Einride AB: 2026 Fleet Autonomy Pivot Near Gothenburg as a 77.9% Net Loss Surge Signals Acute 14-Month Liquidity Ceiling

Date : 2026-07-10

Reading : 185

HDIN Executive Takeaways

1. A 98.3% SPAC redemption rate drained $183.9 million from the trust, anchoring Einride AB's liquidity to a $113.3 million PIPE injection that sustains a $110.55 million pro forma cash balance against a $7.70 million trailing monthly cash burn, implying a rigid 14.3-month survival runway.

2. Accelerated deployments of 216 Connected Electric Trucks (CETs) drove Cost of Sales up 26.6% year-over-year, triggering a 10.1 percentage point gross margin collapse to -46.9% and expanding net losses to $175.57 million.

3. A $92 million contracted Annual Recurring Revenue (ARR) base faces geopolitical friction as Strait of Hormuz blockades halt United Arab Emirates port operations, while $800 million in Joint Business Plan (JBP) pipelines lack binding commitments amidst escalating 10-35% US import tariffs.

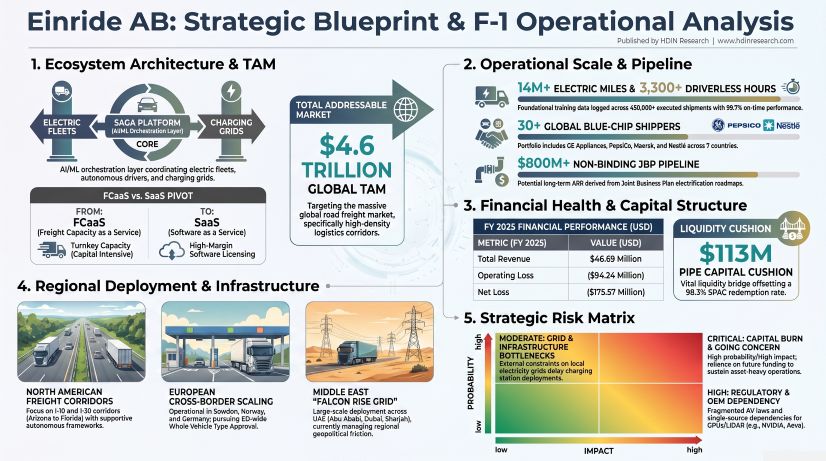

Figure Einride AB: Strategic Blueprint & F-1 operational Analysis

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

Einride AB [NASDAQ: ENRD] strictly bifurcates its revenue model under IFRS 15 (Transport Services) and IFRS 16 (Rental Income). At present, 100% of generated revenue flows from its capital-intensive Freight-Capacity-as-a-Service (FCaaS) model, while the asset-light Software-as-a-Service (SaaS) model—launched in the second half of 2025—will not record recognizable revenue until late 2026. The financial architecture demonstrates severe negative operating leverage, driven by hardware procurement costs outpacing freight service rate realization.

Total revenue generation exhibits high geographic concentration. Operations span seven United Nations-recognized member states, yielding $16.38 million (35.1%) in Sweden, $12.58 million (26.9%) in the United States, and $9.31 million (19.9%) in Germany. The remaining $8.42 million (18.0%) stems collectively from the United Arab Emirates, Norway, Austria, and the Netherlands. All IFRS 16 rental income is derived exclusively from the United States.

The 77.9% expansion in net losses was directly accelerated by a 202% surge in finance costs to $69.06 million, triggered by early convertible debenture conversions and high-yield factoring facilities holding a $36.19 million liability against future receivables. The balance sheet recorded a $13.18 million fair value loss on derivative liabilities. Operations exposed the firm to dual-layered currency volatility: operating FX recorded a $445,442 loss against a $1,153,274 gain, while finance FX recorded an $8,754,946 loss against a $143,076 gain. However, translation effects from the Swedish Krona to the US Dollar improved the Foreign Currency Translation Reserve from ($4,086,274) in 2024 to $2,440,649 in 2025, providing a $6,527,024 non-cash positive boost to Total Comprehensive Income.

Despite 3,308 logged driverless hours and over 14,000,000 accumulated electric miles executing 450,000 shipments with a 99.7% on-time performance rate, the balance sheet records exactly $0 in intangible software assets (down from $31,817 in 2024). A rigid R&D expensing policy forced $33,635,019 of software development costs for the Saga platform directly onto the 2025 income statement (compared to $35,595,962 in 2024). Deferred revenue liabilities dropped from $2,549,765 to $194,473.

Einride relies on "take-or-pay" FCaaS contracts providing 3-to-5-year revenue floors, which secured an Annual Recurring Revenue (ARR) base of $92 million by February 2026 (building on a $49 million run-rate closing out 2025). The top five customers across its 30-shipper cohort—which includes General Electric Appliances, DP World, Mars, PepsiCo, and Carlsberg—concentrate 43% of total revenue. F-1 disclosures highlight a clerical discrepancy here, citing this sum as either $19.78 million or $20.17 million. A joint study with the Fraunhofer Institute documented a 13% reduction in Total Cost of Ownership (TCO) compared to diesel, achieving a 16% reduction in required fleet size, a 10% gain in transport volumes, a 30% increase in pallets per truck, a 73% cut in charging times, and a 50% improvement in charger utilization. Autonomous execution trims emissions by up to 94%.

Infrastructure Layout and Regional Moats

Hardware infrastructure remains heavily asset-bound. The balance sheet holds $81.32 million in Property, Plant & Equipment (PP&E), $58.99 million in Right-of-Use assets, and $65.53 million in total lease liabilities, contrasting standard corporate debt of just $1.66 million. Physical footprints include an 8,000 sq. ft. headquarters in Stockholm, secondary offices in Gothenburg and Austin, and virtual footprints in the UAE. The firm owns 104,000 sq. ft. in Laholm and 90,000 sq. ft. in Hallsberg strictly for charging station construction.

The operational fleet numbers 216 CETs and 3 cab-less Autonomous Trucks, with management targeting an eventual base of 15,000 CETs and 5,000 autonomous solutions. The supply chain relies on a multi-OEM procurement strategy pulling chassis from Daimler, Scania, and BYD, while exposing the firm to severe single-source bottleneck risks for NVIDIA GPUs and Aeva LiDAR arrays. Competitively, the hardware platform faces Kodiak Robotics, Aurora Innovation, Bot Auto, Waabi, Torc, and PlusAI.

Geographic routing prioritizes the I-10 and I-20 logistics corridors in the US, autonomous cross-border freight routes in Norway, and the Falcon Rise Grid covering Abu Dhabi, Dubai, and Sharjah. However, geopolitical military escalation and blockades at the Strait of Hormuz have explicitly paused deployments at the Port of Jebel Ali. Additional macro constraints involve 10-35% fentanyl-related tariffs on imports from China, Canada, and Mexico, plus Section 232 and 301 tariffs on steel and aluminum.

Einride conducts interrelated transactions via a 9% equity stake in Polar Charge AB. In 2025, Einride invoiced the joint venture -$92,494 for construction (down from $3,655,517 in 2024), while simultaneously paying Polar $719,763 in asset lease payments (up from $606,058). This arrangement generated Right-of-Use assets of $10.11 million and corresponding lease liabilities of $10.93 million. Furthermore, Einride carved out its design business to a related party for $3,714,586, retaining a 19% equity stake alongside a 3-year service agreement. European operations are also leveraged; a NOK 18 million term loan from Pareto Bank ASA to Einride Norway AS requires a NOK 5 million parent guarantee and a NOK 20 million asset pledge. The 4-year facility mandates NOK 1 million quarterly payments (NOK 4 million annually) at an effective 9.53% interest rate (NIBOR 3M plus 5%).

HDIN Institutional Verdict

Einride AB executes a market entry strategy severely handicapped by mechanical capital structure overhangs and deficient Internal Controls over Financial Reporting (ICFR). Ernst & Young AB issued a formal "going concern" explanatory paragraph, accompanied by three un-remediated material weaknesses in business process, Information Technology General Controls (ITGCs), and Segregation of Duties (SoD). Operationally, Einride is locked in litigation with Maersk over contract terminations, highlighting the fragility of logistics Service Level Agreements (SLAs).

The Business Combination with Legato Merger Corp. III valued the firm at a $1.35 billion pre-money equity value ($10.90 per share). However, a 98.3% redemption rate drained $183.9 million, leaving a nominal $3.3 million in trust proceeds. Operations are now solely tethered to historical cash of $28.43 million (up from $7.56 million in 2024) and a $113.3 million PIPE investment.

Common equity faces extreme dilution protocols engineered to protect institutional downside. The structure contains 10.34 million Public Warrants ($11.50 strike), 18.35 million PIPE Warrants ($10.90 strike), 2.16 million Pre-Funded Warrants, and 6.941402 million Amazon Logistics Specified Warrants ($34.00 strike). If Einride issues equity below $9.20 accounting for >60% of trust proceeds, Public Warrants adjust to 115% of the higher market value. More acutely, PIPE warrants carry a VWAP-based floor adjustment down to $5.00, or a direct downward match if aggregate proceeds exceeding $500,000 are issued at a lower price.

The 2026 Equity Incentive Plan authorizes a 7.5% issuance with a 5% evergreen clause initiating in 2027. Stock options vest over 3 years, while warrants vest over 33 months with 3-to-5-year expirations. Executive insiders retain 12,177,090 shares (8.52% of outstanding). Founder Robert Falck holds 6.41% (9,116,010 shares) via Navisalma AB and extracts consulting fees via Navisoptus AB ($152,968 initial month; $12,747 monthly). CEO Roozbeh Charli (42) holds 1,164,205 shares (<1%) but benefits from a 2.0% post-closing anti-dilution true-up clause. CFO Anubhav Verma (40) brings SPAC mechanics experience from Exela Technologies and MicroVision. Director Gary Hicok secures $8,000 monthly plus a 0.25% equity award, while Gen. (Ret.) Keith B. Alexander holds a 1.2% equity award via Overlord Investments, LLC. SPAC Sponsor Eric Rosenfeld extracts $20,000 monthly for administrative services via Crescendo Advisors II, previously floating $146,785 in promissory notes. Lorne Abony secured 1,013,620 ADSs ($275,000 cash plus 0.8% equity).

Ultimately, Einride’s survival depends on converting an unbinding $800 million Joint Business Plan (JBP) pipeline into hard SaaS contracts before its 14.3-month liquidity runway evaporates. Conversion faces fierce structural headwinds, including lack of European Whole Vehicle Type Approval (WVTA) harmonization and aggressive lobbying by the International Brotherhood of Teamsters across 20 US states, as well as the European Transport Workers’ Federation (ETF), demanding human-in-the-vehicle mandates.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. A 98.3% SPAC redemption rate drained $183.9 million from the trust, anchoring Einride AB's liquidity to a $113.3 million PIPE injection that sustains a $110.55 million pro forma cash balance against a $7.70 million trailing monthly cash burn, implying a rigid 14.3-month survival runway.

2. Accelerated deployments of 216 Connected Electric Trucks (CETs) drove Cost of Sales up 26.6% year-over-year, triggering a 10.1 percentage point gross margin collapse to -46.9% and expanding net losses to $175.57 million.

3. A $92 million contracted Annual Recurring Revenue (ARR) base faces geopolitical friction as Strait of Hormuz blockades halt United Arab Emirates port operations, while $800 million in Joint Business Plan (JBP) pipelines lack binding commitments amidst escalating 10-35% US import tariffs.

Figure Einride AB: Strategic Blueprint & F-1 operational Analysis

Segmental Realities and Margin CompressionEinride AB [NASDAQ: ENRD] strictly bifurcates its revenue model under IFRS 15 (Transport Services) and IFRS 16 (Rental Income). At present, 100% of generated revenue flows from its capital-intensive Freight-Capacity-as-a-Service (FCaaS) model, while the asset-light Software-as-a-Service (SaaS) model—launched in the second half of 2025—will not record recognizable revenue until late 2026. The financial architecture demonstrates severe negative operating leverage, driven by hardware procurement costs outpacing freight service rate realization.

Table 1: Income Statement & Cash Flow Metrics (FY2025 vs. FY2024)

| Income Statement & Cash Flow Metric | FY2025 (USD) | FY2024 (USD) | Variance / YoY Change |

|---|---|---|---|

| Total Revenue | $46.69M | $39.61M | +17.9% |

| Cost of Sales | ($68.58M) | ($54.18M) | +26.6% |

| Gross Profit | ($21.89M) | ($14.57M) | -50.2% |

| Gross Margin | -46.9% | -36.8% | -10.1 percentage points |

| Operating Loss | ($94.24M) | ($87.26M) | +8.0% |

| Net Loss | ($175.57M) | ($98.68M) | +77.9% |

| Operating Cash Flow (OCF) | ($75.64M) | ($39.73M) | +90.3% |

| Capital Expenditures (CapEx) | ($16.78M) | ($16.86M) | -0.4% |

| Total Free Cash Flow Burn | ($92.42M) | ($56.59M) | +63.3% |

| Implied Monthly Cash Burn | ($7.70M) | ($4.72M) | +63.1% |

Total revenue generation exhibits high geographic concentration. Operations span seven United Nations-recognized member states, yielding $16.38 million (35.1%) in Sweden, $12.58 million (26.9%) in the United States, and $9.31 million (19.9%) in Germany. The remaining $8.42 million (18.0%) stems collectively from the United Arab Emirates, Norway, Austria, and the Netherlands. All IFRS 16 rental income is derived exclusively from the United States.

The 77.9% expansion in net losses was directly accelerated by a 202% surge in finance costs to $69.06 million, triggered by early convertible debenture conversions and high-yield factoring facilities holding a $36.19 million liability against future receivables. The balance sheet recorded a $13.18 million fair value loss on derivative liabilities. Operations exposed the firm to dual-layered currency volatility: operating FX recorded a $445,442 loss against a $1,153,274 gain, while finance FX recorded an $8,754,946 loss against a $143,076 gain. However, translation effects from the Swedish Krona to the US Dollar improved the Foreign Currency Translation Reserve from ($4,086,274) in 2024 to $2,440,649 in 2025, providing a $6,527,024 non-cash positive boost to Total Comprehensive Income.

Despite 3,308 logged driverless hours and over 14,000,000 accumulated electric miles executing 450,000 shipments with a 99.7% on-time performance rate, the balance sheet records exactly $0 in intangible software assets (down from $31,817 in 2024). A rigid R&D expensing policy forced $33,635,019 of software development costs for the Saga platform directly onto the 2025 income statement (compared to $35,595,962 in 2024). Deferred revenue liabilities dropped from $2,549,765 to $194,473.

Einride relies on "take-or-pay" FCaaS contracts providing 3-to-5-year revenue floors, which secured an Annual Recurring Revenue (ARR) base of $92 million by February 2026 (building on a $49 million run-rate closing out 2025). The top five customers across its 30-shipper cohort—which includes General Electric Appliances, DP World, Mars, PepsiCo, and Carlsberg—concentrate 43% of total revenue. F-1 disclosures highlight a clerical discrepancy here, citing this sum as either $19.78 million or $20.17 million. A joint study with the Fraunhofer Institute documented a 13% reduction in Total Cost of Ownership (TCO) compared to diesel, achieving a 16% reduction in required fleet size, a 10% gain in transport volumes, a 30% increase in pallets per truck, a 73% cut in charging times, and a 50% improvement in charger utilization. Autonomous execution trims emissions by up to 94%.

Infrastructure Layout and Regional Moats

Hardware infrastructure remains heavily asset-bound. The balance sheet holds $81.32 million in Property, Plant & Equipment (PP&E), $58.99 million in Right-of-Use assets, and $65.53 million in total lease liabilities, contrasting standard corporate debt of just $1.66 million. Physical footprints include an 8,000 sq. ft. headquarters in Stockholm, secondary offices in Gothenburg and Austin, and virtual footprints in the UAE. The firm owns 104,000 sq. ft. in Laholm and 90,000 sq. ft. in Hallsberg strictly for charging station construction.

The operational fleet numbers 216 CETs and 3 cab-less Autonomous Trucks, with management targeting an eventual base of 15,000 CETs and 5,000 autonomous solutions. The supply chain relies on a multi-OEM procurement strategy pulling chassis from Daimler, Scania, and BYD, while exposing the firm to severe single-source bottleneck risks for NVIDIA GPUs and Aeva LiDAR arrays. Competitively, the hardware platform faces Kodiak Robotics, Aurora Innovation, Bot Auto, Waabi, Torc, and PlusAI.

Geographic routing prioritizes the I-10 and I-20 logistics corridors in the US, autonomous cross-border freight routes in Norway, and the Falcon Rise Grid covering Abu Dhabi, Dubai, and Sharjah. However, geopolitical military escalation and blockades at the Strait of Hormuz have explicitly paused deployments at the Port of Jebel Ali. Additional macro constraints involve 10-35% fentanyl-related tariffs on imports from China, Canada, and Mexico, plus Section 232 and 301 tariffs on steel and aluminum.

Einride conducts interrelated transactions via a 9% equity stake in Polar Charge AB. In 2025, Einride invoiced the joint venture -$92,494 for construction (down from $3,655,517 in 2024), while simultaneously paying Polar $719,763 in asset lease payments (up from $606,058). This arrangement generated Right-of-Use assets of $10.11 million and corresponding lease liabilities of $10.93 million. Furthermore, Einride carved out its design business to a related party for $3,714,586, retaining a 19% equity stake alongside a 3-year service agreement. European operations are also leveraged; a NOK 18 million term loan from Pareto Bank ASA to Einride Norway AS requires a NOK 5 million parent guarantee and a NOK 20 million asset pledge. The 4-year facility mandates NOK 1 million quarterly payments (NOK 4 million annually) at an effective 9.53% interest rate (NIBOR 3M plus 5%).

HDIN Institutional Verdict

Einride AB executes a market entry strategy severely handicapped by mechanical capital structure overhangs and deficient Internal Controls over Financial Reporting (ICFR). Ernst & Young AB issued a formal "going concern" explanatory paragraph, accompanied by three un-remediated material weaknesses in business process, Information Technology General Controls (ITGCs), and Segregation of Duties (SoD). Operationally, Einride is locked in litigation with Maersk over contract terminations, highlighting the fragility of logistics Service Level Agreements (SLAs).

The Business Combination with Legato Merger Corp. III valued the firm at a $1.35 billion pre-money equity value ($10.90 per share). However, a 98.3% redemption rate drained $183.9 million, leaving a nominal $3.3 million in trust proceeds. Operations are now solely tethered to historical cash of $28.43 million (up from $7.56 million in 2024) and a $113.3 million PIPE investment.

Common equity faces extreme dilution protocols engineered to protect institutional downside. The structure contains 10.34 million Public Warrants ($11.50 strike), 18.35 million PIPE Warrants ($10.90 strike), 2.16 million Pre-Funded Warrants, and 6.941402 million Amazon Logistics Specified Warrants ($34.00 strike). If Einride issues equity below $9.20 accounting for >60% of trust proceeds, Public Warrants adjust to 115% of the higher market value. More acutely, PIPE warrants carry a VWAP-based floor adjustment down to $5.00, or a direct downward match if aggregate proceeds exceeding $500,000 are issued at a lower price.

The 2026 Equity Incentive Plan authorizes a 7.5% issuance with a 5% evergreen clause initiating in 2027. Stock options vest over 3 years, while warrants vest over 33 months with 3-to-5-year expirations. Executive insiders retain 12,177,090 shares (8.52% of outstanding). Founder Robert Falck holds 6.41% (9,116,010 shares) via Navisalma AB and extracts consulting fees via Navisoptus AB ($152,968 initial month; $12,747 monthly). CEO Roozbeh Charli (42) holds 1,164,205 shares (<1%) but benefits from a 2.0% post-closing anti-dilution true-up clause. CFO Anubhav Verma (40) brings SPAC mechanics experience from Exela Technologies and MicroVision. Director Gary Hicok secures $8,000 monthly plus a 0.25% equity award, while Gen. (Ret.) Keith B. Alexander holds a 1.2% equity award via Overlord Investments, LLC. SPAC Sponsor Eric Rosenfeld extracts $20,000 monthly for administrative services via Crescendo Advisors II, previously floating $146,785 in promissory notes. Lorne Abony secured 1,013,620 ADSs ($275,000 cash plus 0.8% equity).

Ultimately, Einride’s survival depends on converting an unbinding $800 million Joint Business Plan (JBP) pipeline into hard SaaS contracts before its 14.3-month liquidity runway evaporates. Conversion faces fierce structural headwinds, including lack of European Whole Vehicle Type Approval (WVTA) harmonization and aggressive lobbying by the International Brotherhood of Teamsters across 20 US states, as well as the European Transport Workers’ Federation (ETF), demanding human-in-the-vehicle mandates.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."