AEON Biopharma, Inc.: Structural Financing and Daewoong Monopsony Expose Equity Viability Amid $482.6M Deficit and NYSE Delisting Risk

Date : 2026-07-13

Reading : 292

HDIN Executive Takeaways

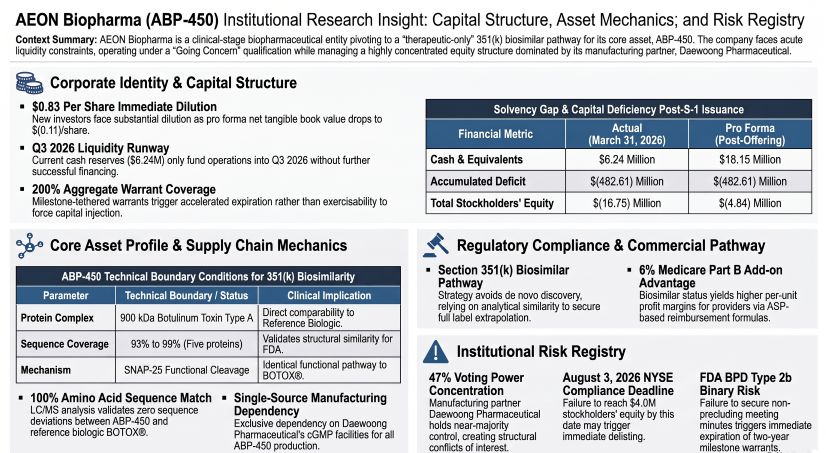

1. AEON Biopharma, Inc. [NYSE American: AEON] faces acute insolvency with $6.24 million in actual cash and a $(482.61) million accumulated deficit; its 17.48 million-share offering priced at $0.7151 per share enforces an immediate $0.83 per share net tangible book value dilution.

2. Daewoong Pharmaceutical Co., Ltd. exercises monopsony control over the supply chain, holding 47% of voting power (11.91 million common shares) while executing exclusive cGMP manufacturing of the 900 kDa complex for U.S., Canada, and EU therapeutic markets.

3. Institutional listing requires clearing a strict August 3, 2026, $4.0 million NYSE American equity compliance threshold and validating a 100% amino acid sequence match to unlock $26.9 million in milestone warrants critical to surviving past Q3 2026.

Figure AEON Biopharma (ABP-450) lnstitutional Research lnsight: Capital Structure, Asset Mechanics and Risk Registry

Capitalization Dynamics and Liquidity Constraints

Capitalization Dynamics and Liquidity Constraints

AEON Biopharma, Inc. is operating under a formal "going concern" warning issued by independent auditor KPMG LLP, triggered by recurring operating losses and negative cash flows. Management confirms that without external intervention, the existing cash runway expires in the third quarter of 2026.

To bridge operations to March 31, 2027, the company is executing a highly dilutive, firm commitment offering of 17,479,373 shares of Common Stock (with Pre-Funded Warrants available for investors facing 4.99% or 9.99% beneficial ownership caps). Driven by distress pricing mechanics, new investors face immediate value destruction. Based on an assumed public offering price of $0.7151 per share, the transaction yields just $11.0 million in estimated net proceeds ($12.8 million if the over-allotment is fully exercised). This capitalization reset drives the pro forma net tangible book value immediately to a deficit of $(4.84) million, or $(0.11) per share, representing an instantaneous dilution of $0.83 per share to new capital. The financial model remains highly sensitive to market execution: every $1.00 decrease in the assumed offering price erodes the total capitalization and pro forma net tangible book value by $16.4 million, while reducing new investor dilution by $0.34 per share.

The financing structure relies on 200% aggregate milestone-contingent warrant coverage structured to force capital injection upon regulatory validation:

* Two-Year Milestone Warrants (100% Coverage): 17,479,373 warrants with an assumed $0.7151 exercise price. Expiration accelerates to 45 days after the FDA provides Type 2B meeting minutes that do not preclude Section 351(k) advancement.

* Five-Year Milestone Warrants (100% Coverage): 17,479,373 warrants with an assumed $0.8224 exercise price. Expiration accelerates to 45 days post-initiation of a Phase 3 clinical equivalence trial against the reference product, BOTOX® (onabotulinumtoxinA).

Failure to trigger these milestones deprives the entity of up to $26.9 million in potential aggregate gross proceeds, virtually ensuring insolvency as out-of-the-money warrants expire with zero value.

The company trades with a ".BC" (below compliance) indicator, following a formal March 31, 2026 non-compliance notice regarding NYSE American Section 1003(a)(ii). The exchange flagged a stockholders' deficit of approximately $55 million as of December 31, 2025, falling below the mandatory $4.0 million threshold (compounding a February 7, 2025 notice regarding a $2.0 million requirement). The exchange mandates compliance by August 3, 2026, to avert delisting.

Biosimilar Architecture and Monopsonistic Supply Interdependence

AEON Biopharma, Inc.’s entire commercial thesis hinges on a single asset: ABP-450, a 900 kDa botulinum toxin type A complex. Rather than pursuing a de novo 351(a) clinical discovery track, the company is deploying a therapeutic-only Section 351(k) biosimilar strategy targeting the 12 FDA-approved therapeutic indications currently monopolized by BOTOX®.

Structurally isolating the biologic for therapeutic applications allows AEON Biopharma, Inc. to insulate its Average Selling Price (ASP) from lower-priced aesthetic applications. Within the Medicare Part B "buy-and-bill" framework, this mathematically incentivizes provider adoption via a 6% add-on payment calculated against the higher-priced reference product's ASP. The global therapeutic market is projected to reach $3.5 billion in 2026 at an 8% CAGR (per Clarivate 2025 data). AEON Biopharma, Inc.'s identical toxin complex is already distributed aesthetically by Evolus, Inc. as Jeuveau® (U.S.) and Nuceiva® (Canada/EU), backed by an Evolus safety database of 2,100 adult subjects, with global biosimilar approvals active in Mexico, India, and the Philippines.

To clear the 351(k) hurdle, liquid chromatography/mass spectrometry (LC/MS) testing must permanently maintain a 100% amino acid sequence match across over 3,400 amino acids, maintaining 93% to 99% coverage for the five constituent proteins. Quality controls dictate zero tolerance for deviations in vial-to-vial ELISA composition, in vivo biological activity (LD50), cell-based potency assays (CBPA), and SNAP-25 functional cleavage. Following a Q3 2024 initial meeting and a January 2026 BPD Type 2a meeting, the FDA confirmed these analytical methodologies appear reasonable. The critical BPD Type 2b meeting is slated for H2 2026.

Operationally, the entity is tethered to Daewoong Pharmaceutical Co., Ltd. via an exclusive License and Supply Agreement granting U.S., Canada, EU, and UK commercial rights. Daewoong operates as the sole-source manufacturer utilizing FDA, EMA, and Health Canada authorized cGMP facilities. This relationship translates into immense structural entanglements. On January 21, 2026, to satisfy up to $15.0 million in March 2024 Senior Secured Convertible "Old Notes," the company issued Daewoong 11,918,380 common shares, 11,236,631 pre-funded warrants, a $1.5 million "New Note," and 8,000,000 standard warrants (strike price $1.09392). The New Note reserves 3,268,860 shares for conversion at an assumed $1.00 conversion price. Consequently, Daewoong controls approximately 47% of the 25,303,058 outstanding voting shares as of March 31, 2026, while maintaining a first-priority security interest across substantially all corporate assets.

Historical operational freedom relies entirely on a June 21, 2021 Settlement and License Agreement with Medytox, Inc. (amended May 5, 2022) to resolve toxin origin disputes, alongside an October 2025 Odeon Settlement Agreement involving the issuance of Odeon Warrants. (Prior July 2023 business combination interim notes have already been converted to Common Stock).

HDIN Institutional Verdict and Structural Governance

The institutional audit identifies severe misalignment between executive compensation, governance architecture, and the common shareholder base. AEON Biopharma, Inc. utilizes 409A deferred compensation structures and relies on an aggregate equity pool containing 11,377,317 Restricted Stock Units (RSUs) and 158,005 stock options carrying an inflated weighted-average exercise price of $296.85. Compensation is dictated by 2019, 2023, and 2025 Incentive Award Plans, with 208,657 Contingent Consideration Shares tethered to a December 2022 business combination agreement. Active employment agreements govern President and CEO Robert Bancroft (April 2025), CFO John Bencich (March 2026), CAO Jennifer Sy (March 2026), and CLO Alex Wilson (July 2023).

Despite the precarious $6.24 million cash position, the Board of Directors—comprising Chairman Jost Fischer, Robert Palmisano, Shelley Thunen, consultant Eric Carter, M.D., Seongsoo Park, and former executive Marc Forth—operates a highly entrenched classified structure (Classes I, II, and III) with staggered three-year terms. Management retains the authority to issue 1,000,000 shares of "blank check" Preferred Stock as a poison pill.

The HDIN verdict concludes that AEON Biopharma, Inc. is functionally operating as a captive financing vehicle for Daewoong Pharmaceutical Co., Ltd. Daewoong's dual position as a secured creditor and dominant 47% voting shareholder structurally nullifies the influence of independent equity holders. Institutional viability relies entirely on flawlessly executing the H2 2026 FDA Type 2b meeting to trigger cash execution on the $26.9 million milestone warrants before the August 3, 2026 NYSE delisting deadline truncates retail and institutional liquidity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer: This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

1. AEON Biopharma, Inc. [NYSE American: AEON] faces acute insolvency with $6.24 million in actual cash and a $(482.61) million accumulated deficit; its 17.48 million-share offering priced at $0.7151 per share enforces an immediate $0.83 per share net tangible book value dilution.

2. Daewoong Pharmaceutical Co., Ltd. exercises monopsony control over the supply chain, holding 47% of voting power (11.91 million common shares) while executing exclusive cGMP manufacturing of the 900 kDa complex for U.S., Canada, and EU therapeutic markets.

3. Institutional listing requires clearing a strict August 3, 2026, $4.0 million NYSE American equity compliance threshold and validating a 100% amino acid sequence match to unlock $26.9 million in milestone warrants critical to surviving past Q3 2026.

Figure AEON Biopharma (ABP-450) lnstitutional Research lnsight: Capital Structure, Asset Mechanics and Risk Registry

Capitalization Dynamics and Liquidity ConstraintsAEON Biopharma, Inc. is operating under a formal "going concern" warning issued by independent auditor KPMG LLP, triggered by recurring operating losses and negative cash flows. Management confirms that without external intervention, the existing cash runway expires in the third quarter of 2026.

To bridge operations to March 31, 2027, the company is executing a highly dilutive, firm commitment offering of 17,479,373 shares of Common Stock (with Pre-Funded Warrants available for investors facing 4.99% or 9.99% beneficial ownership caps). Driven by distress pricing mechanics, new investors face immediate value destruction. Based on an assumed public offering price of $0.7151 per share, the transaction yields just $11.0 million in estimated net proceeds ($12.8 million if the over-allotment is fully exercised). This capitalization reset drives the pro forma net tangible book value immediately to a deficit of $(4.84) million, or $(0.11) per share, representing an instantaneous dilution of $0.83 per share to new capital. The financial model remains highly sensitive to market execution: every $1.00 decrease in the assumed offering price erodes the total capitalization and pro forma net tangible book value by $16.4 million, while reducing new investor dilution by $0.34 per share.

The financing structure relies on 200% aggregate milestone-contingent warrant coverage structured to force capital injection upon regulatory validation:

* Two-Year Milestone Warrants (100% Coverage): 17,479,373 warrants with an assumed $0.7151 exercise price. Expiration accelerates to 45 days after the FDA provides Type 2B meeting minutes that do not preclude Section 351(k) advancement.

* Five-Year Milestone Warrants (100% Coverage): 17,479,373 warrants with an assumed $0.8224 exercise price. Expiration accelerates to 45 days post-initiation of a Phase 3 clinical equivalence trial against the reference product, BOTOX® (onabotulinumtoxinA).

Failure to trigger these milestones deprives the entity of up to $26.9 million in potential aggregate gross proceeds, virtually ensuring insolvency as out-of-the-money warrants expire with zero value.

Table Balance Sheet & Capitalization Metrics (As of March 31, 2026)

| Balance Sheet & Capitalization Metric | Actual (As of March 31, 2026) | Pro Forma As Adjusted |

|---|---|---|

| Cash & Cash Equivalents | $6.24M | $18.15M |

| Accumulated Deficit | ($482.61M) | ($482.61M) |

| Total Stockholders' Equity (Deficit) | ($16.75M) | ($4.84M) |

| Total Capitalization | $8.63M | $20.54M |

The company trades with a ".BC" (below compliance) indicator, following a formal March 31, 2026 non-compliance notice regarding NYSE American Section 1003(a)(ii). The exchange flagged a stockholders' deficit of approximately $55 million as of December 31, 2025, falling below the mandatory $4.0 million threshold (compounding a February 7, 2025 notice regarding a $2.0 million requirement). The exchange mandates compliance by August 3, 2026, to avert delisting.

Biosimilar Architecture and Monopsonistic Supply Interdependence

AEON Biopharma, Inc.’s entire commercial thesis hinges on a single asset: ABP-450, a 900 kDa botulinum toxin type A complex. Rather than pursuing a de novo 351(a) clinical discovery track, the company is deploying a therapeutic-only Section 351(k) biosimilar strategy targeting the 12 FDA-approved therapeutic indications currently monopolized by BOTOX®.

Structurally isolating the biologic for therapeutic applications allows AEON Biopharma, Inc. to insulate its Average Selling Price (ASP) from lower-priced aesthetic applications. Within the Medicare Part B "buy-and-bill" framework, this mathematically incentivizes provider adoption via a 6% add-on payment calculated against the higher-priced reference product's ASP. The global therapeutic market is projected to reach $3.5 billion in 2026 at an 8% CAGR (per Clarivate 2025 data). AEON Biopharma, Inc.'s identical toxin complex is already distributed aesthetically by Evolus, Inc. as Jeuveau® (U.S.) and Nuceiva® (Canada/EU), backed by an Evolus safety database of 2,100 adult subjects, with global biosimilar approvals active in Mexico, India, and the Philippines.

To clear the 351(k) hurdle, liquid chromatography/mass spectrometry (LC/MS) testing must permanently maintain a 100% amino acid sequence match across over 3,400 amino acids, maintaining 93% to 99% coverage for the five constituent proteins. Quality controls dictate zero tolerance for deviations in vial-to-vial ELISA composition, in vivo biological activity (LD50), cell-based potency assays (CBPA), and SNAP-25 functional cleavage. Following a Q3 2024 initial meeting and a January 2026 BPD Type 2a meeting, the FDA confirmed these analytical methodologies appear reasonable. The critical BPD Type 2b meeting is slated for H2 2026.

Operationally, the entity is tethered to Daewoong Pharmaceutical Co., Ltd. via an exclusive License and Supply Agreement granting U.S., Canada, EU, and UK commercial rights. Daewoong operates as the sole-source manufacturer utilizing FDA, EMA, and Health Canada authorized cGMP facilities. This relationship translates into immense structural entanglements. On January 21, 2026, to satisfy up to $15.0 million in March 2024 Senior Secured Convertible "Old Notes," the company issued Daewoong 11,918,380 common shares, 11,236,631 pre-funded warrants, a $1.5 million "New Note," and 8,000,000 standard warrants (strike price $1.09392). The New Note reserves 3,268,860 shares for conversion at an assumed $1.00 conversion price. Consequently, Daewoong controls approximately 47% of the 25,303,058 outstanding voting shares as of March 31, 2026, while maintaining a first-priority security interest across substantially all corporate assets.

Historical operational freedom relies entirely on a June 21, 2021 Settlement and License Agreement with Medytox, Inc. (amended May 5, 2022) to resolve toxin origin disputes, alongside an October 2025 Odeon Settlement Agreement involving the issuance of Odeon Warrants. (Prior July 2023 business combination interim notes have already been converted to Common Stock).

HDIN Institutional Verdict and Structural Governance

The institutional audit identifies severe misalignment between executive compensation, governance architecture, and the common shareholder base. AEON Biopharma, Inc. utilizes 409A deferred compensation structures and relies on an aggregate equity pool containing 11,377,317 Restricted Stock Units (RSUs) and 158,005 stock options carrying an inflated weighted-average exercise price of $296.85. Compensation is dictated by 2019, 2023, and 2025 Incentive Award Plans, with 208,657 Contingent Consideration Shares tethered to a December 2022 business combination agreement. Active employment agreements govern President and CEO Robert Bancroft (April 2025), CFO John Bencich (March 2026), CAO Jennifer Sy (March 2026), and CLO Alex Wilson (July 2023).

Despite the precarious $6.24 million cash position, the Board of Directors—comprising Chairman Jost Fischer, Robert Palmisano, Shelley Thunen, consultant Eric Carter, M.D., Seongsoo Park, and former executive Marc Forth—operates a highly entrenched classified structure (Classes I, II, and III) with staggered three-year terms. Management retains the authority to issue 1,000,000 shares of "blank check" Preferred Stock as a poison pill.

The HDIN verdict concludes that AEON Biopharma, Inc. is functionally operating as a captive financing vehicle for Daewoong Pharmaceutical Co., Ltd. Daewoong's dual position as a secured creditor and dominant 47% voting shareholder structurally nullifies the influence of independent equity holders. Institutional viability relies entirely on flawlessly executing the H2 2026 FDA Type 2b meeting to trigger cash execution on the $26.9 million milestone warrants before the August 3, 2026 NYSE delisting deadline truncates retail and institutional liquidity.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer: This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*