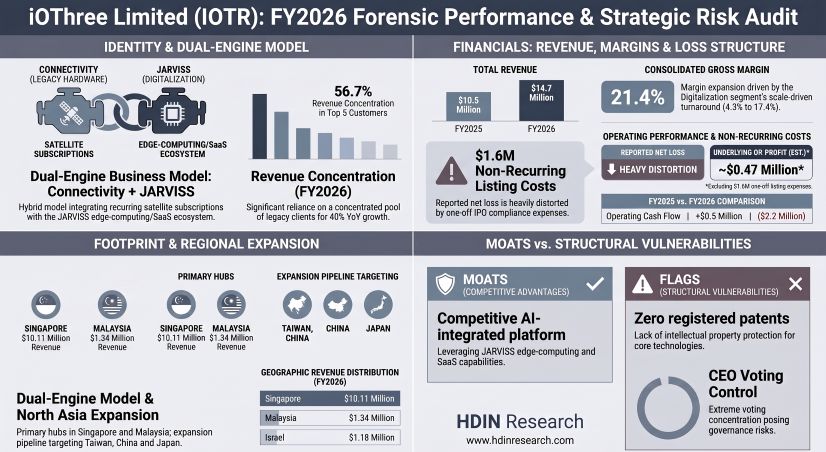

1. iOThree Limited expanded FY2026 revenue by 40.0% to $14.7 million, catalyzed by a 110.5% surge in digitalization platforms, offsetting structural declines in legacy hardware leasing.

2. Operations in Kallang Way and Johor Bahru face severe supplier concentration; five operators control 46.5% of costs amid volatile South China Sea semiconductor supply lines.

3. A 96.89% voting consolidation under the CEO artificially depresses institutional index inclusion, while a $2.2 million operating cash burn limits the liquidity runway to 11 months.

Figure iOThree Limited (lOTR): FY2026 Forensic Performance & Strategic Risk Audit

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

iOThree Limited [NASDAQ: IOTR] executed a deliberate transition from CapEx-heavy hardware deployments to OpEx-driven subscription models during FY2026, driving a 360-basis-point expansion in total gross margin from 17.8% to 21.4%.

Despite reporting a net loss of $1.16 million (expanding from a $0.23 million net loss in FY2025) on total operating expenses of $4.28 million, the core business model demonstrates underlying profitability. Forensic deconstruction of the $1.13 million reported operating loss reveals $1.6 million in non-recurring initial public offering compliance costs, comprising legal and investor relations fees. Normalizing for these one-off expenses yields a positive core operating profit of $0.47 million. Baseline general and administrative costs expanded by $0.8 million primarily due to headcount acquisition, while sales and marketing expenditures remained flat at $0.58 million.

FY2026 Top-Line and Segmental Breakdown:

* Total Revenue: $14.7 million (Up 40.0% from $10.5 million in FY2025).

* Digitalization and Other Solutions: $8.07 million (Up 110.5% from $3.82 million). Propelled by a $3.3 million expansion in IT equipment and services. Segment gross margin expanded from 4.3% to 17.4%. Subscription income specific to this segment totaled $1.41 million.

* Satellite Connectivity Solutions: $6.64 million (Down 0.3% from $6.66 million). Gross margin stabilized at 26.3% (up from 25.5%). High-margin recurring subscription revenue expanded 15.9% to $5.09 million, effectively offsetting a 30.4% contraction in hardware sales and leases, which fell to $1.55 million.

Capital Architecture and Cash Flow Variations:

* Operating Cash Flow: Negative $2.2 million (reversing from a positive $0.5 million in FY2025). Driven by working capital drains, specifically a $1.1 million expansion in deposits/prepayments and a $0.4 million inventory buildup.

* Liquidity Reserve: $2.1 million in cash and cash equivalents against $2.5 million in working capital. Liquidity was bolstered by financing inflows of $3.6 million in net IPO proceeds and $1.4 million via a private placement issuing 2,298,852 Ordinary Shares.

* Liabilities & Debt: Bank borrowings stand at $376,704, secured by insider guarantees carrying zero guarantee fees. Related-party unsecured, non-interest-bearing insider loans of $329,427 were fully repaid, clearing the balance to zero.

* R&D Capitalization: Software under development on the balance sheet totaled $89,923 (expanding from $32,311 in FY2025). The firm recorded a $75,315 write-off for aborted software development costs.

* Accounts Receivable Risk: Aging profiles indicate structural health, with less than 90-day typical aging and only $80,000 exceeding 60 days overdue, requiring zero bad debt reserves. However, two corporate customers command 23.4% of total accounts receivable and sales-type lease investments.

Geographic Revenue Matrix:

* Singapore: $10.11 million (Up 93.0% from $5.23 million in FY2025).

* Malaysia: $1.34 million.

* Israel: $1.18 million.

* Vietnam: $0.51 million.

* Indonesia: $0.31 million.

* Thailand: $0.11 million.

* Taiwan, China: $0.06 million (Down from $0.24 million in FY2025).

* United Kingdom: $0.30 million.

* Republic of Marshall Islands: $0.32 million.

Infrastructure Layout and Regional Moats

The operational footprint of iOThree Limited is heavily concentrated in Southeast Asia, structured to leverage lower-cost IT contracting while maintaining proximity to core maritime hubs. Physical infrastructure obligations are entirely capitalized under ASC 842, totaling $1.20 million in lease liabilities.

Asset-Light Facility Commitments:

* Singapore Headquarters: The principal executive office, product development center, and primary warehouse operate out of 161 Kallang Way, #07-01 and #07-08. This is secured by an operating lease spanning September 15, 2025, to September 14, 2028.

* Malaysia Operations: On April 23, 2025, iOThree Limited incorporated wholly-owned subsidiary iO3 Sdn. Bhd. The firm executed a 24-month tenancy agreement (September 15, 2025, to September 14, 2027) for office and dormitory space at 24 Jalan Wisata, Straits View, Johor Bahru, explicitly to house dedicated IT contractors.

* Liability Structure: Operating lease liabilities equal $919,392 ($374,248 current; $545,144 non-current). Finance lease liabilities covering procurement of deployment equipment equal $282,512 ($193,092 current; $89,420 non-current). Undiscounted lease payments due within the next 12 months remain strictly under $1.0 million.

Supply Chain Architecture and Technology Integrations:

The firm operates as an open-infrastructure integrator utilizing open-source software, rendering it entirely dependent on upstream oligopolies. The top five suppliers command 46.5% of the total cost of sales (historically reaching 50.1%). Bandwidth capacity relies on Inmarsat and Starlink (integrated in 2024), exposing gross margins to orbital network degradation and bandwidth pricing volatility. Physical deployment of JARVISS edge devices, modems, and multi-satellite orbit electronic steering antennas remains highly vulnerable to semiconductor shortages linked to Taiwan Strait and South China Sea geopolitical frictions.

Rather than committing upfront capital to localized global offices, iOThree Limited mitigates geographical entry costs via third-party distributors in Taiwan, China, Vietnam, Indonesia, and Thailand, alongside a May 2025 strategic collaboration with Deckhouse Communications targeting the Turkish and Middle Eastern maritime sectors.

Proprietary Platform Validation:

The F.R.I.D.A.Y. ERP system, launched on May 1, 2024, operates alongside the JARVISS platform and V.Suite applications. The architecture relies heavily on third-party integration: V.SECURE operates via Cydome technology (meeting ISO 27001 and ISO 27017 standards), V.MAIL utilizes ESET endpoint anti-virus, and V.IoT integrates embedded carbon reporting parameters. The company itself holds ISO 9001 and ISO 14001 certifications and secured validation from an international classification society for its planned maintenance software.

HDIN Institutional Verdict

While iOThree Limited has successfully executed a margin-accretive shift into digitalization, the structural architecture of the equity remains precarious for U.S. institutional investors. The firm is caught in a "structural squeeze." On the supply side, five providers dictate nearly half of all direct costs. On the demand side, customer concentration is accelerating at an unsustainable velocity; the top five customers accounted for 56.7% of total FY2026 revenue, expanding from 44.0% in FY2025 and 34.1% in FY2024. This confirms that top-line expansion is currently reliant on upselling an entrenched, concentrated client pool rather than achieving decentralized global market penetration.

Compounding operational risks is a highly asymmetric corporate governance framework. As a Cayman Islands-domiciled "controlled company" and "foreign private issuer," the company is exempt from standard U.S. domestic governance protocols. The dual-class equity structure grants Class A shares a 50:1 voting premium. Through iO3 Strategic Investments Limited (holding 1,428,240 Class A shares, or 78.0% of the class and 75.48% of aggregate voting power) and All Wealthy International Limited (holding 403,435 Class A shares and 89,285 Ordinary Shares), Chief Executive Officer Eng Chye Koh commands an absolute 96.89% voting monopoly. Notably, while Koh holds only 51% of the economic rights in iO3 Strategic Investments Limited—alongside Joanna Hui Cheng Soh (20%), Wei Meng See (10%), Zhenhua Yin (10%), and Loo Koon Goh (9%)—he retains sole dispositive control. Soh’s resignation from the board on January 20, 2026, and the subsequent appointments of independent directors Yangan Ou and Yufei Li do not structurally alter this voting asymmetry, which legally disenfranchises minority shareholders and blocks index inclusion.

Technologically, the platform lacks a defensible intellectual property moat. iOThree Limited possesses zero registered patents and zero software copyrights, relying exclusively on trademark protection for "JARVISS" across the EU, UK, Japan, Singapore, and Taiwan, China. The utilization of open-source software introduces imminent risks of mandatory proprietary code disclosure. With a negative $2.2 million operating cash flow capping the liquidity runway at 11 to 12 months, aggressive internal R&D scale-up is paralyzed, dictating that future growth and technical defensibility must be sourced through targeted Southeast Asian M&A rather than organic engineering.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. iOThree Limited expanded FY2026 revenue by 40.0% to $14.7 million, catalyzed by a 110.5% surge in digitalization platforms, offsetting structural declines in legacy hardware leasing.

2. Operations in Kallang Way and Johor Bahru face severe supplier concentration; five operators control 46.5% of costs amid volatile South China Sea semiconductor supply lines.

3. A 96.89% voting consolidation under the CEO artificially depresses institutional index inclusion, while a $2.2 million operating cash burn limits the liquidity runway to 11 months.

Figure iOThree Limited (lOTR): FY2026 Forensic Performance & Strategic Risk Audit

Segmental Realities and Margin CompressioniOThree Limited [NASDAQ: IOTR] executed a deliberate transition from CapEx-heavy hardware deployments to OpEx-driven subscription models during FY2026, driving a 360-basis-point expansion in total gross margin from 17.8% to 21.4%.

Despite reporting a net loss of $1.16 million (expanding from a $0.23 million net loss in FY2025) on total operating expenses of $4.28 million, the core business model demonstrates underlying profitability. Forensic deconstruction of the $1.13 million reported operating loss reveals $1.6 million in non-recurring initial public offering compliance costs, comprising legal and investor relations fees. Normalizing for these one-off expenses yields a positive core operating profit of $0.47 million. Baseline general and administrative costs expanded by $0.8 million primarily due to headcount acquisition, while sales and marketing expenditures remained flat at $0.58 million.

FY2026 Top-Line and Segmental Breakdown:

* Total Revenue: $14.7 million (Up 40.0% from $10.5 million in FY2025).

* Digitalization and Other Solutions: $8.07 million (Up 110.5% from $3.82 million). Propelled by a $3.3 million expansion in IT equipment and services. Segment gross margin expanded from 4.3% to 17.4%. Subscription income specific to this segment totaled $1.41 million.

* Satellite Connectivity Solutions: $6.64 million (Down 0.3% from $6.66 million). Gross margin stabilized at 26.3% (up from 25.5%). High-margin recurring subscription revenue expanded 15.9% to $5.09 million, effectively offsetting a 30.4% contraction in hardware sales and leases, which fell to $1.55 million.

Capital Architecture and Cash Flow Variations:

* Operating Cash Flow: Negative $2.2 million (reversing from a positive $0.5 million in FY2025). Driven by working capital drains, specifically a $1.1 million expansion in deposits/prepayments and a $0.4 million inventory buildup.

* Liquidity Reserve: $2.1 million in cash and cash equivalents against $2.5 million in working capital. Liquidity was bolstered by financing inflows of $3.6 million in net IPO proceeds and $1.4 million via a private placement issuing 2,298,852 Ordinary Shares.

* Liabilities & Debt: Bank borrowings stand at $376,704, secured by insider guarantees carrying zero guarantee fees. Related-party unsecured, non-interest-bearing insider loans of $329,427 were fully repaid, clearing the balance to zero.

* R&D Capitalization: Software under development on the balance sheet totaled $89,923 (expanding from $32,311 in FY2025). The firm recorded a $75,315 write-off for aborted software development costs.

* Accounts Receivable Risk: Aging profiles indicate structural health, with less than 90-day typical aging and only $80,000 exceeding 60 days overdue, requiring zero bad debt reserves. However, two corporate customers command 23.4% of total accounts receivable and sales-type lease investments.

Geographic Revenue Matrix:

* Singapore: $10.11 million (Up 93.0% from $5.23 million in FY2025).

* Malaysia: $1.34 million.

* Israel: $1.18 million.

* Vietnam: $0.51 million.

* Indonesia: $0.31 million.

* Thailand: $0.11 million.

* Taiwan, China: $0.06 million (Down from $0.24 million in FY2025).

* United Kingdom: $0.30 million.

* Republic of Marshall Islands: $0.32 million.

Infrastructure Layout and Regional Moats

The operational footprint of iOThree Limited is heavily concentrated in Southeast Asia, structured to leverage lower-cost IT contracting while maintaining proximity to core maritime hubs. Physical infrastructure obligations are entirely capitalized under ASC 842, totaling $1.20 million in lease liabilities.

Asset-Light Facility Commitments:

* Singapore Headquarters: The principal executive office, product development center, and primary warehouse operate out of 161 Kallang Way, #07-01 and #07-08. This is secured by an operating lease spanning September 15, 2025, to September 14, 2028.

* Malaysia Operations: On April 23, 2025, iOThree Limited incorporated wholly-owned subsidiary iO3 Sdn. Bhd. The firm executed a 24-month tenancy agreement (September 15, 2025, to September 14, 2027) for office and dormitory space at 24 Jalan Wisata, Straits View, Johor Bahru, explicitly to house dedicated IT contractors.

* Liability Structure: Operating lease liabilities equal $919,392 ($374,248 current; $545,144 non-current). Finance lease liabilities covering procurement of deployment equipment equal $282,512 ($193,092 current; $89,420 non-current). Undiscounted lease payments due within the next 12 months remain strictly under $1.0 million.

Supply Chain Architecture and Technology Integrations:

The firm operates as an open-infrastructure integrator utilizing open-source software, rendering it entirely dependent on upstream oligopolies. The top five suppliers command 46.5% of the total cost of sales (historically reaching 50.1%). Bandwidth capacity relies on Inmarsat and Starlink (integrated in 2024), exposing gross margins to orbital network degradation and bandwidth pricing volatility. Physical deployment of JARVISS edge devices, modems, and multi-satellite orbit electronic steering antennas remains highly vulnerable to semiconductor shortages linked to Taiwan Strait and South China Sea geopolitical frictions.

Rather than committing upfront capital to localized global offices, iOThree Limited mitigates geographical entry costs via third-party distributors in Taiwan, China, Vietnam, Indonesia, and Thailand, alongside a May 2025 strategic collaboration with Deckhouse Communications targeting the Turkish and Middle Eastern maritime sectors.

Proprietary Platform Validation:

The F.R.I.D.A.Y. ERP system, launched on May 1, 2024, operates alongside the JARVISS platform and V.Suite applications. The architecture relies heavily on third-party integration: V.SECURE operates via Cydome technology (meeting ISO 27001 and ISO 27017 standards), V.MAIL utilizes ESET endpoint anti-virus, and V.IoT integrates embedded carbon reporting parameters. The company itself holds ISO 9001 and ISO 14001 certifications and secured validation from an international classification society for its planned maintenance software.

HDIN Institutional Verdict

While iOThree Limited has successfully executed a margin-accretive shift into digitalization, the structural architecture of the equity remains precarious for U.S. institutional investors. The firm is caught in a "structural squeeze." On the supply side, five providers dictate nearly half of all direct costs. On the demand side, customer concentration is accelerating at an unsustainable velocity; the top five customers accounted for 56.7% of total FY2026 revenue, expanding from 44.0% in FY2025 and 34.1% in FY2024. This confirms that top-line expansion is currently reliant on upselling an entrenched, concentrated client pool rather than achieving decentralized global market penetration.

Compounding operational risks is a highly asymmetric corporate governance framework. As a Cayman Islands-domiciled "controlled company" and "foreign private issuer," the company is exempt from standard U.S. domestic governance protocols. The dual-class equity structure grants Class A shares a 50:1 voting premium. Through iO3 Strategic Investments Limited (holding 1,428,240 Class A shares, or 78.0% of the class and 75.48% of aggregate voting power) and All Wealthy International Limited (holding 403,435 Class A shares and 89,285 Ordinary Shares), Chief Executive Officer Eng Chye Koh commands an absolute 96.89% voting monopoly. Notably, while Koh holds only 51% of the economic rights in iO3 Strategic Investments Limited—alongside Joanna Hui Cheng Soh (20%), Wei Meng See (10%), Zhenhua Yin (10%), and Loo Koon Goh (9%)—he retains sole dispositive control. Soh’s resignation from the board on January 20, 2026, and the subsequent appointments of independent directors Yangan Ou and Yufei Li do not structurally alter this voting asymmetry, which legally disenfranchises minority shareholders and blocks index inclusion.

Technologically, the platform lacks a defensible intellectual property moat. iOThree Limited possesses zero registered patents and zero software copyrights, relying exclusively on trademark protection for "JARVISS" across the EU, UK, Japan, Singapore, and Taiwan, China. The utilization of open-source software introduces imminent risks of mandatory proprietary code disclosure. With a negative $2.2 million operating cash flow capping the liquidity runway at 11 to 12 months, aggressive internal R&D scale-up is paralyzed, dictating that future growth and technical defensibility must be sourced through targeted Southeast Asian M&A rather than organic engineering.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."