Holtec Nuclear Corporation: Multi-Billion Decommissioning Deconsolidation via DEAMCO Restructuring as 97.6% Long-Tail Backlog Signals Structural Transition to Merchant Generation Operations

Date : 2026-07-14

Reading : 197

HDIN Executive Takeaways

1. Severe Backlog Duration Asymmetry: Out of Holtec Nuclear Corporation’s [NASDAQ: HNC] $21.14 billion reported backlog, only 2.4% ($520.4 million) converts to revenue within the next 12 months, creating extreme near-term working capital dependencies ahead of its planned initial public offering.

2. Balance Sheet Risk Isolation: The transition to Phase II of the NAMCO Restructuring will deconsolidate $1.7 billion in Asset Retirement Obligations and $2.8 billion in Nuclear Decommissioning Trust assets, transferring volatile liabilities to DEAMCO while preserving steady-state service margins.

3. High-Concentration Supply Vulnerabilities: SMR-300 deployment is structurally dependent on single-source, exclusive supply agreements with Framatome and Mitsubishi Electric Corporation, exposing Holtec Nuclear Corporation's global pipeline to physical and geopolitical disruptions.

Figure Holtec Nuclear Corporation: Strategic Moats, Financial Architecture, and the SMR-300 Pipeline

Segmental Realities and Backlog Illiquidity

Segmental Realities and Backlog Illiquidity

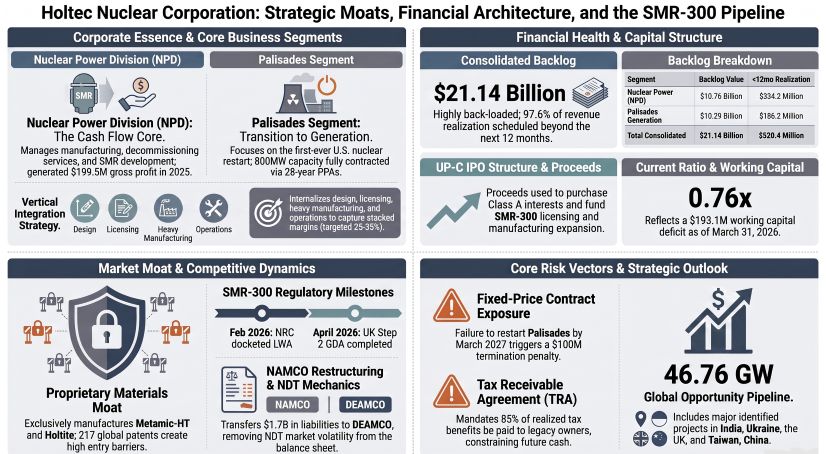

Holtec Nuclear Corporation operates under a bifurcated model consisting of two core segments: the legacy Nuclear Power Division (NPD) and the pre-operational Palisades generation asset.

In fiscal year 2025, NPD generated $576.6 million in total revenues, producing $199.5 million in gross operating profit and achieving a gross margin of 34.6%. The revenue mix of this segment was highly concentrated in Construction and Site Services at $529.0 million, followed by Engineering and Consulting Services at $24.5 million, and Decommissioning Site Services at $23.1 million. The decommissioning line contracted compared to previous periods due to the wind-down of active cleanup tasks at the Indian Point facility. Historically, NPD has yielded gross margins between 15% and 40% on engineering and equipment supply contracts.

Conversely, the Palisades segment—housing the 800 MWe Palisades Nuclear Power Plant—reported $0 in revenues and $0 in gross profit for 2025, reflecting its capital-intensive, pre-operational restart phase. Management is targeting a commercial restart in 2026, aiming for steady-state gross margins of 20% to 40% driven by long-term Power Purchase Agreements (PPAs).

As of December 31, 2025, the consolidated backlog of Holtec Nuclear Corporation stood at $21.14 billion. This backlog is characterized by high duration and limited near-term liquidity, with 97.6% ($20.62 billion) scheduled for realization beyond the next 12 months.

Upon completion of the pending NAMCO Restructuring, the company expects to add more than $2.4 billion to its service backlog via long-term decommissioning agreements with DEAMCO.

Long-Term Market Potential (TAM) Through 2050

* Total Addressable Enterprise TAM: $2.7 trillion to $3.4 trillion.

* Small Modular Reactor (SMR) Segment TAM: $2.3 trillion to $2.9 trillion (aligned with a projected 780 GW global capacity expansion).

* Nuclear Decommissioning Market TAM: ~$60 billion (driven by 81 GW of projected retirements globally, including ~6 GW in North America, with average costs ranging from $750/kW to $1,250/kW).

* Nuclear Services Market TAM: Current U.S. market is valued at ~$20 billion annually, with global fleet expansion projected to add $20 billion annually by 2050.

Infrastructure Layout and Regional Moats

Holtec Nuclear Corporation relies on three domestic advanced manufacturing facilities containing over 1 million square feet of combined production space to maintain its vertical integration:

* Holtec Manufacturing Division (HMD - Pennsylvania): A ~450,000 square foot facility featuring a 200-ton crane capacity. It focuses on the fabrication of heat exchangers, spent fuel storage units, and transport casks.

* Orrvilon Manufacturing Division (Ohio): A ~350,000 square foot facility with a 40-ton crane capacity, specializing in aluminum extrusion, friction stir welding, and proprietary alloy fabrication.

* Advanced Manufacturing Division (AMD - New Jersey): A ~370,000 square foot facility featuring a 400-ton double hoist crane, co-located with the Corporate Engineering Center. It utilizes advanced robotic welding and machining tools for SMR-300 components.

To support SMR-300 scale-up, Holtec Nuclear Corporation is executing a 75,000 square foot warehouse expansion at AMD, refurbishing its HMD facility, and planning a new Advanced Manufacturing Center (AMC) to add 450,000 square feet of heavy fabrication space and 100,000 square feet of warehousing.

Geographic Revenue and Asset Dispersion

* Revenues (2025): United States accounted for $389.7 million (67.6%); Rest of the World generated $187.0 million (32.4%).

* Long-Lived Assets (2025): $1.69 billion is located in the U.S.; $20.9 million is located internationally.

* Global Footprint: Currently services 73 international nuclear stations with dry storage systems. Operational hubs are maintained in the UK, Ukraine, Mexico, Spain, Brazil, and India.

* Taiwan, China: Awarded an international dry storage contract for a boiling water reactor (BWR) fleet using its HI-STORM UVH system.

The SMR-300 Pipeline and Supply Chain Architecture

The SMR-300 is a Generation III+ pressurized water reactor (PWR) producing 340 MWe net (680 MWe in standard dual-unit configurations). It has an initial 80-year design life, utilizes an 18-month refueling cycle, and is designed for a capacity factor exceeding 90%.

The global opportunity pipeline for the SMR-300 is 46.76 GW, split between 14.12 GW domestic and 32.64 GW international:

* United States (14.12 GW): Includes Palisades SMR Pioneer (680 MWe, targeted early 2030s, pre-construction, backed by a targeted $400 million DOE Tier 1 First Mover Award), Oyster Creek (1,280 MWe, target 2036), Indian Point (2,560 MWe), Pilgrim (1,280 MWe), Utah Green River (2,560 MWe), and Entergy Gulf South (640 MWe under MOU).

* Ukraine (6.40 GW): 10 dual-units under development with Energoatom. Operations are exposed to the regional war, and the company is in a $55.6 million ICC arbitration dispute with ChNPP regarding project delays.

* India (9.60 GW): 15 dual-units under MOU, leveraging engineering support from Holtec Asia (Gujarat, India).

* Rwanda (5.12 GW): 8 dual-units planned via the Rwanda Atomic Energy Board (RAEB).

* United Kingdom: 2 dual-units (1,280 MWe) at Cottam under MOU with EDF Energy and Tritax. The SMR-300 completed Step 2 of the Generic Design Assessment (GDA) in April 2026, supported by a GBP 34.5 million cost-share grant from the UK Government.

* Other Markets: 1 dual-unit (640 MWe) each in Hungary and Taiwan, China; plus pipeline interest in Brazil (1,280 MWe) and Sweden (1,280 MWe).

Decommissioning Asset Realignment and Trust Accounting

Holtec Nuclear Corporation has historically operated an "acquire and decommission" strategy, taking over retired stations, their licenses, and Nuclear Decommissioning Trust (NDT) funds. The legacy decommissioning portfolio includes:

* Oyster Creek (NJ): 700-acre site, 637 MW, acquired July 2019.

* Pilgrim (MA): 1,500-acre site, acquired August 2019.

* Indian Point (NY): 240-acre site, acquired May 2021.

* Big Rock Point (MI): Acquired June 2022 (only used fuel remains on-site).

* Palisades (MI): Acquired June 2022 (currently excluded from decommissioning and transitioning to restart).

The NAMCO Restructuring Framework

Under Phase I, Holtec Nuclear Corporation transferred ownership of Oyster Creek, Pilgrim, Indian Point, and Big Rock Point to DEAMCO (a subsidiary of founder-controlled Holtec Holdings). Upon receiving NRC license transfer approvals in Phase II, Holtec Nuclear Corporation will fully deconsolidate these assets, removing $1.7 billion in Asset Retirement Obligations (AROs) and $2.8 billion in NDT assets from its balance sheet. Decommissioning services will transition to a lower-risk, fee-based service model managed by Holtec Decommissioning International (HDI) on arm's-length commercial terms.

Trust Fund and Receivables Status

As of March 31, 2026, the company's historical consolidated balance sheet carried $2.80 billion in NDT assets against $1.71 billion in calculated AROs, applying a conservative 2% real rate of return model on trust assets. NDT earnings are taxed at a 20% federal rate.

Additionally, due to the federal government's delay in creating a permanent geologic waste repository, Holtec Nuclear Corporation records long-term receivables for spent nuclear fuel (SNF) management from the DOE. As of March 31, 2026, gross DOE receivables were $1.07 billion, offset by a $428.3 million allowance for cost adjustments, resulting in a net receivable of $645.0 million.

Regulatory and State Settlement Guardrails

State-level agreements dictate strict minimum NDT balances to prevent premature fund depletion before Partial Site Release:

* Massachusetts (Pilgrim): Must maintain a minimum balance of $193.3 million (in 2019 dollars) until Partial Site Release is achieved, and $38.4 million (in 2021 dollars) thereafter.

* New York (Indian Point): Must maintain a minimum balance of $400.0 million for 10 years post-closing, and $360.0 million until Partial Site Release. The company posted a $110.6 million surety bond to the state. Furthermore, state mandates require that 50% of any DOE litigation recoveries be redeposited into a new NDT subaccount to fund long-term on-site dry storage.

HDIN Institutional Verdict: Capital Allocation and Governance Friction

While Holtec Nuclear Corporation holds a dominant legacy market share—controlling over 90% of the U.S. wet spent fuel storage market, approximately 75% of the dry spent fuel storage market, and loading 149 dry systems in 2025 compared to 53 for its competitors combined—its corporate structure presents material friction for public market investors:

* Dual-Class Control Concentration: The founder-controlled Holtec Holdings, led by Ph.D. founder Dr. Krishna P. Singh (79), holds Class B common stock carrying 10 votes per share. This structure concentrates voting control within the founder's entity. The high-voting power only sunsets to 1 vote per share if ownership drops below 20% of outstanding Class B shares.

* Structured Cash Extraction (TRA): The Umbrella Partnership C Corporation (UP-C) structure binds the public company to a Tax Receivable Agreement (TRA) requiring it to pay 85% of all realized tax benefits directly to legacy owners, reducing long-term retained cash flow. Early termination or change-of-control events will trigger immediate, accelerated cash payouts.

* Executive Compensation and Related-Party Exposure: Executive compensation remains entirely cash-based prior to the IPO, with Dr. Krishna Singh receiving $7.53 million in total compensation in 2025 (including $1.8 million in company-funded services to his family office). Post-IPO, the firm is transitioning to equity-based compensation with a $39 million RSU pool vesting over three years.

* Project Execution Covenants: The Palisades restart is funded by a $1.52 billion DOE Loan Guarantee Agreement (LGA) which carries strict covenants on debt service and dividend limits. Missing the March 2027 in-service deadline triggers a $100 million PPA termination penalty.

* Commodity Inflation Exposure: Due to fixed-price EPC structures, a uniform 10% increase in commodity input prices is estimated to generate $2.9 million in unrecovered costs based on 2025 metrics. This risk is particularly concentrated at the Orrvilon facility, which relies on a specialized aluminum compound sourced from a limited vendor base.

The board has established a majority-independent structure (four out of six independent nominees, including Susan N. Story (66) and Michael W. Rencheck (64) as chair of the newly created Nuclear Oversight Committee), which provides specialized operational oversight. However, the concurrent creation of the Executive Oversight Committee—initially consisting of Dr. Singh, Vice Chairman Martha Singh, and a lead independent director—retains broad executive authority within the founder's family office, presenting a corporate governance dynamic that warrants a cautious valuation multiple at IPO.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. Severe Backlog Duration Asymmetry: Out of Holtec Nuclear Corporation’s [NASDAQ: HNC] $21.14 billion reported backlog, only 2.4% ($520.4 million) converts to revenue within the next 12 months, creating extreme near-term working capital dependencies ahead of its planned initial public offering.

2. Balance Sheet Risk Isolation: The transition to Phase II of the NAMCO Restructuring will deconsolidate $1.7 billion in Asset Retirement Obligations and $2.8 billion in Nuclear Decommissioning Trust assets, transferring volatile liabilities to DEAMCO while preserving steady-state service margins.

3. High-Concentration Supply Vulnerabilities: SMR-300 deployment is structurally dependent on single-source, exclusive supply agreements with Framatome and Mitsubishi Electric Corporation, exposing Holtec Nuclear Corporation's global pipeline to physical and geopolitical disruptions.

Figure Holtec Nuclear Corporation: Strategic Moats, Financial Architecture, and the SMR-300 Pipeline

Segmental Realities and Backlog IlliquidityHoltec Nuclear Corporation operates under a bifurcated model consisting of two core segments: the legacy Nuclear Power Division (NPD) and the pre-operational Palisades generation asset.

In fiscal year 2025, NPD generated $576.6 million in total revenues, producing $199.5 million in gross operating profit and achieving a gross margin of 34.6%. The revenue mix of this segment was highly concentrated in Construction and Site Services at $529.0 million, followed by Engineering and Consulting Services at $24.5 million, and Decommissioning Site Services at $23.1 million. The decommissioning line contracted compared to previous periods due to the wind-down of active cleanup tasks at the Indian Point facility. Historically, NPD has yielded gross margins between 15% and 40% on engineering and equipment supply contracts.

Conversely, the Palisades segment—housing the 800 MWe Palisades Nuclear Power Plant—reported $0 in revenues and $0 in gross profit for 2025, reflecting its capital-intensive, pre-operational restart phase. Management is targeting a commercial restart in 2026, aiming for steady-state gross margins of 20% to 40% driven by long-term Power Purchase Agreements (PPAs).

As of December 31, 2025, the consolidated backlog of Holtec Nuclear Corporation stood at $21.14 billion. This backlog is characterized by high duration and limited near-term liquidity, with 97.6% ($20.62 billion) scheduled for realization beyond the next 12 months.

Table 1: Segment Revenue, Profitability & Backlog Profile (FY2025)

| Segment / Metric | FY2025 Revenue (USD M) | FY2025 Gross Profit (USD M) | FY2025 Gross Margin | Total Backlog (USD B) | Executable Backlog (<12 Months) (USD M) | Long-Tail Backlog (>12 Months) (USD B) |

|---|---|---|---|---|---|---|

| Nuclear Power Division (NPD) | $576.6 | $199.5 | 34.6% | $10.76B | $334.2M | $10.43B |

| Palisades Segment | $0.0 | $0.0 | 0.0% | $10.39B | $186.2M | $10.20B |

| Consolidated Total | $576.6 | $199.5 | 34.6% | $21.14B | $520.4M | $20.62B |

Upon completion of the pending NAMCO Restructuring, the company expects to add more than $2.4 billion to its service backlog via long-term decommissioning agreements with DEAMCO.

Long-Term Market Potential (TAM) Through 2050

* Total Addressable Enterprise TAM: $2.7 trillion to $3.4 trillion.

* Small Modular Reactor (SMR) Segment TAM: $2.3 trillion to $2.9 trillion (aligned with a projected 780 GW global capacity expansion).

* Nuclear Decommissioning Market TAM: ~$60 billion (driven by 81 GW of projected retirements globally, including ~6 GW in North America, with average costs ranging from $750/kW to $1,250/kW).

* Nuclear Services Market TAM: Current U.S. market is valued at ~$20 billion annually, with global fleet expansion projected to add $20 billion annually by 2050.

Infrastructure Layout and Regional Moats

Holtec Nuclear Corporation relies on three domestic advanced manufacturing facilities containing over 1 million square feet of combined production space to maintain its vertical integration:

* Holtec Manufacturing Division (HMD - Pennsylvania): A ~450,000 square foot facility featuring a 200-ton crane capacity. It focuses on the fabrication of heat exchangers, spent fuel storage units, and transport casks.

* Orrvilon Manufacturing Division (Ohio): A ~350,000 square foot facility with a 40-ton crane capacity, specializing in aluminum extrusion, friction stir welding, and proprietary alloy fabrication.

* Advanced Manufacturing Division (AMD - New Jersey): A ~370,000 square foot facility featuring a 400-ton double hoist crane, co-located with the Corporate Engineering Center. It utilizes advanced robotic welding and machining tools for SMR-300 components.

To support SMR-300 scale-up, Holtec Nuclear Corporation is executing a 75,000 square foot warehouse expansion at AMD, refurbishing its HMD facility, and planning a new Advanced Manufacturing Center (AMC) to add 450,000 square feet of heavy fabrication space and 100,000 square feet of warehousing.

Geographic Revenue and Asset Dispersion

* Revenues (2025): United States accounted for $389.7 million (67.6%); Rest of the World generated $187.0 million (32.4%).

* Long-Lived Assets (2025): $1.69 billion is located in the U.S.; $20.9 million is located internationally.

* Global Footprint: Currently services 73 international nuclear stations with dry storage systems. Operational hubs are maintained in the UK, Ukraine, Mexico, Spain, Brazil, and India.

* Taiwan, China: Awarded an international dry storage contract for a boiling water reactor (BWR) fleet using its HI-STORM UVH system.

The SMR-300 Pipeline and Supply Chain Architecture

The SMR-300 is a Generation III+ pressurized water reactor (PWR) producing 340 MWe net (680 MWe in standard dual-unit configurations). It has an initial 80-year design life, utilizes an 18-month refueling cycle, and is designed for a capacity factor exceeding 90%.

The global opportunity pipeline for the SMR-300 is 46.76 GW, split between 14.12 GW domestic and 32.64 GW international:

* United States (14.12 GW): Includes Palisades SMR Pioneer (680 MWe, targeted early 2030s, pre-construction, backed by a targeted $400 million DOE Tier 1 First Mover Award), Oyster Creek (1,280 MWe, target 2036), Indian Point (2,560 MWe), Pilgrim (1,280 MWe), Utah Green River (2,560 MWe), and Entergy Gulf South (640 MWe under MOU).

* Ukraine (6.40 GW): 10 dual-units under development with Energoatom. Operations are exposed to the regional war, and the company is in a $55.6 million ICC arbitration dispute with ChNPP regarding project delays.

* India (9.60 GW): 15 dual-units under MOU, leveraging engineering support from Holtec Asia (Gujarat, India).

* Rwanda (5.12 GW): 8 dual-units planned via the Rwanda Atomic Energy Board (RAEB).

* United Kingdom: 2 dual-units (1,280 MWe) at Cottam under MOU with EDF Energy and Tritax. The SMR-300 completed Step 2 of the Generic Design Assessment (GDA) in April 2026, supported by a GBP 34.5 million cost-share grant from the UK Government.

* Other Markets: 1 dual-unit (640 MWe) each in Hungary and Taiwan, China; plus pipeline interest in Brazil (1,280 MWe) and Sweden (1,280 MWe).

Decommissioning Asset Realignment and Trust Accounting

Holtec Nuclear Corporation has historically operated an "acquire and decommission" strategy, taking over retired stations, their licenses, and Nuclear Decommissioning Trust (NDT) funds. The legacy decommissioning portfolio includes:

* Oyster Creek (NJ): 700-acre site, 637 MW, acquired July 2019.

* Pilgrim (MA): 1,500-acre site, acquired August 2019.

* Indian Point (NY): 240-acre site, acquired May 2021.

* Big Rock Point (MI): Acquired June 2022 (only used fuel remains on-site).

* Palisades (MI): Acquired June 2022 (currently excluded from decommissioning and transitioning to restart).

The NAMCO Restructuring Framework

Under Phase I, Holtec Nuclear Corporation transferred ownership of Oyster Creek, Pilgrim, Indian Point, and Big Rock Point to DEAMCO (a subsidiary of founder-controlled Holtec Holdings). Upon receiving NRC license transfer approvals in Phase II, Holtec Nuclear Corporation will fully deconsolidate these assets, removing $1.7 billion in Asset Retirement Obligations (AROs) and $2.8 billion in NDT assets from its balance sheet. Decommissioning services will transition to a lower-risk, fee-based service model managed by Holtec Decommissioning International (HDI) on arm's-length commercial terms.

Trust Fund and Receivables Status

As of March 31, 2026, the company's historical consolidated balance sheet carried $2.80 billion in NDT assets against $1.71 billion in calculated AROs, applying a conservative 2% real rate of return model on trust assets. NDT earnings are taxed at a 20% federal rate.

Additionally, due to the federal government's delay in creating a permanent geologic waste repository, Holtec Nuclear Corporation records long-term receivables for spent nuclear fuel (SNF) management from the DOE. As of March 31, 2026, gross DOE receivables were $1.07 billion, offset by a $428.3 million allowance for cost adjustments, resulting in a net receivable of $645.0 million.

Regulatory and State Settlement Guardrails

State-level agreements dictate strict minimum NDT balances to prevent premature fund depletion before Partial Site Release:

* Massachusetts (Pilgrim): Must maintain a minimum balance of $193.3 million (in 2019 dollars) until Partial Site Release is achieved, and $38.4 million (in 2021 dollars) thereafter.

* New York (Indian Point): Must maintain a minimum balance of $400.0 million for 10 years post-closing, and $360.0 million until Partial Site Release. The company posted a $110.6 million surety bond to the state. Furthermore, state mandates require that 50% of any DOE litigation recoveries be redeposited into a new NDT subaccount to fund long-term on-site dry storage.

HDIN Institutional Verdict: Capital Allocation and Governance Friction

While Holtec Nuclear Corporation holds a dominant legacy market share—controlling over 90% of the U.S. wet spent fuel storage market, approximately 75% of the dry spent fuel storage market, and loading 149 dry systems in 2025 compared to 53 for its competitors combined—its corporate structure presents material friction for public market investors:

* Dual-Class Control Concentration: The founder-controlled Holtec Holdings, led by Ph.D. founder Dr. Krishna P. Singh (79), holds Class B common stock carrying 10 votes per share. This structure concentrates voting control within the founder's entity. The high-voting power only sunsets to 1 vote per share if ownership drops below 20% of outstanding Class B shares.

* Structured Cash Extraction (TRA): The Umbrella Partnership C Corporation (UP-C) structure binds the public company to a Tax Receivable Agreement (TRA) requiring it to pay 85% of all realized tax benefits directly to legacy owners, reducing long-term retained cash flow. Early termination or change-of-control events will trigger immediate, accelerated cash payouts.

* Executive Compensation and Related-Party Exposure: Executive compensation remains entirely cash-based prior to the IPO, with Dr. Krishna Singh receiving $7.53 million in total compensation in 2025 (including $1.8 million in company-funded services to his family office). Post-IPO, the firm is transitioning to equity-based compensation with a $39 million RSU pool vesting over three years.

* Project Execution Covenants: The Palisades restart is funded by a $1.52 billion DOE Loan Guarantee Agreement (LGA) which carries strict covenants on debt service and dividend limits. Missing the March 2027 in-service deadline triggers a $100 million PPA termination penalty.

* Commodity Inflation Exposure: Due to fixed-price EPC structures, a uniform 10% increase in commodity input prices is estimated to generate $2.9 million in unrecovered costs based on 2025 metrics. This risk is particularly concentrated at the Orrvilon facility, which relies on a specialized aluminum compound sourced from a limited vendor base.

The board has established a majority-independent structure (four out of six independent nominees, including Susan N. Story (66) and Michael W. Rencheck (64) as chair of the newly created Nuclear Oversight Committee), which provides specialized operational oversight. However, the concurrent creation of the Executive Oversight Committee—initially consisting of Dr. Singh, Vice Chairman Martha Singh, and a lead independent director—retains broad executive authority within the founder's family office, presenting a corporate governance dynamic that warrants a cautious valuation multiple at IPO.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."