Embention: 2026 Euronext Growth Pivot Near Alicante as 972% Inventory Expansion Signals Imminent UAV Serial Production Rate

Date : 2026-07-13

Reading : 158

HDIN Executive Takeaways

1. An aggressive 972% inventory expansion to $1.44 million (€1.27 million) insulates operations against aerospace supply chain bottlenecks, mitigating dependency on a 270-supplier network where the top vendor commands 19.7% of procurement volume.

2. The capitalization of $2.07 million (€1.84 million) in internal engineering costs artificially bolsters the 45.0% operating margin, deferring $6.96 million (€6.16 million) in intangible amortization risks to future fiscal cycles.

3. The planned July 2026 transfer to Euronext Growth Paris serves as a capital conduit to finance subsidiary build-outs in Abu Dhabi, Los Angeles, and Austria, aimed at structurally diversifying the current 75.6% revenue reliance on the Americas.

Figure Embention: Scaling the Brain of Autonomous Flight

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

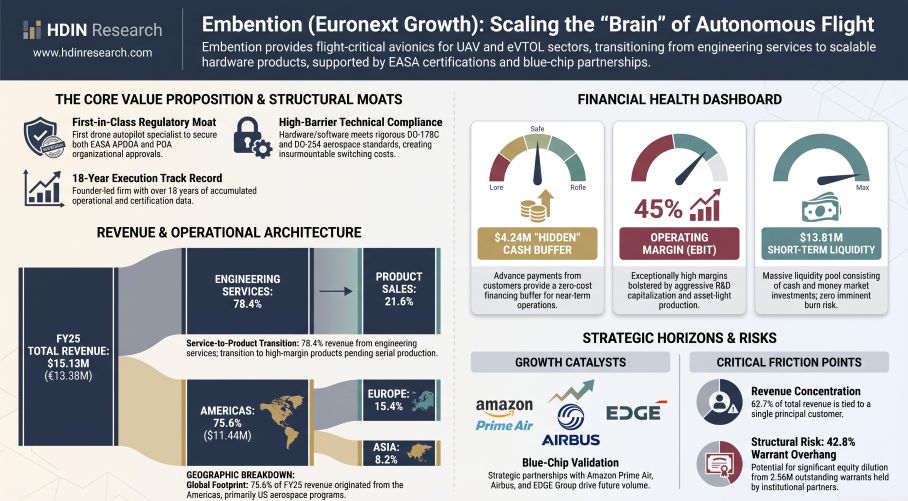

Embention [Euronext Growth: EMB] currently operates an engineering-bottlenecked financial model, functioning primarily as a bespoke technical consultancy for aerospace Original Equipment Manufacturers (OEMs) navigating multi-year certification phases. Total top-line revenue expanded 9.2% year-over-year, climbing from $13.85 million (€12.25 million) in FY24 to $15.13 million (€13.38 million) in FY25.

The quality of these earnings is heavily skewed toward pre-commercial engineering hours rather than high-margin serial hardware sales. Services revenue (integration, Hardware-in-the-Loop [HIL] / Software-in-the-Loop [SIL] configuration, and certification support) generated $11.85 million (€10.49 million), representing 78.4% of total revenue. Product sales, encompassing certified hardware modules, accounted for 21.6% at $3.27 million (€2.90 million), an 8.0% year-over-year contraction reflecting the industry's delayed transition from prototype development to serial manufacturing.

To execute this service-heavy mandate, Embention expanded its headcount from 160 to 242 employees, driving personnel expenses up 13.1% to $6.44 million (€5.70 million). Operating profit (EBIT) grew 8.8% to $6.81 million (€6.03 million), yielding a 45.0% operating margin. Adding back $0.77 million (€0.68 million) in depreciation and amortization generates an implied EBITDA proxy of $7.58 million (€6.71 million). Net income registered at $5.65 million (€5.00 million), a 4.6% expansion hampered by a higher effective tax rate of 17.7% (up from 14.5% in FY24) and $1.41 million (€1.25 million) in cash tax payments. Operating cash flow contracted from $7.79 million (€6.89 million) in FY24 to $6.25 million (€5.53 million) in FY25.

Capital Structure and Working Capital Metrics (1 EUR = 1.1306 USD)

* Total Liquidity: $13.81 million (€12.22 million), consisting of $2.39 million (€2.12 million) in cash/equivalents and $11.42 million (€10.10 million) in short-term financial investments.

* Accounts Receivable: Grew 40.8% to $3.07 million (€2.71 million). Direct trade invoices account for $2.03 million (€1.80 million), while non-operational receivables (public grants and VAT) comprise $1.02 million (€0.90 million).

* Accounts Payable: Surged 58.7% to $5.65 million (€5.00 million). This includes $387,262 (€342,528) in sundry payables and $13,968 (€12,355) owed to controlling entity Albedo Ventures, S.L.

* Zero-Cost Execution Buffer: Customer advance payments account for $4.24 million (€3.75 million) of total payables, providing immediate working capital but creating execution liabilities for pending development services.

* Financial Debt: Total debt stands at $3.96 million (€3.50 million), split between $2.44 million (€2.16 million) long-term and $1.52 million (€1.34 million) short-term.

* Soft Loans: Bank borrowings total $2.50 million (€2.21 million) backed by ICO and Afin SGR guarantees. These carry deeply suppressed interest rates: BBVA and Banco Sabadell (1.50%), Caja Rural (1.80%), and Banco Santander (2.84%).

* Public Subsidies: The balance sheet carries $1.40 million (€1.24 million) in conditionally repayable liabilities tied to R&D milestones, contrasted against $2.73 million (€2.41 million) in non-repayable equity grants.

* Capital Expenditure: Physical PP&E CapEx absorbed just $0.21 million (€0.19 million), while intangible R&D investments consumed $2.28 million (€2.02 million). Operating leases and external rents totaled $2.22 million (€1.97 million).

Infrastructure Layout and Regional Moats

Embention’s operational architecture is headquartered in Alicante, Spain. The primary facility houses high-value electronic manufacturing, climate chambers, vibration tables, and a private airfield dedicated to iron-bird testing. Since its inception in 2007 (originating from the Flamingo project), the firm has accumulated an 18-year operational track record, utilizing a strict capitalization policy where $2.07 million to $2.08 million (€1.84 million) of FY25 internal R&D was activated onto the balance sheet. This expands total intangible assets to $7.20 million (€6.37 million).

To secure raw inputs, the company procures components from over 270 global suppliers. The top supplier constitutes 19.7% of procurement ($533,000 / €471,384), and the second-largest accounts for 7.2%. Reacting to macroeconomic supply constraints, management executed a 972% expansion in physical inventory, growing stockpiles from $0.13 million–$0.14 million (€0.12 million) in FY24 to $1.43 million–$1.44 million (€1.27 million) in FY25. There are zero recorded provisions for environmental liabilities.

Geographic revenue is severely concentrated in the Americas, which generated 75.6% of FY25 sales ($11.44 million / €10.12 million). Europe accounts for 15.4% ($2.33 million / €2.06 million), with the Spanish domestic market providing merely 3% of product and 2% of service sales, while the broader EU drives 25% of product and 4% of service sales. Asia contributed 8.2% ($1.24 million / €1.10 million), with Oceania ($0.06 million / €0.05 million) and Africa ($0.05 million / €0.05 million) delivering sub-0.1% volumes. To localize production and diversify this geographic matrix, Embention established three new entities: Embention Avionics Components and System Manufacture LLC SPC (Abu Dhabi, UAE - 2025), Embention USA Inc (Los Angeles, USA - 2026), and Embention DACH GmbH (Austria).

The product suite encompasses the Veronte Autopilot ecosystem (1x, 4x, DRx, KAI), Vision Based Navigation (VBN), datalinks (SDL, XDL24), I/O expansion modules (CEx, MEx, Serial, Stick), DC-DC converters, motor inverters (MC110), gimbal controls (MC01), and control stations (LCS/PCS).

Commercial penetration is driven exclusively by aerospace regulatory lock-in. Embention is the first drone autopilot specialist to secure European Union Aviation Safety Agency (EASA) Alternative Procedures to Design Organisation Approval (APDOA) and Production Organisation Approval (POA). Its systems conform to DO-178C (ED-12) for software, DO-254 (ED-80) for hardware, and DO-160G for environmental conditions. Additionally, it achieved LufABw VVZ1/VVZ2 certification in Germany and ANAC approval in Brazil. This multi-year certification lag (historically requiring six years from 2007 to 2013) forms the ultimate barrier to entry against niche peers (UAV Navigation/Grupo Oesía, MicroPilot) and indirect Tier-1 integrators (Honeywell, Collins Aerospace/RTX, Thales, BAE Systems).

HDIN Institutional Verdict

While Embention demonstrates formidable gross profitability and an unlevered operational cash profile, its commercial dependency introduces acute vulnerability. Out of a historic base of over 600 clients across 70 countries (with more than 100 active billing customers in FY25), a single blue-chip entity generated 62.7% of total revenue ($9.48 million / €8.39 million). The top five customers cumulatively drive 76.0% of all sales.

The latent commercial pipeline relies on specific platform maturation milestones. Embention’s avionics are currently integrated into Amazon Prime Air (MK30 logistics program), Airbus (Skyways project), EDGE Group (defense collaboration), Lift Aircraft (Hexa eVTOL), EMT (LUNA NG tactical UAV), Israel Aerospace Industries (Air Hopper), Honda, Rheinmetall, and BAE Systems. Once these platforms secure regulatory approval and exit the trial phase, Embention projects a shift from one-off engineering billings to recurring serial product sales.

Corporate governance and capital structure mechanics expose minority shareholders to severe overhang risks. The ultimate beneficial owner, David Julián Benavente Sánchez, commands a 44.97% economic interest (0.44% direct, and 44.53% indirect via holding company Albedo Ventures, S.L., which retains 63.88% of Embention). Institutional backer Axon Innovation Growth IV, F.C.R. holds 29.02%. The company maintains 3.36% in treasury stock (201,018 shares), leaving a highly restricted minority float of 3.74%. Executive compensation remains minimal, with the Board of Directors receiving $79,932 (€70,699). Employee retention is managed via a stock option plan requiring five years of seniority, valued at $0.57 million (€0.51 million), with 11,133 shares delivered from treasury in FY25.

The transition to Euronext Growth Paris lacks institutional-grade safeguards, notably operating without independent audit or remuneration committees and enforcing zero post-listing lock-up agreements. Furthermore, latent dilution mechanisms are aggressive. Axon holds a $565,302 (€500,002) convertible loan yielding 3.5%, maturing in February 2026. This mandate forces the issuance of 57,871 new shares, representing 0.958% dilution at a pre-money valuation of $58.44 million (€51.69 million). Separately, active warrants held by Axon and a third-party commercial partner authorize the subscription of up to 2,560,000 new shares. If exercised, this will expand total share capital by 42.8%, diluting the base from 5,982,684 to 8,542,682 shares. Until these overhangs clear, equity upside remains heavily capped despite the firm's unassailable regulatory moats.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. An aggressive 972% inventory expansion to $1.44 million (€1.27 million) insulates operations against aerospace supply chain bottlenecks, mitigating dependency on a 270-supplier network where the top vendor commands 19.7% of procurement volume.

2. The capitalization of $2.07 million (€1.84 million) in internal engineering costs artificially bolsters the 45.0% operating margin, deferring $6.96 million (€6.16 million) in intangible amortization risks to future fiscal cycles.

3. The planned July 2026 transfer to Euronext Growth Paris serves as a capital conduit to finance subsidiary build-outs in Abu Dhabi, Los Angeles, and Austria, aimed at structurally diversifying the current 75.6% revenue reliance on the Americas.

Figure Embention: Scaling the Brain of Autonomous Flight

Segmental Realities and Margin CompressionEmbention [Euronext Growth: EMB] currently operates an engineering-bottlenecked financial model, functioning primarily as a bespoke technical consultancy for aerospace Original Equipment Manufacturers (OEMs) navigating multi-year certification phases. Total top-line revenue expanded 9.2% year-over-year, climbing from $13.85 million (€12.25 million) in FY24 to $15.13 million (€13.38 million) in FY25.

The quality of these earnings is heavily skewed toward pre-commercial engineering hours rather than high-margin serial hardware sales. Services revenue (integration, Hardware-in-the-Loop [HIL] / Software-in-the-Loop [SIL] configuration, and certification support) generated $11.85 million (€10.49 million), representing 78.4% of total revenue. Product sales, encompassing certified hardware modules, accounted for 21.6% at $3.27 million (€2.90 million), an 8.0% year-over-year contraction reflecting the industry's delayed transition from prototype development to serial manufacturing.

To execute this service-heavy mandate, Embention expanded its headcount from 160 to 242 employees, driving personnel expenses up 13.1% to $6.44 million (€5.70 million). Operating profit (EBIT) grew 8.8% to $6.81 million (€6.03 million), yielding a 45.0% operating margin. Adding back $0.77 million (€0.68 million) in depreciation and amortization generates an implied EBITDA proxy of $7.58 million (€6.71 million). Net income registered at $5.65 million (€5.00 million), a 4.6% expansion hampered by a higher effective tax rate of 17.7% (up from 14.5% in FY24) and $1.41 million (€1.25 million) in cash tax payments. Operating cash flow contracted from $7.79 million (€6.89 million) in FY24 to $6.25 million (€5.53 million) in FY25.

Capital Structure and Working Capital Metrics (1 EUR = 1.1306 USD)

* Total Liquidity: $13.81 million (€12.22 million), consisting of $2.39 million (€2.12 million) in cash/equivalents and $11.42 million (€10.10 million) in short-term financial investments.

* Accounts Receivable: Grew 40.8% to $3.07 million (€2.71 million). Direct trade invoices account for $2.03 million (€1.80 million), while non-operational receivables (public grants and VAT) comprise $1.02 million (€0.90 million).

* Accounts Payable: Surged 58.7% to $5.65 million (€5.00 million). This includes $387,262 (€342,528) in sundry payables and $13,968 (€12,355) owed to controlling entity Albedo Ventures, S.L.

* Zero-Cost Execution Buffer: Customer advance payments account for $4.24 million (€3.75 million) of total payables, providing immediate working capital but creating execution liabilities for pending development services.

* Financial Debt: Total debt stands at $3.96 million (€3.50 million), split between $2.44 million (€2.16 million) long-term and $1.52 million (€1.34 million) short-term.

* Soft Loans: Bank borrowings total $2.50 million (€2.21 million) backed by ICO and Afin SGR guarantees. These carry deeply suppressed interest rates: BBVA and Banco Sabadell (1.50%), Caja Rural (1.80%), and Banco Santander (2.84%).

* Public Subsidies: The balance sheet carries $1.40 million (€1.24 million) in conditionally repayable liabilities tied to R&D milestones, contrasted against $2.73 million (€2.41 million) in non-repayable equity grants.

* Capital Expenditure: Physical PP&E CapEx absorbed just $0.21 million (€0.19 million), while intangible R&D investments consumed $2.28 million (€2.02 million). Operating leases and external rents totaled $2.22 million (€1.97 million).

Infrastructure Layout and Regional Moats

Embention’s operational architecture is headquartered in Alicante, Spain. The primary facility houses high-value electronic manufacturing, climate chambers, vibration tables, and a private airfield dedicated to iron-bird testing. Since its inception in 2007 (originating from the Flamingo project), the firm has accumulated an 18-year operational track record, utilizing a strict capitalization policy where $2.07 million to $2.08 million (€1.84 million) of FY25 internal R&D was activated onto the balance sheet. This expands total intangible assets to $7.20 million (€6.37 million).

To secure raw inputs, the company procures components from over 270 global suppliers. The top supplier constitutes 19.7% of procurement ($533,000 / €471,384), and the second-largest accounts for 7.2%. Reacting to macroeconomic supply constraints, management executed a 972% expansion in physical inventory, growing stockpiles from $0.13 million–$0.14 million (€0.12 million) in FY24 to $1.43 million–$1.44 million (€1.27 million) in FY25. There are zero recorded provisions for environmental liabilities.

Geographic revenue is severely concentrated in the Americas, which generated 75.6% of FY25 sales ($11.44 million / €10.12 million). Europe accounts for 15.4% ($2.33 million / €2.06 million), with the Spanish domestic market providing merely 3% of product and 2% of service sales, while the broader EU drives 25% of product and 4% of service sales. Asia contributed 8.2% ($1.24 million / €1.10 million), with Oceania ($0.06 million / €0.05 million) and Africa ($0.05 million / €0.05 million) delivering sub-0.1% volumes. To localize production and diversify this geographic matrix, Embention established three new entities: Embention Avionics Components and System Manufacture LLC SPC (Abu Dhabi, UAE - 2025), Embention USA Inc (Los Angeles, USA - 2026), and Embention DACH GmbH (Austria).

The product suite encompasses the Veronte Autopilot ecosystem (1x, 4x, DRx, KAI), Vision Based Navigation (VBN), datalinks (SDL, XDL24), I/O expansion modules (CEx, MEx, Serial, Stick), DC-DC converters, motor inverters (MC110), gimbal controls (MC01), and control stations (LCS/PCS).

Commercial penetration is driven exclusively by aerospace regulatory lock-in. Embention is the first drone autopilot specialist to secure European Union Aviation Safety Agency (EASA) Alternative Procedures to Design Organisation Approval (APDOA) and Production Organisation Approval (POA). Its systems conform to DO-178C (ED-12) for software, DO-254 (ED-80) for hardware, and DO-160G for environmental conditions. Additionally, it achieved LufABw VVZ1/VVZ2 certification in Germany and ANAC approval in Brazil. This multi-year certification lag (historically requiring six years from 2007 to 2013) forms the ultimate barrier to entry against niche peers (UAV Navigation/Grupo Oesía, MicroPilot) and indirect Tier-1 integrators (Honeywell, Collins Aerospace/RTX, Thales, BAE Systems).

HDIN Institutional Verdict

While Embention demonstrates formidable gross profitability and an unlevered operational cash profile, its commercial dependency introduces acute vulnerability. Out of a historic base of over 600 clients across 70 countries (with more than 100 active billing customers in FY25), a single blue-chip entity generated 62.7% of total revenue ($9.48 million / €8.39 million). The top five customers cumulatively drive 76.0% of all sales.

The latent commercial pipeline relies on specific platform maturation milestones. Embention’s avionics are currently integrated into Amazon Prime Air (MK30 logistics program), Airbus (Skyways project), EDGE Group (defense collaboration), Lift Aircraft (Hexa eVTOL), EMT (LUNA NG tactical UAV), Israel Aerospace Industries (Air Hopper), Honda, Rheinmetall, and BAE Systems. Once these platforms secure regulatory approval and exit the trial phase, Embention projects a shift from one-off engineering billings to recurring serial product sales.

Corporate governance and capital structure mechanics expose minority shareholders to severe overhang risks. The ultimate beneficial owner, David Julián Benavente Sánchez, commands a 44.97% economic interest (0.44% direct, and 44.53% indirect via holding company Albedo Ventures, S.L., which retains 63.88% of Embention). Institutional backer Axon Innovation Growth IV, F.C.R. holds 29.02%. The company maintains 3.36% in treasury stock (201,018 shares), leaving a highly restricted minority float of 3.74%. Executive compensation remains minimal, with the Board of Directors receiving $79,932 (€70,699). Employee retention is managed via a stock option plan requiring five years of seniority, valued at $0.57 million (€0.51 million), with 11,133 shares delivered from treasury in FY25.

The transition to Euronext Growth Paris lacks institutional-grade safeguards, notably operating without independent audit or remuneration committees and enforcing zero post-listing lock-up agreements. Furthermore, latent dilution mechanisms are aggressive. Axon holds a $565,302 (€500,002) convertible loan yielding 3.5%, maturing in February 2026. This mandate forces the issuance of 57,871 new shares, representing 0.958% dilution at a pre-money valuation of $58.44 million (€51.69 million). Separately, active warrants held by Axon and a third-party commercial partner authorize the subscription of up to 2,560,000 new shares. If exercised, this will expand total share capital by 42.8%, diluting the base from 5,982,684 to 8,542,682 shares. Until these overhangs clear, equity upside remains heavily capped despite the firm's unassailable regulatory moats.

Presentation Download & Video Access:

- Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

- Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."